PRDSY - Prada: Q3 Sales Soften Market Multiples Stay High (Rating Downgrade)

2023-11-01 12:24:30 ET

Summary

- Prada's trading update for 9M FY23 shows healthy revenue growth for the period, but there's a slowing down in Q3 FY23.

- A combination of an unfavourable exchange rate and a genuine slowing down in demand in key markets indicates that growth in the future could be more muted.

- Prada's market multiples compared to peers, don't encourage confidence in the stock right now when seen in combination with softening revenues.

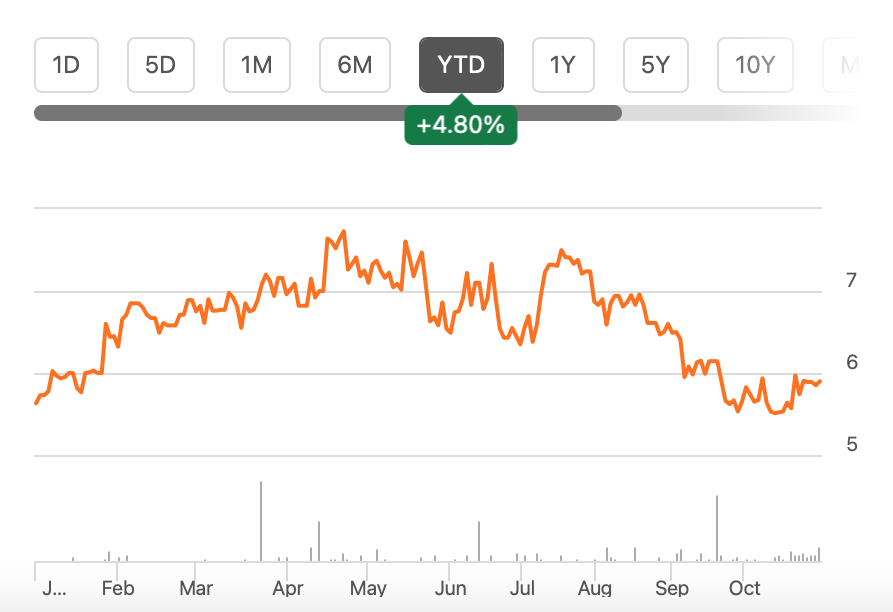

Luxury fashion company Prada ( PRDSF ) hasn’t had much of a year at the stock markets this year, up by just 4.8% year-to-date [YTD]. But could its trading update for the first nine months of 2023 (9M FY23) be exactly the catalyst the stock needs? The reason I speculate this is going by the 9.4% increase in the price of its ADRs ( PRDSY ) after it released its figures today. Let’s find out.

{kind=link}

Price Chart (Source: Seeking Alpha)

