PPG - PPG Industries: Replacing A Dividend King With Another

2023-10-17 04:42:33 ET

Summary

- 3M is facing over $16 billion in liabilities and may have to cut its dividend, making it a risky bet for those looking to hold for its dividend history.

- PPG Industries, another dividend king, is a better prospect with anticipated earnings growth and is in a better position with a lower dividend payout ratio.

- PPG's valuation is reasonable, and it represents a decent time to initiate a position for the long-term income investor.

Written by Nick Ackerman.

Dividend kings are often seen as a solid place to put capital to work; after all, they have these incredibly long histories of maintaining and growing their dividends annually. 3M ( MMM ) is at 64 years, and if it were up to them, they'd probably continue along with growing their dividend. The unfortunate truth is that not everything can or will last forever.

The company is facing $16b+ in liabilities, and it isn't a blue-chip "SWAN" investment any longer. With the upcoming healthcare spin-off, I believe they are setting themselves up for an AT&T ( T ) style dividend cut. This is also being implemented more recently with W. P. Carey ( WPC ).

The idea is that they spin out a substantial portion of their business that no doubt merits an adjustment to their dividend. However, they then take it a step further and over-adjust or take the opportunity to "reset" their dividend payout ratios to more healthy levels - or at least levels that leave their balance sheets a bit healthier.

Honestly, this isn't a bad thing in itself, and that's why I'm still willing to hang on to my 3M shares in a different portfolio. The initial reaction always seems to be the same, too, when these are announced. It is met with a huge drop in the share price even if the stock had been crumbling for a year or two prior. Which is precisely where MMM is today. The share price has been sliding, but no doubt some investors will be stunned or shocked if their dividend is reset to a lower payout post-spin.

With all that being said, I did find another company that just so happened to be a dividend king to replace my 3M shares within my Core Portfolio. For that, I'm leaning into adding an initial position to PPG Industries ( PPG ).

This company isn't quite as popular on Seeking Alpha, with around 24k followers compared to 3M's nearly 200k followers. That being said, it is still a dividend king as it fairly recently announced a dividend bump that put it at 51 years of increases.

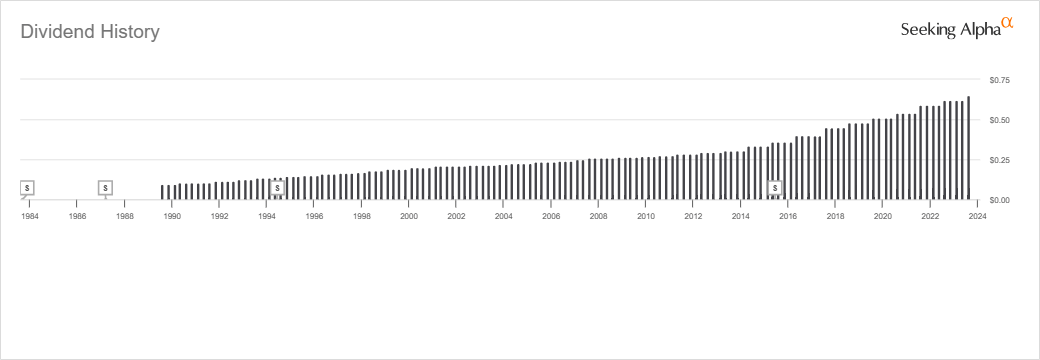

PPG Dividend History (Seeking Alpha)

{kind=link}

When announcing that last increase , they noted that it was the 500th consecutive dividend payment with uninterrupted annual dividends since 1899.

Again, the actual history of dividend payments and the consecutive increases really isn't the important part. It might set up a position where management teams are often loathe to let that sort of history end, but ultimately, it is up to what the outlook of the company is moving forward if the dividend is sustainable or not.

Different Operations, But Prospects Look More Optimistic For PPG

There are several reasons why I believe that PPG is a better prospect going forward than MMM and warrants making this move. However, it should be noted that PPG and MMM are not in similar industries.

