PPG - PPG: Good Performance But Not 'Outperformance'

2023-08-31 15:01:55 ET

Summary

- PPG Industries has underperformed the S&P 500 but has remained in the green.

- The company has seen improvements in operating cash flow, adjusted EPS, and top-line sales in Q2 2023.

- PPG's future is uncertain due to weaknesses in non-automotive and aerospace-related industrial sectors and the potential slowdown of growth in China.

Dear readers/followers,

Given the chaotic status of the market, every positive development might be worth highlighting. Because even if my portfolio is, as I see it, riddled with qualitative businesses that are going to see significant longer-term upside, clear winners this year so far have been pretty rare. This is likely due to my underexposure to the tech side of things, which has been doing remarkably well, and better than I expected.

My investment in PPG ( PPG ) has been doing okay - but not spectacular by any means. By that, I mean that the company has underperformed the S&P500, but has performed at least in the green.

Seeking Alpha PPG (Seeking Alpha)

If you follow my work you may note that I'm more of a "directional" investor. By that I mean that I invest in undervalued businesses based on fundamentals and trends I see long term - that I expect a business to grow, though I'm always clear that it's uncertain of how quickly, or how strongly that direction materializes or ends up. If over 10 years in the market have taught me anything, it's that the market is both fickle and unpredictable in all but the very long term. Some investments where I was convinced that the market would see value still haven't seen their thesis fulfilled - while others where I was convinced we would see the thesis materialization within no quicker than 5 years did so in 5 months, enabling rotation/trimming.

So, fickleness.

In this article, I mean to revisit PPG and give you my update for the 2H23 period.

PPG Industries - Some upside materialized, but the future is somewhat uncertain

Like most paint and coatings companies, PPG has become a play on specialty products. This seems to be the mantra for most companies in basic materials overall. Finding niche growth and specialty markets, and becoming master-of-one instead of master-of-none - though usually combined with the legacy segments that, while having low growth, provide a good fundamental income level.

