ETD - Preferred Updates: Past Preferred IPOs Trading Below Par Capital Southwest Notes Offering

2023-07-05 09:46:46 ET

Summary

- The tightening of financial conditions has led to a decrease in preferred stock and ETD offering activity, with no new preferred stocks offered in June and only one new ETD.

- Capital Southwest offered $62.5 million worth of 7.75% senior notes due 2028, rated Baa3 by Moody’s.

- Fitch Ratings assigned a "stable" outlook to CSWC, but warned of potential headwinds due to slower growth at portfolio companies and higher debt service burdens, as well as potential constraints if bank financing becomes more limited for the sector.

- The article also discusses the high yields seen across recent ETD offerings from BDCs and the criteria for CDx3 compliance, which requires at least five years of call protection.

* Tightening financial conditions have drastically reduced preferred stock / ETD offering activity, with no new preferred stocks offered during the month of June, and just one new ETD.

* Internally managed Business Development Company Capital Southwest Corporation offered $62.5 million worth of 7.75% senior notes due 2028, rated Baa3 by Moody’s.

* Here is a comparison against the highest quality preferred stocks in our coverage universe, as ranked by our internal “CDx3 Compliance Score” metric:

* CDx3 preferreds ranked 10 out of 10 are meanwhile selling for an average discount to par of about 6.8% and offer an average current yield of 6.38%.

* Past preferred stock IPOs now trading below par: a look at recent par crosses.

New offering summary:

CDX3Investor.com

SEC filings for further information: Term Sheet ; Prospectus

Last month we reported on externally managed Business Development Company Gladstone Investment (GAIN), which priced an offering of $65 million worth of new 8% exchange traded notes due 2028 (symbol GAINL), and receiving a BBB credit rating from Egan-Jones Ratings Company. That offering had followed April’s ETD offering from fellow externally managed BDC Saratoga Investment Corp (SAR), which had priced a $50 million offering of 8.5% notes due 2028 (symbol SAZ), which was rated BBB+ by Egan-Jones.

And this month we saw internally managed BDC Capital Southwest ( CSWC ) come to market with an ETD offering of their own, pricing a $62.5 million offering of exchange traded notes due 2028, at 7.75%. The new notes trade under symbol CSWCZ on the Nasdaq, and received a rating of Baa3 from Moody’s. Shortly following the pricing of the offering, CSWC announced it had also received a Fitch rating, at BBB-.

In its rating action commentary, Fitch noted that CSWC's focus on lower middle market companies means their portfolio companies have below-average EBITDA relative to peers, which could increase CSWC's portfolio risk in an economic downturn; on the other hand Fitch noted that CSWC's focus on senior debt investments (at 86% of the portfolio) was above the average of its rated peer BDCs.

Although Fitch assigned an outlook of "stable" to their rating, they indicated that their outlook for the sector in general is for BDCs to experience weaker asset quality metrics in 2023 due to slower growth at portfolio companies and higher debt service burdens, amidst broader macroeconomic headwinds. Fitch also implied that as an independent internally managed BDC with no affiliation to a broader investment platform (of an external manager), CSWC could face headwinds if bank financing becomes more constrained for the sector, saying:

“Fitch also believes CSWC's lack of affiliation with a broader investment platform could be a headwind longer term should bank financing become more constrained for the sector.”

-- Fitch Ratings, June 13, 2023 Rating Action Commentary

Here Fitch is implicitly referring to certain peer BDCs that are externally managed and affiliated with large asset management firms, like Ares Capital ( ARCC ) which is externally managed by a subsidiary of the Ares Management ( ARES ) investment platform, and MidCap Financial Investment Corporation ( MFIC ) which is externally managed by an affiliate of Apollo (APO).

Here at CDx3 we would point out that while such peer BDCs may experience certain credit-enhancing benefits from their external manager affiliations, the external management structure also tends to result in notably lower common stock valuation, thus constraining such companies’ ability to raise equity capital: According to the Price/NAV screener at BDCInvestor, while CSWC presently enjoys a healthy price/NAV valuation of 1.18x, ARCC meanwhile trades at 1.01x, GAIN is at 0.98x, and MFIC is all the way down at 0.80x.

Of the ten BDCs presently listed at levels above 1.00x NAV at the time of this writing, we would note that four of them are internally managed BDCs, and the top three BDCs by price/NAV overall are all internally managed BDCs -- and they happen appear on the list in the exact order of their equity market capitalization from largest to smallest: Main Street Capital ( MAIN ) takes the #1 spot, followed by Hercules Capital ( HTGC ) in spot #2, and Capital Southwest at #3.

In CDx3’s view, this ordering is no coincidence, and is driven by the economy of scale benefits of internal management that we mentioned in our report last month, as conveniently illustrated by the recent ETD offerings we were reporting on: for example, the external manager of Gladstone Investment Corporation charges a 2% annual fee on average gross assets, which means that the GAINL offering at 8% implies that new investments must yield in excess of 10% before they cover both the interest cost to pay GAINL holders plus the 2% management fee. Meanwhile, as an internally managed BDC with economy of scale benefits, Capital Southwest common shareholders begin to benefit if new investments yield in excess of the 7.75% interest cost paid to CSWCL holders.