PPG is a company in the basic materials sector as a specialty chemicals company. MMM is an industrial sector stock as an industrial conglomerate.

PPG " develops and delivers paints , coatings, and specialty materials." They segment their business through Performance Coatings and Industrial Coatings, with each category related to more specific industries or regions in each broader classification.

The Performance Coating includes aerospace, refinish, architectural EMEA, architectural Americas & AP, protective & marine and traffic solutions. This is the largest segment of the company and accounts for over 62% of the company's net sales.

With that being said, despite being in two different industries, both of these companies are going to be fairly cyclical in nature. That is, they'll rely on a strong economy to generally perform well. That's important to consider when looking at the earnings forecast and growth outlook for each company.

Despite being tied to the economy, PPG is looking like it is anticipated to grow going forward, while MMM is going to experience some declines in terms of revenue and earnings going forward. Besides the massive albatross of $16b+ in liabilities, that is a hindrance to their operations and prospects going forward, which makes their dividend even more susceptible to potentially being cut.

Earnings Outlook

Through fiscal 2023, analysts are expecting MMM to decline in earnings before returning to some growth in the following years. Over the next four years, MMM's earnings growth is expected to come in at less than 3%. I chose four years because that's comparable between both MMM and PPG, where at least more than 1 analyst has estimated.

MMM EPS Growth Forecasts (Seeking Alpha)

{kind=link}

For PPG, analysts are expecting EPS growth going forward over the next four years to average ~13.4%.

PPG EPS Growth Forecast (Seeking Alpha)

{kind=link}

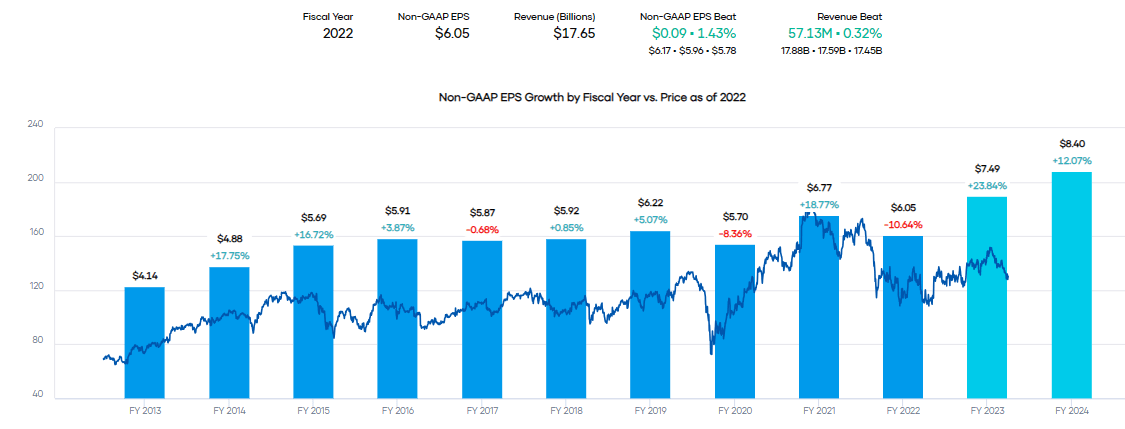

Despite being susceptible to downturns in the economy, PPG has been fairly consistent with trending upwards in terms of its earnings. 2022 was weaker, and that is one of the results of why growth in this next year is looking even rosier. However, earnings coming in this year are anticipated to top the 2021 fiscal year, meaning the trend of growing earnings is expected to remain even after the slump in 2022.

PPG Earnings History and Estimates (Portfolio Insight)

{kind=link}

Like most companies, they faced significant inflation headwinds in the prior year. With volumes coming in flat to slightly down, most of their growth is coming through price increases. However, with inflation cooling, the company should be able to stabilize a bit, and I believe that's what we are seeing in their earnings now. In their last quarter, price contributed to the 4% in organic growth for net sales.

PPG Net Sales (PPG Industries)

One thing the company remains focused on is improving margins for their business, which is going to translate into those big bumps in earnings .