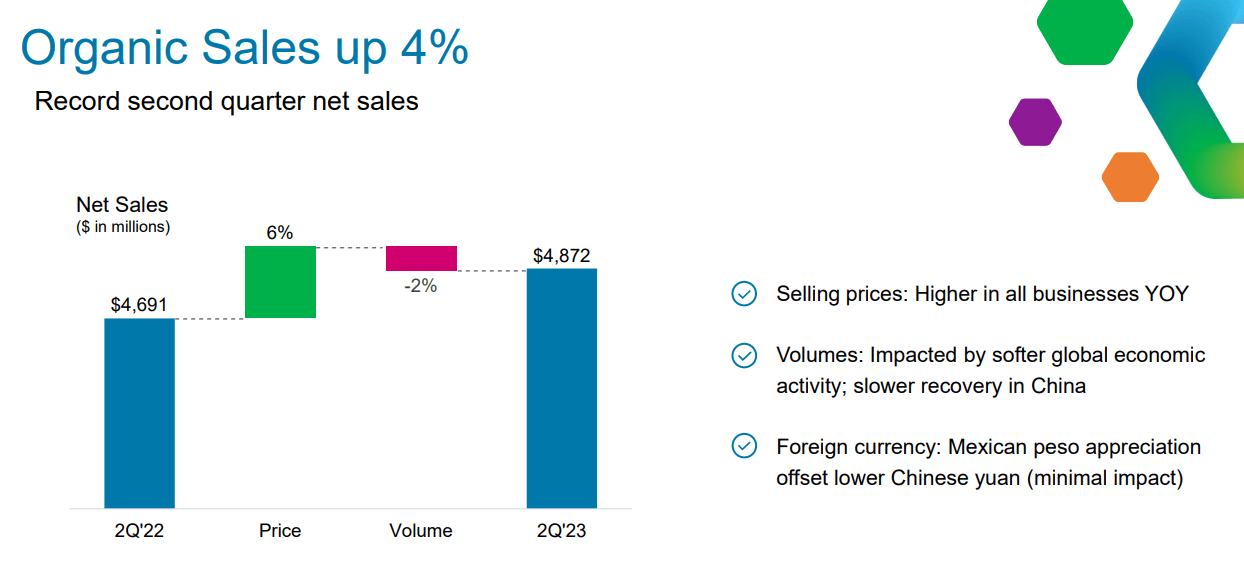

2Q23 results for this company with these ambitions and these operations were good. We're looking at solid operating cash flow of over half a billion, a double-digit increase in adjusted EPS, margin and return improvement, and a 4% increase in top-line sales on a net basis. Looking at those results, I knew we'd see improvements from a pricing perspective, but the company's positives for 2Q go beyond this. We have improved availability of input, strong demand both from global aerospace, and recovery in OEM automotive, resulting in strong cash generation.

The non-automotive and aerospace-related industrial sectors show weakness - but this shouldn't be a surprise to anyone who's been following any of my articles on companies in either basic materials or industrial - parts of the industry are currently weak.

{kind=link}

The positives speak for themselves here. The negative - including construction, the housing market, industrial production, interest rate, labor, China, inflation, and a downturn in consumer spending - are all things to either watch or be careful with.

But as with other companies that I've reviewed, PPG in no way controls the trends for these factors - they are a chip of wood adrift in a sea, following the current like all of the other companies in the same sector.

Meanwhile, sector-specific results are worth looking at. As expected, the positives were not a result of volume, but pricing and FX.

{kind=link}

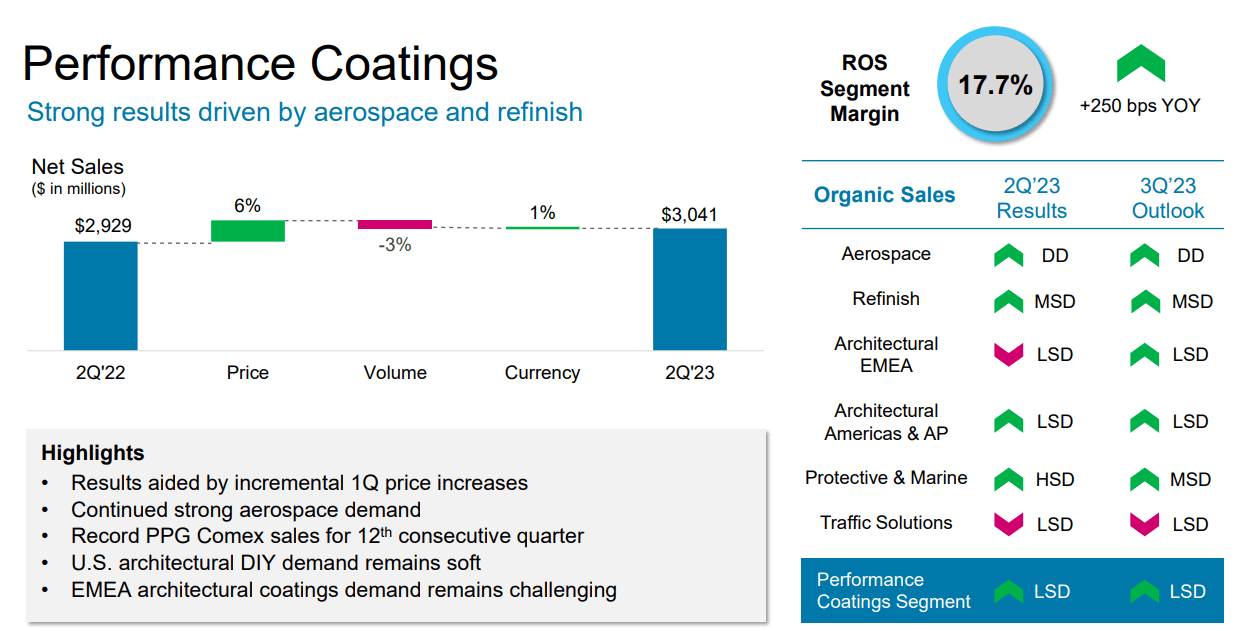

Similar trends in Industrial Coatings, though we saw less volume decline and negative as opposed to positive FX. China is a larger disruption on the industrial side.

