PRDSF - Prada: Strong Performance But Pricey

2023-04-25 11:23:47 ET

Summary

- Prada has a lot going for it. The Italian luxury company's 2022 performance was strong and it is optimistic about growth this year too.

- However, its operating margin is lower than that of peers, as is its 5-year revenue CAGR. Its P/E is also elevated compared to the luxury industry.

- If it sustains growth in the first quarter, an update for which is due in May, a better picture will emerge on whether it is one to Buy now.

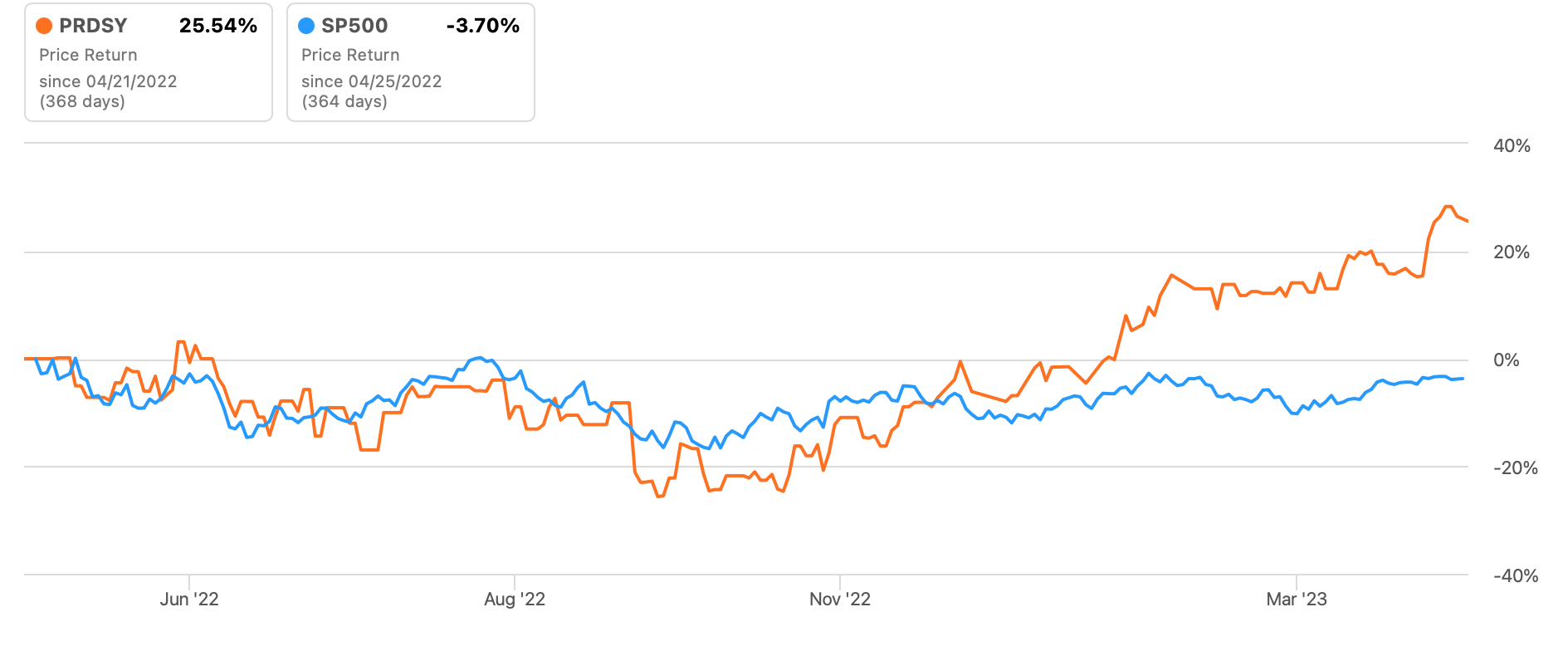

One look at the developments at the Italian Prada ( PRDSY ) underlines why luxury companies can be great investments in a recessionary environment. Its full-year 2022 results are strong and the company is actually expanding its employee base at this time as well. It is little wonder then that its price is at multi-year highs. Year-to-date [YTD] its price is up by almost 29% and over the past year, it has risen by 26%.

