PD:CC - Precision Drilling Corporation: Improving Drilling Activity And Margin Expansion

2023-06-26 11:28:31 ET

Summary

- Precision Drilling Corporation has experienced a 13% increase in drilling activity in the US and Canada, with a growing market share and high utilization of its rig fleet.

- PDS has secured contracts in Kuwait and Saudi Arabia, and its valuation looks attractive with a forward P/E of just 4, significantly below the sector average of 8.7.

- Risks include potential volatility in commodity markets and the possibility of no significant improvement in natural gas pricing, which could negatively impact gas drilling.

Investment Summary

So far in 2023 Precision Drilling Corporation ( PDS ) has done very well in growing its business and capturing the demand the industry is lacing on them. Most notable from the last report was the growing drilling activity the company experienced in both the US and Canada, up by 13%. This paints the picture that the industry is very much still alive and well and prospects remain high.

PDS has continued to scale both its Alpha and EverGreen product lines across its super triple rig fleet and managed to boost revenues as a result of it. Right now, PDS has a FWD p/e of just 4, and I think a correction upwards is due as PDS proves its capabilities and executes well going forward. The risk/reward ratio here seems very favorable, and PDS trading under 5 p/e makes it in my opinion a very intriguing buy.

Strong Presence And High Utilization

In the US, right now PDS holds an 8% market share for onshore drillers, making it the fourth-largest one. Within their fleet, they have 101 drilling rigs, including the 66 AC super triple rigs. With this market share, they have a presence in every single major US unconventional oil & gas basin.

Market Position (June Presentation)

With that, PDS sees strong momentum going forward as growing LNG exports are continuing. Some suggest that LNG exports will grow by 152% between 2022 and 2050. That would create a solid long-term growth path for the industry, and that is something that PDS also recognizes as they are increasing their product line to gain an upper hand-over competitors.

Apart from growing LNG exports, the oil prices remain quite stable so far, as opposed to the volatility in the market in 2022. As prices are supported by demand, PDS noted customers are maintaining production and continue to replenish inventories, which creates recurring revenues for PDS.

PDS is also growing its international presence and bids continue on their idle rigs in Saudi Arabia, Kuwait, Kurdistan, and Georgia, with 5 idle rigs in total. Right now PDS operates one of the new fleets in the region and has received 4 5-year contracts in Kuwait last year, and 5-year contracts for rig extensions in Saudi Arabia. This means that PDS expects to have at least 8 rigs active by mid-2023. Progress on this front I think should remain in investors' minds, and delays could lead to a lower multiple for PDS.

