NGG - PPL Corp.: Record Is Too Short To Buy This Restructured Utility

2024-01-16 02:28:04 ET

Summary

- PPL Corporation is a holding company for four utilities serving 3.6 million electric and gas customers in Pennsylvania, Kentucky, and now Rhode Island, a new addition.

- PPL cut its quarterly dividend by 51.8% in 2022, leading to a drop in its share price. The current yield is 3.55%.

- At $27.00, shares look fully valued today, and there are more attractive yield alternatives. A longer track record is needed from PPL before investing.

- However, the company operates in favorable regulatory environments, with allowable returns on equity above national averages, and this may help in the long term.

PPL Corporation ( PPL ) has only existed in its present form since 2022. The past year, 2023, was the reshaped company’s first full year of operations. Today, PPL Corporation is a holding company for four utilities: PPL Electric Utilities Corporation (PPL, originally Pennsylvania Power and Light), Rhode Island Energy, Louisville Gas & Electric (LG&E), and Kentucky Utilities (KU Energy). The electric business has 1.5 million customers in Pennsylvania, 1.0 million in Kentucky, and 500,000 in Rhode Island. It serves several mid-sized cities including Louisville, Lexington, Harrisburg, Allentown, Scranton, and Providence. Gas is a much smaller percentage of operations with about 300,000 customers in both Kentucky and Rhode Island. The company is headquartered in Allentown and has a total rate base of $24.2 billion with a current market cap of $19.9 billion. According to Edison Electric Institute , it is the 19 th largest of the 44 U.S. investor-owned electric utilities. Standard & Poor’s rates the parent company as A-, or medium investment grade. Below are maps of PPL’s territory:

PPL Service Territory (2023 Investor Presentation)

In 2011, PPL acquired Western Power Distribution with 7.9 million customers in England and Wales. It held onto this asset for 10 years and sold in June of 2021 for about $10.5 billion. National Grid ( NGG ) acquired Western and assumed $8.9 billion in debt that PPL had taken on in its purchase. At the time, this debt would have equaled about a third of PPL’s market cap. In a related transaction , PPL acquired National Grid’s Narragansett Electric (now Rhode Island Energy) for $5.3 billion plus $1.5 billion in debt, but this deal was not closed until May 2022. PPL was able to net about $4.9 billion on these transactions (after taxes) and get all its business back in the states. At the time, Moody’s Investor Service said this was “an opportunity for PPL to improve its credit profile as it becomes a U.S.-only utility holding company with operations in three supportive regulatory jurisdictions.”

They Cut the Dividend in 2022

In March 2022, PPL reduced its quarterly dividend by 51.8% from $0.415 to $0.20. This was done before the completion of the Narragansett Electric acquisition but after the sale of Western Power. There was a “warning” of sorts about the dividend – it remained fixed at $0.415 all through 2020 and 2021, and the two years before that, in 2018 and 2019, the dividend growth was only 0.5% per year. This should have made dividend investors wonder what was going on.

The dividend cut was considered part of a reorganization that included PPL buying Narragansett Electric from National Grid ((NGG)). With the Western Power sale completed first, PPL used at least part of the money for purchasing stock and the balance to pay down debt. According to Edison Electric Institute: “the company completed a targeted $1 billion share repurchase program on December 31, 2021, which returned value to existing shareholders in a different manner than dividends.” This latter statement may be true, but the stock dropped about 13.0% in response to the dividend cut. I think many investors would have preferred to have the dividend.

PPL’s current yield is 3.55%, while the overall utility sector averages a 4.0% dividend. Today’s three-month treasury yield is 5.2% and there are money markets paying over 5.0%, like T. Rowe Price U.S. Treasury Money Fund ( PRTXX ), which pays 5.1%. Higher yields are also easily available at many other utilities like Duke Energy ( DUK ) at 4.22%, American Electric Power ( AEP ) at 4.32%, Avista Corporation ( AVA ) at 5.2%, or Pinnacle West ( PNW ) at 4.96%. An investor would have to get significant share price appreciation to make up for the lower yield, but I’m not sure that will happen in the near term as discussed below.

{kind=link}

Payout Ratio Over Time (Author Calculated)

The utility industry’s average dividend payout ratio was 69.4% in 2022. The payout ratio for PPL got rather high at 81.37% in 2020, and then in 2021 it reached 313.21% when PPG sold its UK utility Western Power. Thus the 2022 dividend cut. The payout ratio for 2023 was 61.29% and for 2024 it is estimated at 60.59%, these latter two figures being more in line with industry standards and more sustainable. However, since the dividend cut, the share price has been mostly range-bound and traded between $25 and $30.

