PPG - PPG Industries: Strong Market Position Brings Margin Expansion

2023-06-22 01:11:43 ET

Summary

- PPG Industries has grown its adjusted EPS by 33% YoY, with a strong presence in over 70 countries and 51 consecutive years of dividend increases.

- The company has a solid market share in the paint and coatings industry, with a total addressable market worth around $185 billion, and has shown the ability to leverage its position to maintain robust margins.

- Despite risks such as currency fluctuations and challenges in the U.S. housing market, PPG is rated a buy due to its history of shareholder value and potential for growth in 2023.

Investment Summary

Investing in a company that produces and sells paint and coatings might be a very niched opportunity. But growth can be had here too, and plenty of it as proven by the last report by PPG Industries, Inc. ( PPG ). They managed to grow adjusted EPS 33% YoY on the back of strong performances across all the segments of the business.

PPG is present in over 70 different countries right now and has increased its dividend for 51 consecutive years in a row. That sort of dedication highlights why PPG is such a solid long-term opportunity. PPG remains one of the largest in its industry and sees the TAM being around $185 billion . Despite the recent runup of the share price, I think that PPG is at a decent price to start a position and will be rating it a buy as a result.

Solid Market Share Brings Growth

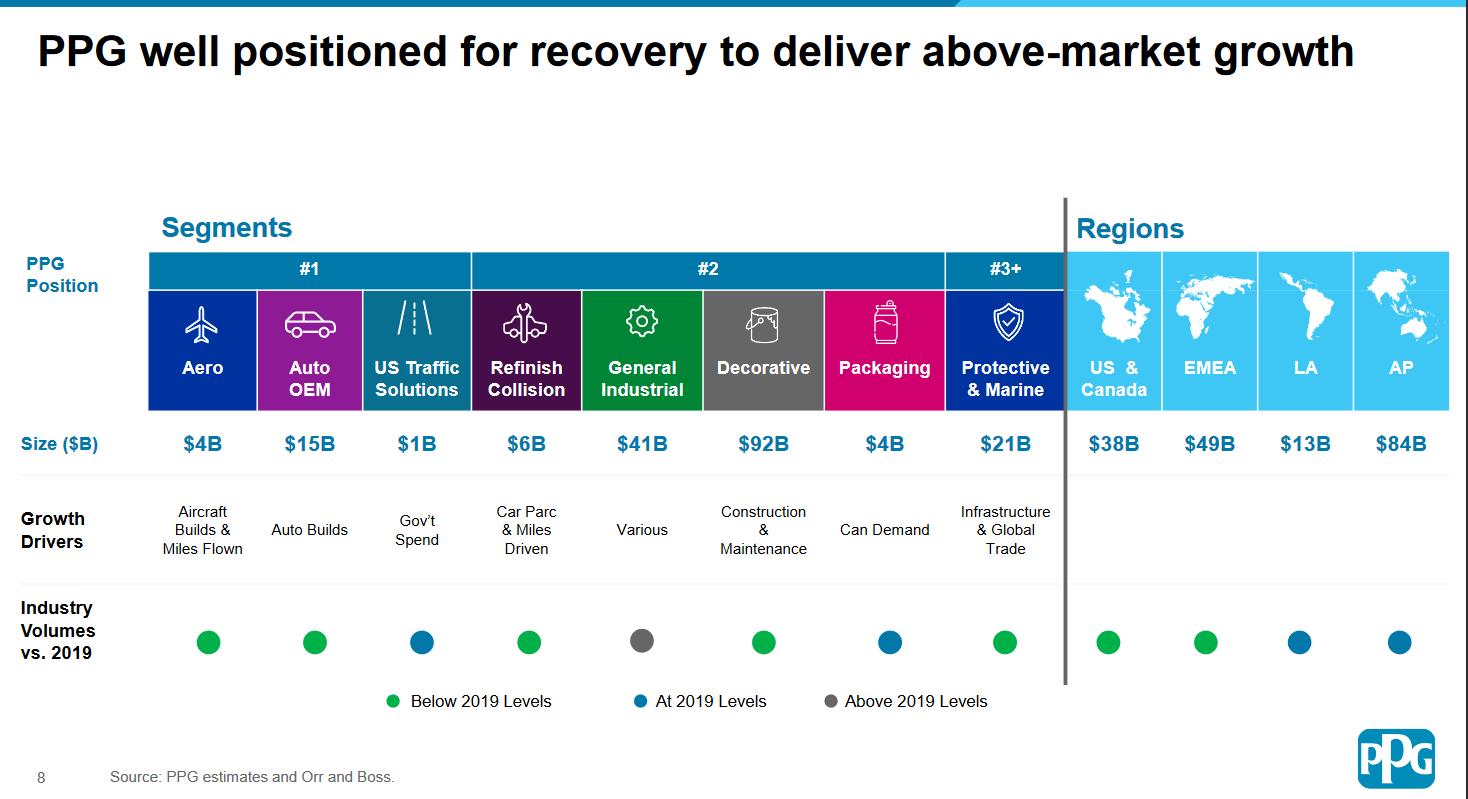

As I said at the beginning of the article, PPG has managed to grow its business into one of the largest in the industry. Right now they hold the number one position in the following segments, Aero, Auto OEM, and US Traffic Solutions. Those markets are worth a combined $20 billion. In Q1 of 2023 PPG achieved record sales of $4.4 billion which reflects that PPG can leverage its position and grow efficiently.