{kind=link}

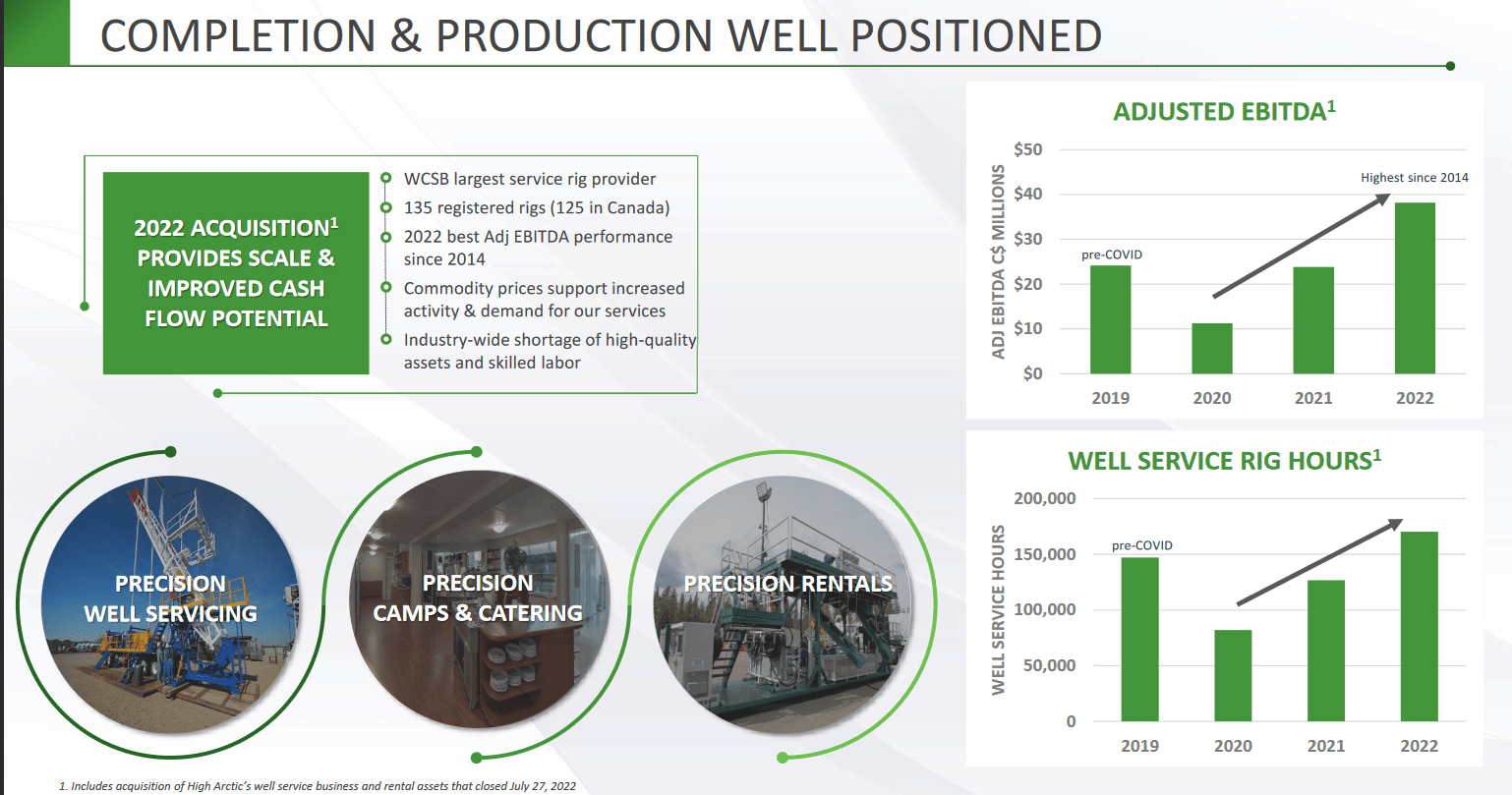

The improving market position that PDS now has translated into several positives for the business. Most notably, that adjusted EBITDA has grown around 13% YoY between 2019 and 2022. An impressive feat as PDS improves well service rig hours and continues to make strategic acquisitions to strengthen its market position.

Quarterly Result

PDS started the year with a solid quarterly performance and the bottom line made strong progress. Back in Q1 of 2022, the EPS was negative $3.25 but in 12 months PDS grew to a positive $7.02 instead. Showcasing that their operational performance has been strengthened. Margin expansion like this has been driven by growing funds provided by operations, which increased 433% YoY.

Financial Highlights (Q1 Report)

As I discussed before, PDS is continuing to push to strengthen its international presence further, as on a YoY basis it has lost ground. Down nearly 20% is worrying, but it has been backed up by growth in the US market.

Operating Highlights (Q1 Report)

Even with a declining contract drilling rig fleet, PDS performed very well. This to me argues that perhaps the company deserves a higher valuation. Trading at a p/e of 4 is in my opinion too little and presents PDS as undervalued and a solid buying opportunity. Where my attention will be for the coming couple of quarters will be growth regarding utilization days. I think that will correlate with growing EPS for PDS and eventually results in the share price coming out of the last couple of months' decline and rising again.

Risks

One of the main risks with any commodity-related company is the volatility in the market and inconsistent quarterly performances. That seemed to have happened for PDS last year as oil prices were up and down, which had customers be cautious about investing into new projects.

My second concern revolves around gas pricing . If there is no significant improvement in natural gas pricing, it could negatively impact gas drilling. Currently, there are no apparent factors that could drive up gas prices, making this a plausible outcome. In such a situation, PDS shares could either decline or remain stagnant at their present levels.

Valuation & Wrap Up

I want to reiterate a little of what has been said here before, PDS has been growing its market share at a very impressive rate and now holds 8% of the market share for onshore drilling in the US. This market is where a majority of the revenue is generated, but that hasn't stopped PDS from growing its international presence either, securing contracts in both Kuwait and Saudi Arabia.

{kind=link}

With a p/e of just 4 right now, I think the valuation looks very attractive. It's a fair bit under the sector's average p/e of 8.7, and I think there is room for the share price to move upwards and PDS continues to post solid operational performances. I am rating PDS a buy at these price levels.

For further details see:

Precision Drilling Corporation: Improving Drilling Activity And Margin Expansion