PSX - Prepare To Buy High-Quality Yield With Phillips 66

Summary

- In this article, we discuss a high-yield opportunity in the energy sector.

- Phillips 66 has a high yield, strong and rising free cash flow used to support high dividend growth and a balance sheet that supports aggressive buybacks.

- While PSX shares are attractively valued, the market is pricing in recession risks. I believe the stock can be bought at better prices before growth expectations bottom.

Introduction

It's time we talk about Phillips 66 ( PSX ) . In this case, there are multiple good reasons. The first one is that one of America's largest refiners offers a good yield, backed by a stellar business. Moreover, economic developments could provide buyers with an even bigger yield as demand estimates are likely to come down a bit. Additionally, I discussed its peer Valero Energy ( VLO ) in several articles , which has increased interest in its higher-yielding peer Phillips 66.

In other words, we get to discuss an interesting high-yield play not only capable of paying a juicy yield, but one that is also eager to use buybacks to distribute additional free cash flow. The result is a stellar total return - even for a big mature (and somewhat boring) refinery giant.

FINVIZ

So, let's dive into the benefits of owning a high-yield refinery company!

PSX - A Cyclical Energy Powerhouse

There are many ways to buy high-yield investments. A lot of them are in the energy sector. After all, that sector is extremely mature. Investments in growth capital are low, most businesses are mainly focused on maintenance, and high prices are providing companies with high operating cash flow. It's a perfect recipe for high free cash flow. Companies that have healthy balance sheets can (and often do) decide to let investors benefit from their success. Phillips 66 is one of them.

The company's history goes back to 1927 when the Phillips 66 brand was born. However, the stock price history of the Houston-based company goes back to May 1, 2012, when the company was spun off from ConocoPhillips ( COP ).

