CRUS - Pre-Earnings Update On Cirrus Logic

2024-01-18 11:35:06 ET

Summary

- Cirrus Logic's stock price dropped after an Apple downgrade by Barclays.

- Cirrus Logic is focused on advanced analog design for smartphone camera modules and many other parts.

- The company sees opportunities in both adding more cameras and functionality to smartphones and in existing cameras seeing increased penetration.

- The massive PC opportunity is now coming to pass.

Cirrus Logic ( CRUS ) isn't for the faint of heart. Recently, the price hit $85 and after the stinging downgrade of Apple ( AAPL ) by Barclays, the price plummeted south to the high $70s. The Barclays downgrade added a level pain for the opening of 2024 with Apple ((AAPL)) and Apple suppliers.

In any company report, it must discuss both the present and future. Keeping with that theme, we continue our coverage of Logic hoping to add thoughts of both the last quarter and coming business into 2024. Getting a pair of glasses above the cover in order to spy can be tricky, but we shall do our best.

Cirrus' Latest Conference

During December, Cirrus held a conference with Barclays ', Thomas James O'Malley. The fireside chat opened, confirmed and focused investors into the future of the company.

After an overview for new investors, the company headed by John Forsyth, Cirrus' CEO, discussed in great detail several important present and future endeavors. Beginning with the camera chip ((CLC)), new information includes:

- The chip clocks at "many thousands of times a second" to provide the stabilization capability for a camera. It isn't trivial.

- In considering size, power usage and functionality, the technology is leading edge.

- "[W]e also have a rich and aggressive road map for further features. I think no sign whatsoever that this area is done." Increased ASPs are coming.

- In addition, analysts claim major upgrades in iPhone 17 cameras are coming in 2025.

- This could add one to two more CLCs at $0.40 each.

- This technology continues to cascade down. (At this point, the high-end iPhone carries nine parts from Cirrus of which four are likely CLCs. At $0.35-$0.40 per part, the ASP is the $1.50 range and climbing. Older phones are in $0.70 - $1.00 ASP range and new phones at higher ASPs will drown out the older levels.)

We are waiting for the report on the new Vision Pro product release for confirmation of the presence of multiple CLCs, maybe as high as 30, two per camera.

Cirrus confirmed the new 22 nm codec and new amplifier technology, but still refrained from offering guidance on any ASP increase. We still believe that it will be in the $2 range.

Management confirmed its relationship with Apple.

"I think the best indicator though is the number of opportunities that we have in discretion or at some level of being in flight with that customer. And I think that's -- I think there are more of those across a broader range of areas than we've ever had in the past ."

Next management opened a discussion on power control.

- It isn't conventional power management ICs ((PMIC)).

- This is a crowded space.

- It is about managing overall power.

- it looks across the whole device.

- Eliminating burn out situations.

- Preventing power surges.

- Leveling usage even under low battery charge states.

- it looks across the whole device.

- Manages battery health.

Forsyth noted that the value of this function isn't truly recognized until you see one with and one without side-by-side.

PCs

Next, management discussed and confirmed size and functionality for a newer grass-roots business with Personal Computers. They confirmed:

- Market size at 200 million units per year.

- A progression for new revenue starting in FY-2025.

- Expecting revenue greater than current Android business by CY-25/26.

- We believe that equals greater than $200 million.

- ASPs could reach $7 or more per device (from previous conferences).

- Long-term potential equals $1.4B.

- Driven by thinner designs.

During the chat, Cirrus management noted that once a product uses the Cirrus' approach with its premium quality, it is difficult for vendors to walk back to sub-par quality though cheaper approaches.

The Apple Downgrade

The December quarter is always rich in bantering about the sales strength of new Apple products, in particular, the iPhone. This December was no different. From the news in early January,

"On Tuesday, Barclays downgraded Apple’s stock to underweight and trimmed its price target to $160 from $161, citing weakness in iPhone 15 sales, signaling likely lower demand for iPhone 16 and other products. Apple shares closed 3.58% lower on Tuesday."

We have tried to identify his sources for claiming weakening demand without success. In fact, we found the opposite.