{kind=link}

Share Price History (Seeking Alpha Charting)

2023: A Lawsuit Settled, A Fine Paid

Back in 2014, PPL sold non-regulated generating assets it owned in Montana. This spinoff became part of Talen Energy and it included several hydro assets. In 2022, Talen filed for bankruptcy , seeking to reduce $4.5 billion in debt. Talen then sued PPL regarding the 2014 sale, initially seeking $900,000,000 in damages. In December of 2023, PPL settled for $115.0 million. A second issue for the company last year was inaccurate billing in Pennsylvania for which the Public Utility Commission fined the company $1.0 million and asked PPL to write off $16.2 million in errors. I estimate that together all these cost the company about $0.18 per share in its final 2023 results.

Regulatory ROE > National Average

PPL operates in three main state regulatory environments and each is considered favorable. The Pennsylvania Public Utility Commission has five governor-appointed members, Rhode Island Public Utility Commission has three governor-appointed board members, and Kentucky Public Service Commission has three governor-appointed board members. Appointed members are typically considered more utility-friendly than members elected by a public that may look to the utility commission for lower rates.

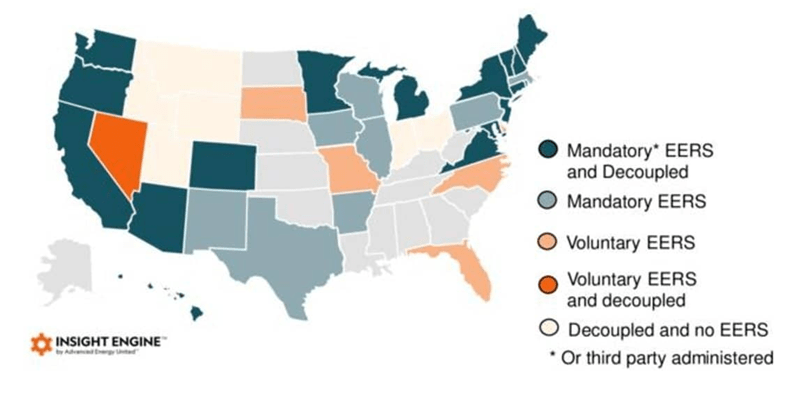

Of these three states, only Rhode Island is rate decoupled – meaning that the utility’s revenue is not strictly consumption-based, and it can earn an adequate return even if sales are lower than expected. Pennsylvania has discussed moving to rate decoupling in its legislature, but this has not yet happened.

The allowable return on equity in all three states is quite favorable compared to national averages. PPL's base return on equity ((ROE)) for Kentucky gas and electric was increased to 10.0% from 9.45% in June of 2023. Pennsylvania’s allowed return on equity is 9.95%, with add-ons like a pass-through of energy charges, and storm damage recovery. In Rhode Island electric transmission has a 10.57% return on equity with supplements that could raise it up to a maximum of 11.74%. Electric distribution is 9.275% and gas distribution is 9.275%, however both with incentives up to 10.275%. Most of these returns are well above the national average ROE, which as of September 2023 was 9.55% for electric and 9.66% for gas according to Gabelli Funds , (although Standard & Poor's lists the average electric ROE as 9.71%).

As far as electric rates, PPL was averaging $0.1230/kilowatt hour in 2022 and was at the middle of the pack for the US investor-owned electric utilities. Peer WEC Energy ( WEC ) was $0.1236, while Pinnacle West was at $0.1250; the cheapest was Otter Tail ( OTTR ) at $0.0842 per kilowatt hour and the most expensive was Sempra ( SRE ) at $0.3225 and Hawaiian Electric ( HE ) at $0.430 per kilowatt hour. This leads me to believe there is some room for PPG's electric divisions to ask for rate increases in the future.

A Costly Renewables Transition

{kind=link}

Debt Maturities (PPL Investor Presentation)

PPL has already reduced its carbon emissions by almost 60.0% from a 2010 base. However, the transition to renewables, away from carbon, will require substantial expenditures by PPL and the utility industry over the next two decades. According to analyst Woods Mackenzie , the estimated the total cost for the transition in the US will be $4.5 trillion, and will add substantially to utility rate bases.

Described as the most important climate change legislation produced, the Inflation Reduction Act of 2022 has set targets of a 40.0% reduction in greenhouse gases by 2030, down from a 2005 benchmark ( Edison Electric Institute estimates we are almost there now) and carbon-free by 2050. The legislation will achieve this by providing incentives to utilities that include a new tax credit for nuclear facilities, and credits for the next 10 years to install solar and wind generation. The act also provides $9.7 billion in loans for rural “electric cooperatives to purchase or build new clean energy systems.” Also important is the Bipartisan Infrastructure Law , which set aside $65.0 billion in grants for development of clean energy projects and upgrades to transmission lines, specifically to make them more resistant to climate change. PPL has already been awarded $100 million in grants from the Bipartisan Infrastructure Bill.

