HOLI - Potential Turnaround Stories: Hollysys Is A Buy Whether Buyout Or Not

2023-09-11 09:00:59 ET

Summary

- Hollysys, a company that has experienced stagnant performance, has undergone a leadership shakeup with the return of founder Changli Wang as CEO.

- In his first year back, Wang has driven large sales growth. However, this has been at the expense of decreased operating margins.

- Despite the reprioritization towards growth, Hollysys has strong profitability in its operations and continues to be a turnaround story.

- Even if the board does not accept the 26% premium, Hollysys is likely to see share price appreciation due to its strong business performance.

Introduction

In this new series "Potential Turnaround Stories", I will be searching for a variety of companies that have been through tough times but have a high probability of a "turnaround". This encompasses companies with a list of opportunities:

- Undercovered securities

- M&A targets

- Historically poorly managed firms with new leadership

- Firms with a quick turnaround in operations

If you have any suggestions for opportunities within this list, let me know in the comments!

For this analysis, I will be diving into an opportunity that is characterized by three of the above categories. Hollysys ( HOLI ) experienced a leadership shakeup in January 2022 when the company's founder Changli Wang was invited by the board to lead the company again after eight years of absence ( Letter to Investors ). This leadership change is set against the backdrop of relatively stagnant performance between 2014 and 2020. Furthermore, since the leadership change, Hollysys has been solicited with buyout inquiries on several occasions - all of which have been declined by the board. Shareholders are getting fed up with the lack of communication from management and have recently requested a special meeting to vote on adding six new members to the board of the company ( Hollysys Press Release ). For this turnaround story, I will be going through each of these components in more detail.

The New CEO: Changli Wang

On January 24th Changli Wang sent a letter to investors expressing his priority for Hollysys going forward. He set out three top priorities: reunite the invaluable employees and rekindle their working aspirations, examine each business unit to optimize them and seek growth opportunities, and restore the confidence of Hollysys' investors. Wang published an aspiring text which is such in the spirit of this series that I must quote it here:

"I believe that my time away from Hollysys has given me perspective and that I will be able to revitalize the company and its growth. When Steve Jobs returned to his post as chief executive officer of Apple in 1997, he led one of the most remarkable business turnarounds in history and led a transformation that resulted in Apple becoming the most valuable company in the world. While I have no illusions of Hollysys becoming the most valuable company in the world, I hope to be able to use the example Steve Jobs set to lead our own turnaround and increase shareholder value. Based on discussions with board members as well as many colleagues, I believe that it is in the best interest of shareholders to focus on strengthening and optimizing the business operations of the Company rather than considering a sale at present."

Wang founded, now a subsidiary, Beijing HollySys in 1993. In 1999, he began serving this subsidiary as the CEO and vice chairman. Later, in 2007 he was appointed as CEO and Chairman of the Hollysys Group until he retired from the company in 2013 ( Hollysys Press Release Jan 3rd, 2022 ). His turnaround message is inspiring and since taking over again as CEO, he has delivered on his promise.

Financial Performance

Historical Performance

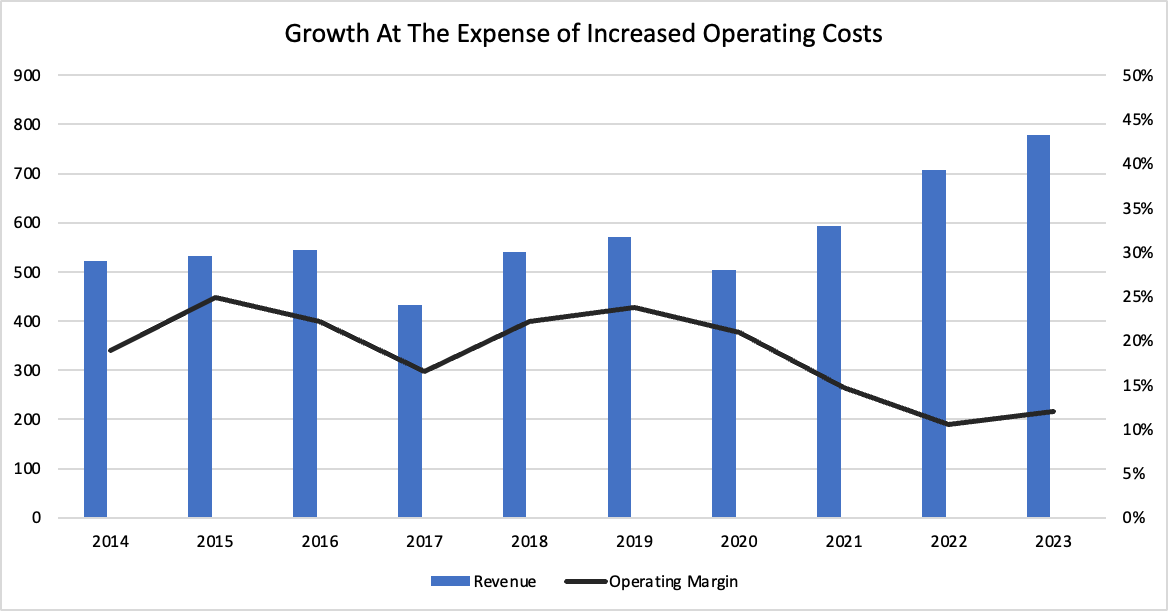

As shown in the chart below, Hollysys experienced rapid revenue growth from 2009 to 2014 where revenue more than fourdoubled. However, from 2014 to 2020 revenue stagnated at around $500 million annually.

While this period was a time of stagnation, it was also a time in which operating margins were being optimized. Once the company began prioritizing for growth again, operating margins decreased significantly. As shown in the image below, operating margins peaked at around 25% in 2015, decreased to 17% in 2017, and most recently declined sharply to around 12% in the latest year.