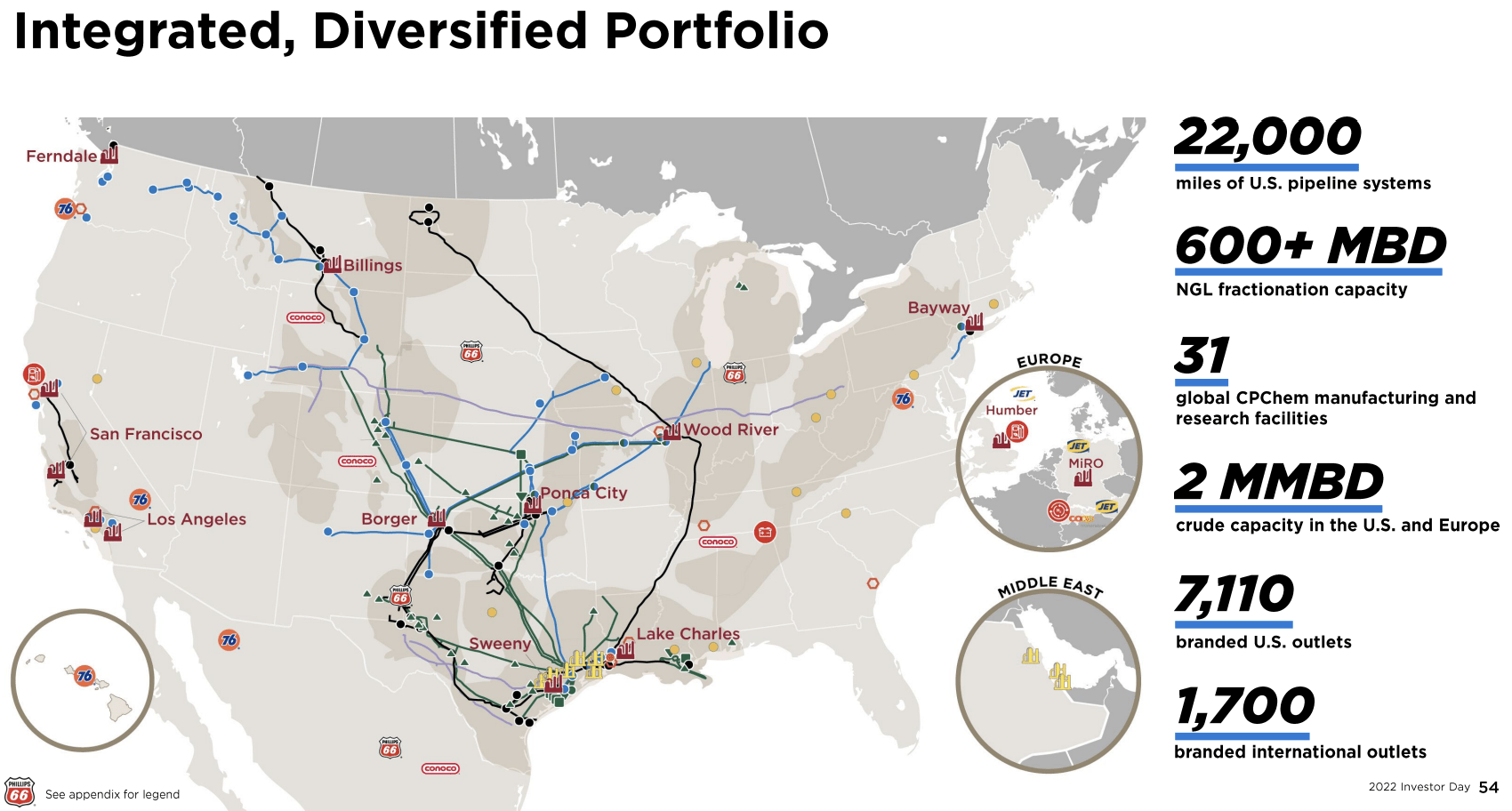

The company has a large integrated portfolio of assets supporting energy transportation, refining, specialty products, and exports. The company has 31 global CPChem manufacturing and research facilities and 12 refineries processing close to 2 million barrels of crude oil per day. Nine of these refinery assets are located in the United States. Most of them are on the Gulf Coast, where refiners have access to reliable feedstock through pipelines and export facilities. Note that CPChem stands for Chevron Phillips Chemical, a 50-50 joint venture between Phillips 66 and energy giant Chevron ( CVX ). CPChem is a major producer of products like ethylene, propylene, benzene, and other products needed in various chemical supply chains. Having spent some time in the chemical industry myself, I can say that these assets are high-value products that are becoming increasingly important as changing energy fundamentals make US producers more important than ever in this space.

{kind=link}

The company also engages in midstream operations through its master limited partnership Phillips 66 Partners LP and its 50% equity investment in DCP Midstream, LLC (to be fully acquired ).

Since 2012, PSX shares have risen 196%. Including dividends, the total return is 320%, which beats the S&P 500's 240% return during this period.

What makes Phillips 66 worth buying is its yield.

