PWFL - PowerFleet: Unclear Return On Investment In Unity SaaS Platform

2024-01-08 10:48:42 ET

Summary

- PowerFleet, once a high-growth company, has seen its revenue growth slow from about 50% in 2019 to 7% in 2022.

- The company’s balance sheet shows a consistently unfavourable debt profile since 2018.

- The Cash Conversion Cycle (CCC) has been increasing, indicating a longer time to generate cash from inventory.

- Since 2023, the company has invested in a new SaaS platform, “Unity”, to grow its business. Despite PowerFleet’s slowing revenue and gross profit growth, investors need to consider if the investment in Unity will materially reaccelerate PowerFleet's growth.

Investment Thesis

PowerFleet, Inc. (PWFL), once a high-growth company, has seen its revenue growth slow from about 50% in 2019 to 7% in 2022, with the cost of revenue under control but operating expenses exceeding gross profit. Net income has been negative from 2018 to 2021, with a slight increase in 2022. The reinstatement of pandemic-halted "Selling General & Admin Expenses" (S&A) expenses suggests future persistence.

PWFL has maintained a healthy working capital since 2018, but this was achieved with significant debt accumulation. To make matters worse, PWFL's net interest expense to EBITDA ratio suggests the company's difficulty in servicing its debt, with the ratio exceeding 100% in some years. The only exception was in 2022 when no interest expenses were incurred. Overall, PWFL's balance sheet has shown a consistently unfavourable debt profile since 2018.

