PSA - Preferreds Weekly Review: Rate Rally Shines Light On Call Risk

2023-12-17 03:38:55 ET

Summary

- We take a look at the action in preferreds and baby bonds through the second week of December and highlight some of the key themes we are watching.

- Preferreds finished lower as Treasury yields slightly backed up, but most sectors remained positive for the month.

- Investors should consider lower-coupon preferreds to mitigate redemption risk and leave room for a rally if rates continue to decrease.

- We highlight the new bond from BDC NMFC.

Welcome to another installment of our Preferreds Market Weekly Review, where we discuss preferred stock and baby bond market activity from both the bottom-up, highlighting individual news and events, as well as the top-down, providing an overview of the broader market. We also try to add some historical context as well as relevant themes that look to be driving markets or that investors ought to be mindful of. This update covers the period through the second week of December.

Be sure to check out our other weekly updates covering the business development company ("BDC") as well as the closed-end fund ("CEF") markets for perspectives across the broader income space.

Market Action

Preferreds finished lower on the week as Treasury yields backed up slightly. Most sectors, however, remain in the green month-to-date.

Systematic Income

The yield for the median retail preferred remains north of 7% - well off a near-8% level just last month.

Systematic Income Preferreds Tool

The recent drop in yields is primarily due to the fall in Treasury yields as credit spreads have remained range-bound.

Systematic Income Preferreds Tool

Market Themes

The broader income market has enjoyed nice gains since the start of November as longer-term rates have rallied. The median $25-"par" preferred has gotten off the floor and rallied a couple of points as the following chart shows.

Systematic Income Preferreds Tool

This rally highlights an important risk that has not exactly been top of mind for preferreds investors since 2022 - redemption risk.

As many investors know, nearly all preferreds are callable/redeemable by issuers. This tends to happen just at the worst time when interest rates fall and the previously "juicy" yields are called away by issuers only to be refinanced by securities with lower coupons and yields.

There are a couple of ways that investors can mitigate this dynamic. One is to tilt to lower-coupon preferreds which are much less likely to be redeemed as their price tends to be further below "par" than higher-coupon preferreds from the same issuer.

A side benefit of lower-coupon preferreds is that they have much more room to rally if rates keep moving lower. Once preferreds prices move north of $25, the rally invariably stalls given the increased likelihood of redemption. This is particularly the case for preferreds that are immediately callable.

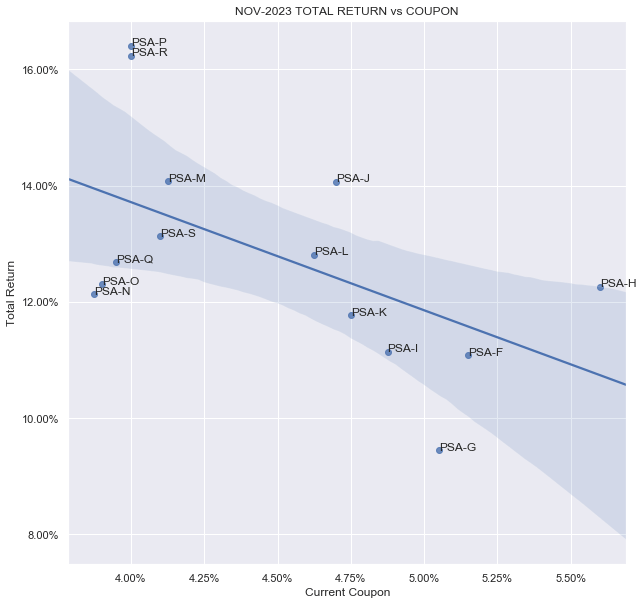

For example, the chart below shows the Public Storage ( PSA ) suite of preferreds. Lower coupon preferreds (those on the left side of the x-axis) have rallied more over November than higher coupon PSA preferreds. This is for the simple reason that the lower coupon preferreds trade at lower prices with more room to rally up to $25.

{kind=link}

In short, investors who want to mitigate the risk of redemption and leave more room for a rally in case of even lower rates should consider lower-coupon / lower-price shares of the same issuer, particularly if they are not giving up any yield to do that.

As a technical sidenote, higher-coupon securities of the same issuer should trade at a slightly higher yield than their lower-coupon counterparts to compensate investors for their greater likelihood of redemption (i.e. due to a higher price for the embedded call that shareholders are implicitly short). However, because this doesn't always happen, it creates an opportunity for investors to achieve the same yield while lowering the likelihood of redemption.

Another way to mitigate the chance of redemption is to, well, buy non-callable preferreds. Admittedly, there are not a ton of options here but there are some. A couple of bank preferreds like WFC.PL and BAC.PL with yields at 6.6% and 6.3% respectively are worth a look (some non-callable preferreds are convertible, however, their conversion strikes are often far enough to keep the possibility of conversion minimal) as well as stocks like SOCGP and LBRDP with yields of 6.1% and 8.6%.

Market Commentary

The NMFC BDC baby bond ( NMFCZ ) started trading recently. The timing of the bond wasn’t very favorable for the company and it has already rallied 5%. The NAV has been stable over time - an important factor for bondholders. Leverage is above average and the first-lien allocation is below average which is not ideal. The credit facility makes up around half the liabilities, which is about average for the sector.

Overall, the metrics are pretty decent. What’s less decent is the yield which is now sub-6%. At that level, the bond makes very little sense. It’s trading to the 2025 call date (i.e. the yield-to-worst is calculated with the assumption that it is redeemed in 2025 at par) which offers around 1% more than the 2Y Treasury bond - pretty ridiculous. The yield-to-maturity is better at 7.2% however this assumes no redemption until maturity - certainly possible but not necessarily a sound assumption.

Stance And Takeaways

Given the sharp drop in Treasury yields and the jump in preferreds prices, investors need to be on the lookout for preferreds that have traded back up to "par". Specifically, it's worth checking within the issuer suite for lower-priced preferreds trading at a similar yield. A rotation to a similar-yielding lower-price preferred of the same issuer can give investors a "free lunch" to lock in the same yield but lower the risk of redemption.

Something else to keep an eye on is the overall duration of the portfolio. Overall yields are now somewhat less compelling at current levels and are more prone to a reversal higher. Lightening up on duration by rotating to Fix/Float and floating-rate preferreds takes advantage of a once-again very inverted yield curve and mitigates potential portfolio losses if rates move back up.

For further details see:

Preferreds Weekly Review: Rate Rally Shines Light On Call Risk