PPL - PPL Corporation's Geographic Footprint Limits Upside

2023-12-06 11:23:18 ET

Summary

- PPL Corporation shares have underperformed due to higher rates and concerns about interest costs for capital programs.

- Q3 earnings were slightly ahead of expectations, driven by increased rates and cost discipline, despite lower electricity usage.

- PPL's capital program aims for 6-8% earnings growth through 2026, but population and economic trends in its service regions pose risks.

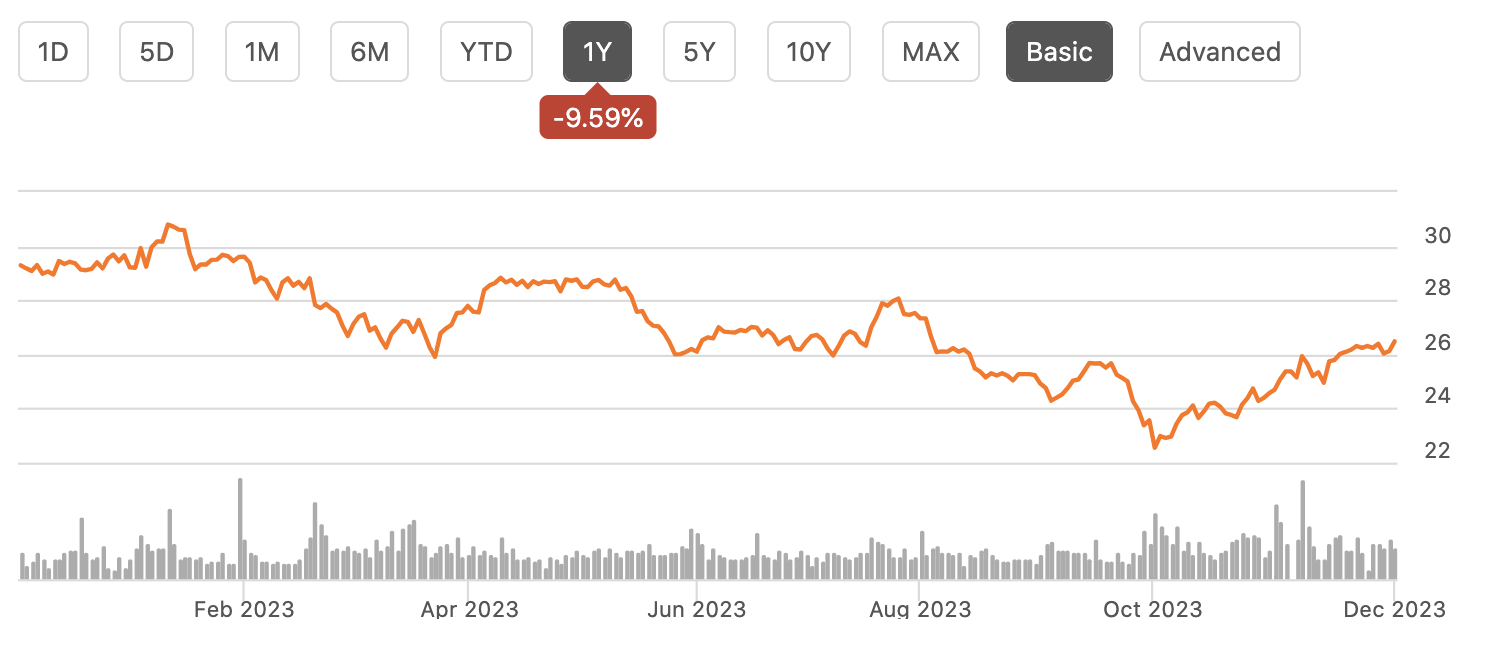

Shares of PPL Corporation ( PPL ) have been a poor performer over the past year, losing about 10% of their value. Utility stocks have been negatively impacted by higher rates, as dividend yields are less compelling when treasury bond yields rise. Moreover, higher interest cost for their large capital programs is a concern for investors. As the ten-year treasury yield (US10Y) has fallen in recent weeks, we have seen shares recover some losses. Shares are likely to continue to respond to rate moves, but I view them as broadly fair value relative to other utility opportunities.