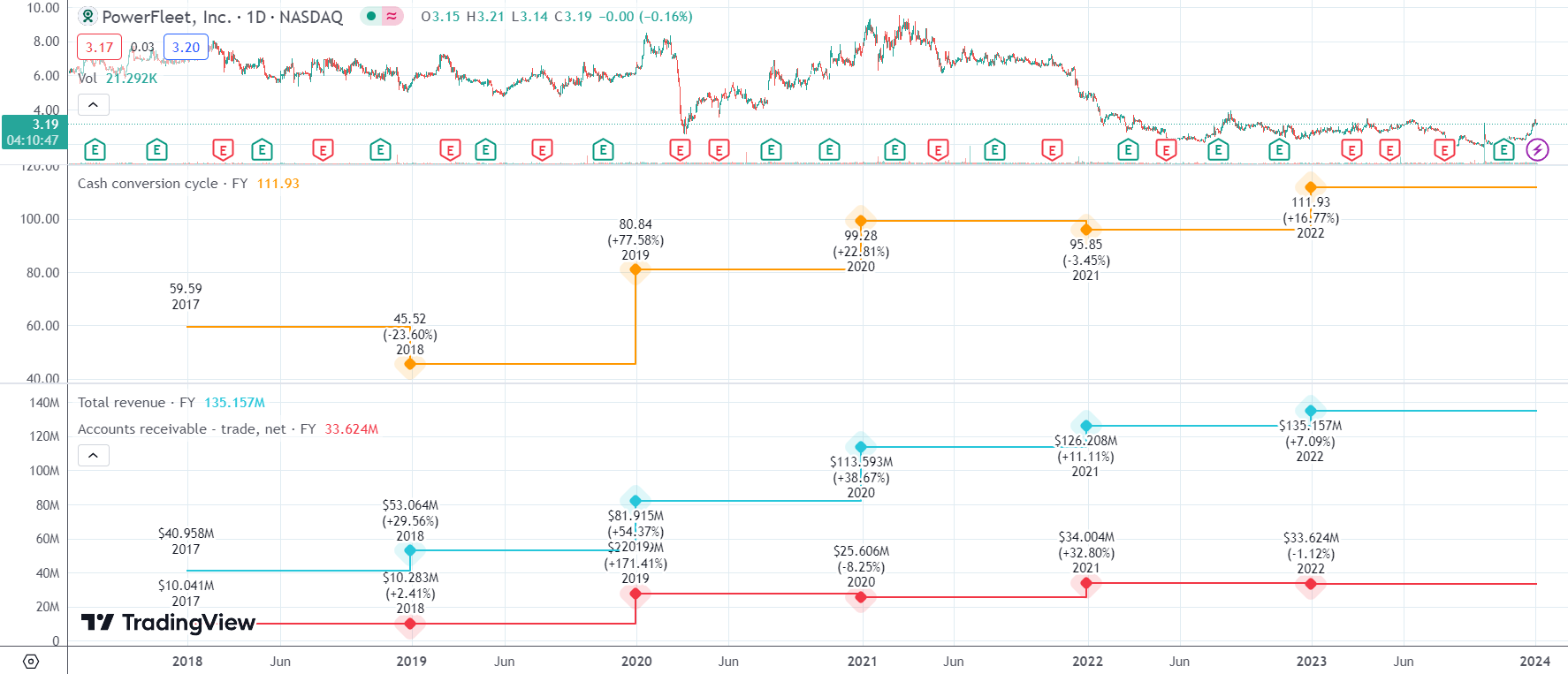

Since 2020, PWFL's operational cash flow has been mostly positive, with 2021 being the exception. The negative cash flow in 2021 was largely due to a significant increase in accounts receivables and inventory. Since 2018, PWFL's revenue has grown faster than its accounts receivable, but the Cash Conversion Cycle (CCC) has been increasing, indicating a longer time to generate cash from inventory. While an increase in accounts receivable is not concerning if it doesn't exceed revenue growth, investors should monitor the increasing CCC trend.

Since 2023, the company has invested in a new SaaS platform, "Unity", to grow its business, resulting in an accumulated deficit of $143.3 million as of September 30, 2023. The management expects sufficient cash for the next 12 months' growth plans, assuming they yield the intended results. Unity, an AI and data platform, integrates with external data sources to optimize assets and processes, offering cross-selling opportunities within the existing subscriber base and minimizing customer acquisition costs. Despite PWFL's revenue and gross profit growth since 2019 slowing recently, investors need to consider if the investment in Unity will materially reaccelerate PWFL's growth.

Company Profile

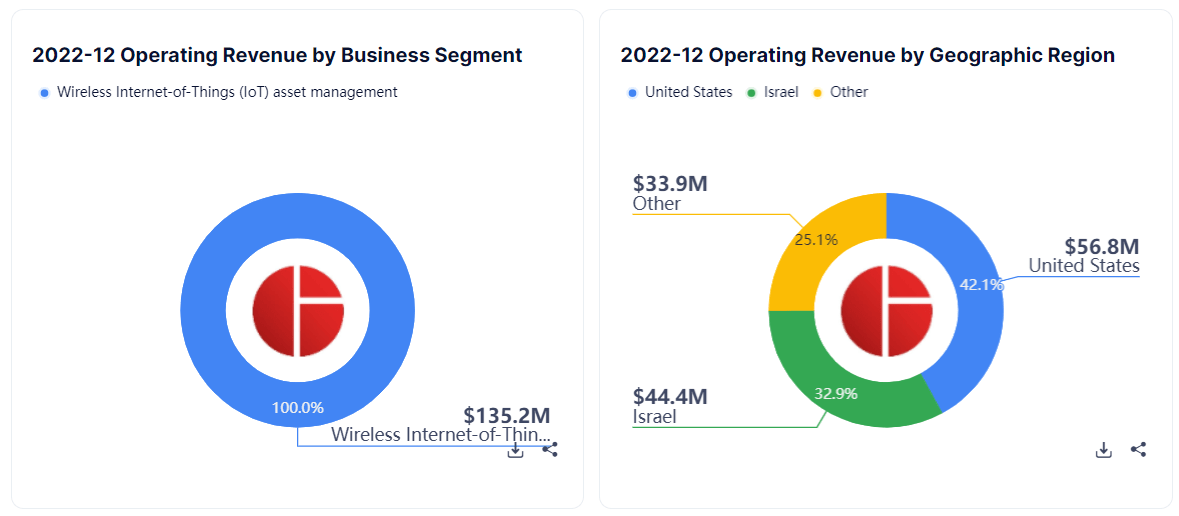

PWFL is a global leader in providing wireless Internet-of-Things ("IOT") asset management solutions . The company specializes in fleet management solutions for logistics, industrial, and vehicles. The company's solutions optimize the performance of mobile assets and resources, unifying business operations. It offers solutions for securing, controlling, tracking, and managing high-value enterprise assets such as industrial trucks, trailers, containers, cargo, and truck fleets. These solutions are subscription-based .

