PINC - Premier: Second Guidance Downgrade Is Telling

2023-05-26 01:24:05 ET

Summary

- Another guidance downgrade is a key risk that must be factored into the debate.

- Economic earnings tightening, even with a lighter capital base, implying profitability headwinds going forward.

- Downgrades in both core business segments are telling of their underlying performance.

- Net-net, revise down to hold.

Investment Summary

A second guidance revision to the downside from Premier, Inc.'s ( PINC ) management has got me far less constructive on the company going forward. I do not believe it is a short candidate, but the latest examination findings suggest there's notable hurdles to overcome. Chief among these are regaining traction in its core business segments, and ratcheting up capital productivity, based on my estimates. Since my March publication on PINC , shares have sold off 18% at the time of writing.

The firm's Q3 FY'23 numbers do nothing to abate the near-term concerns. Management have revised FY'23 guidance down to $1.34Bn with downsides in both segments and this is not to be ignored. The stock still trades at 17x forward earnings, a nice discount, but not deep enough to overcome the impeding top-line headwinds. Question turns to what's been priced in already, and my estimates suggest the market may have already captured it all and have PINC priced accurately given the new set of forward expectations. Net-net, I revise my rating on PINC to a hold.

Figure 1.

{kind=link}

PINC Q3: A Look At What is Priced In

To understand the market's revised expectations on PINC's stock price, it is necessary to delve into the firm's various business' and each segment's performance. Notably, there are quality assets holding up each business segment in my opinion. The market's concerns are more financial-related in my estimation, something the firm can certainly overcome.

Curiously, the adjacent markets businesses have exhibited robust QoQ growth and are projected to achieve a notable 30-40% growth rate in FY'23. However, I find myself questioning the sustainability and long-term viability of this growth trajectory, following management's FY'23 revisions. Question is, is there enough spine in the rest of the portfolio.

I. Contigo Contributions

1. Integration

My thoughts are focused on Contigo Health, the firm's direct-to-provider ("DTP") and direct-to-employer ("DTE") health benefits platform. PINC has used Contigo as a vehicle to extract value at times:

- In 2022, it purchased key assets from TPRN Direct Pay and Devon Health ("TPRN") in October FY'22. This was on a $177.5mm valuation, and comprised contracts involving >900,000 providers across 4.1mm locations. I touched on this in my December PINC publication.

- Reports on integrating the assets are pushing along, per management (such as the centres of excellence and 3-rd party health plan solutions), but it is still early to gauge successes just yet in my opinion.

2. ConfigureNet Launch

The firm launched its ConfigureNet offering in Q1 as well, the rebranding of the TPRN assets. This is an out-of-network wrap offering, built from the 900,000 providers/4.1mm locations discussed earlier. Management noted it has shown initial traction and that is promising too, securing several customers in the quarter. This is absolutely needed given the revenue headwinds discussed later. Several new ConfigureNet customers have been secured in recent months. However, the sustainability of this momentum remains uncertain in my view, and ongoing scrutiny will be necessary.

Contigo's customer base is centred on provider-sponsored health plans and Fortune 50 companies, as well as other large self-insured employers. While this presents an avenue for potential expansion (in terms of pipeline), it is essential to assess whether this business is truly poised to penetrate self-funded employer health plans nationwide, outside of the large corporates. Is PINC offering a differentiated solution to reduce healthcare cost burden, or is it merely one among many players in a crowded market? That's a difficult one to answer in full, but my findings (presented later, regarding ROIC) suggest the competitive advantage may be waning.

II. Financial Performance - Revenue Downsides

Shifting to the financial performance, PINC's Q3 numbers caused a stir on the sell-side after release. Baird cut to neutral immediately and others followed suite.

1. Top Line Troubles

- Revenues contract by 7% YoY, supply chain services ("SCS") hit worst on a 14% decline. Performance services also tightened 9% YoY. In SCS fee revenue was flat and there was no help from its Continuum of Care group in Q1. On that note, I'd opine PINC's focus on technology enablement to enhance member efficiencies is commendable, but it raises questions about the sustainability and scalability of this growth driver.

