WHF - Preferreds Weekly Review: PMT Holders Got Robbed?

2023-09-09 11:59:29 ET

Summary

- We take a look at the action in preferreds and baby bonds through the last week of August and highlight some of the key themes we are watching.

- Preferreds had a strong week with a nearly 2% return, bringing sector valuation.

- Investor indignation over two PMT preferreds failing to switch to floating rates sparks debate on fallback options.

- We highlight the new baby bond from BDC WHF.

Welcome to another installment of our Preferreds Market Weekly Review, where we discuss preferred stock and baby bond market activity from both the bottom-up, highlighting individual news and events, as well as top-down, providing an overview of the broader market. We also try to add some historical context as well as relevant themes that look to be driving markets or that investors ought to be mindful of. This update covers the period through the last week of August.

Be sure to check out our other weekly updates covering the business development company ("BDC") as well as the closed-end fund ("CEF") markets for perspectives across the broader income space.

Market Action

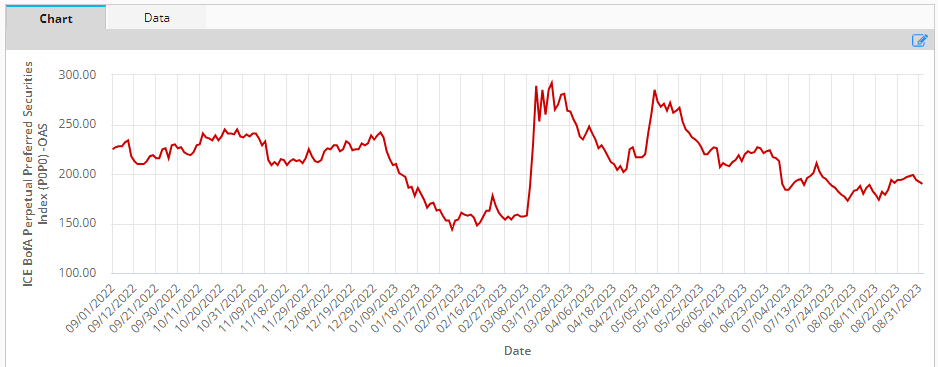

Preferreds had a strong week with a nearly 2% return. The sector valuation, as gauged by the option-adjusted spread, is back to the level of the start of the year, prior to wild swings we saw in the first half of 2023.

{kind=link}

Despite this rally in spreads however, the recent back-up in Treasury yields means that overall sector yields remain at very attractive levels.

Systematic Income Preferreds Tool

Market Themes

There is a lot of investor indignation about the two PMT preferreds that are failing to switch to floating rates and will instead carry on paying their original fixed coupon - something we discussed in more detail here . Here we highlight 5 responses we have seen.

One view has it that on the first floating period instead of using the previous fixed dividend as the fallback, the stock should set the coupon to Libor first and then use that fixed Libor level plus spread as the new dividend going forward. The reason this doesn’t make sense is very simple. Libor no longer exists so by the time PMT.PA and PMT.PB float there will be no Libor to use for that first dividend period.

Two, PMT can’t do this because that wasn’t the intent of the issuance. The stock was marketed as a Fix/Float stock and float it must. This is not how security documentation works. You can almost use this logic to argue that a default is not legal because all debt securities (ex zero coupon securities) are marketed as coupon paying securities so a default and failure to pay the coupon is not legal - obviously absurd.

The reason Libor fallbacks exist in the prospectus is to show precisely what happens if Libor is no longer there. Just because people don’t like the fallback doesn’t make it illegal.

A third complaint is that the SEC and the Fed have not mandated a switch to SOFR for Fix/Float Libor preferreds. However, this would result in the government effectively tearing up private contracts between consenting adults and replacing it with something "better" - not a great precedent. Many people who fall on the wrong side of the PMT issue would be up in arms if the government did the same in the future on something that went against their interests.

Four, holders should have an easier time suing PMT than MS (recall that Morgan Stanley also fixed their Fix/Float preferreds) because it's easier to prove harm. The Fix/Float PMT preferreds fell 6-7% in the week following the announcement, underperforming the sector by around 6%. The fixed-rate PMT.PC has not moved a whole lot. MS Fix/Float preferreds, on the other hand, didn't appear to move much on their announcement.

This sounds airtight until we recall that the board of the company has a limited duty to preferreds holders. As we wrote earlier,

the board's fiduciary duty to preferred stockholders is limited. Specifically, there is no duty to maximize the return of preferred stockholders. And while the board has fiduciary duties to preferreds stockholders those duties are limited to cases where the interests of preferred and common stockholders are aligned.

Clearly the interests of common and preferreds shareholders are not aligned here. In fact, it's easier to argue that PMT's common shareholders could have sued the company if it chose to float the preferreds. Of course this would be a stretch but it's an easier argument to make.

Moreover, this is just how optionality works. If there is some uncertainty between two outcomes (say a call / no call or floating / remaining fixed), the price of a security will be somewhere between the two outcomes. Once the outcome is known the price will move to fully reflect that outcome rather than only partly reflect that outcome. That's what happened here. PMT had an option and it chose to fix the preferreds so the prices moved to reflect that choice.

Five, PMT is in the wrong because the possibility of Libor going away was not listed as a risk factor in the prospectus. Neither did MS and, in any case, this is surely an odd argument. After all a big chunk of the prospectus talks about Libor going away and what the company can do if that happens. It's odd to then require it to also list it as a risk factor. We may as well ask the company to list its perpetual structure as a risk factor as well - you may never see your principal again because this is a perpetual security.

Outside of these "hot takes", perhaps the most important point to consider is who exactly is going to sue PMT? The total loss for individual shareholders is not large and there are unlikely to be PMT preferred "whales" who lost a ton of money and will fund the lawsuit. Institutional investors are unlikely to be able to claim that they were misled by the company. There is also unlikely to be a large dollar payoff at the end of the road even if the lawsuit is successful - making it improbable that a law firm would take on the case in the hope of a big settlement.

Overall, we are not convinced of the view that PMT is plainly in the wrong and it's only a matter of time that it is sued and found at fault. Clearly, this is disappointing and unfortunate. It's also not economically sensible given the small footprint that preferreds have in the company's capital structure and given its risk premium will likely increase over the medium term, likely offsetting a modest benefit it gets in the near term.

Market Commentary

The BDC WhiteHorse ( WHF ) bond is now trading ( WHFCL ). It has the usual 5Y non-call 3Y structure i.e. a 5Y maturity with a first call date in 3 years.

Checking in on the key fundamental metrics important for BDC bonds, 1) leverage of the company is reasonable - a bit above the sector median, 2) historic NAV resilience is good - the company has outperformed the sector on a 5Y basis and underperformed on a 3Y basis, 3) the secured debt portion of the capital structure is below the sector average which is good and 4) the company’s first-lien allocation is well above the sector average - also good.

The yield kicked off around an attractive 8.5% level and has now moved to sub-8% which is fair value in our view - at the upper end of decent-quality BDC baby bonds. The bond is a reasonable choice for the purpose of diversification from other BDC baby bonds and in its own right.

For further details see:

Preferreds Weekly Review: PMT Holders Got Robbed?