{kind=link}

In the company’s third quarter , PPL earned $0.43 in adjusted earnings, about a penny ahead of consensus . This was up about 5% from last year. While revenue fell 4% from last year, this was primarily due to lower fuel and commodity costs, which are passed through to customers; as a regulated utility, PPL is not taking direct commodity risk. Alongside these results, management narrowed guidance to $1.55-$1.60 keeping the same $1.58 midpoint.

Earnings growth was powered by increased rates in its Pennsylvania, Kentucky, and Rhode Island utilities, alongside strong cost discipline. Management aims to cut $175 million in operating and maintenance cost by 2026. So far, it estimates it has delivered $50-$60 million of those cuts. That is evident in the fact O&M spending is $41 million lower than last year at $637 million. This was partially offset by interest expense, which rose $29 million to $165 million as the company refinanced $1.7 billion in debt and issued $1.4 billion in incremental debt. Interest expense was a $0.03 headwind to results.

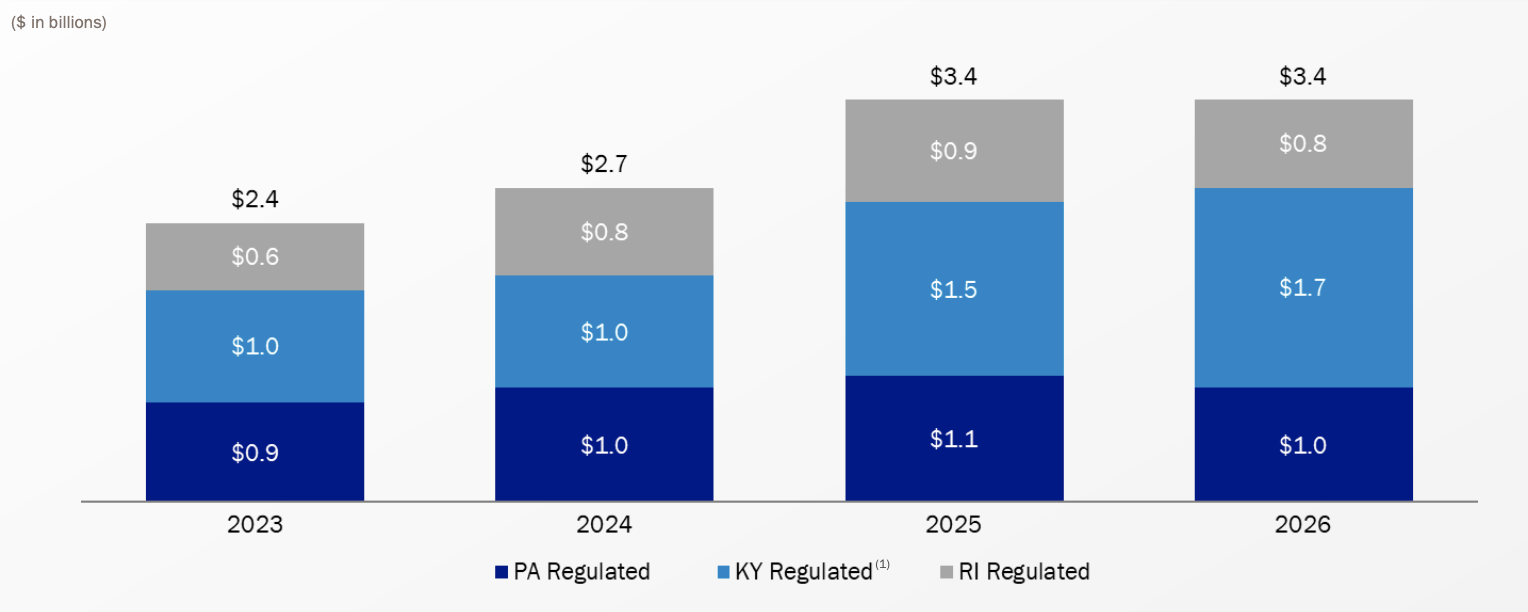

This new debt is funding its large capital program, with $2.5 billion in 2023 cap-ex. This is the beginning of a large multiyear capital program across its three regulated utilities. PPL is forecasting 6-8% earnings growth through 2026 via $12 billion in capital spending. Based on its capital budget, it expects to increase the regulated rate base by 5.5% over the next three years to $30.1 billion from $24.2 billion last year, with growth accelerating in 2025-2026.

