CFRHF - Prada: Softer Outlook And Still High Market Multiples

2023-09-30 21:57:06 ET

Summary

- Prada's ADR has seen a 23% drop since April on a weakening sentiment for the luxury sector.

- This is despite the company's financials showing strong revenue growth and improved operating margins in H1 FY23.

- Expectations of a significant slowdown in revenue growth for H2 FY23 and Prada's elevated market multiples, however, still encourage caution.

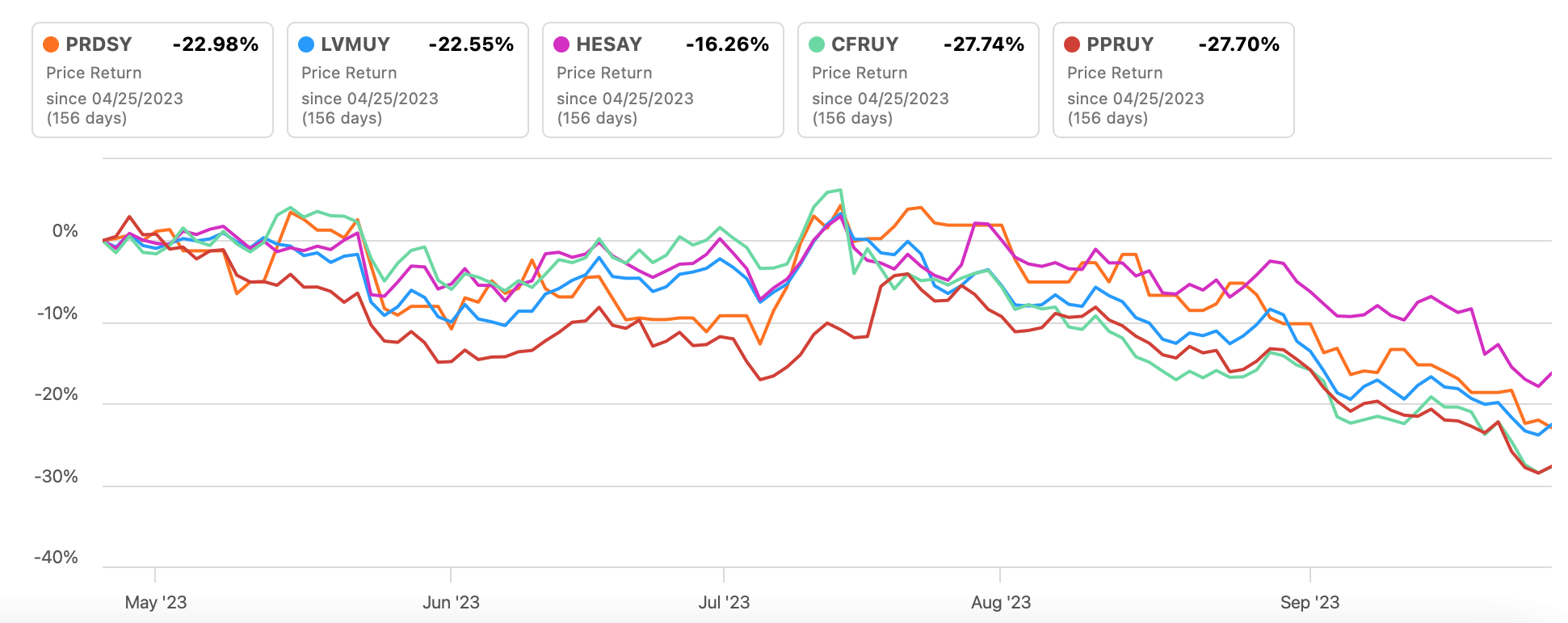

This is a challenging time for luxury stocks and Prada S.p.A. ( PRDSF ) is no exception. Since the last time I wrote about it in April , its ADR ( PRDSY ) has seen a 23% drop. This is similar to its peers' performance, except Hermès ( OTCPK:HESAY ), which has seen a smaller decline.

Price Returns (Source: Seeking Alpha)

{kind=link}

As a result of the decline however, its trailing twelve months [TTM] GAAP price-to-earnings (P/E) ratio has dropped sharply to 22.9x from 39.1x the last time I checked. At that time, I had given it a Hold rating based on its elevated market multiples, and despite its strong fundamentals.

This raises the question: Is Prada a Buy now?