We expect selling prices to remain positive in the second half 2023, recognizing prior year price increases will reach anniversaries as the year progresses. As I said at my CEO investor briefing in May, margin recovery is the top near-term priority. And we have made great progress this year in improving our segment margins toward our historical profile. Our aggregate segment margins in Q2 were about 16%, which is 330 basis points higher than the second quarter of 2022. This included the Performance Coatings segment delivering margins of near 18%, the highest since 2016.

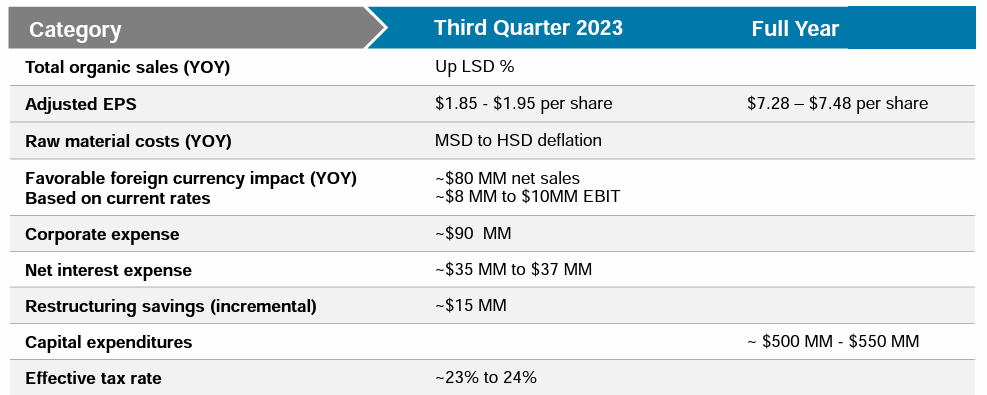

Interestingly, PPG's full-year financial projections for adjusted EPS come to $7.28 to $7.48.

PPG Earnings Outlook (PPG Industries)

{kind=link}

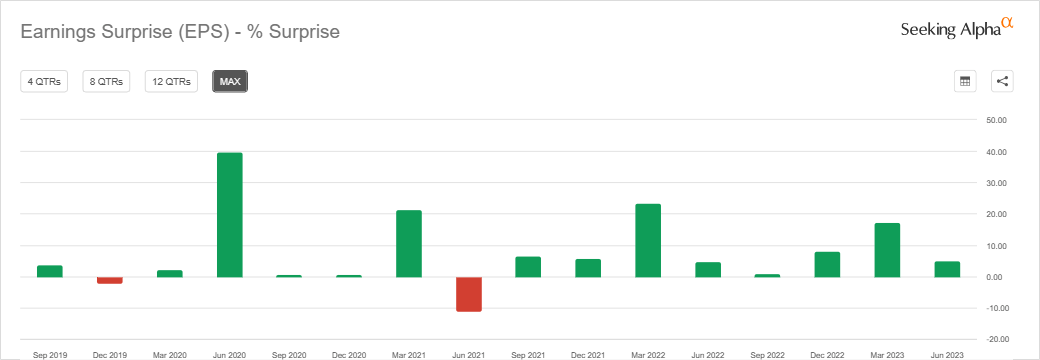

With analysts projecting $7.49 EPS for the fiscal year, that does mean they are guiding for a somewhat softer earnings outlook. However, if history is any guide, the company has often delivered above expectations, so the likelihood of earnings exceeding their own projections is mostly expected. This is generally the case with most companies, under-promise and then over-deliver.

PPG Earnings Surprise History (Seeking Alpha)

{kind=link}

Debt Paydown

One other area that can help PPG is paying down its debt. They were asked on the last call whether they were looking at buybacks or M&A. They answered by saying paying down debt was their priority.