{kind=link}

Regulated utilities earn a return on equity and recoup the cost of their capital improvements to enhance reliability, or make their grids cleaner. For instance, PPL has $10 billion in capital needs to retire its Kentucky coal-fired plants. 20% of generation comes from coal today; it expects to reduce this to 13% by 2026. As such, rate-base enhancing cap-ex spending will deliver higher cash flow, earnings power, and dividend capacity over time. PPL has also sized its program so that no equity issuance is needed to support its capital program.

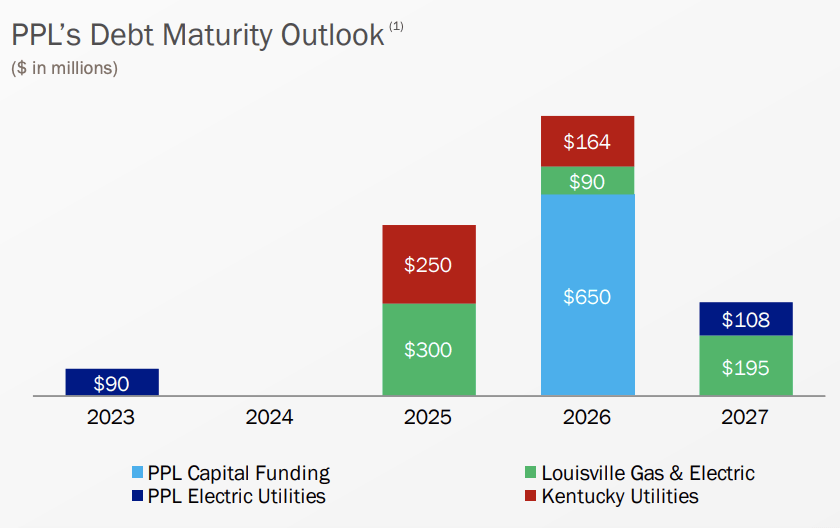

I am somewhat cautious about this outlook given the fact the company is targeting faster earnings growth than rate base growth. Now, reduced O&M spending will flow through to the bottom line and accelerate earnings, but some of this will be offset by higher interest expense, as we are already seeing. Now fortunately, while PPL has $14.8 billion in debt, most of this is long-dated with no maturities next year and just $550 million in 2025. As such, it will not have to roll over debt at higher rates for some time. This will help to limit the increases in interest expense, but increases are still likely to occur.

{kind=link}

One thing a utility cannot readily change is the region that is services. This is an issue I see for PPL, which make me concerned that growth ambitions will not be fully realized. In the last quarter, electricity volumes were down 1.8% in Pennsylvania and 1.4% in Kentucky, normalized for weather. Including weather, they were down 3.5% and 2% respectively. Not all years are equally hot or cold, which impacts how much energy consumers use for air conditioning or electric heat. That is why I like to focus on weather-normalized results to see underlying demand. The declines across its two primary utilities are concerning. While all segments were down, the company has seen some weakness in industrial demand with PA down 2.7% and KY down 2.3%, due in part to normalization from steel production following its post-COVID surge.

