PPG - PPG Industries: Buy This Fairly Valued Dividend Aristocrat Now

2023-12-30 07:15:00 ET

Summary

- Shares of PPG have sharply rallied in 2023.

- The industry reported robust net sales and adjusted EPS growth in its third quarter.

- Through the first three quarters of this year, PPG's interest coverage ratio has been strong.

- Shares of the paints and coatings producer look to be priced 1% below fair value.

- PPG could be positioned to outperform the S&P 500 in the next 10 years.

Many bright minds who came before me often argued that the stock market is a market of stocks. After all, some stocks are frequently blazing to new 52-week highs and some seem to constantly slump to new 52-week lows.

{kind=link}

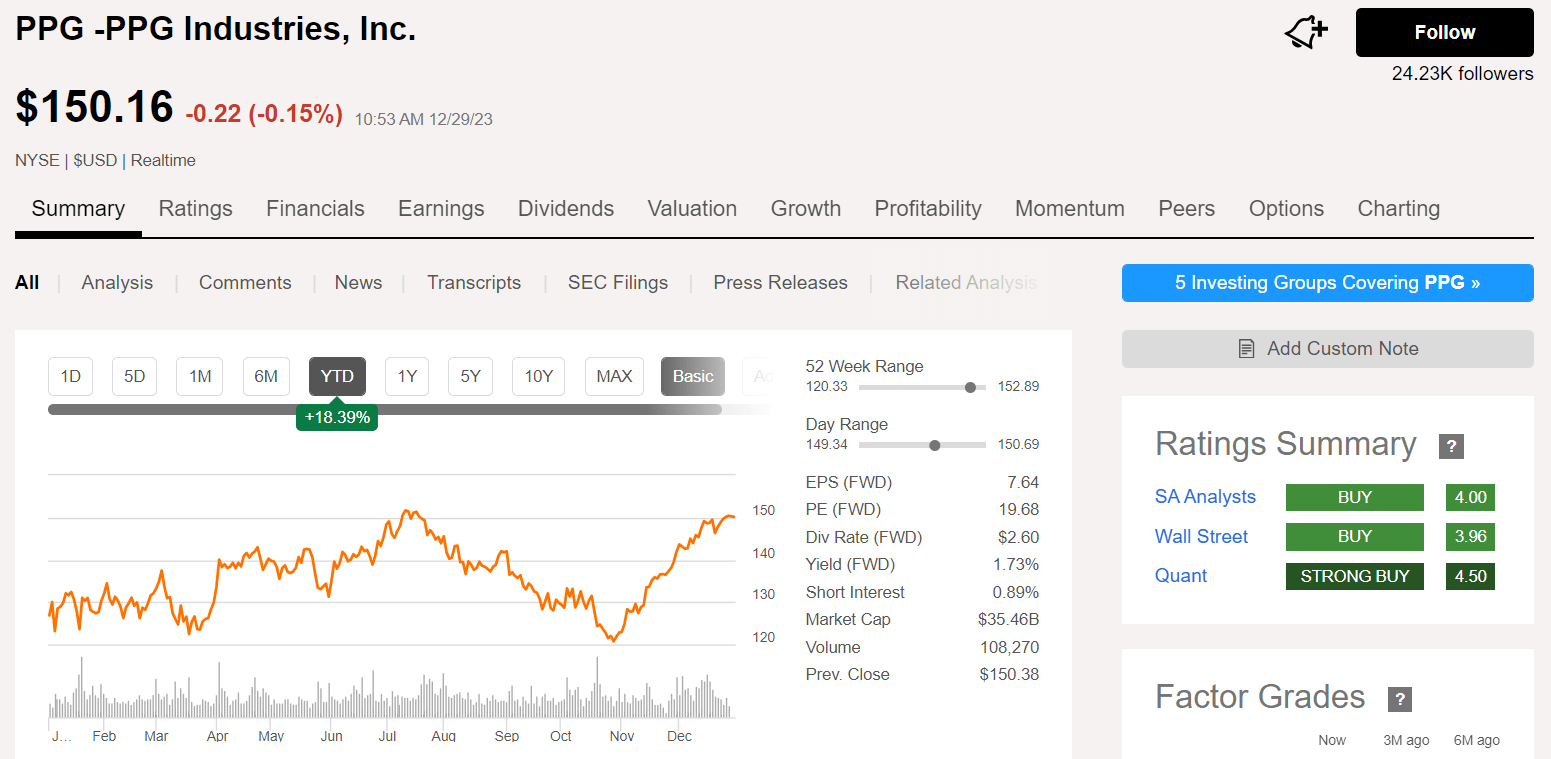

One stock that has been busy doing the former is PPG Industries ( PPG ). With just a partial day of trading left in the year, shares of the industrial have climbed 18% thus far. This is just 1% off of the 52-week high that the company set in the summer.