From GuruFocus's breakdown of its business segment, it appears to be a pure-play IoT company as opposed to other IoT players. It operates mostly in the US and Israeli markets:

Revenue Breakdown (Guru Focus)

{kind=link}

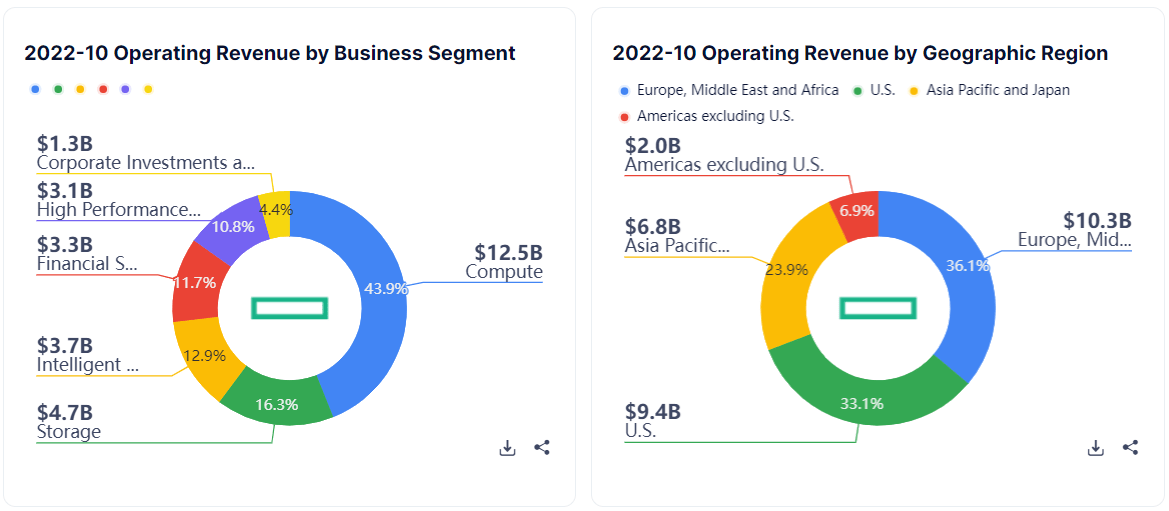

In my opinion, PWFL's pure-play business model in IoT is a potential concentration risk . While more established players like Hewlett Packard Enterprise ( HPE ) also provide IoT solutions , it mitigates concentration risks by diversifying its products and services, as can be observed in these pie charts .

{kind=link}

In terms of geographical diversifications, HPE also did a better job by deriving revenue in a much wider range of regions. For example, while HPE derives revenue from the whole of the "Middle East", PWFL derives a significant share of the revenue from "Israel", which is only one part of the "Middle East".

Income statement

We infer from Seeking Alpha's Income Statement to understand more about PWFL's top and bottom lines.

Income Statement (Seeking Alpha)

{kind=link}

We can observe that:

