XLF - Predicted 14% Yielding TPVG's Dividend Hike; Potential NAV Growth Now

2023-08-16 02:36:18 ET

Summary

- Triplepoint Venture Growth is a high-yielding fund that can provide stable income even during market downturns.

- TPVG's NAV is still down from its peak, but its NII has continued to increase, indicating the potential for a repricing upwards.

- The market's punishment of tech companies has created buying opportunities for TPVG, and its strong NII growth makes it an attractive investment.

Triplepoint Venture Growth ( TPVG ) has the potential to be a portfolio staple. With mostly debt investments in cash flow positive private tech companies, it gives retail investors access to private equity and tech growth while also tapping directly into these companies revenue streams before other debtors or shareholders get their piece of the pie. Timed well, it has the potential to provide returns less correlated to other assets typically in an investor's portfolio (most notably U.S. Treasuries) while also providing substantial returns and incredible liquidity.

Brass taxes: TPVG is a 14% yielding fund that you can rely on even if the other stuff in your portfolio isn't doing so hot. And if you time your trades correctly, you can end up with a huge income stream.

I speak from experience. During the March 2020 downturn I bought a few shares of TPVG in March 2020 as it climbed to the bottom.

Charles Schwab Charles Schwab Charles Schwab

Including some smaller transactions not pictured here, I ended up spending about $10,000 on TPVG for around $5 on average, which means that that investment currently has a 32% yield on cost for $266.67 per month in income (excluding special dividends).

Yes, I deeply regret not buying more, but as the market was in freefall and Armageddon looked upon us I couldn't commit too much to the truth that was at that moment obvious: if the world was going to end money wouldn't matter anyway, and if it wasn't then TPVG would recover. And boy did it recover, both with NAV and with NII.

More buying opportunities appeared last year and earlier this year as the inflation-hype bear market and banking micro-crisis impacted TPVG. This prompted me to predict TPVG's dividend hike on December 10 ; that hike happened less than three months later .

While the market has fully recovered, even the Financial Select Sector SPDR Fund ( XLF ) is up YTD. TPVG, on the other hand, is not, even if its market price is up.

BDCinvestor

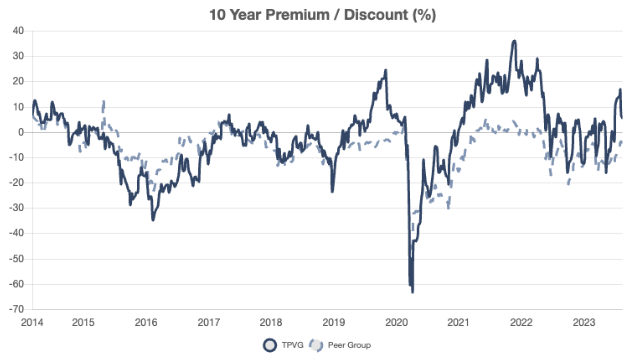

With a NAV still down 23.7% from its 2021 peak, risk-averse income investors remain leery, resulting in TPVG's 6% premium remaining curtailed post-banking crisis, whereas its premium has reached double-digits for sustained periods in bull markets.

{kind=link}

The reason for this is quite simple: TPVG's NAV is marked-to-market slowly, and credit valuations remain impacted by the very brief and now mostly forgotten banking crisis of earlier this year.

Holihan Lokey

Private credit valuations are down 47% from where they were at the peak in 2021, causing discounts to widen to -2.45% currently (in the chart above seen as a positive number). TPVG's portfolio has seen a less severe markdown, which is a glass is half full or empty kind of thing, so arguments to resolve that question are likely to be fruitless.

There is, however, an important underlying fact about TPVG that indicates its portfolio is going to see a repricing upwards. Throughout the crises of the last few years, TPVG's NII has continued to increase, helping its NII/dividend ratio stay very healthily at 133% YTD versus the 115% BDC average .

Considering the fact that the banking crisis has ended but debt valuations have not, and considering the fact that TPVG's NII remains unchallenged following a year of five bad loans on its books.

TPVG

3.3% defaults is higher than the 1.64% last reported by Proskauer, but it's not too far from the 2.4%-2.7% default rate seen in sub-$25m private credit (TPVG's wheelhouse) over the last year:

Proskauer

The 70-ish basis point delta between TPVG's default rate and the broader market's makes complete sense given its tech concentration and the market's punishment of tech companies in 2022.

Masochist that it is, TPVG brushed off those punishments and continued to deliver income thanks to how good TPVG is at finding strong performing assets and just how ridiculously low the market is valuing those assets. At its current valuation and NII run rate, TPVG earns a net 16.8% return on its assets with NII rising yoy:

TPVG

Net of PIK, which admittedly has grown to become 13.8% of total NII, TPVG's net return on its net assets remains 14.7%, close enough to its payout/NAV ratio of 14.95%, indicating more dividend sustainability.

TPVG

If TPVG gets PIK down, which is likely as the credit market stabilizes and it makes more debt investments in a higher interest rate regime.

As the market realizes this, two things will happen: TPVG's market price will rise as investors realize its well-deserved premium is now too cheap. Additionally, momentum in the credit markets will boost private credit valuations as default rates continue to ease, resulting in TPVG's NAV rising that, in turn, will boost its market price.

It took three months for TPVG's strong NII to result in the dividend hike I expected; NAV valuations and market prices, depending on the animal spirits of credit and equity markets as they do, are harder to predict. Nonetheless, TPVG's sustained NII growth and its incredible IRR on its portfolio make it an obvious buy. I have increased my position in the last few months and will likely increase it again in the next few months.

I hope enough people will disagree with this article to sell it off, getting me shares even cheaper.

For further details see:

Predicted 14% Yielding TPVG's Dividend Hike; Potential NAV Growth Now