EAF - Preformed Line Products Company: Patience Is Key

2023-10-24 13:13:31 ET

Summary

- Preformed Line Products Company offers products for data infrastructure, including power conductor and fiber communication cables.

- Despite the stock's underperformance, Preformed Line Products' financial performance is strong, with growing revenue, profits, and cash flows.

- On a forward basis, Preformed Line Products stock is attractively priced, with low multiples, making it a potentially good investment opportunity.

In a world that is becoming more and more data-centric by the day, the products and services that are needed in order to make everything function is bound to change. Although data itself might seem like an easy thing to work with, the amount of infrastructure needed in order to collect it, organize it, and transport, is significant. And one of the firms that is dedicated to these kinds of activities is Preformed Line Products Company ( PLPC ). This particular enterprise creates goods centered around power conductor and fiber communication cables, protective closures used for fixed line communication networks, and more. Of course, the firm does offer up its products for other industries as well, such as the energy industry.

Earlier this year, in May to be precise, I found myself taking a bullish stance on the company. I found myself impressed with the attractive upside that shares had seen leading up to that point. This upside was not without cause, however. It was driven, I concluded at that time, by robust financial performance. With that trend set to continue and with shares of the company looking attractively priced, I could not help but rate the company a "buy." This is the kind of rating I assign a firm that should achieve an upside that outperforms the broader market for the foreseeable future. But sadly, that has not come to pass. Since the publication of that article, the stock has been virtually flat. That compares to the 6% increase seen by the S&P 500 (SP500) over the same window of time.

You would think, given this return disparity, that the financial picture of Preformed Line Products was beginning to worsen. But that couldn't be further from the truth. Revenue, profits, and cash flows are all growing nicely. Shares look very attractive, particularly on a forward basis. So, given these factors, I do still believe that the "buy" rating I assigned the stock previously remains appropriate for now.