Even with this meaningful rally, I am initiating a buy rating on shares of PPG. Please allow me to elaborate on the company's fundamentals and valuation to support this argument.

{kind=link}

PPG's 1.7% dividend yield clocks in just above the 1.5% yield of the S&P 500 index ( SP500 ). What differentiates the company, though, is its dividend growth track record. Since 1899, PPG has paid uninterrupted dividends. Not to mention that in July , the company's 4.8% increase in its quarterly dividend per share was its 52nd consecutive year of dividend increase. That makes PPG both a Dividend Aristocrat and a Dividend King.

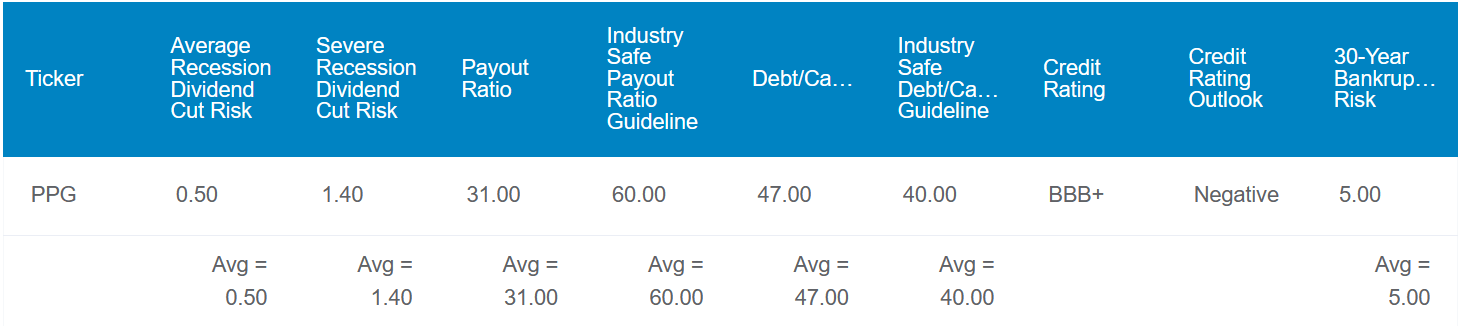

What's more, the company's 31% EPS payout ratio is roughly half of the 60% EPS payout ratio that rating agencies think is sustainable for its industry. If that weren't enough, PPG is a financially solid business. The company's 47% debt-to-capital ratio is only a bit above the 40% that rating agencies desire. This is why S&P awards a BBB+ credit rating to PPG on a negative outlook, which limits its bankruptcy risk over the next 30 years to around 5%.

Considering these factors, Dividend Kings pegs the company's probability of a dividend cut in the next average recession at 0.5% - - tied for the lowest estimated probability for any dividend stock. If the next recession were to be severe, this risk remains subdued at 1.45% - - not much higher than the minimum of 1% for any dividend stock.