The PSX Dividend

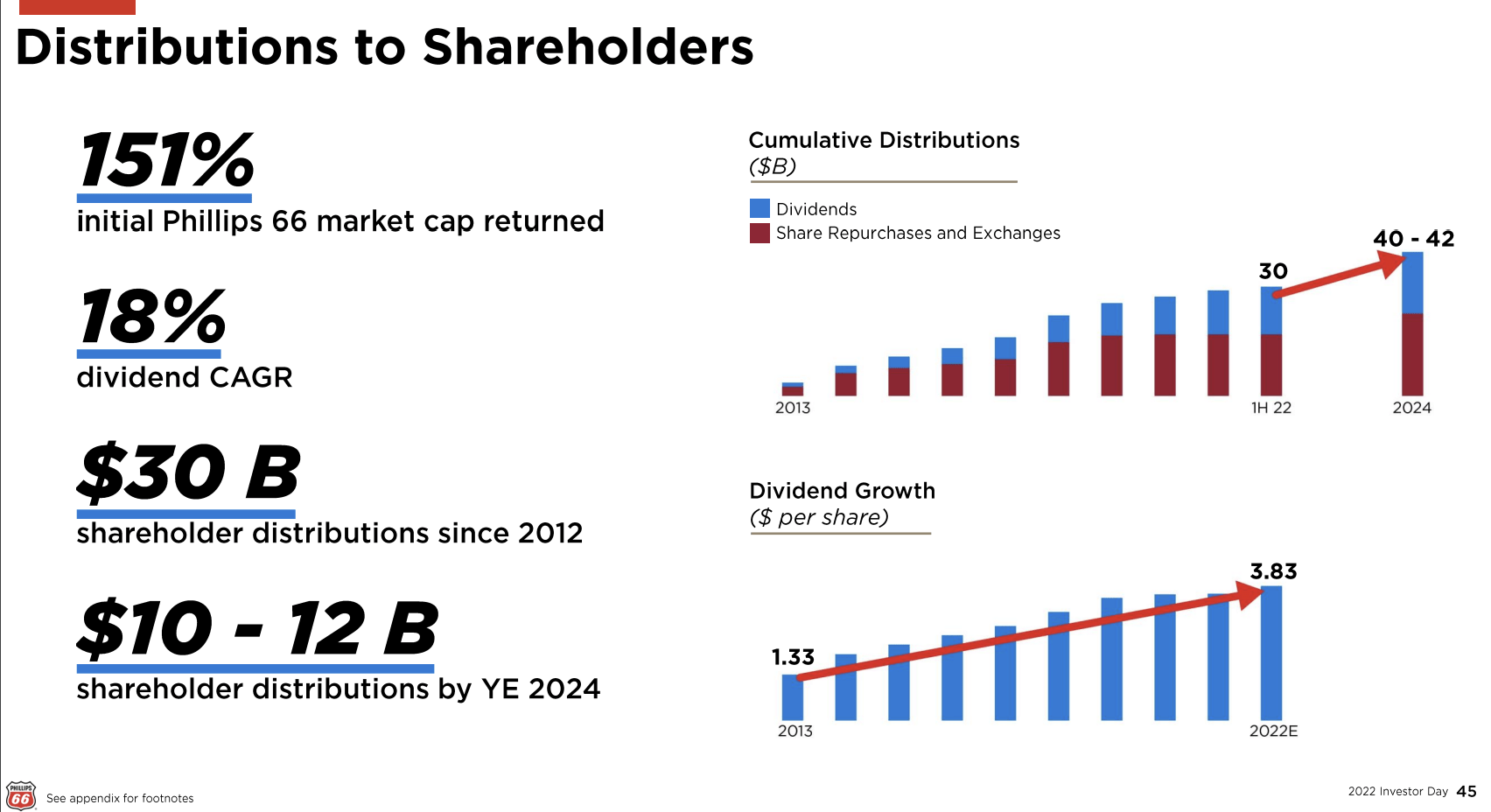

The company is proud of its achievements when it comes to rewarding shareholders - and rightfully so. Since its 2013 spin-off, the company has boosted its dividend by 18% per year, returning $30 billion through dividends and buybacks. It returned more than 150% of its initial market cap, as the company not only aggressively bought back shares but also excelled at timing these repurchases.

{kind=link}

With that said, Phillips 66 currently yields 3.9%. This is based on a $0.97 per share per quarter dividend.

This yield is one of the highest in its short history, excluding the spike during the challenging years of 2020 and 2021.

It is also important to mention that while the company has hiked its dividend by 18% per year since its spin-off, this growth rate has come down significantly. That makes sense as 18% dividend growth is not something a high-yield company can maintain.

These are the latest recent dividend hikes:

- 2Q22: +5.4%

- 4Q21: +2.2%

- 2Q19: +12.5%

- 2Q18: +14.3%

What's interesting is that even in 2018 and 2019, the company was still hiking by double digits. Only the pandemic was able to stop that trend.

However, unlike its peers Valero and Marathon Petroleum ( MPC ), PSX did not stop dividend payments. It also did not cut its dividend.

In 2020, lockdowns caused driven vehicle miles to implode. The same goes for industrial production, which hurt chemical demand. As a result, Phillips 66 did not have enough operating cash flow to service capital expenditure requirements - let alone distribute cash to its owners.