Decent results for 9M FY23

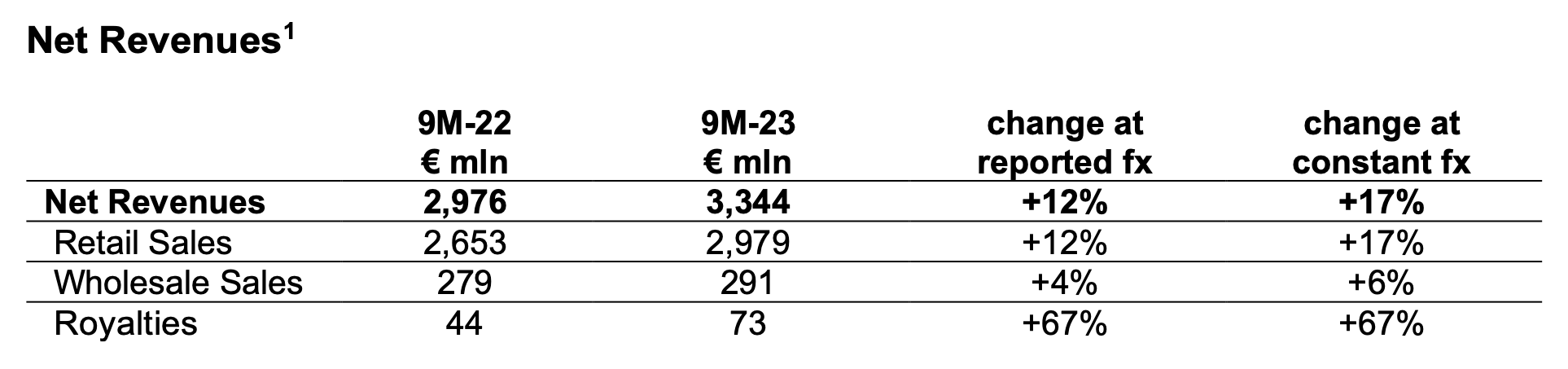

The update isn’t bad at all on the face of it. Prada’s net revenues have risen by 17% year-on-year (YoY) at constant exchange rates. This is a good number, but it is a softening from the 20% growth seen in the first half of the year (H1 FY23). Unfavorable exchange rates have also resulted in a far smaller growth rate of 12% in reported terms, compared to 17% in H1 FY23.

{kind=link}

Source: Seeking Alpha

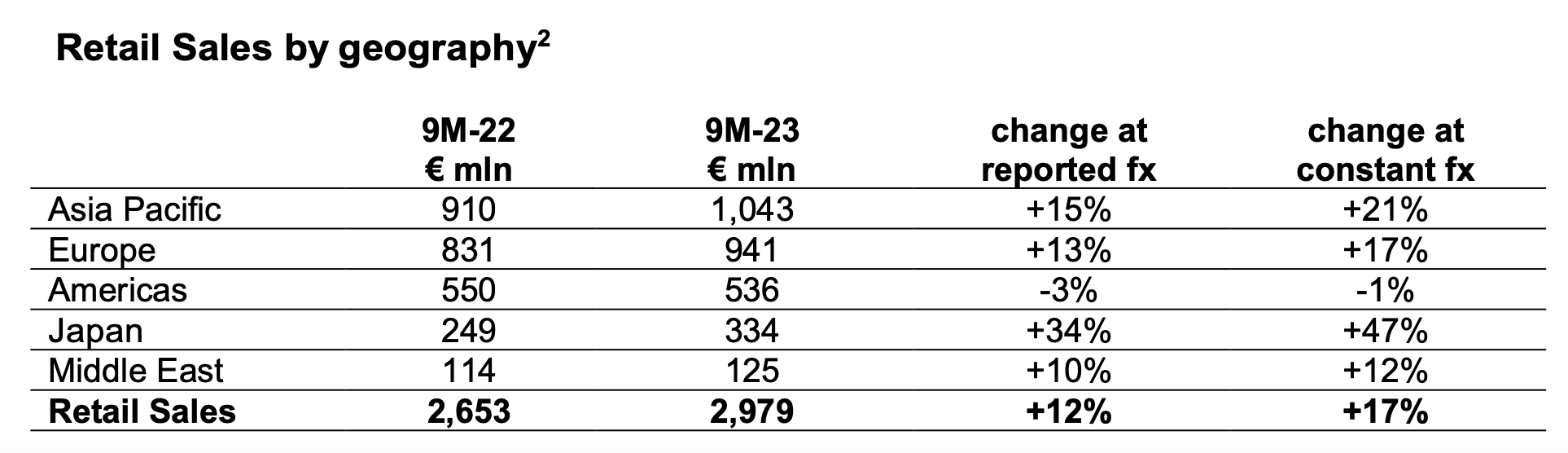

The geographical split-up of revenues is also largely good. In providing figures by geography, the company focuses on retail sales only, which is in any case the lion's share of net revenues.

Sales in Asia Pacific, its biggest market, grew by a healthy 21% at constant currency. This is a small cooling off from H1 2023 when they grew by 25%. But there could be a base effect at play here since the company mentions “significant disruption” during Q2 2022, presumably on account of the lockdown in China during the time, which impacted sales particularly favourably. By corollary, a firmer base in the latest quarter means lower Q3 sales growth, which is explored in greater detail in the next section.