{kind=link}

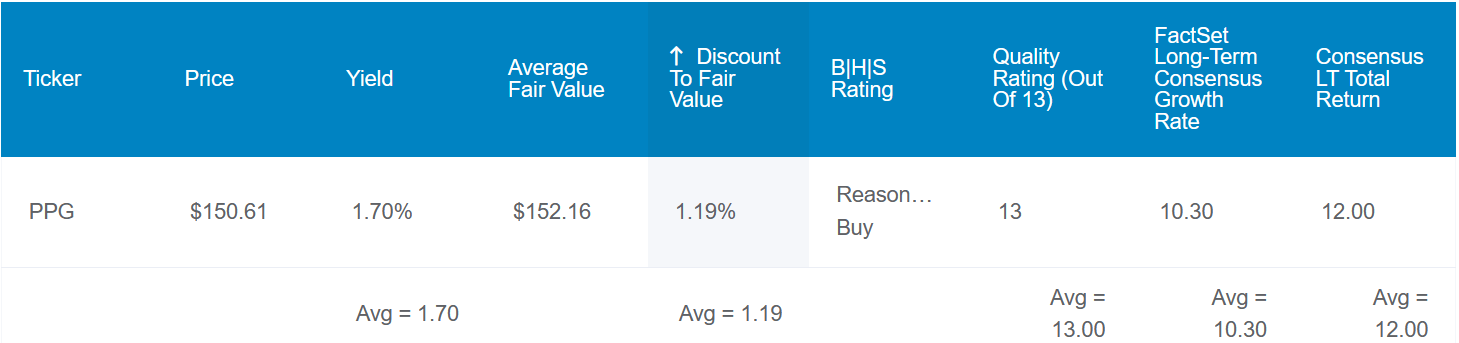

Fundamentals aside, PPG isn't just a great business. It also appears to be valued at a fair price right now. If the average of historical P/E ratio and dividend yield are any guide, Dividend Kings estimates shares of PPG are worth $152 each. Relative to the $150 share price (as of December 29, 2023), PPG is trading at a 1% discount to fair value.

If the industrial matches the present growth consensus and reverts to fair value, here are the total returns that PPG could deliver in the next 10 years:

- 1.7% yield + 10.3% FactSet Research annual growth consensus + 0.1% annual valuation multiple expansion = 12.1% annual total return potential or a 213% 10-year cumulative total return versus the 8.6% annual total return potential of the S&P 500 or a 128% 10-year cumulative total return

PPG Is Delivering For Shareholders

Since its founding in 1883, PPG has established itself as a leader in the paints, coatings, and specialty materials industry, operating in 70-plus countries. The company's reputable brands include the eponymous PPG Paints, Glidden premium paint, and Sigma professional paint. PPG's products are used throughout a variety of industries, such as packaging material, automotive refinish, aircraft and marine equipment, and industrial equipment.

PPG is divided into two business segments:

- Performance Coatings: This segment sells a variety of products, such as coatings, sealants, paints, adhesives, and finishes. The segment's strategic business units include aerospace coatings, architectural coatings Americas and Asia Pacific, Architectural Coatings Europe, Middle East and Africa, automotive refinish coatings, protective and marine coatings, and traffic solutions. The segment comprised 61.5% of PPG's $13.9 billion in total net sales through the first three quarters of 2023.

- Industrial Coatings: This segment sells similar products that are geared toward automotive original equipment manufacturer coatings, industrial coatings (e.g., kitchenware, consumer electronics, and appliances), and packaging coatings (i.e., metal cans for food, beverage and personal care). The segment accounted for the remaining 38.5% of PPG's total net sales through September 30, 2023 (details for previous two paragraphs according to pages 4-5 of 116 of PPG's 10-K filing and PPG's Q3 2023 earnings press release ).

{kind=link}

When examining PPG's recent operating results, it's not hard to understand why its underlying stock has performed well in 2023. Aside from the market upswing, the company is fundamentally doing very well. At some point, this receives favor from the market.

