PTA - Preferreds Opportunity: Assessing The Carnage What's Been Thrown Out With The Bathwater

2023-04-19 08:47:46 ET

Summary

- The failure of SVB and Signature Bank created a maelstrom of fears and deja vu of 2008. But Credit Suisse merging into UBS smashed the preferred stock space.

- Credit Suisse's AT1/CoCos were marked down to zero which surprised investors in these bonds, causing other banks' CoCos to plummet in price.

- Preferred stocks sit just below CoCos and AT1s on the capital structure. Like those bonds, preferred typically have a perpetual maturity and count towards a bank's tier one capital.

- The contagion appears to be somewhat contained, though investors and the market are still of the view that another shoe is going to drop soon. We think there are great opportunities to pick up.

- We go through the preferred space, both individuals and CEFs, and analyze the opportunity. As is typical in a fast moving, highly volatile environment, everything gets sold together.

(This report was issued to members of Yield Hunting on March 28th. All data herein is from that date or prior.)

The fall of two large US banks and the merging of one of the largest global banks with another in order to save it has created turmoil in the banking sector. Much of this has eerie recollections of 2008 when the banking sector was at the center of the Global Financial Crisis. This has created a PTSD sort of shoot first, ask questions later kind of response.

We go through the preferred space, both individuals and CEFs, and analyze the opportunity. As is typical in a fast moving, highly volatile environment, everything gets sold together without hesitation creating opportunity for those willing to do the work.

Backdrop - Death of Silicon Valley Bank

By now, everyone knows the story. You had a volatile brew of a fast-growing bank, terrible mismanagement, highly concentrated customer base that was burning cash, and rising interest rates. Aided by social media, on March 9th, customers rushed to move their money from the bank. Over $42B in deposits flew out the door in a single day - more than 25% of the bank's total deposits.

To wrap your head around that number, think about this. The bank stress test, meant to simulate a 'worst case scenarios', had less than that amount of deposits leaving the bank in a year. It happened in 8 hours!

This has created panic as investors recreate 2008 in the back of their minds. Like most investors who are reactive instead of proactive, they sell everything, everywhere, all at once (there, I used the idiom).

Less than one week later, we had Credit Suisse on the verge of failing. The Swiss National Bank ("SNB") forced a merger/acquisition by UBS ending the existence of the 162 year old bank.

With three large banks failing in less than 10 days, it didn't take long for investors to go full blown panic-mode. Adding fuel to the fire, the Swiss National Bank wrote down the AT1 bonds of Credit Suisse to zero, wiping out investors.

Now everything bank-related is being sold off en masse.

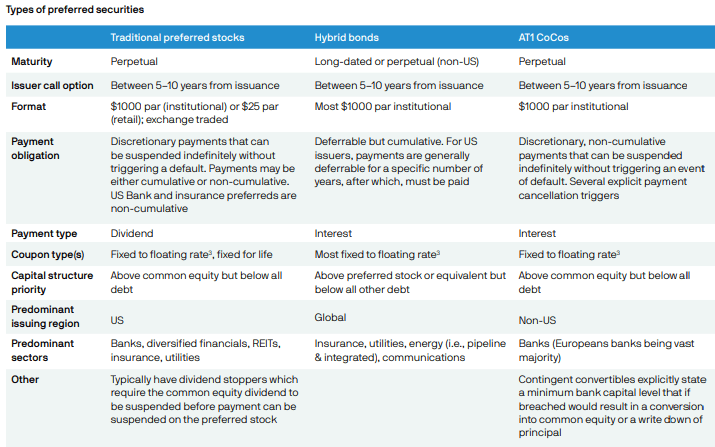

What Are CoCos and AT1 Bonds?

The core of these bonds is revealed in the name itself. CoCo bonds are a hybrid security and are convertible into shares contingent on some event happening. One of the ways these are similar to preferred stocks is that they have no maturity - unlike traditional bonds. Thus, they are perpetual securities. All CoCos are perpetual bonds, but all perpetual bonds are not CoCos. They have only been in existence since the Financial Crisis.

A 'trigger' event must occur for the conversion, which makes them different than more traditional convertible bonds. The majority of CoCos are issued by banks as a form of tier one capital.

