BSMP - Positive Muni Returns Are Not A Sure Thing. A Look At The Risks For 2024

2023-11-24 07:35:15 ET

Summary

- Munis have become more attractive as an investment opportunity due to weaker inflation readings and expectations for Fed rate cuts in 2024.

- Munis continue to be my preferred area of choice for fixed-income. And there is a path for them to move higher next year.

- Risks include the possibility of a rebound in inflation, declining tax receipts, and the fact that the market has already shown strong interest in munis.

Main Thesis/Background

The purpose of this article is to discuss the municipal ((muni)) bond sector and how attractive it is as an investment opportunity at the moment. This is an area that I regularly review for optimal entry points - which were generally lacking in 2023! However, over the past month munis and fixed-income as a whole have gotten a nice boost from weaker inflation readings and the expectations for Fed rate cuts in 2024. This has led me to consider whether a buy case for munis is truly the right call as we wrap up the year.

On the surface, munis do look attractive to me. The yields are historically high and buying in after a negative year is typically a smart move. History shows us that back-to-back declines in the muni bond sector are not the norm. Further, the tailwinds of strong revenue growth for cities and states, high cash reserves or "rainy day" funds, and billions in pandemic stimulus remain supportive of strong credit rating for most muni debt.

However, readers should be mindful that risks are present too. Understanding and evaluating these risks is important before deciding whether or not this sector is right for you - in terms of whether now is a good time to add to a position or initiate a new one. In this review, I will tackle some of the pros and cons of buying in now as I see them, to help readers gauge whether this truly is a buying opportunity for the sector.

Interest Rate Outlook, Cooling Economies Are Tailwinds

To begin, I want to take some time to focus on the reasons why investors may be wanting muni exposure right now. As my followers know, this is my preferred sector for fixed income - and I am often a muni bull. This outlook does ebb and flow based on macroeconomic conditions, but long term I have generally preferred it over corporate debt and treasuries. Further, while there are always risks present in the sector, these risks are often balanced with positive attributes as well. So a balanced review is appropriate here as usual.

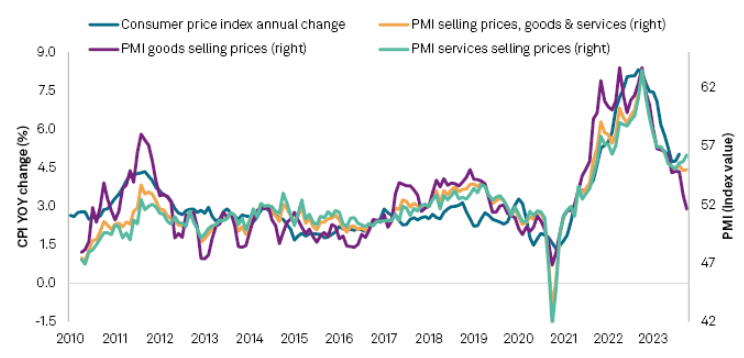

So what are some of the tailwinds for munis right now? Most of these tailwinds are applicable to bonds as a whole. These are absolutely relevant for munis too, but readers should understand that many of the reasons for the recent uptick in muni prices are the same forces that have been driving other debt sectors higher too. In particular, we have seen a cooling of inflation - both here in the US and globally. This is evidenced by drops in CPI figures and by a decline in global PMI figures (a common measure of expected future economic activity):

Global CPI and PMI Metrics (S&P Global)

{kind=link}

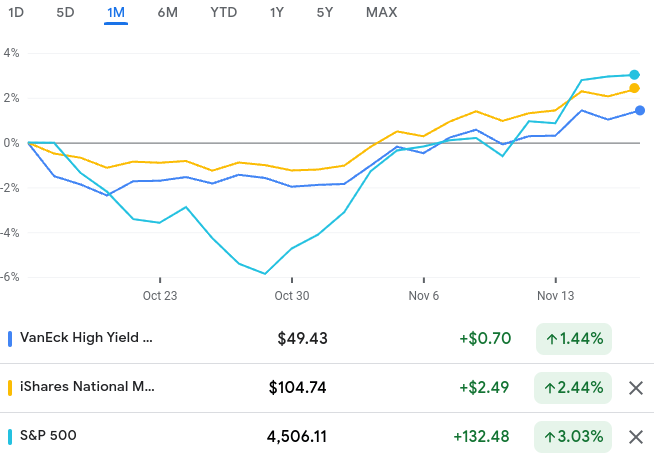

As you can see, the global economy appears to be coming off its "sugar high". This may not be the best economic news - it depends on your perspective - but it has been a bullish signal for bonds. This has led to an upward push in munis (both IG-rated and junk-rated) as well as equities over the past month:

1-Month Performance (Munis and Equities) (Google Finance)

{kind=link}

This is certainly a welcome move for bond bulls who have been hit fairly hard this year. The good news for those investors is that the reason behind the move is interest rate expectations - and that outlook is getting more dovish by the day. Whether this is truly warranted is a subjective debate at this point, but there is no denying the market has started to price in rate cuts:

Fed Funds Rate (Implied) (Bloomberg)

The net result has been that the "higher for longer" mantra has been replaced by the optimism of potential rate cuts in 2024. Time will tell whether this outlook will materialize into reality, but for now, it means investors are content to scoop up bonds to lock in above-average yields. This is an ongoing tailwind for fixed-income across the board - benefiting munis along with it.

Bonds Took A Beating In '23 - If Fed Hawks Prevail, Watch Out

As the prior paragraph shows, there are reasons to start building on to muni positions now and into 2024. But this isn't meant to suggest there are not any risks. After the sector's performance in 2023, all investors should be especially mindful of the risks. Yes, munis are a relatively "safe" sector compared to equities and even other debt areas. But that doesn't mean gains are automatic and losses can certainly pile up.

We don't have to look too far back to understand the truth of this. Both state and local muni bonds have posted negative returns over the past twelve months, albeit they are offering higher income than investors are used to:

Muni Bond Performance Since 12/22 - State and Local Bonds (Yahoo Finance)

{kind=link}

What I am trying to convey here is that there are market environments where munis will perform relatively poorly. The current year is an example of that and it stems mostly from stubborn inflation readings and a persistent rate hiking campaign from the Federal Reserve.

Now, those two factors are starting to diminish - leading to the uptick in bond prices. But I would emphasize that market expectations and reality are two different things. Many market participants got inflation and Fed action wrong this year - and it is very possible their outlooks for 2024 are off the mark. This poses a longer-term risk for this sector. In the short term, investor sentiment on a more dovish Fed is likely to give munis a sizable boost. I welcome this move. But as we shift to 2024, if the Fed disappoints (in terms of keeping rates higher or even continuing to hike) then we will likely see a sharp correction in the bond market. This is something to be keenly aware of and suggests investors would be wise to add selectively and perhaps even take short-term wins when they present themselves.

Tax Collections Dropping A Bit

Another factor that is raising some eyebrows is tax collections. In fairness, tax receipts are strong across the country for the most part on a wide historical lens. This is due to inflation (as prices rise, so do sales taxes, leading to higher receipts), strong employment numbers (more people working, more people paying taxes), and rising home values which give a boost to property tax collections. This is all good news and is generally supportive of the muni market, especially in the General Obligation ((GO)) space.

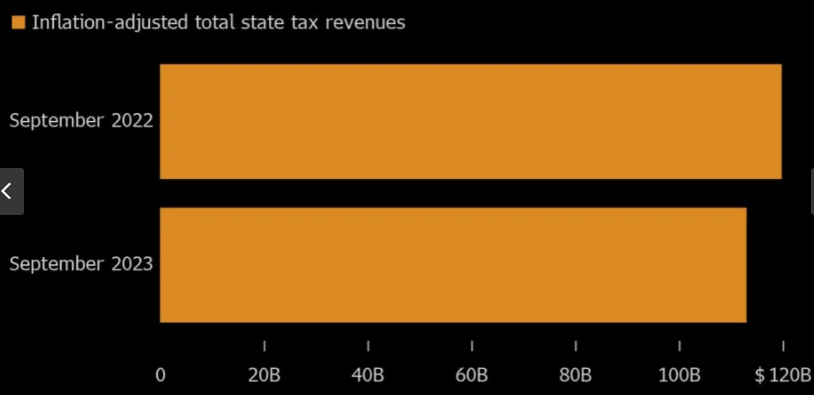

However, I would note that tax revenues, on an inflation-adjusted basis, are down from a year ago. Again, they are still high based on prior years and decades, but the year-over-year comparison does show some weakness:

State Tax Revenues (Aggregate) (Bloomberg)

{kind=link}

The bigger headwind is that the reasons for this drop are valid. There is not just one factor, but many. These include slowing economic growth, recent tax cuts, and poor stock market performance which result in less tax money coming in.