There are also state targets that will apply to PPL: Pennsylvania requires an 80% cut to greenhouse gas emissions by 2050, and Rhode Island's electric generation has to be 100% fossil-free by 2030, per its Renewable Energy Standard. Kentucky, on the other hand, currently has no emissions mandates or targets.

PPL’s 2023-2026 capital expenditure plan is $11.9 billion and is addressed at achieving climate goals, as outlined in the 2023 Investor Presentation . In Kentucky, PPL will replace four coal-fired power plants (Mill Creek at 600 megawatts) with gas and steam units generating 640 megawatts. This cost is estimated at $2.1 billion, with $10.0 billion needed to replace all coal generation by 2050. Kentucky also approved 1,000 MW of new solar and energy storage. PPL has submitted proposals for offshore wind generation in Rhode Island with a plan for 1,200 Megawatts. It is also working on modernizing the grid in this state.

{kind=link}

Energy Efficiency Resource Standards (Insight Engine)

Shares Look Fully Valued Now

In the third quarter of 2023, earnings were $0.43 per share. There’s really nothing to compare this to as Rhode Island Energy was only a part of the company for the second half of 2022, and Western Power, which had 7.9 million customers and was part of the company for 10 years, was sold at the end of 2021. Estimated annual earnings per share for 2023 were narrowed in the third quarter from $1.50 to $1.65, to $1.55 to $1.60 (Value Line estimates $1.55). The company also stated that it expects annual earnings growth of 6.0-8.0% through 2026. However, during the last year, Rhode Island had its fourth warmest winter on record, while winter in Pennsylvania was also one of the warmest on record, which reportedly impacted earnings. Now we have more unusual weather as an extreme arctic event could set new record lows this week, and in anticipation, natural gas prices have jumped more than 400%.

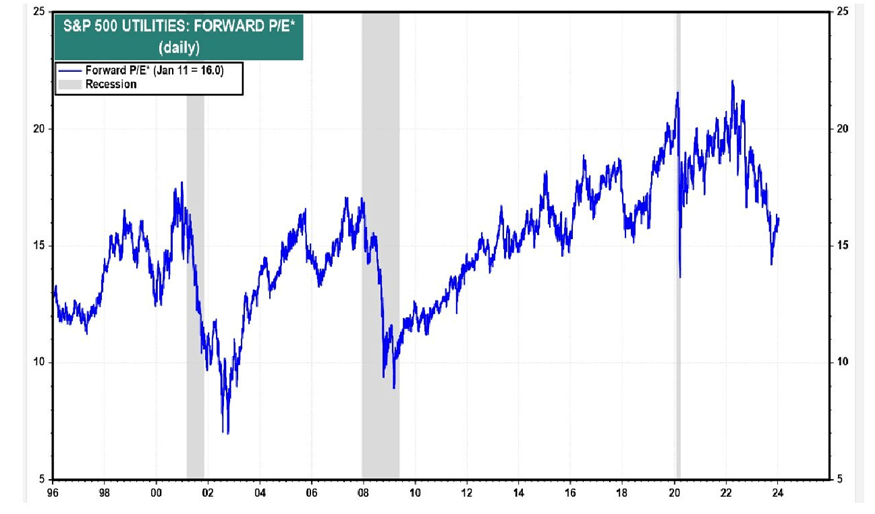

In 2023, PPL shares reached their low in October, when they dropped to $23.44, after the Fed’s September 20 th meeting and the subsequent published minutes , which indicated rates would stay higher for longer. Back then, interest rates were forecast to be above 5.0% through 2024. Utility multiples bottomed at just under 15.0 times earnings, as seen in the P/E chart for the S&P 500 Utilities from Yardeni Research . They have now rebounded to 16.0, but still per Morningstar, these are the about the lowest since 2009 . Gabelli Funds also published updated P/E multiples on January 4 th in their Utilities Insights . For all electric utilities, the forward P/E ratio is 15.6, while for gas utilities it is 15.2.