- You can see capital expenditures allocated towards each segment paring back substantially from 2022-2023 over the 9-months, falling from $61mm to $58.4mm on aggregate. This tells me the firm isn't allocating further capital towards growing the top line either. I'd be looking to operating efficiencies and perhaps inorganic earnings growth (margins) from here.

Figure 2.

Data: PINC 10-Q, Q3 FY'23

2. Guidance Revised Lower

Several adjustments have been made to the revenue ranges given impeding headwinds that have seen PINC slash guidance twice now, once in the Q1 results, and once in February. The second downward revision is telling. Each respective business is plagued by fairly rudimentary hurdles:

- SCS revenue from excess market supply, and manufacturing delays;

- Performance services adjusted lower from pure demand weakening (macro-issues basically);

- Both from overall macro-challenges (tight money, cost inflation, etc.).

- The major drivers on this - a lower outlook in direct sourcing products to $250-$265mm in, and SCS revenues to $895mm. It also lowered performance services net revenue to $440mm at the lower rend of range.

Simply, it tells me that both businesses are underperforming. Hence, these revisions underscore the potential risk in the PINC investment debate right now, and uncertainties that PINC faces in the near term. Taking all these factors into account, management now projected FY'23 revenue of$1.34Bn to $1.39Bn, on new adj . EBITDA of $490mm to $510mm.

These adjustments also reflect the impact of changes in revenue guidance and Premier's amended agreement with FFF Enterprises, which has resulted in a change in accounting methodology for PINC's ownership interest. It owns 49% of FFF through stock, and the investment was no longer accounted for under the equity method of accounting from the March quarter (per PINC's Q3 FY'23 10-Q, pp. 33: " Other Income, Net" ;).

I II. Capital Productivity, Return on Owner Capital

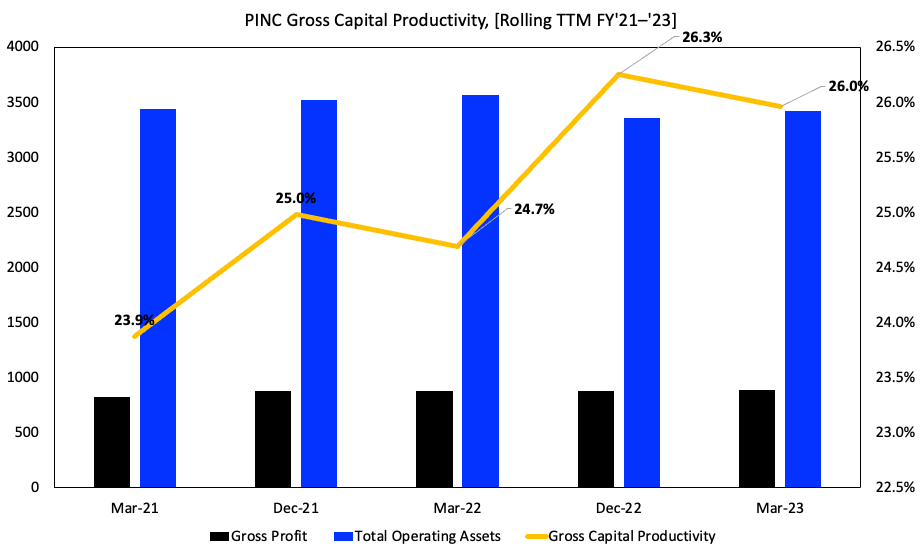

1. Gross Productivity

Despite the top-line troubles you wouldn't notice it at the margin for PINC. Gross margins have crept up from 52% in Q3 FY'21 to 66% in Q3 FY'23 (TTM numbers).

Putting this in terms relevant to investors, the gross profit scaled by the firm's size of operating assets has increased too, from 23% to 26% in the TTM. This is seen in Figure 3, where the rolling TTM gross profit is divided by the total assets each quarter, to show the asset productivity on a rolling basis. This tells me you're getting $0.26 in gross back for every $1 put to work in productive capital, not bad, but could do with improving considering some names are pushing in the 90's at present. The fact it is increasing on a relatively stable asset base is good news too.