Again, this is not meant to be alarmist. Revenues are still pretty healthy and rainy-day funds are, on average, above historical norms. This will limit - and perhaps prevent altogether - the need for any immediate cuts in many municipalities. But the bottom line is that change has come and investors need to be aware of this. Cities and states across the country are going to have to make some tougher decisions in the years to come. As muni investors, we will need to keep a close eye on this going forward.

Not An "Under The Radar" Move

My final point touches on the fact that buying munis right now is not a contrarian play. This is a well-thought-out investment proposition that many analysts and TV talking heads have been pushing for a while. While it can sometimes be good to follow the herd, we generally find "alpha" when we find hidden gems or buying-in to panic-selling. That could have worked out with munis over the past month or so but, going forward, this is definitely a sector that has been getting a lot of attention. That can limit future returns.

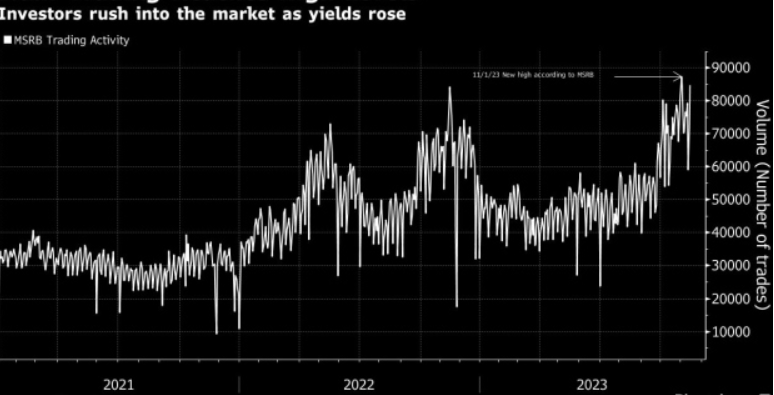

To illustrate, let us look at sector trading activity. In what was a fairly boring space for 2022 and most of 2023, munis have seen a rush of interest. As yields in the sector rose, coupled with a more dovish outlook for inflation and Fed action, traders have been surging into the sector. Average daily trading volume has shot up recently, with no sign of slowing down:

Muni Sector Trading Activity (Bloomberg)

{kind=link}

This is somewhat of a positive sign - certainly for current holders of muni debt. It means the market is warming back up to this idea and helping drive up prices in the short term. For those who got in over the past month, this has led to gains. For those nursing losses, it is helping take the string off a bit. If the trend stays intact, then good days lie ahead.

But the opposite argument should be considered. Investors have been rushing into this sector and it might be too far, too fast. As I said, I prefer sector investing - whether muni or otherwise - when the herd mentality is against it. This is far from the case for the time being. If we buy in now we are following the herd, and that can often mean mediocre returns as a result. Keep this in mind when deciding how to position yourself in the months ahead.

Bottom-line

Munis have had a welcome reprieve and I certainly am glad to see a broader fixed-income rebound. A cooling of inflation, an outlook for a more dovish Fed, and historically high yields are all working in munis favor. That is the good news as we bring 2023 to an end.

While those positive features do exist, we should also note the risks. Always be skeptical when anyone presents any investment thesis - whether for a stock, fund, or sector - and advises it will "soar" or can "only go up". That is never the case. There are always risks to any idea and, with respect to munis, that includes this sector. Munis have a few headwinds, including a decline in tax receipts for states and municipalities, the possibility of a rebound in inflation (which would shift sentiment on the Fed's next moves), and the fact that the market has already warmed up to this idea and has been buying feverishly. That demand is good for the short-term but may result in longer-term weakness if it doesn't keep up.

In the end, there is a lot to consider. While I will remain long munis and see the merits to owning them as we enter 2024, I wanted this review to demonstrate this is not a risk-free arena and that readers should perform careful due diligence before buying in if they choose to.

For further details see:

Positive Muni Returns Are Not A Sure Thing. A Look At The Risks For 2024