CGBD - Preferreds Weekly Review: PSEC Sneaks In A Tender Offer For Series A

2023-12-10 01:24:47 ET

Summary

- We take a look at the action in preferreds and baby bonds through the first week of December and highlight some of the key themes we are watching.

- Preferred stocks had a strong return of over 3% this week, pushing the sector to a 7% return for the year.

- BDC Prospect Capital completed a tender offer of their public preferred Series A, with low participation due to falling yields.

- CGBDL - a new bond from BDC CGBD - started trading, however the yield is too low to be interesting.

Welcome to another installment of our Preferreds Market Weekly Review, where we discuss preferred stock and baby bond market activity from both the bottom-up, highlighting individual news and events, as well as the top-down, providing an overview of the broader market. We also try to add some historical context as well as relevant themes that look to be driving markets or that investors ought to be mindful of. This update covers the period through the first week of December.

Be sure to check out our other weekly updates covering the business development company ("BDC") as well as the closed-end fund ("CEF") markets for perspectives across the broader income space.

Market Action

Preferreds delivered another strong return of above 3% this week, only second to REITs, across the broader income space. The late rally across both stocks and Treasuries pushed the sector to a respectable 7% return on the year, despite a couple of Bank-related wobbles during the year.

Preferreds spreads are not far off their tights over the last couple of years, making the sector somewhat less compelling for new capital at this point.

Systematic Income CEF Tool

Yields have retraced around 0.8% and appear to be headed back towards 7%.

Systematic Income CEF Tool

Market Themes

BDC Prospect Capital ( PSEC ) completed the tender offer of their public preferred Series A ( PSEC.PR.A ). There are a couple of reasons why they chose to do this.

One, rates had shot up prior to the tender offer (pushing the price of the preferred lower). Perhaps PSEC thought that rates were going to fall so they want to get rid of their low-priced long-dated financing in the hope of replacing it with lower-rate financing down the road. You can't fault them here - rates did indeed fall sharply right after the tender offer announcement though perhaps too sharply for the tender offer to be successful.

Two, the PSEC NAV has been under pressure over the last 6 quarters or so and they just don’t need as much financing now that book value is lower.

Systematic Income

Third, perhaps instead of having the public preferred they would rather replace it by issuing additional private preferreds for various reasons. The low dollar price of the public preferred is not making the company look good for one (the private preferreds are marked at $25).

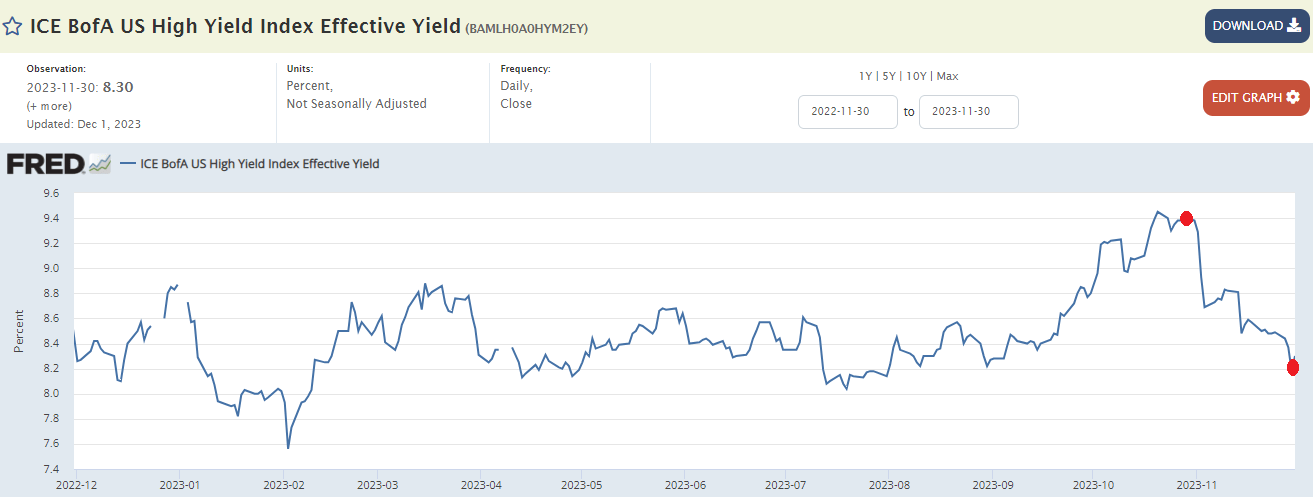

In any case, with the tender offer behind us we can have a look at the results. The company said that out of 5.88m outstanding shares, there were 0.63m of shares tendered back or a bit over 10%. That seems low and it’s low because the tender wasn’t as good a deal as it was when it was first announced. This is for the simple reason that corporate yields have fallen a lot over November as the chart below shows. The first red dot marks the announcement of the tender offer and the second marks its expiration.

{kind=link}

So while the tender offer was originally at a premium of $1.7 to the then trading price, that premium has obviously moved lower as yields have fallen (and fixed-income asset prices have risen).

An important question for investors evaluating the tender offer was whether there was any premium embedded in the tender offer by the end of November. Immediately prior to the tender expiry we estimated the fair-value of the preferred price. This was done based on a yield of 8.41% i.e. 1% below the pre-tender offer 9.41% yield (in line with the drop in high-yield corporate bond yields). The answer was $15.90 - right near the tender offer price. In other words, it didn't look like there was any premium left at all in the tender offer.

We can quibble about this calculation - PSEC.PR.A has a higher-quality profile, going by ratings, than the typical high-yield corporate bond and a much longer duration. However, in our view these differences were partly, if not largely, offsetting.

The fact that PSEC.PR.A ended the week around $15.85 suggests we weren't miles off our calculation and explains why the tender offer take-up was pretty low. It's very likely the company will reset the tender at a higher price to see if it has better luck.

Market Commentary

The new 8.2% 2028 bond ( CGBDL ) from BDC CGBD has started trading. In terms of the key risk factors, leverage is slightly below average which is good as is the allocation to first-lien loans which is less good, the NAV profile has been fairly stable which is good and the credit facility takes up well below half of the liability profile which is also good.

Systematic Income

The yield of the bond at 6.5% is quite a bit below the BDC baby bond average of 8%. This is, arguably, deserved given the combination of the risk factors however it doesn't make the bond a buy.

For further details see:

Preferreds Weekly Review: PSEC Sneaks In A Tender Offer For Series A