We said earlier this year, we would pay somewhere between $500 million and $600 million down We paid about $200 million of that down so far this year. So we've got a bit more of that to do. But I'll tell you, we're going to have a really good cash year. We're going to have really good cash year, which gives us a lot of optionality. Probably not time to talk about specific actions on the M&A side, but that clearly remains a priority for us. And we are seeing properties come across our desks there. But bottom line, we're going to have a really good cash generation year. We're going to pay down some more debt. And then we're going to make decisions on how best to use that cash to deliver shareholder value based on what we see at the time.

They listed net debt at $5.6 billion; against EBITDA of $2.6 billion, we are looking at a net debt to EBITDA of 2.15. This isn't terrible, but any reduction in debt means they won't have to potentially refinance at higher rates and cut into their profitability.

That's another place where MMM is looking like they have a healthy balance sheet for now. They last reported net debt of $11.7 billion, against EBITDA of $7.469 billion, and we get net debt to EBITDA of 1.57. They have tons of free cash flow but, with a lack of meaningful growth and significant liabilities, could have to take on more debt going forward. That is debt that isn't going to go to growth initiatives but simply their liabilities. 3M earlier this year saw their debt downgraded due to these liabilities as the rating agencies expect debt to rise. However, it still remains an investment-grade-rated company.

Dividend Safety And Growth

As mentioned, I believe that MMM will take the opportunity to adjust its dividend and reset it lower when the healthcare division is spun off. This also means that the current and much higher yield for MMM is less important in making this decision overall. So, automatically, I am already more optimistic on that front in favor of PPG. Given the outlook for further earnings improvement and growth going forward, that also bodes well for PPG.

Historically, the dividend was being increased similarly to the sector median. Though within the basic materials and even within the specialty chemicals industries, there can be some significant differences between the companies. This still gives us some color of how PPG has been able to grow its dividend historically.

PPG Dividend Growth Relative to Sector (Seeking Alpha)