{kind=link}

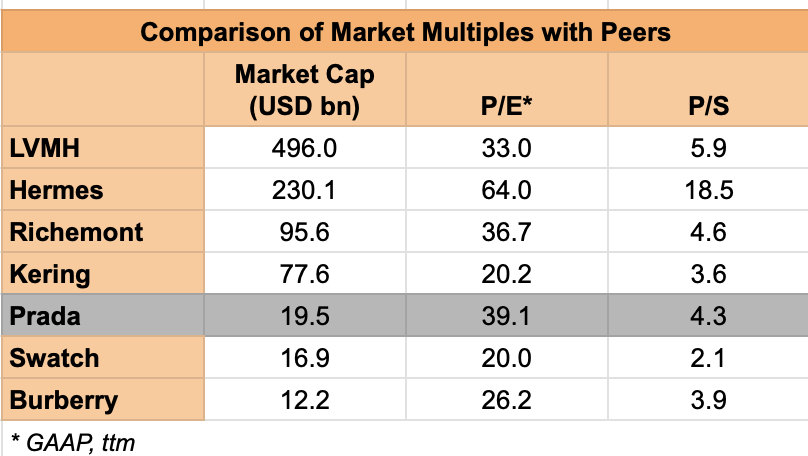

But here's the catch. A rising price comes with its own challenges, namely, an elevated price-to-earnings (P/E) ratio. At present, Prada's P/E is at 39.1x, significantly higher than the 15.5x for the consumer discretionary sector. To be fair that's not an equal comparison though. Luxury stocks are in a league of their own, especially since they are not as vulnerable to cyclical economic fluctuations as the typical consumer discretionary stock.

Here I take a look at what makes Prada stand out in the run-up to its first quarter update scheduled for release on May 11. I then see how it compares with its luxury peers to assess if it is indeed high priced or whether there is more steam in it.

Strong performance continues

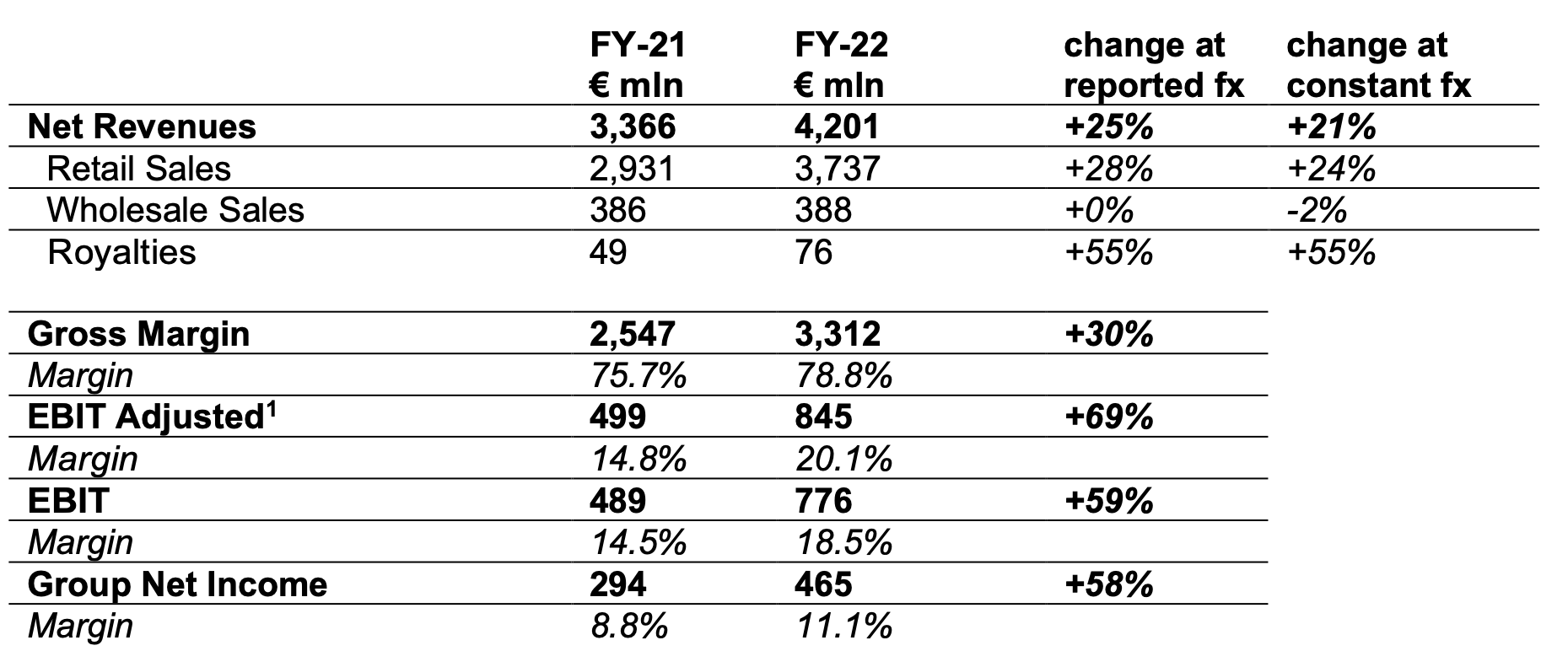

The company's strong performance since the pandemic continues. Revenue growth in 2022 was expectedly slower at 21% at constant currency compared to the 40% seen in 2021, which saw a bump up from the low base effect after a revenue fall in 2020. But it is still significantly higher than the five-year compounded annual growth rate [CAGR] of 7% .