Performance keeps getting better

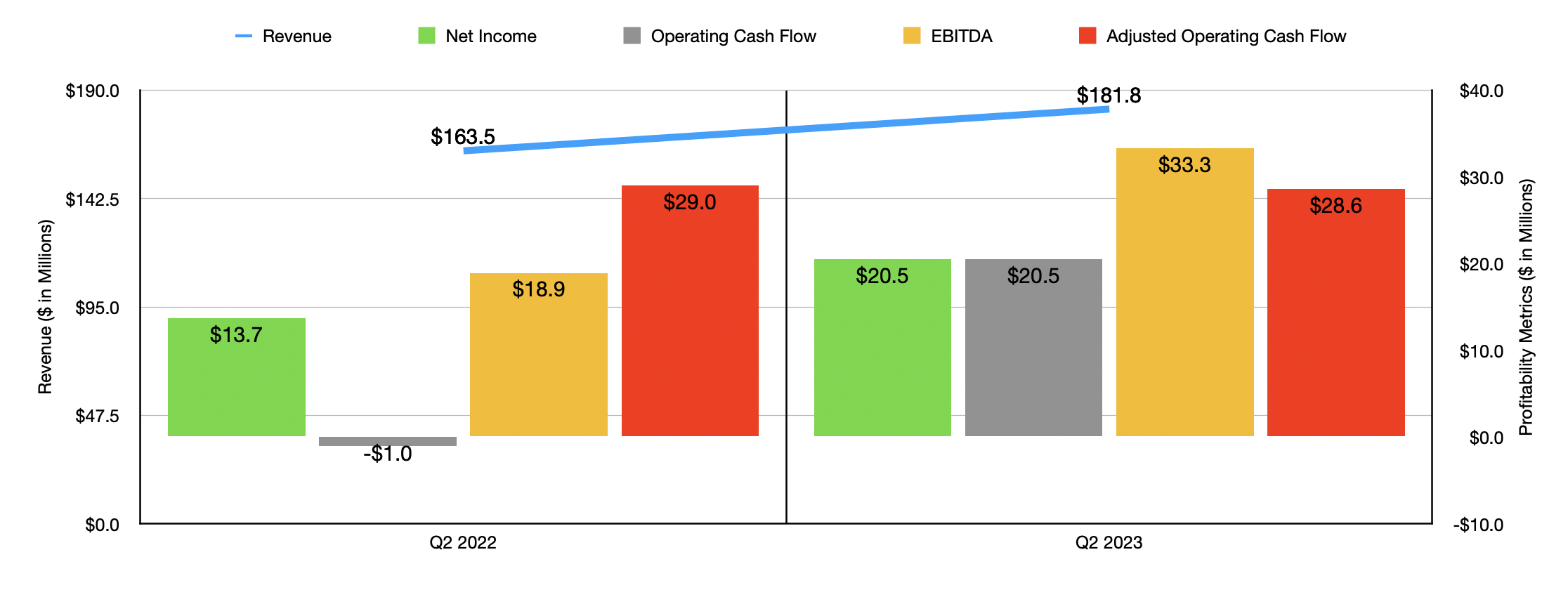

When you see a significant return disparity between one company and the market, the general assumption you might make is that the fundamental performance of that company has been weakening. But that couldn't be further from the truth. Consider, for instance, the most recent quarter for which data is available. This is the second quarter of the company's 2023 fiscal year. For that time, revenue came in at $181.8 million. That's 11.2% higher than the $163.5 million generated one year earlier.

{kind=link}

The vast majority of this sales increase, approximately $13.6 million in all, came from its PLP-USA operations. This is the domestic unit of the company and, as of its most recent quarter, it accounted for $97 million, or 53.3%, of the company's revenue. This jump in sales, amounting to a year-over-year increase of 16.2%, was largely thanks to a volume increase from both the energy product and communication spaces. Digging in deeper, this is not surprising to me. Even though it's true that the company does generate a lot of revenue from the telecommunications space, a whopping 60% of sales come from energy customers.

There were, of course, other parts of the company that grew as well. Revenue under the EMEA (Europe, Middle East, and Africa) operations of the company jumped 13.6%, while revenue under the Asia Pacific unit grew 5.1%. The only weakness came from the Americas, excluding the US, with sales dropping from $22.4 million to $21.5 million. But if we adjust for foreign currency fluctuations, even it would have increased modestly to the tune of $338,000.

{kind=link}

This rise in revenue was accompanied by a rise in profits as well. Net income for the most recent quarter totaled $20.5 million. That's up 49.6% over the $13.7 million reported only one year earlier. The rise in revenue absolutely helped with this. But the company also enjoyed an increase in its gross profit margin from 32.2% to 36.5%. When applied to the revenue generated in just the most recent quarter on its own, this disparity accounts for another $7.8 million, approximately all the bottom line that the business was missing. This improvement, management said, was attributable to increased sales volumes, higher prices, and a reduction in material costs.