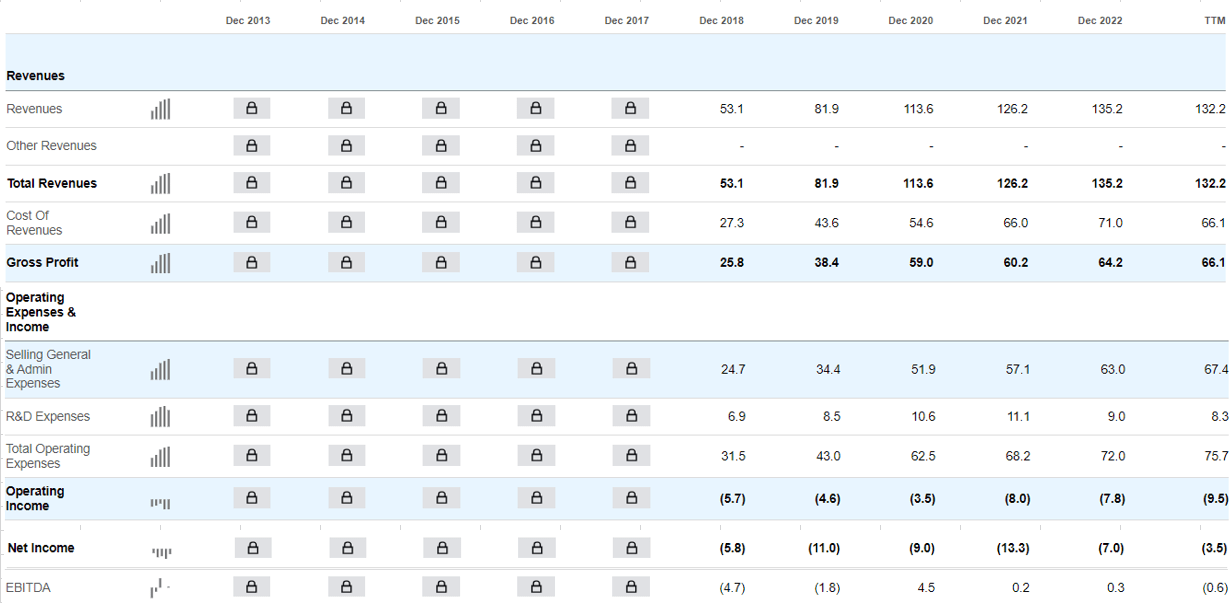

- PWFL's top-line revenue has generally been growing since 2019. However, this growth has slowed significantly from a high of more than 50% in 2019 to just about 7% in 2022. The year full of 2023 has not been reported yet, but from the TTM, we can observe the revenue is already slightly lower compared to Dec 2022. Since there is only one more quarter of earnings to be reported for 2023, it does not look likely that the company's overall annual revenue will significantly beat the year 2022.

- Despite the slowing growth, the cost of revenue has been kept largely under control. Since 2018, this cost has consistently maintained at about half of its total revenue. This results in a gross profit that is just mildly increasing.

- Unfortunately, if we drill deeper and observe the operating expenses, it consistently outstripped its gross profit since 2018, resulting in a consistently negative operating income. The greatest contributors to operating expenses are observed under S&A.

- When its overall net interest expenses/income and other non-operating expenses were included in its bottom line, it pushed its overall net income further into the negative territory in most years from 2018 to 2021. In 2022 and the latest TTM periods, net income only increased (becomes less negative) slightly.

From the company's latest annual report :

Operating Expense (Annual Report)

{kind=link}

The company reinstated S&A expenses that were previously on hold due to the pandemic. This suggests the expenses are likely to persist in subsequent years.

Overall, PWFL's income statement exhibits a previously high-growth company that appears to have slowed down significantly. Investors must consider whether this tapered growth is a permanent trend or just due to some temporary headwinds.

Balance Sheet

We now look at some figures extracted from Seeking Alpha's balance sheet .

Balance Sheet Line Items (Compiled by Author)

{kind=link}

We can observe that:

- The current ratio has been consistently above 1 since 2018 implying PWFL has a good track record in maintaining a healthy working capital. Unfortunately, this was achieved with a significant amount of debt accumulated. This debt-ridden trend has been quite consistent since 2018. The favourable figures are highlighted in green while those not are in red.

- If we compare the net debt against PWFL's EBITDA, they are not favourable in most years. Although the EBITDA was negative in 2018, the company also had a negative net debt, meaning it had enough liquid assets to offset its debt. For this reason, I considered this ratio to be favourable. For the figures reported in 2019 and 'Last Report' the positive net debt is compared against a negative EBITDA and so they are not favourable. From 2020 to 2022, the ratio is consistently above 4. In my opinion, any value that is above 3 is considered unfavourable.