From the same article, "

“We’re seeing that suppliers are still seeing robust growth on the iPhone 15. We’re in the middle of a supercycle,” said Ray Wang of Silicon Valley-based Constellation Research. . . There’s still 200 to 300 million iPhones that get replaced onto 5G, at least for the next 24 months, so I’m not sure exactly the downgrade on growth, but on valuation . . . . "

This downgrade was proceeded by a list of back and forth earlier in the quarter. Reports hit that new iPhone sales in China were off by almost 10% year over year driven from a new purported successful Huawei product. Another article in the same time frame reported double digit growth in Korea. A report in October claimed China sales were down 5% year over year while sales in the U.S. remained strong. A later article quotes Tim Cook , Apple CEO, saying, "In mainland China, we set a quarterly record for the September quarter for iPhone," Qorvo reported at its November report that Huawei was a flash in the pan so to speak, hot for a bit than cooling but still small in comparison. Still another later report claimed iPhone strength in Africa.

Continuing, in mid-November this headline appeared, Foxconn revenue to fall in the holiday quarter, as iPhone 15 faces triple challenge . A month later an update caries this headline, iPhone assembler Foxconn expects strong sales for the holiday quarter . Are you confused? I believe you should be.

The preponderance of the evidence suggests that for December sales should experience at least slightly positive results year over year and maybe much better. What isn't discussed yet is March.

A table on past revenue might help guesstimate December and March revenue.

| Cirrus Revenue (Million) |

| Sept. 2022 |

| Dec. 2022 |

| March 2023 |

| Sept. 2023 |

| Guidance |

| $450-$490 |

| $520-$580 |

| $340-$400 |

| $430-$490 |

| Actual |

| $540 |

| $590 |

| $375 |

| $480 |

| Apple |

| $443 |

| $520 |

| $304 |

| $422 |

| Non-Apple |

| $97 |

| $70 |

| $71 |

| $58 |

A second table includes September 21 through March 22 plus guidance for December 2023.

| Cirrus Revenue (Million) |

| Sept. 2021 |

| Dec. 2021 |

| March 2022 |

| Dec. 2023 |

| Guidance |

| $430-$470 |

| $490-$530 |

| $400-$440 |

| $510-$570 |

| Actual |

| $465 |

| $550 |

| $490 |

| Apple |

| $370 |

| $450 |

| $387 |

| Non-Apple |

| $95 |

| $100 |

| $103 |

Trying to make sense of coming revenue isn't simple. It seems that Apple's iPhone 15 is selling slightly better than the 14. Cirrus, with its newer higher ASP CLC chip in the two new Pro phones plus Apple dropping off iPhone 13s, will have higher overall ASPs. But on the other side, non-Apple business like other suppliers reported tanked, by almost in half. What is also clear is that Apple was over purchasing in both March and September of 22 by approximately $50-$60 million. It seems also clear that Apple used March and June of 23 to unload extra inventory. It is also noted that June of 23 contained a major exchange for the CLC chip, an event that is known to skew results significantly. We could argue that September's 22 over purchase significantly affected March 23 results. But September of 22 also had $40 million higher in non-Apple revenue than September of 23. At some extent we should ask, was Apple stuffing channels or just adding higher ASP inventory in this September? Guidance for December 23 was relatively unchanged year over year even with the likelihood that non-Apple business was in the tank.