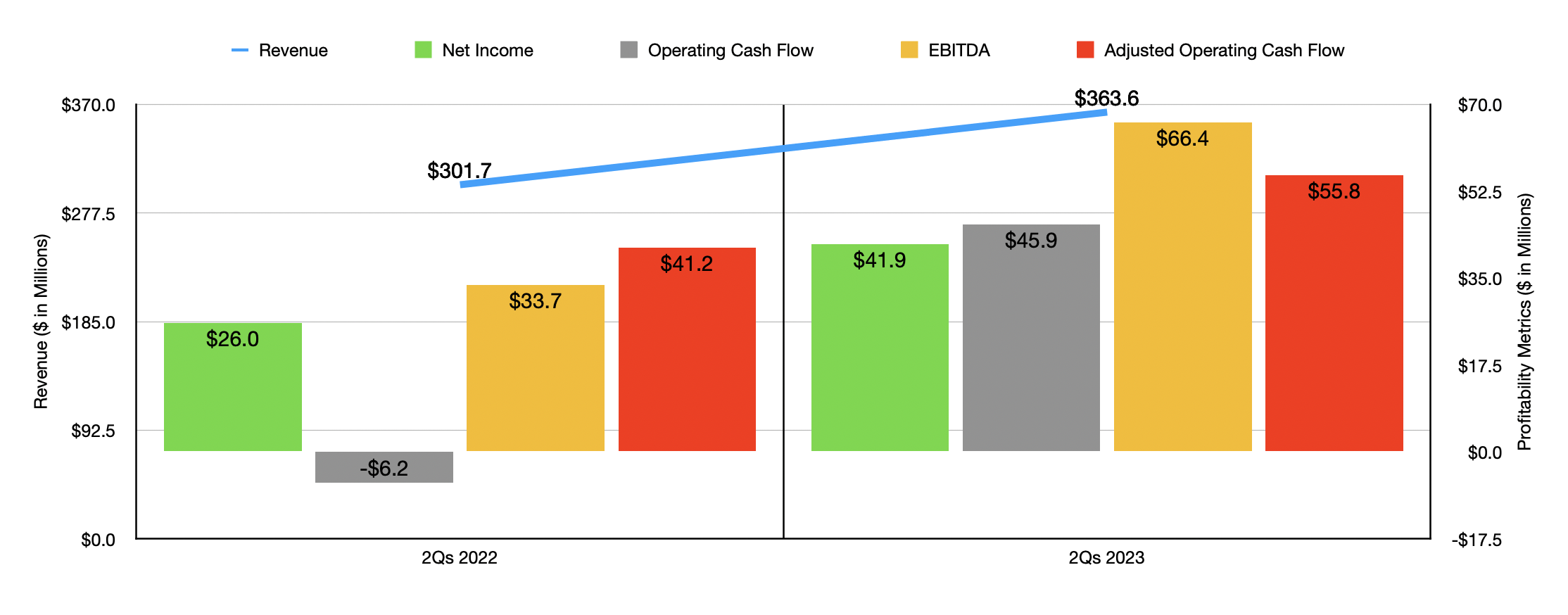

Other profitability metrics followed a similar trajectory. Operating cash flow went from negative $1 million to $20.5 million. If we adjust for changes in working capital, it would have declined from $29 million to $28.6 million. On the other hand, EBITDA for the company expanded from $18.9 million to $33.3 million. As you can see in the chart above, financial performance for the first half of this year in its entirety is also quite a bit higher than what it was at the same time in 2022. So the second quarter was not a one-time blip on the radar.