- Debt-ridden companies can still sustain their operations for a very long time if their debt-servicing obligations are relatively low. I benchmarked PWFL's net interest expense against its EBITDA (Net interest Expense/EBITDA) to understand how it fared over the last 5 years. In 2018, 2019, and the last reported period, EBITDA was negative, meaning the company can't even maintain a positive earning, let alone service its debt. In 2020 and 2021, there were some EBITDA positive earnings, but it's low compared to its debt-servicing expense. In these years, "Net interest Expense/EBITDA" ranged from 100% to 1400%. In my opinion, any value of more than 30% is unfavourable, and PWFL's ratio is way above this threshold. PWFL only had one favourable year in 2022, where there were no interest expenses incurred.

Overall PWFL exhibits a very unfavourable debt profile on its balance sheet that appears to be a consistent trend since 2018.

Cash Flow And Operational Efficiency

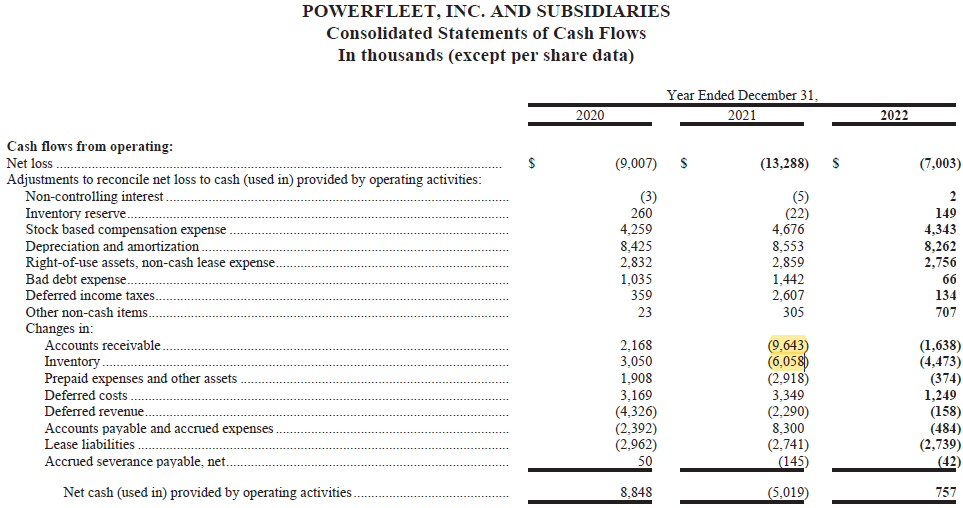

In recent years since 2020 right up to the TTM period, PWFL's cash flow from operations has turned positive on most years. The only exception is in 2021:

{kind=link}

If we calculate the free cash flow that includes the capital expenditure, it is barely positive. On average, since 2018, I consider the free cash to have broken even.

The company's annual report shows that the greatest line item contributing to this negative cash flow is a huge increase in accounts receivables and inventory in 2021.

{kind=link}

From a multiyear perspective, since 2018, we can observe that PWFL's revenue (blue line) has always been increasing faster than its accounts receivable (red line). The orange line representing the CCC is visibly increasing, suggesting it is taking the company a longer time to generate cash from its inventory.

Accounts Receivable and CCC (Trading View)

{kind=link}

In my opinion, increasing accounts receivable is not a concern as long as the rate of increment does not exceed that of revenue.

However, investors should observe whether the trend of increasing CCC gets out of control.