Quick Recap

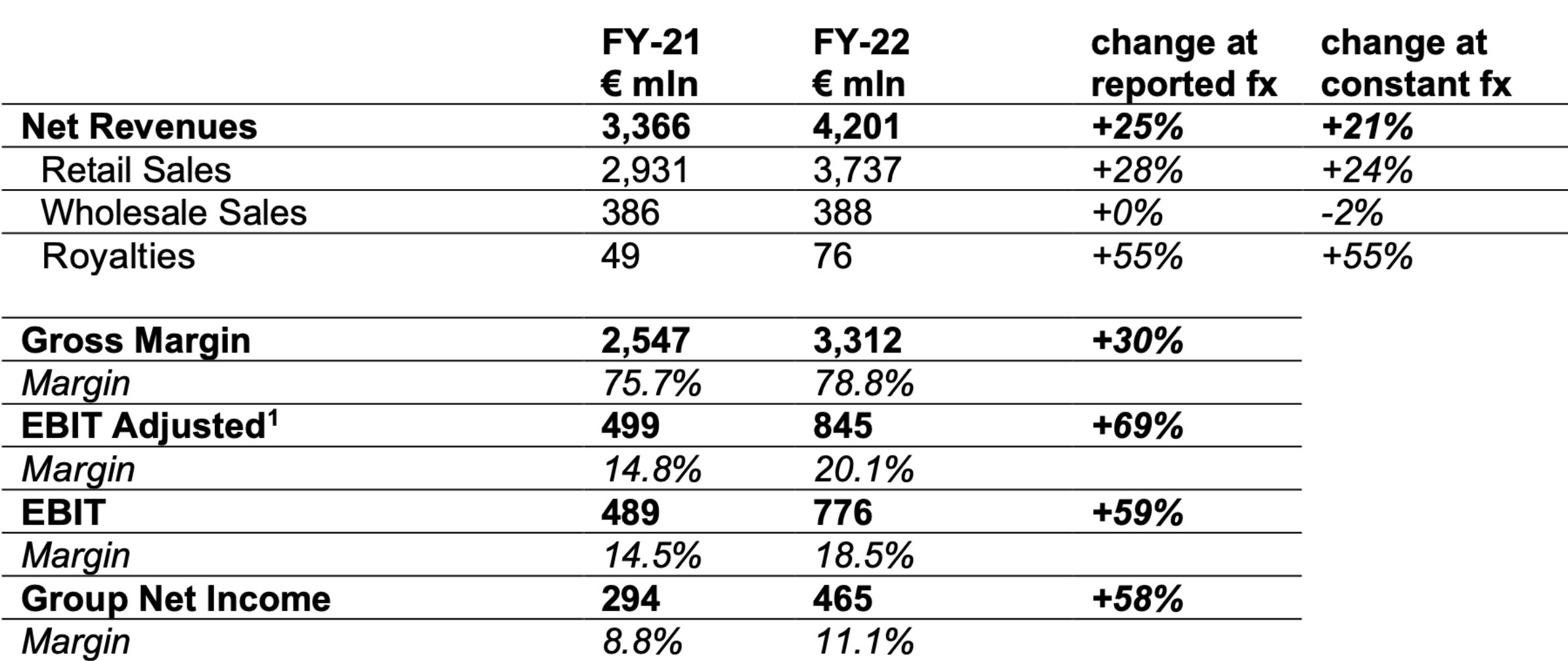

To assess this, I look at how its financials have changed in the past months. But first, a quick recap of where it was at the last I checked. At the time, its full-year 2022 (FY22) results were available, which showed both strong revenue growth and improved operating margins (see table below).

Key Financials, FY22 (Source: Prada)