Sales were driven by strong retail performance, which constitutes 89% of the total revenue, with an increase of 24%. Growth has softened slightly to 22% year-on-year (YoY) in the second half of 2022 (H2 2022) from 26% in H1 2022, but it does remain strong.

{kind=link}

Mixed margin performance

But the standout feature of Prada's performance is its impressive industry-beating gross margin at a huge 78.8%, which rose from an already high 75.7% in 2021. Its operating margin is less so, though. Even though EBIT rose by a huge 58.6% during 2022, the margin is at 18.5%. It has risen, to be sure, by a notable 4 percentage points from last year, and in a year when inflation has been high.

Performance can sustain

Moving forward, the company has a couple of advantages. The first is its Asia Pacific performance, which can pick up as demand from China comes back. Reports from the Spring Festival in January and February indicate improvement in luxury demand , especially at the country's duty-free Hainan island, during the holiday period.

Not only can it improve growth in the company's largest geographical market, but it might also even make up for the softening possible in the Americas market, which has a 20% share in Prada's revenues. Growth slowed down to 9% YoY in H2 2022, a sharp dip from 41% in H1 2022. If this were an isolated case, I would be less concerned. But a similar pattern was visible for Gucci owner Kering ( PPRUY ), which I wrote about recently , indicating a challenging time for the luxury sector there. With recessionary conditions expected in the US in 2023, I would not rule out further weakening in demand.

Next, I am optimistic about the company's operating margins. It managed to increase them in a year of high inflation, by actually reducing them as a percentage of revenue to operating expenses from last year. With inflation already showing signs of cooling off, coming quarters might just show further improvement in margins.

Comparing market valuations

That said, its price does look high compared not just to the consumer discretionary sector, but also to its peers. Only the Birkin manufacturer Hermes ( HESAY ) has a higher P/E of 64x. As coveted as Prada is, it does not compare to Hermes, which also has a super-strong operating margin of 41.5% and a 5-year revenue CAGR of 16%.

In fact, Prada falls behind even LVMH ( LVMUY ), arguably the biggest luxury company in the world, with a 5-year revenue CAGR of 13.2% and an operating margin of 26.5% in 2022. Yet, it has a slightly lower P/E of 33x. It is a similar story for Kering and even Richemont ( CFRUY ), which will likely see an increase in operating margins when it releases its full-year results in May.

Only smaller companies by market capitalization like Swatch ( SWGAY ) and Burberry ( BURBY ) have seen negative growth and much smaller growth respectively. Also, Swatch's operating margin is lower than that of Prada and Burberry's is comparable.

{kind=link}

But that still leaves us with three luxury companies, which are also much bigger than Prada in terms of market capitalization, that have lower P/Es while their growth and margins are higher. This leads to the question, why buy Prada? One reason is that it expects "above market average" growth, which could hold it in good stead.

A look at its price-to-sales (P/S) figure at 4.3x, is lesser only than that for Kering at 3.6x, among the three peers in consideration. Its one advantage over Kering is that its Americas sales look much stronger. Kering saw a 15% dip in Q4 2022 and just 1% growth in Q3 2022 from the market. In other words, its sales could slip faster than Prada's. But that still leaves us with LVMH and Richemont as better placed.

What next?

I like Prada, for a number of reasons, including both its performance and its prospects. Not only can its sales benefit from a return of demand from China, but the fact that it is increasing hiring is also a reflection of its expansion. Luxury companies are also good buys during a slowdown, which is expected in key economies like Europe and the US this year. The drop in Americas' sales growth is already visible. How much worse it can get will become clear soon when it releases its quarterly figures.

In the meantime, however, its P/E does look elevated, especially compared to LVMH. It does have a lower P/S compared to some peers and expects better-than-average growth, but how that goes remains to be seen. And its price is already pretty elevated. At this time, I would like to wait until its next results before taking a call on buying Prada.

For further details see:

Prada: Strong Performance But Pricey