Investment In "Unity SaaS Platform"

Since the beginning of 2023, the company has been leveraging on the investment of a new SaaS platform of "Unity" to grow its business significantly resulting in losses and negative cash flows:

Importance of Unity (Quarterly Report)

{kind=link}

The management expects the company to have enough cash to maintain its growth plans for the next 12 months, but only with the assumption that the plans yield the intended financial results:

Management Comments (Quarterly Report)

{kind=link}

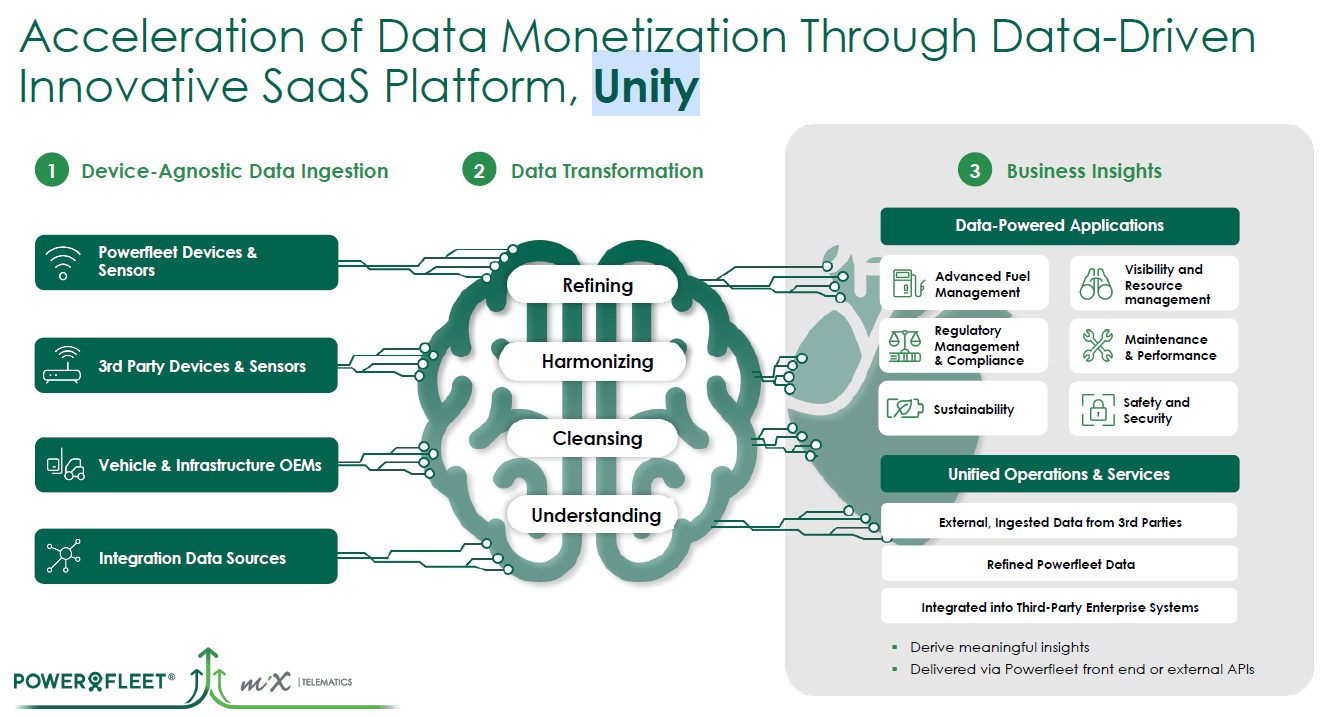

From the company's investor day presentation , Unity is an 'AI and data platform' that integrates with external data sources to optimize mobile assets, individuals operating the assets, and business processes:

Unity Business Use Case (investor day presentation)