This isn't an article on China specifically, but the China issue does influence PPG. My view is that the nation's growth has stalled. We've already seen a slowdown in annual GDP growth to 3% back in 2019, and this is now down to less, with expectations that we'll be at 2% in 2030. Based on this, the nation fails to meet its objectives of a doubling of the economy size by 2035 (Source: WSJ ). This marks the end of the 40-year growth trajectory we've seen which has been around for as long as I've been alive. What comes next is something we'll see - but companies like PPG would do well to prepare for the eventuality that China will provide significantly less growth going forward.

The company did note record-level operating levels of cash flow for the YTD period in June, at $621M, and provides us with full-year projections with adjusted EPS of upwards of $7.5/share on the high end (minus a few cents). The company's net debt is at a level of around $5.6B, and the company has over $1.2B cash on hand as of the end of 2Q - plenty to meet what obligations it does have.

PPG has, and still is a premiumized company when it comes to how it is valued and what you should expect when you invest. You don't have much yield to speak of - below 2% even at today's level in fact, despite the fact that we're not even close to the premium we saw back in 2020 and 2021.

The company makes up for this with BBB+ credit, a long-term debt of less than 44% to capital, and being in a more or less market leadership or significant position when it comes to market share for many of its key products.

As I mentioned in the last quarter, the company recently acquired Tikkurila, one of the primary paints manufacturers in Finland, which is a great addition to the company's lineup - and PPG continues to be M&A-heavy, with the balance sheet and credit to match those ambitions well.

The company also, at this time, remains one of the more profitable businesses in the entire segment, with superb gross margin levels of almost 40%, and squeezing a net margin of over 7% based on the latest published data (Source: GuruFocus). In every metric that matters in terms of profitability, the company is either at sector-beating levels or slightly above the average, and the sector we're talking about specifically here is the chemicals sector, with peers such as LyondellBasell ( LYB ), Dupont ( DD ) which I recently wrote about, Albemarle ( ALB ), International Flavors & Fragrances ( IFF ), Westlake ( WLK ) and others.

All in all, it's fair and even accurate to say that PPG delivered all-time record-high financial results. That's also the reason, or part of it, why much of the premium is intact and why despite trading high, the company hasn't declined much. 5 out of 9 business segments were at excellent levels, but this was mostly the result of pricing adjustment, not significant volume growth. In fact, volume for the most part was down.

But margin has been the company's focus for some time now, as it should be. I'd rather see margin improvements than volume growth for a company like this (though ideally of course both).

The core point to keep in mind here is the same for most industrial and chemical companies. It's all in the macro. We're looking for improvements on a global scale, but those improvements will telegraph for conscious investors who follow industry order trends and other macro indicators. So while there are key smaller segments that could see earlier improvements here in the business, overall it's mostly a macro play. The fact that we've seen stability in both aerospace and automotive is reassuring and goes toward further earnings stability and perhaps even improvement, justifying at least some of the upside here.

PPG Industries - As with many companies here, the upside is based on premiumization

As with other companies that I'm reviewing, the issue is that continued market-beating or 15% growth or above, on an annual basis, is something that's based on continued premiumization in an environment that has nothing in common with the circumstances that caused some of that premiumization we're using to forecast historically.