{kind=link}

January 11 Utility P/E Ratios (Yardeni Research)

{kind=link}

January 4 P/E Ratios (Gabelli Funds Insights)

I will use two methods, P/E multiple comparables and a discounted cash flow, to value PPL shares here. Despite the extreme weather, we have revised earnings guidance for 2023, and I have concluded at $1.55, at the low end of the range to be conservative. I also have a Value Line projection for 2024 of $1.70 earnings per share, an increase of 9.7%. Using the forward 2024 earnings estimate of $1.70, and Gabelli’s electric multiple of 15.6, the value would be $1.70 x 15.6 = $26.52.

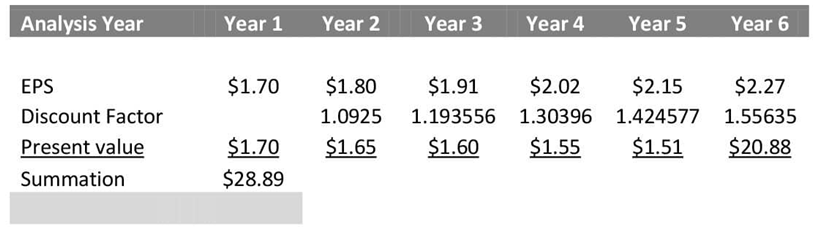

Alternatively, I used a discounted cash flow to value shares. With the 2024 estimate of $1.70 per share and an annual earnings growth rate of 6.0% (the low end of PPL's range), I have projected out five years. As a discount rate, I referenced the long-term average annual return of the S&P 500 over time, which has been about 9.8%. Warren Buffett has implied he uses a 10.0% rate of return for this kind of calculation. However, I assigned a 9.25% rate for PPL given its favorable regulatory environment and monopoly status in its territory. The reversion rate here was 7.0%.

{kind=link}

Discounted Cash Flow (Author Calculated)

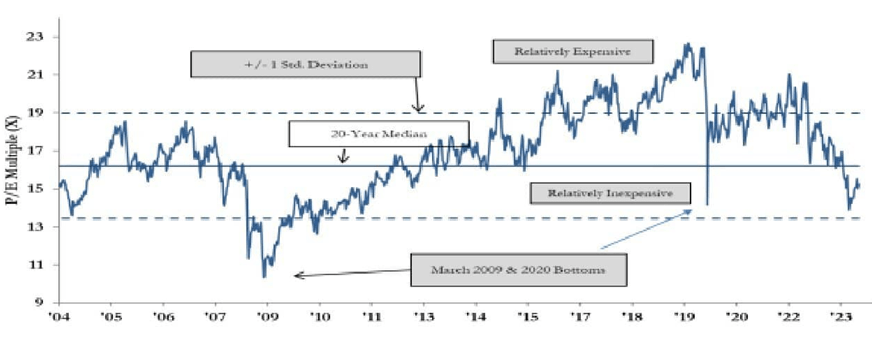

The numbers produced by these two methods indicate a value range of $26.52-$28.89, so a fair value of about $28.00 per share. PPL is currently trading at $27.08 so shares appear to be about fully valued today and within the range of values indicated. Below is a history of utility sector P/E ratios over time, as a point of interest, indicating that the sector is still slightly inexpensive.

{kind=link}

Utility P/E Ratio History (Thomson One, Gabelli)

A Few Risks to Outlook

PPL’s rates are only decoupled in Rhode Island, so in Pennsylvania and Kentucky its revenues are linked to usage. This means that an unusually warm winter or cool summer will lower earnings. Another area of risk is the Fed’s current higher rates - although we now know they are likely to cut in 2024, we just don’t know by how much or when. PPL’s long-term debt was $10.6 billion in 2021 or 31.9% of total assets. At the end of 2022, it was $12.9 billion or 34.1% of total assets, a slight increase. As of the end of the third quarter 2023, it has jumped to $14.5 billion or 37.6% of total assets. A cut in rates will be beneficial to PPL, just as it will be to many utilities.

{kind=link}

Upcoming Debt Maturities (PPL Investor Presentation)

Conclusion

This utility was only recently reshaped, with the acquisition of the Rhode Island operations and the sale of UK operator Western Power to National Grid. The dividend was cut in 2022 and is now only 3.55%, even though management says it will increase going forward in line with earnings at 6.0-8.0% per year. While an increase could come in March of 2024, a dividend cut is always a warning. And it’s hard to be enthusiastic about this dividend yield when money market funds are still paying over 5.0%. Meanwhile, the dust hasn’t yet settled from the new acquisition. Add the fact that shares are about fully valued at their current price of $27.08 and there are just not enough positives to invest in PPL at this point. I will wait and let the company develop a new track record from which to judge, and maybe an opportunity will emerge down the line.

For further details see:

PPL Corp.: Record Is Too Short To Buy This Restructured Utility