{kind=link}

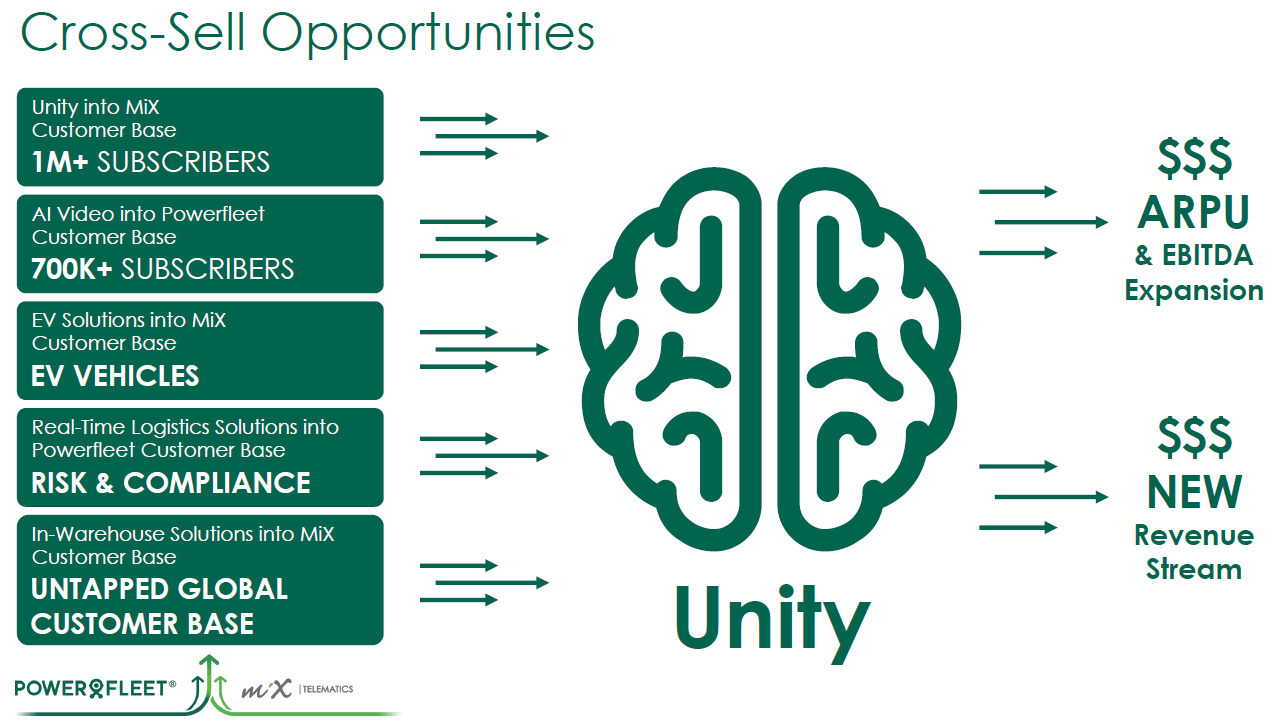

This should provide the company with cross-selling opportunities within its already existing subscriber base, minimizing customer acquisition costs.

Unity Business Use Case (Investors Day Presentation)

{kind=link}

As discussed earlier, PWFL's revenue and gross profit have been growing since 2019 but slowed recently. Investors need to consider whether this investment in Unity will materially reaccelerate PWFL's growth in the long run.

Specifically, in subsequent 'investor day presentation' slides, under "Cross-Sell Opportunities", investors should expect to see the '$$$' signs eventually replaced by real revenue and earnings values.

From the company's quarterly report , PWFL incurred a substantial deficit of $143.3M and is expecting the returns on investment of Unity to offset these deficits:

The Company has incurred recurring losses and negative cash flows from operations since inception and had an accumulated deficit of $143.3 million as of September 30, 2023. The Company anticipates incurring additional losses until such time that growth in revenue and gross margin from its strategic plan centered on its Unity SaaS platform and Industrial safety product offerings exceed necessary investments in operating expenses, capital expenditures and debt financing costs.

Moving forward, in subsequent 'investor day presentation' slides, under "Cross-Sell Opportunities", investors should expect to see the '$$$' signs eventually replaced by real revenue and earnings values (refer to the previous image).

Ideally , the amount of "NEW Revenue Stream" reported for Unity should be close to or even higher than $143.3M to materially offset the accumulated deficit for the company to achieve long-term profitability.

However, this scenario might be overly optimistic given that the highest revenue reported over the last 5 years is only $135.2M in 2022. Moreover, we also need to assume the cost of maintaining the platform is so immaterial that almost all the revenue generated trickled down to its EBITDA.