This dynamic gives the internally managed BDCs a clear long-term advantage over their externally managed peers when it comes to the ability to raise new capital at reasonable cost: debt capital raised does not require an “extra” additional fee to be overcome, and, equity valuations tend to be stronger, providing a long-term tailwind when it comes to equity capital raises. In CDx3’s view, these advantages are a strong positive credit-enhancement for holders of the exchange traded debt.

As regulated investment companies ("RICs"), all BDCs like those mentioned above have built-in investor protections including a limit on leverage, and investors in debt instruments issued by BDCs have pointed to favorable historical outcomes, such as making it through the financial crisis unscathed (as far as BDCs meeting their debt obligations) as evidence for an often-investment-grade level of risk involved in investing in the ETDs (and preferred stocks) issued by the top BDCs.

Given this strong issuer credit profile across BDCs in general, coupled with the high yields we are seeing across these last three ETD offerings from BDCs (SAZ at 8.5%, GAINL at 8%, CSWCL at 7.75%), some have wondered why we here at CDx3 only rate these a 9 on our 10 point CDx3 Compliance Score scale, and not a full 10 out of 10? The answer is the call dates: in each of these three cases, the debt can be repaid at par about two years after issuance, whereas the criteria for CDx3 compliance established by Doug K. Le Du in his book Preferred Stock Investing , requires at least five years of call protection:

"By selecting preferred stocks that become callable five years after their IPO date we are able to switch on the power of the Rule of Call Date Gravity. When the whole world knows that on a specific future date the issuing company of your preferred stock can purchase it from whomever owns it any time they wish, and, if they do, they are required to pay a specific price per share, the market price can behave very differently as that date approaches.

Knowing what the market price of any investment is likely to be at some future point is a rare gift. By selecting only preferred stocks that have a known, fixed call date we bestow that rare gift onto ourselves. We want to fix the call date at a specific, known point in time for CDx3 Preferred Stocks. Doing so allows us to take advantage of the known changes in the market price that your CDx3 Preferred Stock may realize as the call date approaches."

-- Doug K. Le Du, Preferred Stock Investing, 5 th Edition

In essence, these recent ETDs only rate a 9 because the issuers have too much of an advantage over us from that option to refinance in two years if/when interest rates are lower; and at CDx3 we require five years from issuance as our call protection window. But of course, while many investors will want to stick with only those preferred stocks and ETDs with a CDx3 Compliance Score rating of 10 out of 10, many investors will also find room in their portfolio for 9-score-and-lower securities like these ETDs that we often see issued by BDCs.

BDCs were created in 1980 by Congress to encourage the flow of public equity capital to private U.S. businesses, with a requirement for BDCs to invest primarily in private companies in the United States. BDCs were also given a structural requirement to distribute 90% of their taxable income to shareholders, much like we see at Real Estate Investment Trusts (REITs).

Because of this taxable earnings distribution requirement , BDCs generally pay extraordinarily high dividend yields and meanwhile by their very structure these companies cannot reinvest their earnings into portfolio growth. Instead, if they wish to grow their portfolios, BDCs must rely on the equity and debt markets in order to raise fresh capital to fund that portfolio growth. As a result, many BDCs (like those discussed today) are routine issuers of both preferred stocks and exchange traded debt securities, even at times of abnormally high market yields.

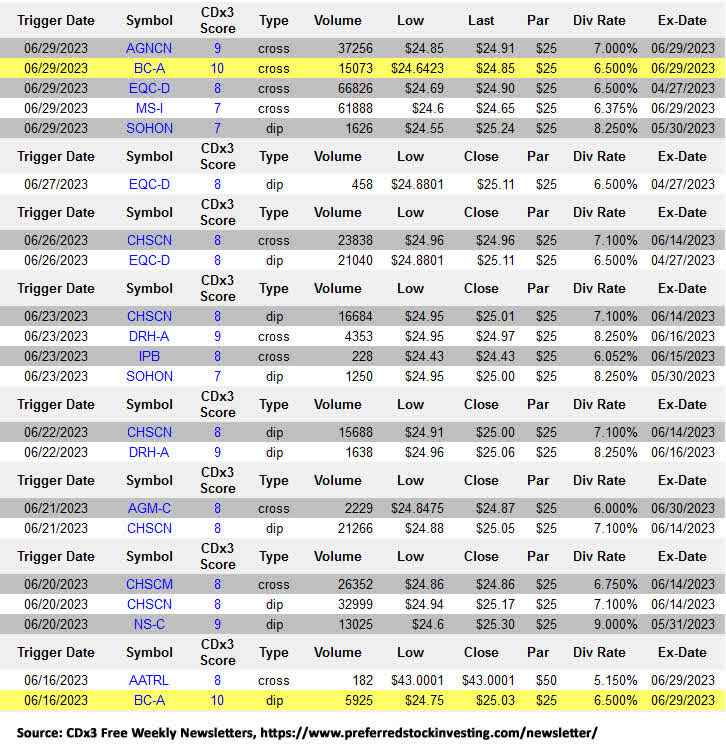

Past preferred stock IPOs below par

In addition to covering new preferred stock and ETD offerings, we also track past offerings, with alerts when securities fall below their par values. To close this article, we would like to share with you some of the dips/crosses below par we recently observed:

{kind=link}

Note: Any yellow highlighted entries indicate eligibility for the “CDx3 Bargain Table.”

See you next time, and thanks for reading!

For further details see:

Preferred Updates: Past Preferred IPOs Trading Below Par, Capital Southwest Notes Offering