{kind=link}

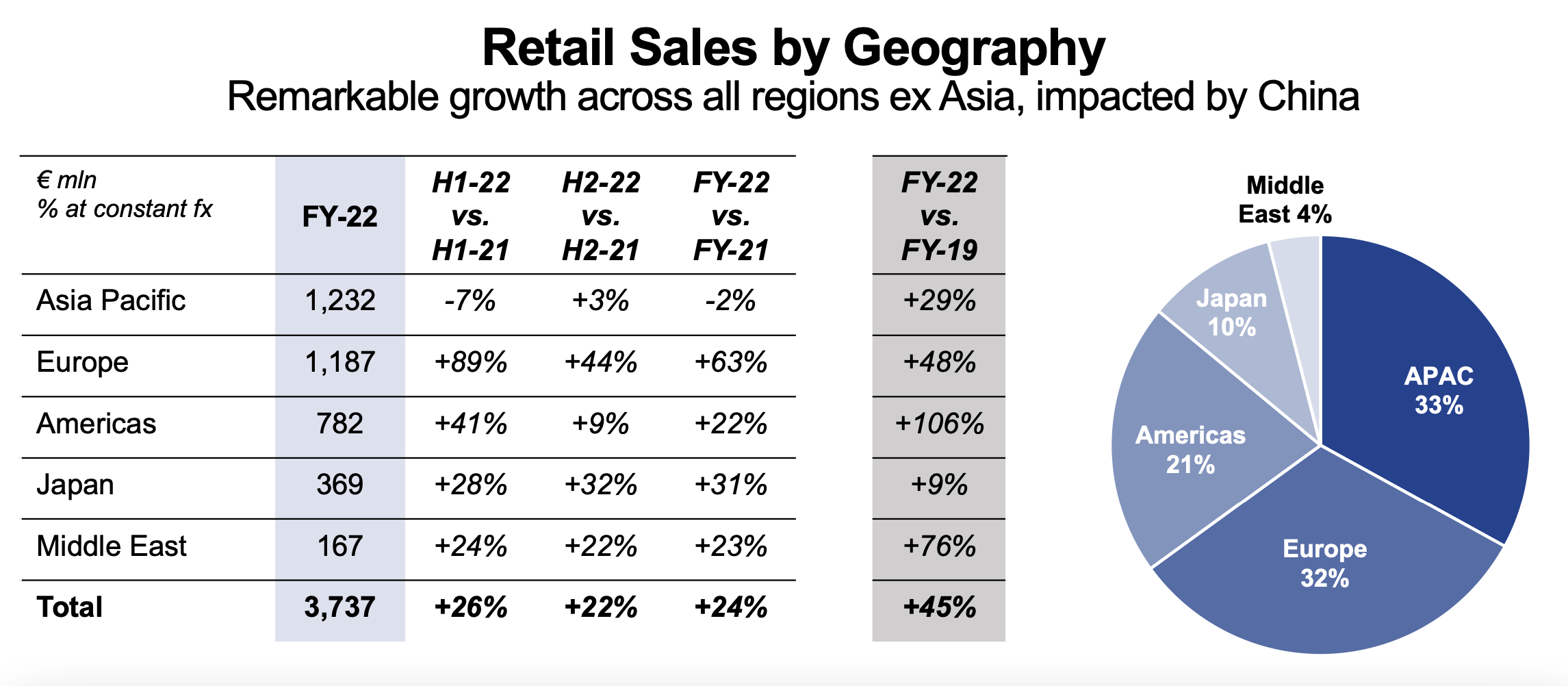

The second half of the year showed a softening in retail revenue growth from the Americas, adding to sluggish performance from Asia Pacific, its biggest market, because of lockdowns in the big China market (see table below). However, with the relaxation of COVID-19 regulations in China, there was a possibility of a surge in Asia-Pacific demand, even as the Americas could continue to soften.