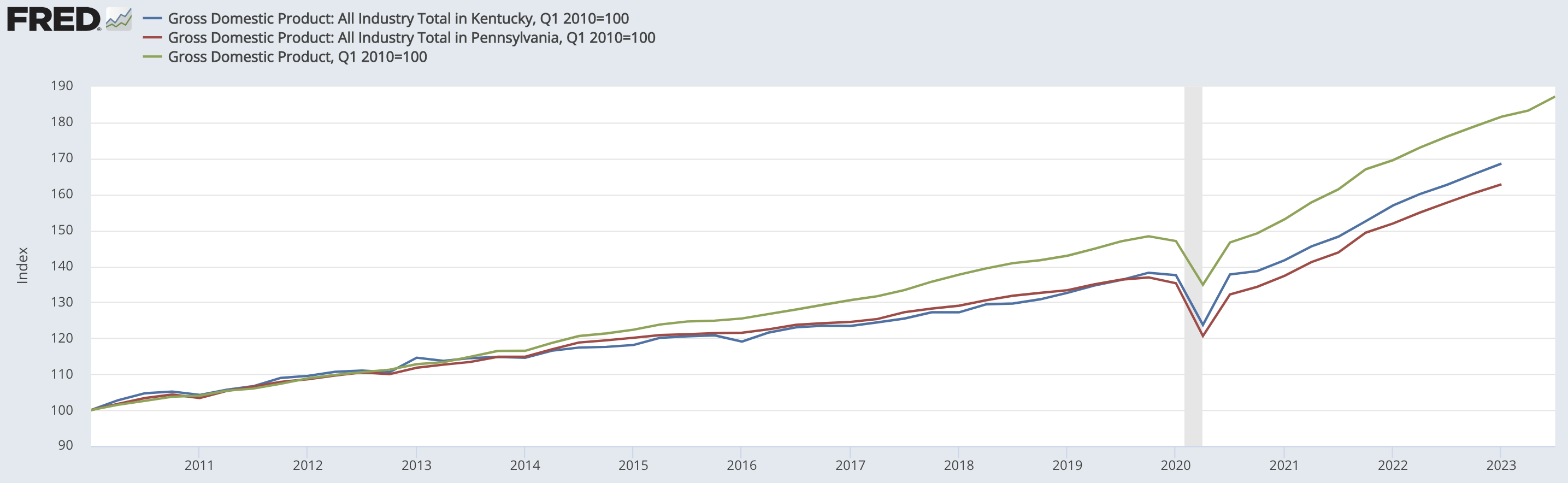

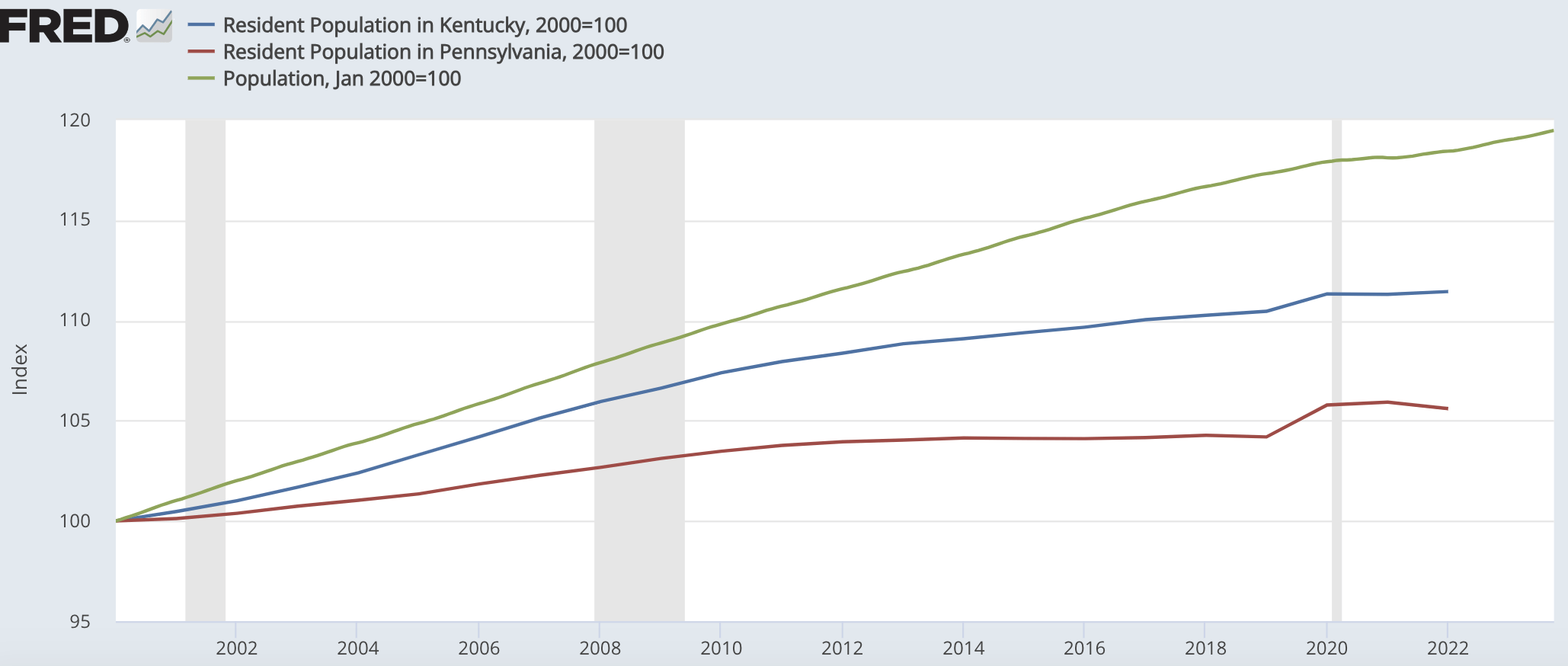

As you can see below, PA and KY have been significant economic underperformers over the past ten years. In the long-run, electricity demand is tied to economic growth. More sluggish growth means less electricity demand. These two states have been structural underperformers, as they have seen coal production decline and have limited exposure to high-tech industries, though increased natural gas production in PA has been a tailwind.

{kind=link}

Economic growth is comprised of two things fundamentally, population growth and productivity growth. The core culprit for their economic underperformance is weak population growth in both states, as you can see below. In recent years, we have seen significant population migration towards the Sun Belt and away from the Rust Belt and Northeast. A combination of taxes, weather, economic opportunity, and cost of living are likely contributing to this trend.

{kind=link}

PA & KY have been on the losing end of this migratory pattern. Again, there is nothing PPL about this trend. It is not as though a utility can pick up its power plants and move them from Pittsburgh to Miami. Its PA and KY utilities will always serve PA and KY. Management is doing a solid job operating within these states, as evidenced by the modest earnings growth despite lower usage as it has been able to earn higher rates. Ultimately though, it will be easier for a utility to grow earnings overtime when the population is growing more quickly. I see little reason to expect population and migratory trends to reverse recent patterns.