{kind=link}

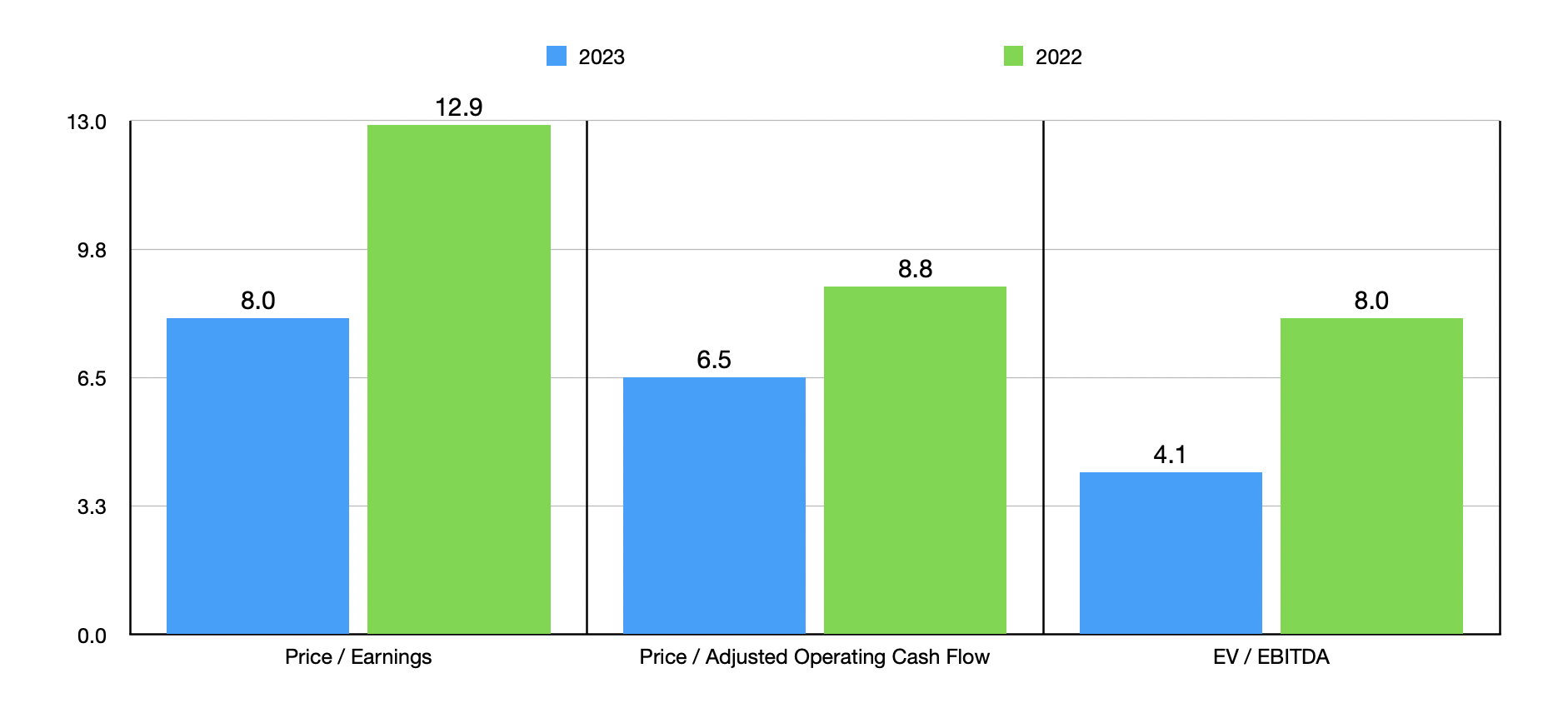

Since we really don't know what to expect for the rest of the fiscal year, I decided to annualize the results experienced so far. That gave me projected net profits of $87.7 million, adjusted operating cash flow of $108.1 million, and EBITDA of $183.6 million. I then took that data and used it to value the company on a forward basis. This can be seen in the chart above. On a price-to-earnings basis, the company is trading at a multiple of 8. This is a meaningful improvement compared to the 12.9 rating that we got using data from last year. Other multiples showed meaningful declines as well. The price-to-adjusted operating cash flow multiple fell from 8.8 to 6.5, while the EV-to-EBITDA multiple was nearly halved from 8 to 4.1.

It's always tempting to assume that the future will look like the recent past. But it's always better to be safe rather than sorry. Instead of assuming that my forward estimates for the company are accurate, I believe that the significant disparity in valuation caused by that should push investors to value the company instead of using the data from 2022. If the firm comes out as attractive with those higher multiples, then you are baking in a nice margin of safety. And when dealing with real money, that's always a good idea.

So in the table below, I compared the data from 2022 to five similar firms. Using both the price-to-earnings approach and the EV to EBITDA approach, I found that only one of the five companies was cheaper than the Preformed Line Products Company. And using the price to operating cash flow approach, only two were.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Preformed Line Products Company |

| 12.9 |

| 8.8 |

| 8.0 |

| Powell Industries ( POWL ) |

| 26.8 |

| 7.6 |

| 14.4 |

| GrafTech International ( EAF ) |

| 7.1 |

| 6.8 |

| 6.6 |

| Thermon Group Holdings ( THR ) |

| 24.2 |

| 19.8 |

| 12.5 |

| Shoals Technologies Grou p ( SHLS ) |

| 16.1 |

| 26.7 |

| 13.6 |

| Acuity Brands ( AYI ) |

| 16.7 |

| 10.0 |

| 10.0 |

Takeaway

So far this year, things are going quite nicely for Preformed Line Products Company. It's unclear whether this trend will continue. But even if financial performance reverts back to what it was last year, shares look cheap on both an absolute basis and relative to similar firms. Yes, the stock has underperformed the broader market in recent months. But investing is not about short-term gains. Rather, it is about the long haul. And those who focus on the long haul should appreciate how cheap the stock is at this time and how healthy it currently appears to be.

For further details see:

Preformed Line Products Company: Patience Is Key