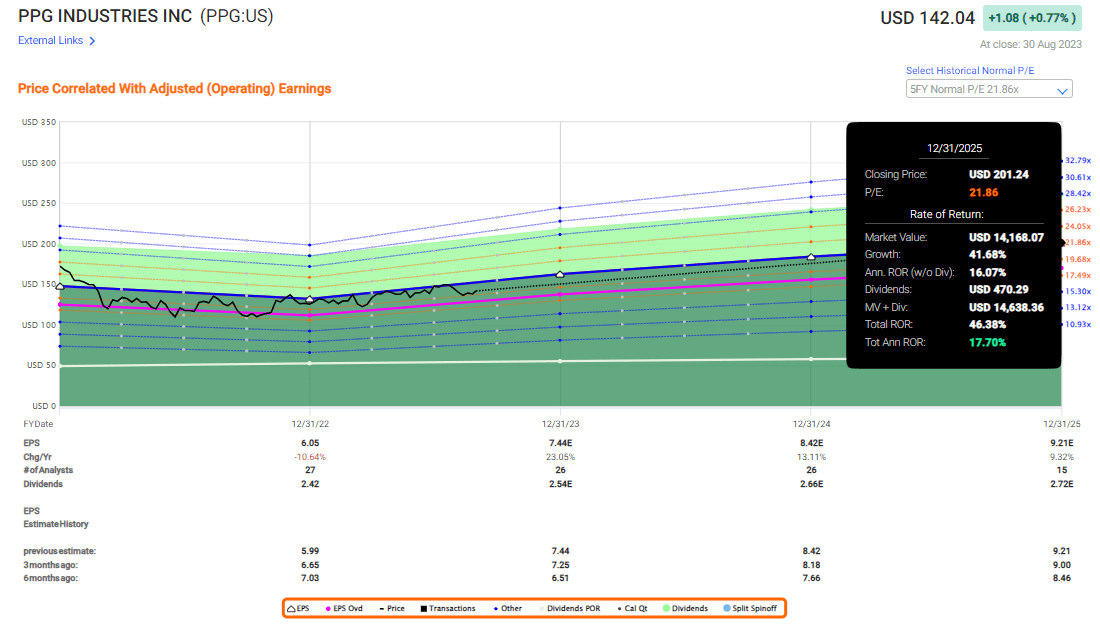

This company typically is at around 19-21x P/E, has a low yield, but has averaged impressive growth. The company's current guidance confirms the forecast of 23% EPS growth for this year, followed by another double digits in 2024E and potentially 2025E as well. The upside based on full premiumization, meaning almost 22% here is almost 18% per year, which of course is enough for where I would consider it a "BUY".

F.A.S.T graphs PPG Upside (F.A.S.T graphs)

{kind=link}

But so much of this is based on continuation on a premium, that I'm not sure if this is something we want to forecast. If we look at the lower levels to which the company has dropped as late as 2022, then the upside goes down to single digits. 9.5% per year, but still single digits, and that's inclusive of dividends with dividend growth.

S&P Global analysts and other targets give the company ranges between $115/share to $180 - a pretty wide spread, with an average of about $160/share. This is a 12.2% upside from today's share price level, but again, based on a fairly high premium. Out of 24 analysts, less than half (10) are at "BUY", with 14 at combined ratings of either "HOLD", Underperform or "SELL". So while price targets and trends show upside, there is doubt whether the company will be able to materialize the same premium in its valuation that we've seen historically.

I do give the company a $160/share price target - much like these analysts. But $160/share in the long-term represents a 17.5x P/E, not a 21x P/E. That means the long-term upside if you invest with a $160/share PT, is around 7.35%, which is half what I typically look for in a company that I want to invest in.

Half is not good enough for me - but it may be good enough for you. And at $150/share, the company is too cheap for what it offers. Just keep in mind that I don't validate the premium here. I consider the company likely to actually underperform relative to this going forward, given the risk-free rate changes and costs in funding.

With that, here is my thesis on PPG industries as of this time. In my last article, I gave you some options you could go for. But with the premium declines we've seen for the cash-secured put side of things, these options are for the most part not attractive any longer. Even in the last article, the option I published had an annualized RoR of 9% - not something I would go for today with what is available on the market.

Thesis

- PPG Industries is a quality company in chemicals/coatings. It has a solid history, good dividend growth, and very good fundamentals, despite an increasing debt due to M&A.

- At current valuations, there's a realistic upside to 2023-2025E based on market normalization in key segments, M&A/Integration synergies, cost savings, and increased demand. The risk is that these developments take longer or don't materialize. The problem here is premiumization.

- I believe the likelihood is high that a company that's been performing well for 20 years will continue to do just that. My thesis, based on this picture, is, therefore, a "BUY" with a PT of $160/share, and this price target remains here.

- Just be aware that I don't believe you can see 14-15% annualized from this investment, but a 7-9% per year is more likely here based on current trends.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

I can't call the company cheap based on current valuation trends for 2022-2023 - but I can call it attractive for the long term if 7-9% is enough for you.

For further details see:

PPG: Good Performance, But Not 'Outperformance'