{kind=link}

Latest financials

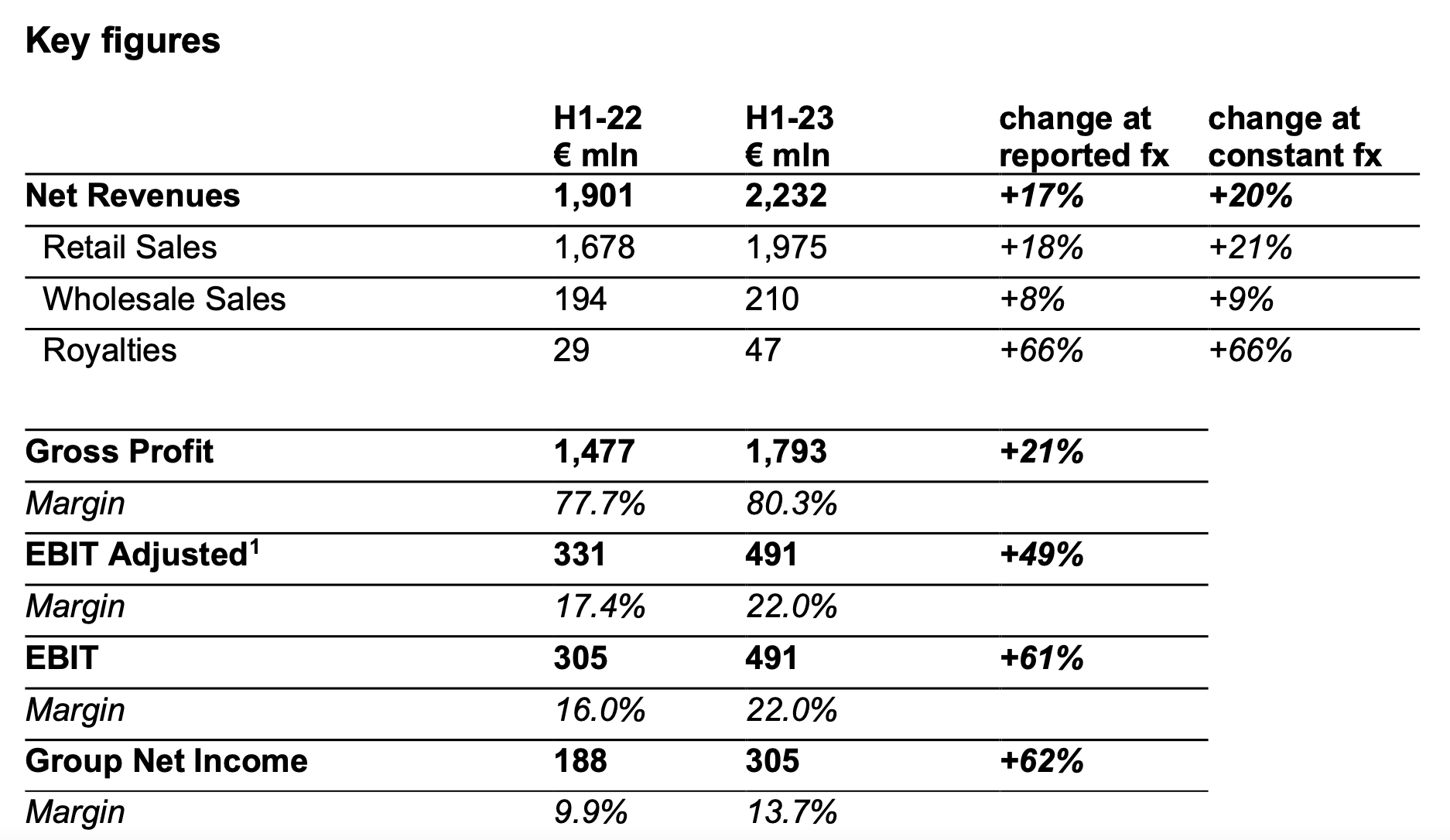

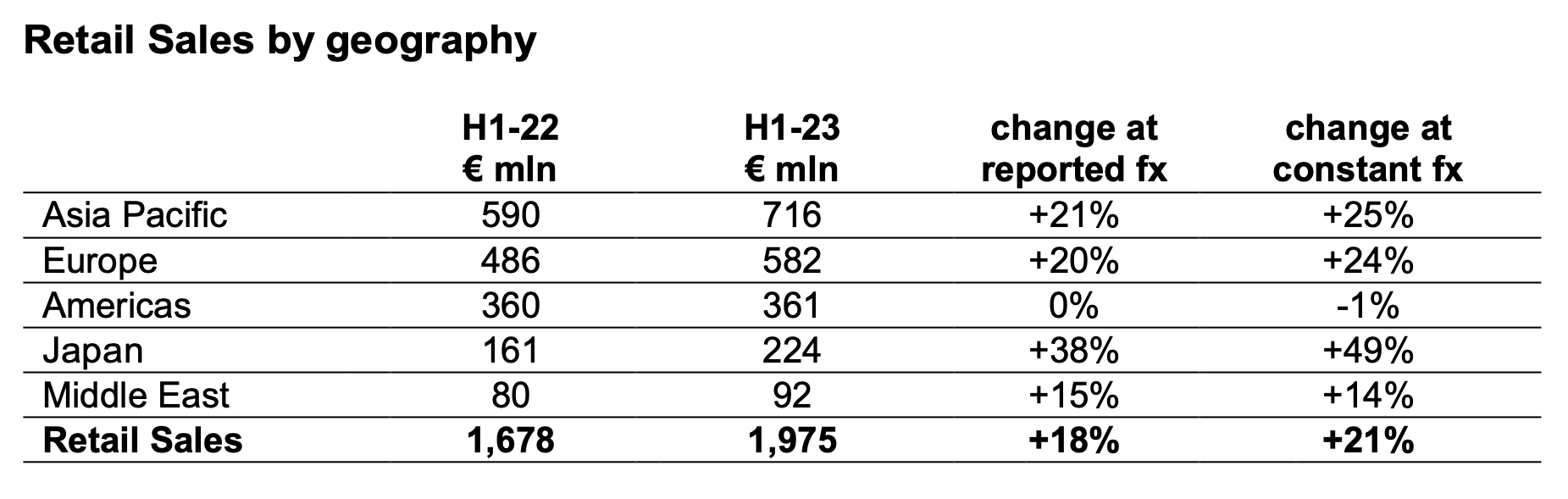

The expected geographical trends have played out in the first half of this year (H1 FY23), resulting in revenue growth of 20% year-on-year (YoY) at constant currency, almost the same as the 21% seen for the full year FY22.