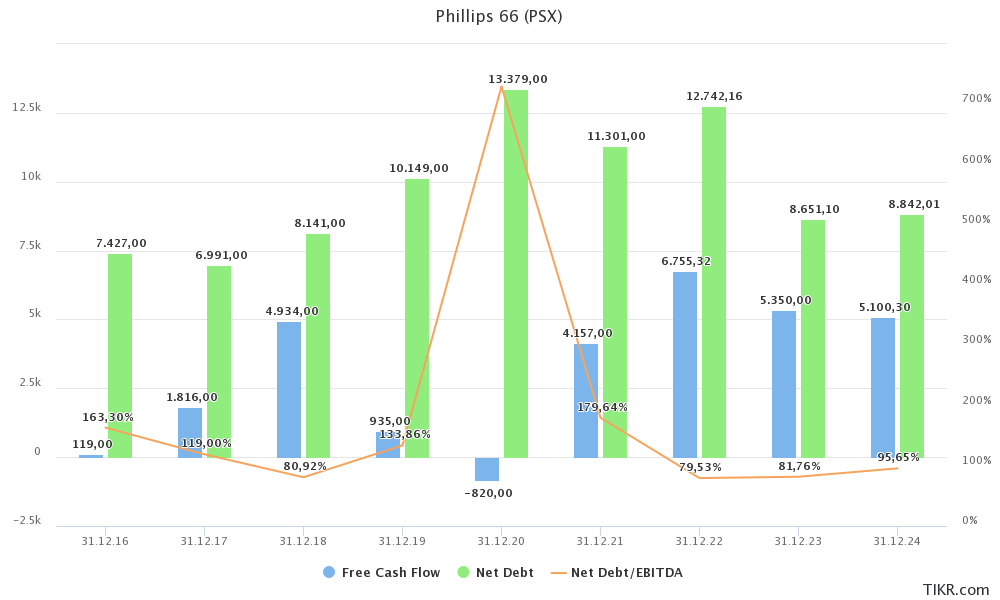

Hence, in 2020, net debt soared to $13.4 billion, which was more than 7x EBITDA back then. However, thanks to the company's balance sheet, it did not have to cut its dividend. Most high-quality energy companies used their balance sheets to protect their dividend. While that is not sustainable on a long-term basis, I agree with that strategy as it uses the benefit of having a healthy balance sheet.

Now, the company is healthy once again. 2022 is expected to see a final net debt number of $12.7 billion, which is 0.8x EBITDA. This year (2023), net debt is expected to fall to $8.7 billion. Its debt is BBB+ rated.

{kind=link}

The chart above also shows free cash flow expectations. Free cash flow is operating cash flow minus capital expenditures. In other words, it's cash a company can spend on distributions after taking care of maintenance and growth CapEx. As Phillips 66 has a healthy balance sheet, nothing is keeping Phillips 66 from spending free cash flow on shareholders.

So, what does this mean? Using current estimates, the company is set to maintain close to $5.2 billion in annual free cash flow. That number can rise much higher in a situation of supply shortages (like we saw in 2022) or lower if economic demand slows. However, for now, I'm using $5.2 billion.

$5.2 billion is 10.9% of the company's $47.6 billion market cap. This implied free cash flow yield suggests that the company is in a good spot to distribute cash worth close to 11% of its market cap on an annual basis. That's a very high number, which leaves room for aggressive dividend growth even in times when debt reduction is prioritized.

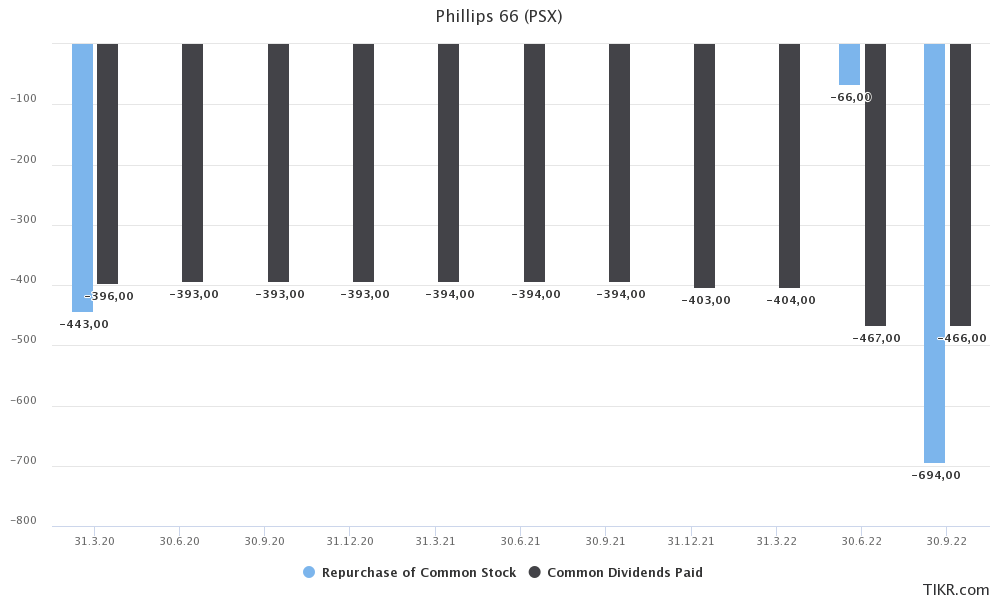

Hence, in 2Q22, the company's gross share repurchases started again. In 3Q22 PSX bought back close to $700 million in shares, which exceeds pre-pandemic buybacks (due to the low payout ratio). The GAAP payout ratio is just 18%, which is 10 points below the sector median.