{kind=link}

Founded in 1883 PPG has had a long history of growing its brand. A reassuring fact about the company is that they don't necessarily rely on one region or market for its growth. The primary sales come from both the US and Canada, but Europe, the Middle East, and Africa still make up 31% of the sales.

Performance Coating (Q1 Report) Industrial Coating (Q1 Report)

Looking at how PPG managed to perform in the last quarter the most notable trend they had was simple price increases across the board. The selling prices for their products increased in the high single digits which most likely is a result of inflation and PPG being able to pass down costs to customers. This is a very good example of how PPG is able to leverage its position in the industry and still generate solid returns in difficult market environments.

But the acquisitions of new customers in the U.S. architectural space helped spark growth in the performance coatings segment. One of the risks I mentioned below here is that PPG is suspectable to currency fluctuations and that was visible in Q1 2023. In total, the sales were reduced by around $100 million as a consequence of the unfavorable currency translations. That then would be around $10 million in net income.

Balance Sheet Highlights (Q1 Report)

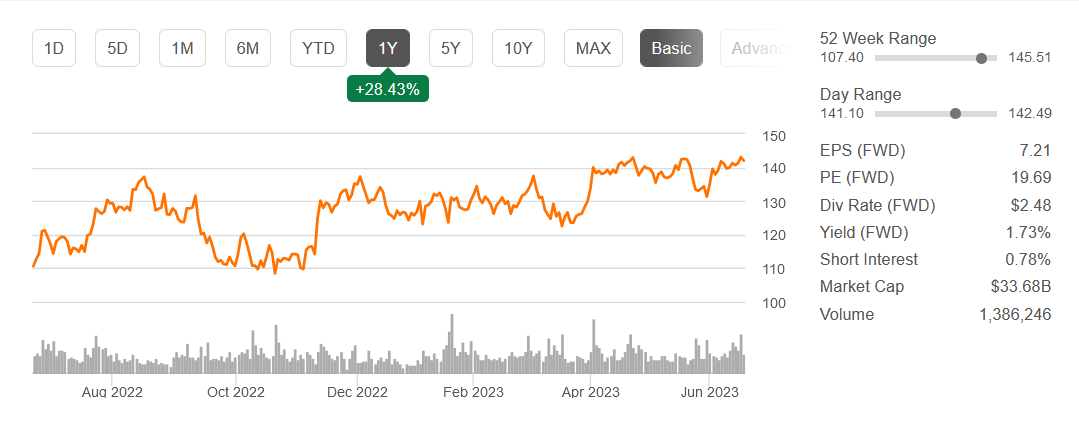

I think that PPG did solid work on their balance sheet for the quarter, reducing both the net debt QoQ and increasing the cash position. As I have made it clear PPG is a dividend addition to a portfolio given its 51-year history of raising it. The yield sitting at 1.73% right now looks compelling. For Q1 2023 they managed to distribute $145 million in dividends as the operating cash flows improved by $400 million YoY.

As for where PPG sees the market going they anticipate the macro environment to remain largely the same as in the first quarter, with stabilization of the economy actively in Europe and a slight improvement in China. Where they spot a slowing pace is in certain end-user markets where most of them are related to the construction industry. But there are positives too, the supply chain issues seem to be easing and PPG is experiencing a broader raw material availability. I think that will help maintain margins and result in consistent quarterly growth for the company.

{kind=link}

The second quarter will be all about maintaining and perhaps increasing margins I think as the company proves it can leverage the previous price increase and maintain them. That would be a very bullish signal I think that could lead to the share price increasing further and reaching new yearly highs. Adjusted EPS remains at $6.95 - $7.25 which on the high end would make PPG trade at an FWD p/e of 19.5, a number I think is fair to pay for the quality you are getting.

Risks

With PPG being so broad regarding where they do business, they are prone to some currency fluctuations. With most of the sales being in the US and Canada the increasing value of the US dollar seems to have offset some of the losses otherwise seen. But going forward, fluctuations like this will have an effect on the earnings from the company and I think that might help carry a slightly lower valuation for PPG.

Company Risks (Investor Presentation)

Where PPG themselves sees challenges is that the U.S housing market which is quite turbulent still but housing still remains in high demand . The increasing interest rates are also having an impact on PPG as they have been increasing their long-term debts constantly over the last few years and now have $7 billion in total. The interest expense for PPG has been increasing and sits on a TTM just under negative $200 million right now. Lowering the interest rates would most certainly impact the bottom line of PPG in a positive way I think.

Valuation & Wrap Up

Having exposure to the paint and coating industry might not be on every investor's mind. But PPG sees the TAM worth around $185 billion and with them being the second largest company they have shown they can leverage this position to pass down expenses to customers and maintain robust margins.

{kind=link}

The history of PPG shows that they have prioritized increasing the dividend and bringing value to shareholders. The company remains confident that it will perform well in 2023 and with the easing of supply chain issues I am optimistic about PPG growing sales at an impressive rate. I am rating PPG a buy.

For further details see:

PPG Industries: Strong Market Position Brings Margin Expansion