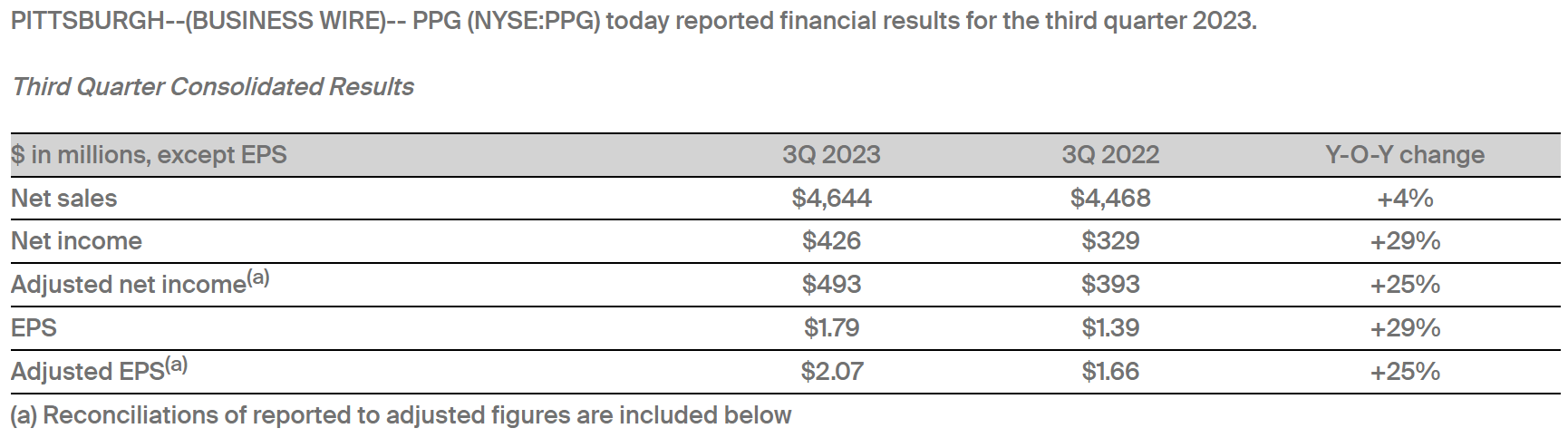

PPG's net sales grew by 3.9% year-over-year to a third-quarter record of $4.6 billion. This equaled the analyst consensus for the quarter. What was behind these admirable results?

A thriving Performance Coatings segment is what mostly contributed to PPG's record net sales in the third quarter. The segment's net sales rose by 6.5% over the year-ago period to $2.9 billion during the quarter. PPG's higher selling prices contributed to half of this topline growth while the other half was due to favorable foreign currency translation. Even with these higher selling prices, the company's customers were unphased, with volumes flat for the quarter.

The Industrial Coatings segment logged $1.8 billion in net sales, which was up approximately 0.1% over the prior year's third quarter. Decreased global industrial activity led the segment's sales volumes to fall 4% in the quarter. However, 2% higher average selling prices, a 1% foreign currency translation tailwind, and a 1% lift from acquisitions offset the volume headwind.

PPG's adjusted EPS rocketed higher by 24.7% year-over-year to $2.07 during the third quarter. Put into perspective, that was $0.13 ahead of the analyst consensus. The company's higher revenue base and a 180 basis point expansion in non-GAAP net profit margin to 10.6% explains how adjusted EPS growth outpaced net sales growth for the quarter.

PPG's interest coverage ratio also remained exceptional. Through the first three quarters of 2023, the company's interest coverage ratio was 17.6. This implies that PPG can service its debt without issue.

More Than Enough Free Cash Flow To Support Dividend Growth

In the last five years, PPG's quarterly dividend per share has increased by 35.4% to the current rate of $0.65 . Moving forward, I would expect dividend growth to accelerate.

This is because, through the first three quarters of 2023, PPG has generated $1.1 billion in free cash flow. Compared to the $445 million in dividends paid during that time, this works out to a 39.3% free cash flow payout ratio. This provides PPG with a nice cushion to keep growing the dividend and repay debt.

Risks To Consider

PPG is fundamentally strong enough to earn a perfect 13/13 quality rating from Dividend Kings. However, that's not to say that the company doesn't have its risks like all other businesses.

PPG is exposed to the risk of having to refinance debt at higher interest rates. As of the end of last year, nearly $2.4 billion of its total $6.5 billion in long-term debt due beyond a year was coming due in 2024 and 2025. These are on notes that were at interest rates ranging from sub-1% to the 2% range (details per page 46 of 116 of PPG's 10-K filing). Refinancing this debt will result in higher interest expenses for the company. The good news is that PPG is financially fit enough to take on these increased interest expenses without experiencing duress.

Another risk to PPG is the potential that its cost of raw materials could rise. If the company isn't able to pass these higher costs onto customers, it could negatively impact margins. Additionally, any shortage of raw materials could lead to disruptions to PPG's operations. That could also hurt the company's financial results.

Finally, PPG is subject to a variety of environmental regulations. If these regulations were to evolve and require additional resources from the company to remain compliant, this could hold profits down for a while as well.

Summary: A Wonderful Company At A Fair Price

Although short-term volatility is a fact of life, buying above-average businesses at or below fair value generally works out over the long run. Having upped its dividend for more than a half-century, PPG has earned its distinction as a superior business. Sealing the deal, shares of the stock seem to be priced at a 1% discount to fair value. That's why I am starting coverage on PPG with a buy rating.

For further details see:

PPG Industries: Buy This Fairly Valued Dividend Aristocrat Now