{kind=link}

The only reason why buybacks in 2Q22 were subdued is the blackout period.

Note that not even the full acquisition of DCP Midstream will change the company's view on shareholder returns.

According to EVP and CFO Kevin Mitchell during the 3Q22 earnings call :

So in terms of the DCP roll-up, our expectation is that will be a combination of debt issuance and cash on hand we'll use to fund that. And to my earlier comments, I feel pretty confident that with where the balance sheet sits with the cash position we have, with the cash generation we have, we'll be able to manage that in terms of -- yes, we will want to subsequently reduce debt. But with the overall cash position, we should be in a position to continue to return significant amounts of cash to shareholders. So I'm not too concerned that the DCP transaction is going to negatively impact our ability to buy back shares.

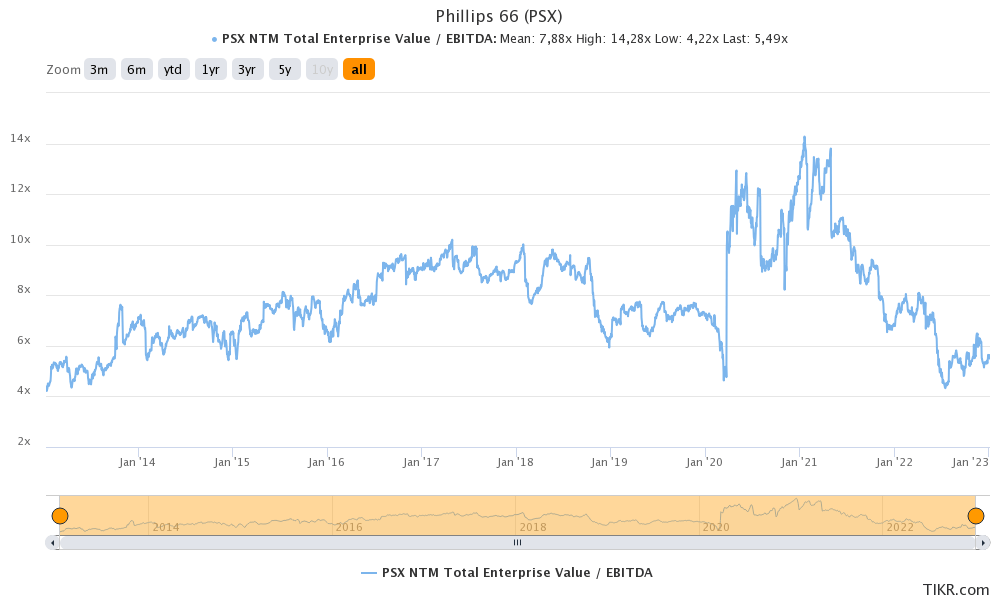

Valuation

Phillips 66 is attractively valued. The company is trading at 5.9x 2023E EBITDA of $10.6 billion. This is based on its $62.4 billion enterprise value, consisting of its $47.6 billion market cap, $8.7 billion in 2023E net debt, $1.0 billion in pension liabilities, and $5.1 billion in minority interest.

{kind=link}

That is a very attractive valuation as the company usually trades close to 7.5x NTM EBITDA. This would imply room to $135 per share (roughly 35% upside).

Unfortunately, instead of rising, the stock price is 11% below its 52-week high as investors are starting to price in a recession.

Leading economic indicators like the ISM index continue to deteriorate, indicating a high likelihood of a manufacturing recession. This happens at a time when the Fed is eagerly fighting inflation. Given persistent (sticky) inflation and strong labor market dynamics, supporting higher wages, it is unlikely that the Fed is easing anytime soon.