Like most convertible bonds, CoCos have a strike price and a yield, but as noted above, can only be converted upon a trigger event. This is when losses are started to be absorbed. Obviously, CoCos and AT1s are higher in the capital structure than common equity but lower than most senior secured bonds/loans.

twentyfouram.com

This shows the waterfall of priority a different way:

bondvalue.com

AT1 bonds are a form of a CoCo bond created to prevent the need for future government bailouts of poorly run banks taking too much risk. The AT1 bond market totals $275B - acting as a cushion to absorb losses if a bank's capital level falls below a certain threshold. They would then be converted to equity and be written-off, diluting the equity shareholders.

They are the riskiest type of bond a bank can issue and so carry a higher coupon.

If AT1s are converted into equity, this supports a bank's balance sheet and helps it to stay afloat. They also pave the way for a "bail-in", or a way for banks to transfer risks to investors and away from taxpayers if they get into trouble.

AT1 bonds and CoCos have been all over the news lately because of the write-down of the Credit Suisse bonds to zero. At the same time, equity investors of CS stock actually received something for their shares. This is where the ire has been centered as bonds are above stocks on the capital structure.

What Are The Broader Implications Of The Move?

It is safe to say that most investors who held these bonds didn't think the potential merger with UBS - which was discussed several days before it occurred - would result in their bonds becoming worthless. Otherwise, they likely would have dumped them for any price on the days leading up to the bank's demise. In other words, investors were taken for surprise.

The prospectus clearly states that the SNB could legally write the bonds issued by Credit Suisse to zero if it was part of a merger to "save the bank". In other words, the SNB essentially said that CS was bankrupt, taken over, and immediately sold to UBS for $2B, all in a couple of hours.

The write-down of these bonds to zero has spread to other AT1 bonds. The thinking goes if they can do that to the CS bonds, they could do that to any AT1 bonds from any other bank if the bank gets in trouble. This will certainly make it tougher for banks to issue these bonds in the future and force them to pay more yield.

Bid prices on AT1 bonds from banks, including Deutsche Bank, HSBC, UBS and BNP Paribas, dropped 9-12 points on March 27, sending yields sharply higher, data from Tradeweb showed.

Preferred Stocks Took A Bath Too

Preferred stocks sit just below CoCos and AT1s on the capital structure. Like those bonds, preferred typically have a perpetual maturity and count towards a bank's tier one capital.

From PIMCO :

Preferreds are issued primarily by banks and insurance companies. REITs, utilities and other financial institutions also issue preferreds. Preferred securities count toward regulatory capital requirements so banks issue preferreds to help them maintain their required capital ratio. Preferreds can also offer issuers structural benefits, lower capital costs and improved agency ratings.

stonebridge

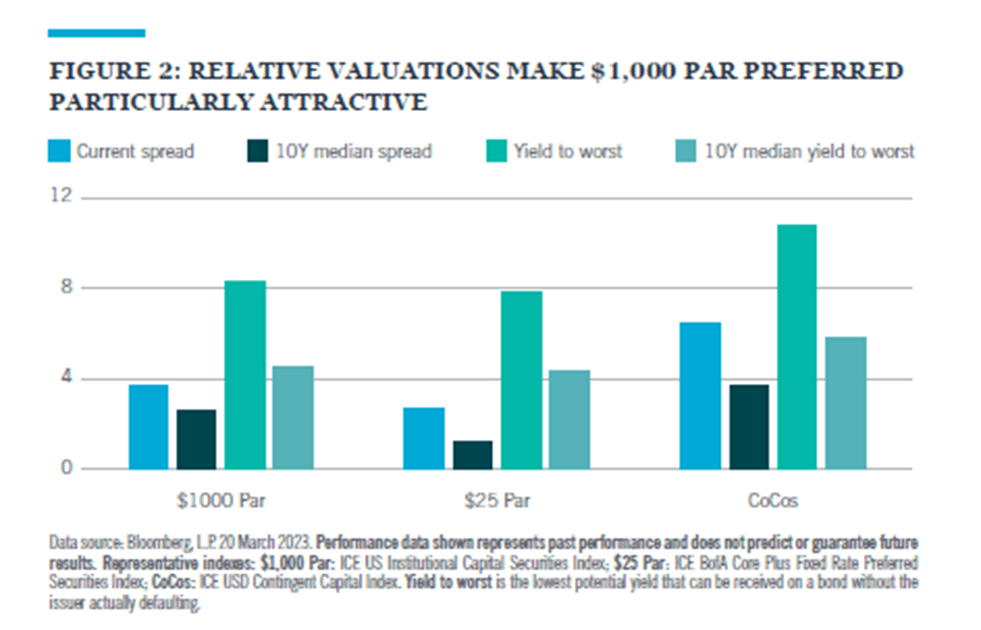

The opportunity in $1,000 preferreds seems to be massive:

This current move in preferred securities is unprecedented, as spreads over Treasuries widened 122 bps between 28 February and 20 March. If the spread finishes this month at its current level, it would represent the third-largest monthly increase since the inception of the ICE BofA All Capital Securities Index in 2012. At present, we think the preferred sector offers attractive valuations. Within preferreds, we favor $1,000 par over $25 par preferred securities, as they offer more attractive valuations and feature almost onethird less duration (Figure 2). We also think the $1,000 par side of the market should be more liquid and less volatile.

{kind=link}

Like AT1s and CoCos, preferred stocks of banks and insurers got clobbered recently. Investors took a cue from the carnage across all AT1s following the Credit Suisse write down and just sold bank preferreds indiscriminately. Suddenly and seemingly overnight, bank stocks, bonds, and preferreds have become kryptonite.

A quick profile of the preferreds market:

stonebridge

And a good summary of hybrid securities. The preferreds/CoCo/AT1 market totals about $1.75T in total assets.

{kind=link}

What Funds Were Affected Most?

Investors across the globe started investigating annual reports and fund holdings looking for Credit Suisse line items. Unfortunately, this is NOT what was a good indicator of what would be hit on price. AT1 allocation within bond funds was.

That is because most bondholders of CS bonds were actually made whole. We discussed this a bit on the SA chat as some investors/members were holding Credit Suisse AG senior secured bonds.

For example, check out the difference between two Credit Suisse bonds; one is a AT1 and one is a traditional debt obligation.

Here is a CS AT1 bond - Credit Suisse AG 7.50% 12/31/3999 (H9200RAA9) . The bonds were trading at approximately $94 and then, poof!, they fell off a cliff. Even today, they trade around $4 as some investors think there is a chance that, through lawsuits, they will be able to recover more than that.

finra

Next, we have the traditional debt obligation. This is the Credit Suisse AG London 4.0% 2024 (22553QAB3) . You can see from the price chart below that while the price took a hit from $99 to $90, it was no where even near distressed levels (typically considered sub-$70) or near bankruptcy levels.

finra

Investors focusing on counterparty risk (derivatives issued by Credit Suisse but owned by another entity like a closed-end fund) or direct bonds of Credit Suisse should instead be looking for exposure to AT1 bonds. That exposure is what hurt most of these preferred stock fund NAVs in the last two weeks as investors shunned the space following the Credit Suisse write-down.

Closed-End Funds Have Been Pummeled

And not just on price, but on NAV. Many of these funds have CoCo/AT1 exposure. Some have just recently began adding them into their portfolios or recently increased it. For instance, JPT, as part of their conversion from a term fund to a perpetual, included an investment policy amendment to increase exposure to CoCos.

All of the Nuveen preferred CEFs can invest in CEFs. But some have constraints as to how much. JPT, when they converted to a perpetual fund, changed their investment policy to state:

The Fund will invest at least 80% of its Assets (as defined below) in preferred securities and other income producing securities, including hybrid securities such as contingent capital securities (sometimes referred to as “CoCos”).

NPCT can only invest up to 20% in CoCo's.

PTA up to 20%

LDP unlimited

PSF unlimited

JPI unlimited

JPT unlimited

JPI is interesting here as it is the last term fund in the preferred space. It is now trading at the lowest z-score ("cheapest") with a -6.5% discount and liquidates Aug. 31, 2024 (16 months). That discount is thus a captured return - what we call tailwind yield - over that time period. That is in addition to, the state covered yield.

However, there is a HIGH risk that the fund will do what JPT did and convert to a perpetual fund. If they do, they will likely do the same shareholder-friendly initiatives that they did last time. Those included:

Prior to the effectiveness of the restructuring, the fund will conduct a tender offer allowing shareholders to offer up to 100% of their shares for repurchase at net asset value . The fund expects to announce the tender offer shortly. If the fund’s net assets taking into account shares properly tendered in the tender offer would be $70 million or greater, the tender offer will be completed and the fund’s term structure will be eliminated. If the fund’s net assets after taking into account the shares tendered in the tender offer would be less than $70 million, the tender offer will not be completed and no common shares will be repurchased, the restructuring proposal will not be implemented and instead, the fund will proceed to terminate as scheduled pursuant to its original term on or before March 1, 2022

Thus, whether they liquidate on time or not, they will likely give investors an opportunity to tender at NAV.