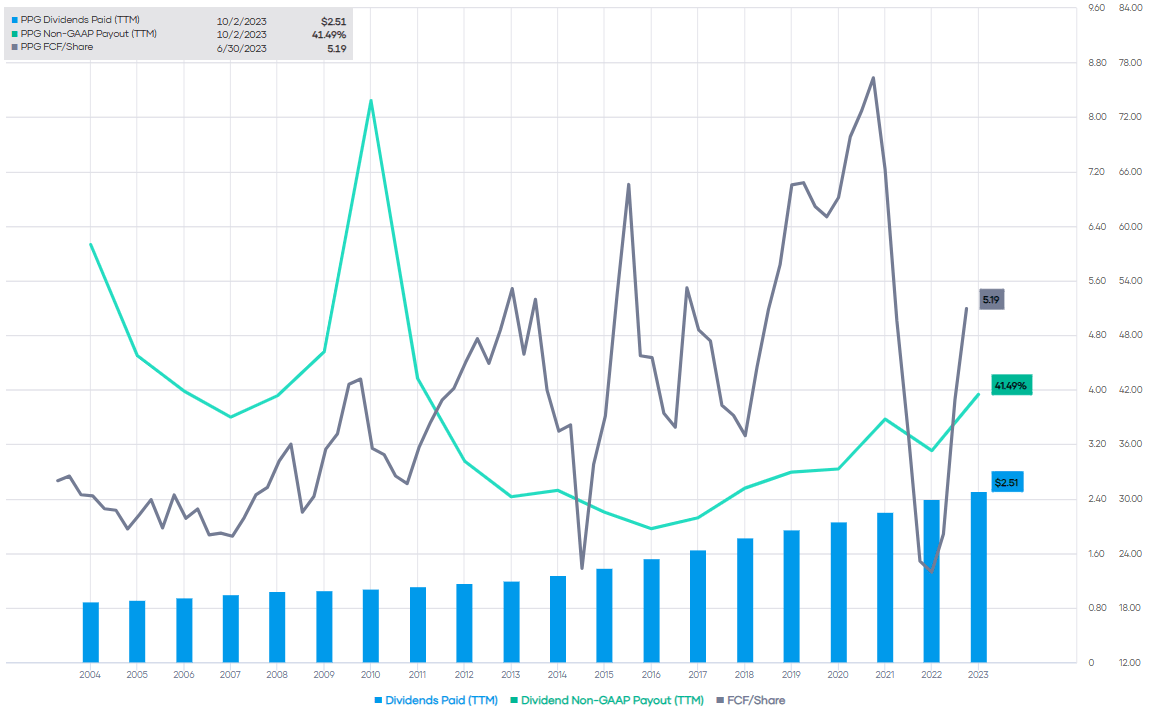

The dividend payout ratio for PPG remains low, and that's a positive for when the economy turns sour; it leaves them more of a cushion before having to cut. On a FCF basis, the dividend is also looking pretty healthy, with a payout ratio of around 48%.

PPG Dividend Payout Ratio and FCF/Share (Portfolio Insight)

{kind=link}

For comparison, MMM has a payout ratio of almost 68% on a forward non-GAAP EPS basis. In terms of a FCF dividend payout ratio, we are looking at ~75%.

Valuation

The one place that MMM could be considered to beat out PPG is in terms of its valuation.

MMM's forward P/E is at 10.55x compared to PPG's 17.32x multiple. This is similar to what we are seeing across the board in terms of valuation as well, though when looking at the forward PEG ratio, it would favor PPG. That would be due to the expectation for brisker growth going forward.

PPG Vs. MMM Valuation (Seeking Alpha)

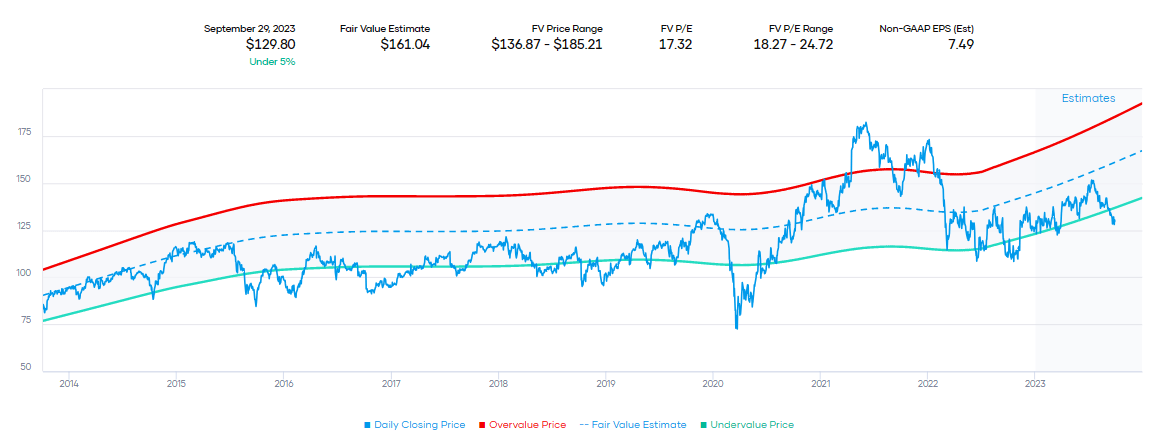

Additionally, I don't believe that PPG is looking richly valued. Historically, we are trading below the lower end if we look at the fair value range of the shares. Now, this could be due to the expectation for softer earnings than originally anticipated going forward if a recession hits. That would certainly be a valid argument; however, I can't predict the future. I also believe that MMM would be hit just as badly as PPG in the case of a slower economy.

PPG Fair Value Estimate Range (Portfolio Insight)

{kind=link}

Of course, again, as if it isn't reiterated enough, MMM is trading with the fact that they are looking at a minimum of $16b+ in liabilities. That's going to be something they are dealing with for many years going forward.

Conclusion

I believe that PPG represents a fairly attractive entry price for a company with a brighter future. I believe it is a good replacement for fellow dividend king MMM. So, I'm going to be dethroning dividend king MMM in my Core Portfolio and passing the crown onto PPG.

For further details see:

PPG Industries: Replacing A Dividend King With Another