Valuation

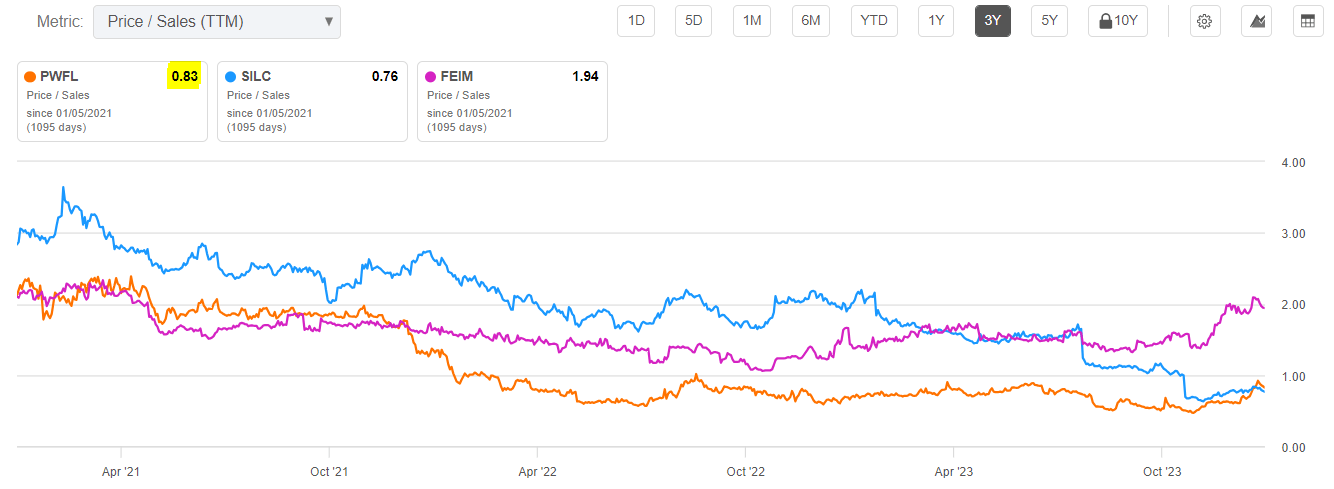

PWFL does not have consistently positive cash flow and profits. Hence, we will compare the company's valuation using its Price/Sales (P/S) ratio.

We will compare PWFL with Silicom Ltd ( SILC ) and Frequency Electronics ( FEIM ). Both of these companies are comparable with PWFL in terms of market capitalization (around 100M).

We compare the P/S ratio over the last 3 years and observed PWFL to be the 2nd most undervalued ticker in the list.

{kind=link}

The average P/S in the list is 1.18. Assuming PWFL should be trading at this P/S, the intrinsic value is 4.37, implying that that stock is 29.74% undervalued:

Intrinsic Value (Calculated by Author)

Risk

As discussed earlier in the section on 'Income Statement' PWFL runs a business that is expected to permanently operate with S&A expenses that are significantly high. Investors should expect these expenses to cause a significant drag in the company's attempt to turn profitable in the foreseeable future.

While the company expects current growth projects like Unity SaaS Platform to significantly elevate future revenue, the company offers 'no assurance' that it will happen, as mentioned in the latest quarterly report:

{kind=link}

Conclusion

PWFL runs a business that is not profitable in accounting profits, mainly due to its high S&M expenses, which are likely to persist in the foreseeable future.

The company does have growth plans that are likely to boost its gross margins and possibly trickle down to its bottom-line net margins. However, as acknowledged in the company's quarterly report, there is 'no assurance' that it will happen.

However, the company is significantly undervalued compared to its peers. Assuming the company's growth plans materialize and barring any macroeconomic headwinds like the recent pandemic that may further increase its already increasing CCC, investors can still benefit significantly.

In my opinion, investors should hold and observe whether there are any significant updates from the company about how much tangible revenue and earnings the Unity SaaS Platform is contributing to the company.

For further details see:

PowerFleet: Unclear Return On Investment In "Unity SaaS Platform"