The Cohen & Steers funds are enticing since they have been able to utilize fixed-cost leverage in a rising rate environment. That has allowed them to maintain their distribution while most other funds have cut multiple times.

Cohen & Steers Tax-Adv Pref Sec & Inc ( PTA ) was even able to increase their distribution on Jan 1, 2023.

If we look at NAV total returns over the last year, Cohen&Steers Limited Duration Pref&Inc ( LDP ) leads the pack for this very reason. PTA and PSF are in the quartile of 1-year total returns. But they are also the most expensive funds in the preferred space.

The funds most susceptible to rising rates - Flaherty & Crumrine funds and to a lesser extent, the Nuveen funds, are near the bottom of the pack.

So the question is, if we have seen peak rates, then wouldn't we want to do the reverse and be in the funds that were at the bottom of the pack last year.

The funds that have cut the most, and had the most headwind due to rising rates, should be best positioned going forward from declining rates and their cheaper valuation.

Our best options:

- Nuveen Pref & Inc Term ( JPI ), discount -6.5%, yield 8.51%

- First Trust Inter Dur Pref & Inc ( FPF ), discount -11.6%, yield 8.7%

- Flah & Crum Total Return ( FLC ), discount -8.6%, yield -8.6%

Individual Preferreds From Landlord Investor

With elevated uncertainty in the banking sector, I would be cautious on buying bank preferreds and bonds. However, the widespread decline in the preferreds/hybrids market has resulted in the "baby getting thrown out with the bathwater", particularly in the insurance industry. Below are some preferreds and jr. subordinated notes worth considering.

Insurance

Prudential 6.75% 2053 jr. sub note par $1000 CUSIP 744320BL5: Large life insurer. Callable 2033 when it floats at 5 YR UST + 2.84%. Yield: 6.9%. Baa1/BBB+

ALL-B : Large P&C insurer 2053 jr. sub note that is currently floating at L+3.16%. 49 cent ex-div on 3/31. Baa1/BBB

LNC-D : Life insurance. On negative watch due to underwriting issues that should be one-time. Yield: 9%. Baa3/BBB- (neg)

ATH-E : General annuity provider. No listed common stock but wholly owned subsidiary of Apollo Global Management. Yield: 8.2%. Baa3/BBB

ESGRP : Specialty and runoff insurance. Solid long term track record but significant equity holdings in their investment portfolio. Yield: 8.25%. BB+

BHFAN : Variable annuity provider. VA providers tend to do better in a rising rate and rising stock market environment. Yield: 8.2%. Ba2/BBB-

JXN-A : Variable annuity provider. Yield: 9.3%. Ba1/BB+

KMPB : P&C insurance. 2062 jr. sub note. Yield: 8%. Ba1/BB+

SPNT-B : P&C insurance and reinsurance. Floats at 5 YR UST + 7.3% in Feb 2026. Yield: 8.7%. BB+ (neg watch)

Asset Management

AAM-A/B : Large asset management company. No listed common stock but wholly owned subsidiary of Apollo Global Mgmt. Yield: 7.5%. BBB

OAK-B . Large asset management company. No listed common stock but majority owned subsidiary of Brookfield Financial. K-1. Yield: 7.75%. BBB

Infrastructure:

BEPH : Renewable power generation company. Sells electricity on 10+ year contracts with inflation escalators to strong counter-parties. Yield: 7.7%. BBB-

BIPI : Diversified infrastructure. Yield: 7.8%. BBB-

Banking

WFC-Q : Fourth largest US bank should be beneficiary of deposits fleeing regional banks. Floats at L+3.09% on 9/15/2023. Baa2/BB+

ZIONL : Regional bank. 2028 jr. sub note that will float at L+3.89% on 9/15/2023. YTM: Over 10%. BBB

Concluding Thoughts and Action Items

Preferreds are an area of the market that is currently being dislocated thanks to the banking sector events of the last few weeks. The contagion appears to be somewhat contained though investors and the market are still of the view that another shoe is going to drop soon.

It will take time for that fear to subside. Once it does, you'll start to see prices/NAVs recover but it will be slow. As we have noted, these tend to fall fast and recover slow. The good thing is that you get paid to wait while they recover.

For further details see:

Preferreds Opportunity: Assessing The Carnage, What's Been Thrown Out With The Bathwater