{kind=link}

Source: Seeking Alpha

Sales to Europe also grew by a healthy 17%, which is a good sign. They have declined from 24%, indicating a slowdown, but overall growth is still healthy. Americas' sales continued to shrink by 1%, the same as in H1 FY23. The good news, if it can be called that, is that the market hasn’t taken a turn for the worse, but it isn’t exactly adding to sales growth either.

Q3 sales disappoint

The overall picture, however, hides the grim Q3 FY23 sales in reported terms, which aren't reported separately. Net revenues showed a far smaller growth of 3.4% YoY during the quarter. All the key markets of Asia Pacific, Europe and the Americas, which account for 75% of net revenues, have reported softening sales.

Source: Prada, Author's Estimates

Asia Pacific revenues have seen a growth slowdown to 2.2%, which is concerning considering that the region's robust demand has held up luxury demand not just for Prada during the earlier part of the year, but also for other luxury companies. The softening can then indicate that the sector slump has started.

Sales to Europe also grew by just 4.1% during the quarter, also a sharp drop compared to the growth seen YTD. Not too long ago, the Swiss luxury company and Cartier owner Richemont ( CFRUY ) had sounded a warning about slowing sales in the region due to inflation, which has now come to pass. Americas' sales showed a decline of 7.9% during the quarter in reported terms.

However, I don't believe it's all downhill from here. First, the picture for Q3 FY23 is obfuscated by the availability of only reported numbers, whereas constant currency figures would be the true measure of consumer demand. Prada does point out that in Q3, retail sales as such grew by 10% (at constant currency).

Sales could also look significantly better in Q4 on account of the festive season coupled with the low base effect from Asia Pacific’s revenues at the same time last year. But, it’s also clear that luxury demand is indeed slowing down.

The outlook and market multiples

Prada’s 9M 2023 net revenue growth in USD terms is now at 12.3%, almost the same as the 12.2% forecast by analysts for the full year FY23 as well. Let's stay with these, to assess what continued healthy growth in Q4 FY23 would mean for the market multiples.

If growth stays at this level for the full year, coupled with a net margin of 11.1% profit growth can still be healthy. I had made the net margin assumption the last I wrote about Prada based on the average of H1 FY23 and full year FY23, considering that margins could also be impacted in H2 FY23 by a relatively weak demand environment. This yields a net profit growth of 23%.

The resulting forward P/E is now at 24.9x, compared to 23.7x last month, since the price has inched up in the interim. This is higher than that of peers like LVMH ( LVMUY ) and Richemont, which are at 20.9x and 15.3x respectively. I’ve omitted Hermès ( HESAY ) and Kering ( PPRUY ) from the analysis, since they are outliers. Hermes typically has a higher P/E than the rest while Kering’s poor performance and company related challenges have dramatically reduced investor interest in it.

Prada's trailing twelve months [TTM] GAAP P/E at 24.2x has the same trend as the forward P/E. It compares unfavourably to LVMH at 20.4x and Richemont at 15.8x.

What next?

Prada's story so far is quite likely telling of what to expect from luxury demand in the foreseeable future. While the overall picture still looks good, signs of strain are becoming very visible, as evident from the Q3 sales figures. An unfavourable exchange rate drags reported sales down further.

It's also likely that Q4 figures would look relatively better, on a base effect and festive demand, keeping full-year growth buoyed. But further slowing down going into 2024 cannot be ruled out.

At this time, I believe Prada is at a disadvantage since it is valued higher than its peers. It's tough to see much further upside to the stock now, especially after its robust performance today. I believe some price correction is due now, and at any rate, there's unlikely to be much price rise. I'm downgrading Prada to Sell from Hold. This can change if its profits for the remainder of 2023 turn out significantly better than expected or if its 2024 outlook is optimistic.

For further details see:

Prada: Q3 Sales Soften, Market Multiples Stay High (Rating Downgrade)