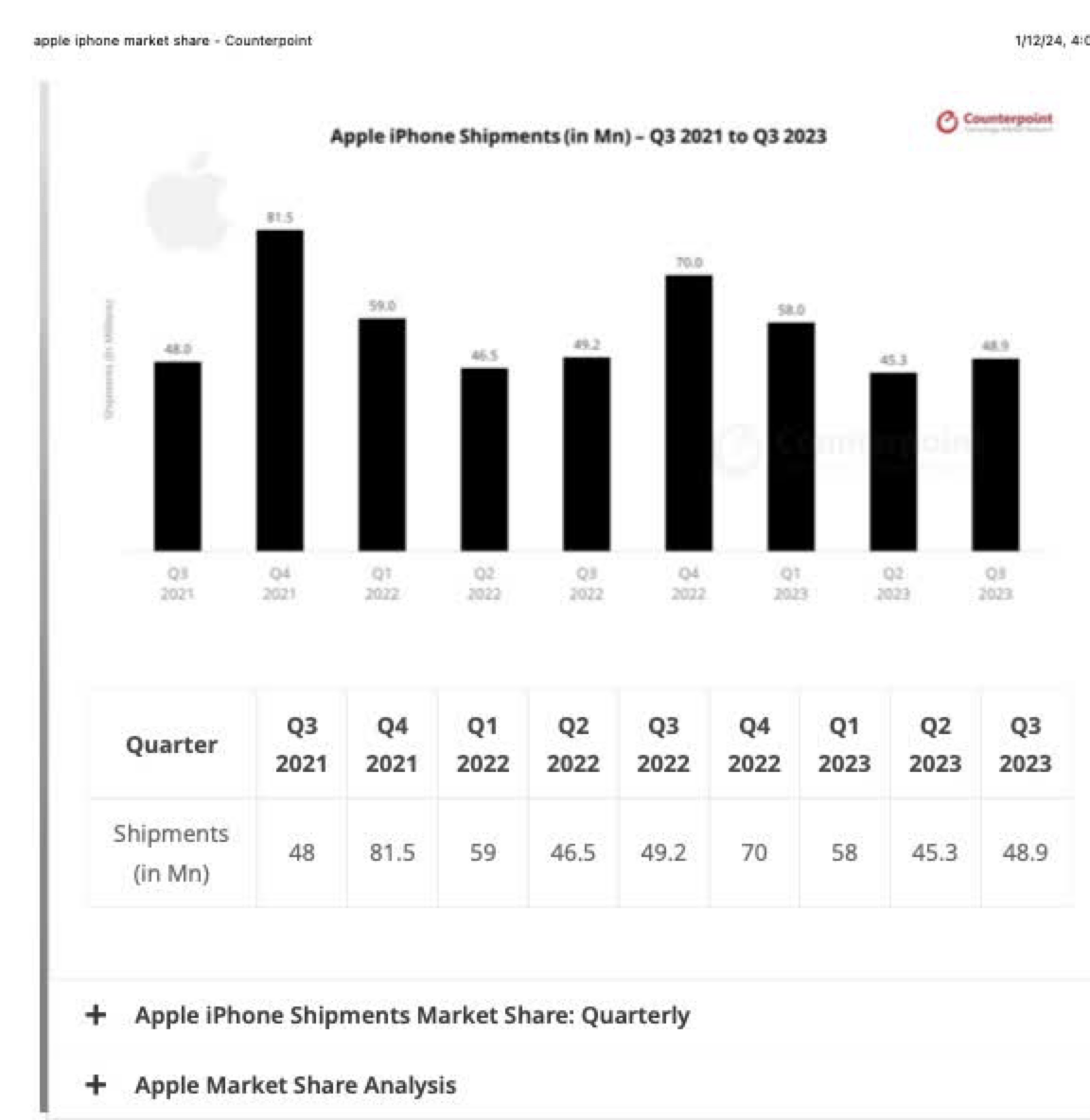

Continuing with iPhone unit sales, Counterpoint Research published this interesting article with its take on unit sales by quarter. A chart from the article follows.

{kind=link}

September quarters have been consistent at 50M minus for the last few years. The December quarter has been all over the map at 80M in 2021 and 70M in 2022. IDC wrote recently this comment, "Not only is Apple the only player in the Top 3 to show positive growth annually, but also bags the number 1 spot annually for the first time ever." Taken literally, the above chart with the quarters outside of December being in total 3-5 million less year over year, December must be at least in the middle 70 million range. News articles taken in aggregate suggest that December of 2023 will fall between the two years and probably in the middle. We haven't discussed tablets or earpieces with some articles suggesting a level of weakness.

Now add data with analysts showing $540 million for December and $360 million for March. We are expecting something near the top end of guidance in December based on likely iPhone unit sales and the value of the high-end of guidance, maybe even above guidance. For March, again iPhone unit sales have been steady in the 60M minus a few million range. We think analysts might be low for March, perhaps closer to $400M but with less confidence.

The Long-term Vision in Place

From the conference with Barclays, Cirrus' long-term vision and growth remains in place. Weakness in Android at $200 million year will in time recover. New higher ASP products are coming in 2024. We expect management to discuss more details during the February conference call. A check for December for investors might come if Qorvo continues its practice of reporting a day before Apple. If it reports revenue more than $50M above guidance and continues to report weakness in its Android business, Apple probably had a huge quarter.

Risk

Again, for Cirrus Logic investors, it isn't for the faint of heart. With unknowns in place for March, we put our hold back on, temporarily. This is down from a strong buy in our last report. Any reasonable correction afterward would be a grand buying opportunity in our view. Yes, the risk of crippling recession exists for all the consumer suppliers. Our hold is only based on unknowns for March guidance. Long-term, we continue our strong buy. Yes, we did get the glasses above the tarp.

For further details see:

Pre-Earnings Update On Cirrus Logic