Figure 3.

Data: Author, PINC SEC FIlings

{kind=link}

2. Returns on Capital Provided, Capital Invested

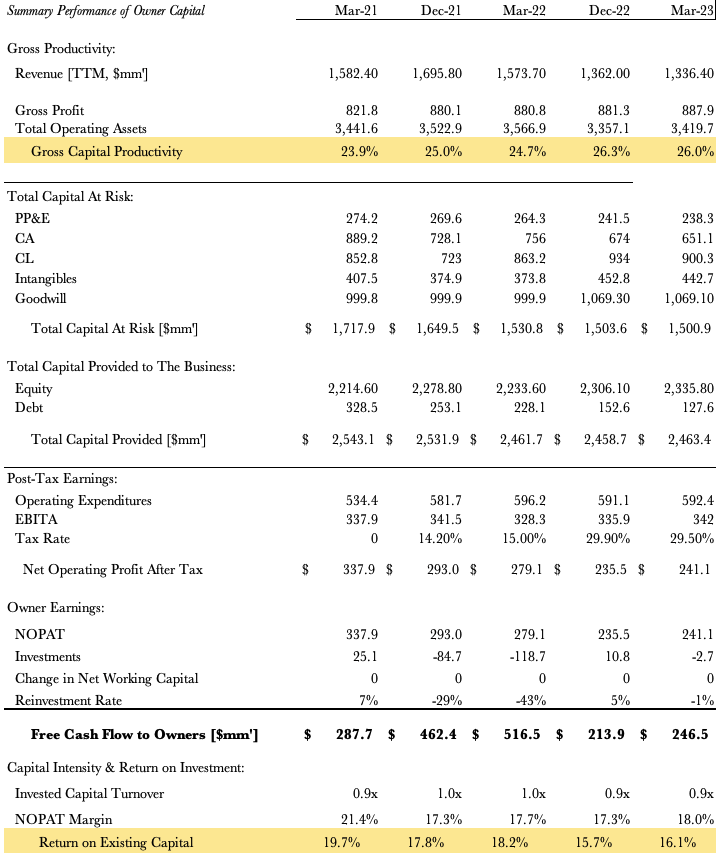

Challenges from the thin gross capital productivity are observed in the translation of gross to post-tax earnings. Figure 4 illustrates a reconciled investor statement summarising the performance of the capital owned by shareholders of the business. As 'owners' of the business' capital, you'd want to see the company producing returns on the money it invests higher than what's available elsewhere.

The total capital provided by investors (equity, debt) is shown, alongside the total capital PINC has invested into productive asset ("Capital At Risk"). You can see the firm hasn't put all the capital provided to work, with ~$900mm in facility remaining at $1.5Bn in capital at risk.

Several findings are gleaned:

- Absent growth in post-tax earnings, reducing from $338mm in 2021 to $241mm last quarter (TTM figures);

- Downsizing incremental investments, ~$200mm in net divestitures across 2021-'23 to date; reinvestment rates negative;

- OpEx increased from $534mm to $592mm with $200mm less capital invested;

- Trailing turnover down ~$246mm over the same time, not the most ideal set of combinations.

The firm is still able to throw off strong amounts of cash flow to shareholders each period, and spun off $246mm in trailing FCF last quarter. However, thinking in first principles, there's headwinds here.

For starters, I'm looking at the earnings, the lack of growth, and the amount of capital consumed in order to get there. There's a tighter capital base for sure, but it is producing 3 percentage points less return on existing capital for 1, and the invested capital turnover at 0.9x tells me the capital intensity is still high anyways.

Figure 4.