Key Financials, H1, FY23 (Source: Prada)

{kind=link}

Asia Pacific picked up with 25% growth, while the Americas’ saw a small sales contraction (see table below). Encouragingly, sales from Europe also showed robust growth. This is particularly encouraging for the company since its Europe market was almost as big as its Asia Pacific market as of FY22. In fact, to this extent, it's also distinct from luxury peers who often see a substantially bigger Asia Pacific market compared to Europe.

On the downside, it can also imply a bigger dent in demand if the region slows down. There have been recent warnings about softening demand from the region on inflation by Richemont ( OTCPK: CFRUY ), which may well have had a sentimental impact on luxury stocks across the board, as it did for Richemont.

{kind=link}

Reported sales also showed a healthy 17% increase, but were lower than the 25% seen last year, reflecting the unfavourable exchange rate effect so far this year.

The highlight continued to be expanding margins, with the gross profit margin rising to 80.3%, from the already-high 78.8% in FY22. The operating margin also rose to 22% from 18.5% last year, as the rate of increase in costs slowed down. While the growth rate in cost of revenues fell to a third of that in H1 FY22, operating expenses’ rise fell to half of last year’s growth. These are good signs for the company’s full-year profits, even if revenue growth slows down, as is discussed next.

The outlook

The second half of the year is unlikely to be quite so buoyant for Prada, however. Analysts pencil in a 12.2% revenue growth in FY23 (in USD terms), down from a rise of 17.4% last year. This indicates a substantial drop in growth in H2 FY23 to 6.4% from 18.6% in H1 FY23.

On the face of it, this looks like a glaring drop. But if demand growth in Europe slows down, the Chinese economy also cools off and the exchange rate continues to be unfavourable, it’s possible. This is especially so considering that Prada hasn’t always been a fast-growing company. In fact, just before the pandemic, in 2018 and 2019, its revenues grew at under 1%.

So let’s go with it. Now, let’s also assume that the company’s margins are also impacted in a weaker demand environment. Here I’ve considered the full-year FY23 margin to be the average of 11.1% in FY22 and 13.7% for H1 FY23. This still results in an almost 23% net profit growth, even though it's a cooling off from the 63.7% rise (in USD terms) seen in H1 2023.

The market multiples

From the net profit value, we get ta forward price-to-earnings (P/E) ratio of 23.7x. This is higher than the corresponding ratio for all the other luxury companies with bigger market capitalisations than Prada, save Hermès, which is at 42.9x. But HESAY is always an exception, so the real comparison is with LVMH ( LVMUY ), Richemont, and Kering (PPRUY). These are at forward ratios of 20.7x, 16.9x, and 1.4x, respectively.

Exactly the same trend shows up for its TTM P/E ratio, with Hermes at 44.2x, LVMH at 21.4x, Richemont at 16.1x, and Kering at 15x, compared to Prada at 22.9x.

The point here is that it’s hard to justify any upside for Prada, especially now that demand is expected to wane. I do expect that if revenue growth doesn’t decline as sharply as analysts project, and the net margin also stays elevated, the forward P/E at least could look more attractive. That's possible, considering Prada's strong growth in Europe in the first half of FY22. But that remains to be seen.

What next?

The full Prada picture answers the initial question clearly, it’s still not a Buy. Positive as its H1 FY23 numbers are, with healthy revenue growth and margin expansion, there are downsides to consider too.

First, there are expectations of a significant slowdown in revenue growth for H2 FY23 as key markets like the Americas, Europe, and the Asia Pacific can see a cooling off. Unfavourable exchange rates don’t help either.

If Prada had always shown sustained revenue growth, I’d take these estimates with a pinch of salt. But as its pre-pandemic numbers show, it’s possible for its revenue growth to slow down to a crawl.

Next, even with a sharp drop in its TTM P/E, it’s still pricier than its luxury peers. It’s the same story with the forward P/E. A higher P/E could be justified by Prada’s good growth if the market was in an expansionary phase. But that’s not the case either. Right now, the market multiples only encourage caution. I’m reiterating a Hold on Prada.

For further details see:

Prada: Softer Outlook And Still High Market Multiples