AGNCO - Preferreds Weekly Review: Mortgage REITs Kick Off The Earnings Season

Summary

- We take a look at the action in preferreds and baby bonds through the first week of February and highlight some of the key themes we are watching.

- Preferreds put up another strong week, extending their rally into February.

- Mortgage REITs put up good Q4 numbers with a rise in book values and additional equity issuance - two factors supporting equity coverage.

This article was first released to Systematic Income subscribers and free trials on Feb. 5 .

Welcome to another installment of our Preferreds Market Weekly Review, where we discuss preferred stock and baby bond market activity from both the bottom-up, highlighting individual news and events, as well as top-down, providing an overview of the broader market. We also try to add some historical context as well as relevant themes that look to be driving markets or that investors ought to be mindful of. This update covers the period through the first week of February.

Be sure to check out our other weekly updates covering the business development company ("BDC") as well as the closed-end fund ("CEF") markets for perspectives across the broader income space.

Market Action

Preferreds put up another positive week, extending a consistently strong performance period. Year-to-date all sectors are up with half the sectors sporting double-digit returns.

Systematic Income

January was the strongest month for the space since the bounce in April of 2020.

Systematic Income

Yields have fallen close to 1% from their peak last year.

Systematic Income Preferreds Tool

Market Themes

As usual, agency mortgage REITs kicked off the income reporting period. AGNC Investment Corp ( AGNC ) reported good results. Book value rose 8% over the quarter, though it remains more than a third below its end-2021 level. Over Q4, the company issued 23.3m of new shares for a total of $187m. This is about a 3% increase in equity and is a boost to the equity / preferreds coverage figure. Overall, current equity coverage of 4.7x is pretty good though not as high as that of DX or NLY which are also worth a look in the sector.

An important point about allocating to mREIT common shares is that the AGNC portfolio had $82bn of assets at the end of 2021 and this has been reduced to $60bn - a drop of 27%. If Agency spreads miraculously revert back to their 2021 levels, AGNC book value will not retrace its 2021 level for the simple reason that it now holds fewer assets - a function of not just the price drop but also of a lower "notional" value of the Agency MBS in its portfolio.

For instance, agencies are down around 10% over the past year - a much smaller figure than the 27% asset value drop. This residual of 17% is the stuff the company had to sell down to keep leverage from rising. This will continue to be a drag on the company's income and return profile. It also means that it's unlikely to retrace its previous book value of $16+. This makes holding Agency mREIT common shares "through the cycle" a very tough strategy and one that requires a more tactical approach. Preferreds, on the other hand, are much more compelling as strategic assets. The chart below shows the normalized total return of AGNC common and preferred shares over the last decade.

Systematic Income

Another Agency mortgage REIT - Dynex Capital ( DX ) - released Q4 numbers. Book value was up 4% and leverage moved lower to 6.1x. Dynex Capital tends to run a lower-beta portfolio. Recall AGNC book value was up about twice the DX figure in Q4, however it also means the book value will hold up during drawdowns - since end of 2021 its book value is down less than 20% versus more than 30% for AGNC.

Another positive feature of DX is that its equity / coverage tends to be on the higher side in the sector. This was boosted by $90m of new equity issuance over Q4 which is nice to see. At the moment the equity / preferred coverage is the same as NLY at 7.1x, sharing the highest level of the sub-sector, however Q4 NLY coverage will likely move higher given book value trends. DX has only one preferred - ( DX.PC ) and its positive feature is a high reset yield of 9.2% (i.e. the expected stripped yield when the stock floats on the first call date if not redeemed) for the Agency preferred sub-sector.

This tends to anchor the stock - it's down less than 2% over the past year which is unusual for a relatively long-dated first call in 2025. The high reset yield along with the lower-beta nature of the portfolio and high equity/preferred coverage makes the preferred one of the strongest in the sector. This is not really recognized by the market so it tends to trade at an elevated yield. It remains in our Core Income Portfolio at a 7.5% yield.

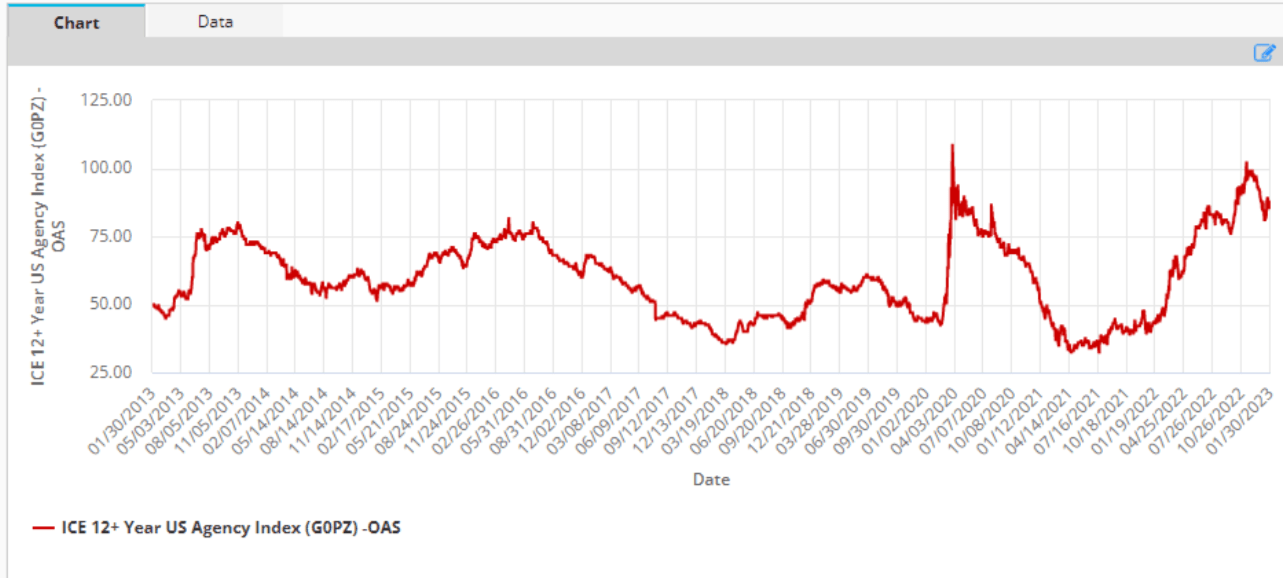

Overall, Agencies remain fairly compelling assets even with the recent rally. Comically, longer-term, Agency spreads (i.e. Agency MBS yields above Treasuries) bounced off a very similar level they reached in March of 2020, before staging a sharp rally. Reaching a credit spread north of 1% was a nice time to add to the asset class, whether through common or preferreds. In terms of the big picture, holding zero credit risk assets with a similar credit spread as investment-grade bonds, lower duration than investment-grade bonds and without the overhang of negative convexity does seem like a very good trade. Maybe not good enough to buy common mREIT (perhaps for those with an iron stomach or a very tactical approach) but certainly good enough to buy Agency mREIT preferreds from NLY, DX and AGNC.

{kind=link}

Longer-term agency spreads are still on the order of 0.85% or so, so the sector remains attractive. Sector preferreds have rallied quite a bit already - on the order of mid-to-high single digits this year but yields remain attractive. Stocks that remain decent options are NLY.PF which already floats at Libor + 5% (i.e. north of 10% yield) as well as a longer-duration option like AGNCL (8.3% yield) - not the first time these are highlighted. This kind of allocation also diversifies across Libor and Treasury coupon anchors as well as duration profile.

For further details see:

Preferreds Weekly Review: Mortgage REITs Kick Off The Earnings Season