Data: Author, PINC SEC FIlings

{kind=link}

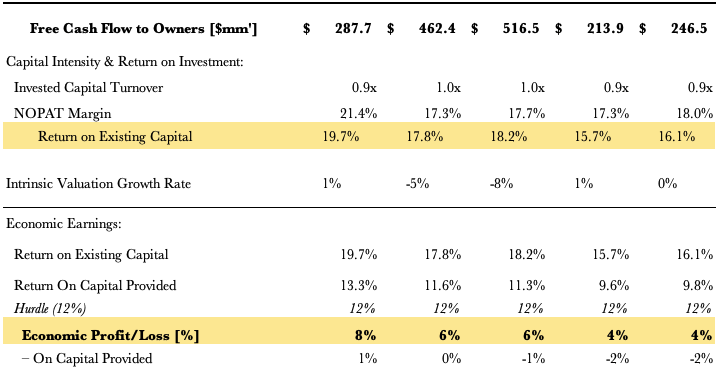

3. Economic Earnings

My regular readers will know I'm always on the hunt for companies that possess exceptional economic characteristics. A thoughtful analysis shows us the value in doing so - if you can get the market return (hurdle rate), you'd want your company to be getting that, or better, in order to allocate more capital (or any in the first place) towards an investment.

A firm that is generating returns on its capital investments above the hurdle rate (in this instance, 12% to reflect the long-term market averages) shows us it can focus on growing without jeopardising value to its shareholders, and vice-versa. Economic earnings, the amount of post-tax profit above the hurdle rate, quantifies this nicely.

Looking at PINC's returns [TTM], you'll note the economic profits have been thin, ranging from 4-8%. The market wants double-digits at minimum in my opinion in order to rate a company higher with more market capitalization. There's really no scope for this to occur otherwise, especially with headwinds on the financial side. Further, with the cost of capital rating higher over time, the market's expectations have moved in tandem with this. Hence, a 12% rate isn't unreasonable, and the firm is resting 4-8 points above this each quarter, not an eye-popping return to attract large investment.

Figure 5.

Data: Author, PINC SEC FIlings

{kind=link}

IV. Valuation

The firm is relatively attractively priced at 17.3x forward earnings, a smirk-inducing 33% discount to the sector. At 11x forward EBIT this is attractive too and could potentially suggest some mispricings. Looking to the current market cap of $3.14Bn, taking a 12% discount rate, it looks as if the market has PINC's future cash flows at $377mm ($377/0.12 = $3,141). At the trailing NOPAT of $241mm, this calls for a 3-year CAGR of 16% over the coming 3-years, getting you to the $3.14Bn range (241x1.16^3)/0.12 = 3,135).

This is certainly feasible and my numbers call for the firm to do ~$240mm in NOPAT this year, with just 250bps of revenue growth [see: Appendix 1]. Hence, this would suggest my numbers align with the market's expectations, indicating there's no mispricing in my opinion.

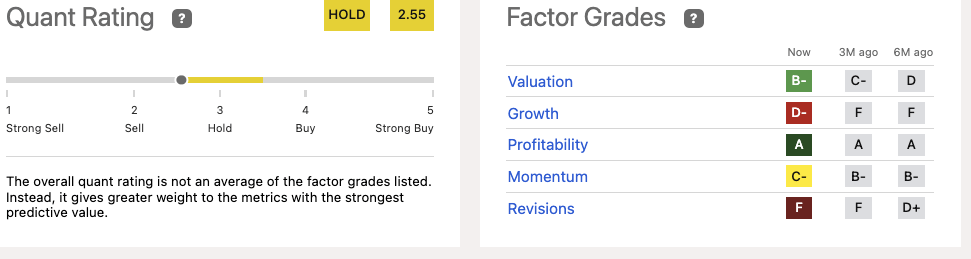

These findings are well supported by quantitative findings illustrated by the quant rating system. The firm is rated lowly on growth and valuation, in tandem with my own findings presented here.

Figure 6.

{kind=link}

In short

Looking to my latest examination findings, it suggests that PINC has a set of clear hurdles to overcome in order to attract a higher market valuation over the coming 12 months. There are good talking points, but management's guidance revisions - times 2 now - combined with the economic findings in its capital allocation strategy suggest a hold is warranted. Further, the quant system backs this up with similar findings to my own, giving confidence to the estimates. Based on the culmination of this data, my opinion on PINC is now a hold, and I am revising my rating on the company down from a buy to reflect this.

Appendix 1. PINC Forward Estimates

{kind=link}

For further details see:

Premier: Second Guidance Downgrade Is Telling