{kind=link}

Although this is not favorable to investors in the short term, picking up the growth initiative is positive for long-term shareholders. Changli Wang did not promise to "optimize operating margins" but rather to "seek growth opportunities". This is evidently reflected in the company's financial performance and will likely continue to be the case going forward. In the most recent annual filing, the company offered one piece of forward guidance: 10-20% revenue growth ( Seeking Alpha Press Release ). Hence, it is evident that growth is the only current priority.

Profitability

When calculating profitability, I want to analyze the return that Hollysys achieves from its operations based on the amount of net operating assets the company has. Furthermore, in the analysis, I will use the company's return on net operating assets ("RNOA"), net financial assets to equity ("NFA/E"), and return on net financial assets ("RNFA") to calculate the company's return on equity ("ROE").

Return on Net Operating Assets

Hollysys has total operating assets at year-end 2022 worth $977.8 million, which primarily comprise accounts receivable ($317 million), estimated earnings from excess billings in projects ($232 million), "PPE" ($98.2 million), inventory ($91 million), and investments in equity investees ($46.5 million). The company also has a large amount of financial assets - cash and cash equivalents plus short-term investments worth $692 million.

To find the amount of net operating assets, we must subtract the firm's operating liabilities from its operating assets. Hollysys has a total of $488 million, of which, the majority is comprised of accounts payable ($176 million) and deferred revenue or cash paid for services that have not yet been carried out ($206 million). In sum, Hollysys has a net operating asset position of $487.5 million.

The Author

Next, I find that Hollysys achieved an operating income of $97.9 million after tax for the full year ending in 2023. In order to come to this conclusion, I have started with the firm's comprehensive income before tax, subtracted its net interest earned (since it is not an operating income), subtracted the reported tax expense, and added back the tax expense that Hollysys incurred on its net interest income of $11.4 million. In this case, I assume that the company is taxed at a rate of 20% on interest income.

The Author

Using the company's operating income from the year-end and its opening balance of net operating assets, I find that Hollysys earned a return on net operating assets of 22.43%.

| OI |

| $97 859 |

| NOA |

| $487 581 |

| RNOA |

| 20.07% |

In my opinion, this is a good rate of return. Although the firm's operating margins have been decreasing, some profitability is made up for with other comprehensive income such as "forex" gains, other income, and share of net income in equity investees. Furthermore, the firm has a large amount of operating liability leverage of 1, which is calculated by dividing its "OL" by its "NOA". This means that the firm leverages supplier credit in order to finance its operations. It does this by asking for cash upfront for projects and by paying suppliers later than receiving its goods. This profitability measure provides a much more relevant picture of Hollysys' profitability on its core business when comparing it with its "ROE" which we will look through below.

Return on Equity

Return on equity can be calculated indirectly using the following formula:

"ROE" = RNOA - [NFA/E * (RNOA - RNFA)]

In other words, the return on equity for Hollysys is equal to its return on net operating assets, less its net financial assets over equity multiplied by the spread between its return on operating assets and return on financial assets. Hollysys has the following financial metrics that we can plug into the formula to receive a return on equity of 9.2%:

| NFA |

| $676 247 |

| E |

| $1 163 828 |

| RNFA |

| 1.36% |

| "ROE"= |

| 9.20% |

Essentially, this formula tells us that the large cash hoard that the company is sitting on is driving down its "ROE". It's being driven down by its high net financial position (since the company has almost no borrowings) and by the relatively low amount of interest that the company is earning on these assets (1.36%). In all, the company's "ROE" paints a vastly different picture of profitability compared with the company's "RNOA".

Takeover Offering

Hollysys has recently received a takeover bid from the same consortium - led by Recco Control Technology Pet and Dazheng Group Investment - for a price of $25/share ( Seeking Alpha News ). However, in September 2022, Hollysys also received an offer for $29/share from the Beijing municipal government, which represented a much larger upside than the consortium's proposal ( Seeking Alpha News ). In all, I would describe Hollysys' past two years as a rollercoaster ride of excitement and pain. Management has decided to turn down one offer after the other for the sake of reinvigorating the company and increasing shareholder value. Whether declining these offers has actually served to increase shareholder value, though, is highly questionable. Hollysys stock is currently trading for a price of $19.80 per share, which is $10 less than the bid it received most recently.

As we can see from the stock price chart, Hollysys stock has literally speaking been a rollercoaster during the past three years. Each offer has caused the share price to rise dramatically but never to the offer price, and fall just as dramatically as the signs of a deal have waned off. Currently, Hollysys has an implied upside if it accepts the following deal of 26.2% which would be a fine upside for a short-term investor willing to bet on a buyout.

How To Capitalize On The Turnaround

From my own, long-term-oriented perspective, I believe Hollysys is a buy. There are two outcomes that are now possible going forward:

- Buyout for $25 or more representing at least a 26.2% capital gain

- No buyout, but a continued turnaround story with regard to growth

So, in my opinion, this stock can be bought for the buyout speculation with relatively low risk. If the board declines the buyout offer, shares of the stock are very likely to fall steeply. However, over the long term, I believe Hollysys will recoup its value given its high return on net operating assets as well as its strong sales growth since the founder Changli Wang took over as CEO. Another catalyst that may help the share in the short-term, given the board turns down the offer, is that the company issues a dividend or share repurchase. This has happened historically when the company increased its dividend by 60% in March 2022 ( Seeking Alpha News ). The dividend would return some gains to shareholders, strip the company of excess cash, and as a result, increase the return on equity.

For further details see:

Potential Turnaround Stories: Hollysys Is A Buy Whether Buyout Or Not