The more customers grow, the more widely a utility can spread its rate base, reducing the per capita base growth. This helps to limit to bill increases, which regulator and politicians clearly watch. Slower growth risks increasing customer bills more quickly, which is already a concern of mine given faster targeted earnings growth than rate base growth. As such, I see risks skewered to PPL under-achieving its earnings growth targets, even as it delivers on its capital program.

With a $34.3 billion enterprise value, PPL is trading at a 1.42x enterprise value/rate base ratio. Notably, NiSource ( NI ) trades at about 1.45x EV/rate base, roughly equivalent. While it also targets 6-8% earnings growth, it expects its rate base to grow slightly more quickly than earnings, an assumption I feel more comfortable with. It also has been able to dispose of assets at premium valuation of 1.85x/rate base, creating some upside from further stake sales.

CenterPoint Energy ( CNP ) has a lower starting yield of 2.8% vs. PPL’s 3.6% yield, but given its exposure to the faster growing Texas market, it may find it easier to achieve its growth targets. After all, strong customer growth there has kept bills flat for a decade. Ultimately, PPL will be able to deliver some earnings and cash flow growth from higher rates, but I expect earnings growth to be closer to 5-6% than 7-8% given its capital program and local economic dynamics. That still provides a path to about an 8-9% long-term return based on its starting yield and its ability to grow its dividend alongside earnings.

I view that as a market-like return, making PPL Corporation shares fairly valued and a hold. I think investors would be better served looking at NI & CNP, which are likely to offer a better combination of dividend income and growth based on their geographies and capital structures.

For further details see:

PPL Corporation's Geographic Footprint Limits Upside