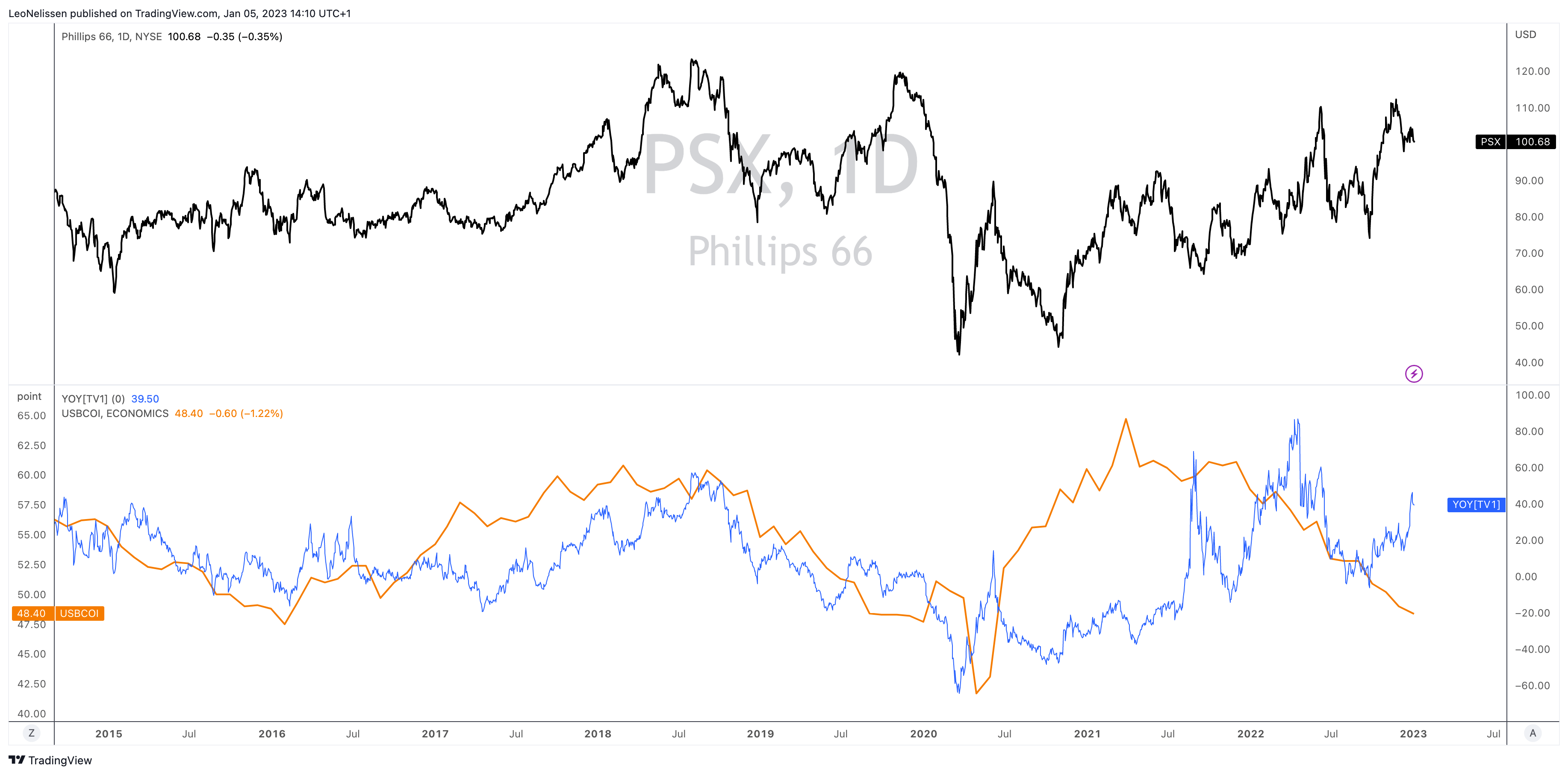

The chart below shows the PSX stock price and a comparison between the year-on-year performance of Phillips 66 and the ISM manufacturing index.

What we see is that the stock is running into resistance as economic growth slows down. If history is any indication, PSX won't gain upside momentum until the ISM index bottoms. I expect that this happens at the end of the first half of this year.

TradingView (PSX, PSX Y/Y vs. ISM Index)

{kind=link}

However, as a dividend investor, this does not worry me. If anything, we can use weakness to add to positions at attractive valuations.

PSX is one of the stocks I think investors will enjoy buying during economic weakness.

Takeaway

In this article, we discussed Phillips 66's dividend growth qualities. The company offers a dividend yield close to 4%, has a healthy balance sheet with a good credit rating, and high free cash flow allowing the company to maintain high long-term dividend growth with excess cash being spent on buybacks.

While I remain bullish on the company's long-term growth outlook, driven by traditional refinery and fast-growing liquidity, we need to take the risks of a recession into account. PSX is attractively valued, yet its stock price has run into resistance.

I believe that interested investors might be able to buy the stock between $80 and $90.

(Dis)agree? Let me know in the comments!

For further details see:

Prepare To Buy High-Quality Yield With Phillips 66