WPC - Preparing And Profiting From Another Real Estate Meltdown

2023-06-05 07:00:00 ET

Summary

- My grandmother often told me about her life as a child and the adversity that her parents faced growing up on a small family farm in rural South Carolina.

- My great grandparents witnessed the crippling of the banking system as panicky depositors withdrew cash, and of course, unemployment soared.

- I can only imagine what life would have been like during the Great Depression, a period in which real estate values were in a tailspin.

My great aunt Maudelle Finley recently passed away at the age of 99. That’s the same age my grandmother passed away a few years ago.

I hope I have the same genes as these wonderful ladies, who weren’t wealthy women, but were quite blessed to have health on their side for almost a full century.

Given the fact that they both lived so long, I’m convinced that they were heavily influenced by the stock market crash of 1929.

My grandmother often told me about her life as a child and the adversity that her parents faced growing up on a small family farm in rural South Carolina.

When I heard about my great aunt’s passing last week, I began to ponder the similarities in time leading up to the Great Depression and today.

As conveyed in Homer Hoyt’s classic One Hundred Years of Land Values in Chicago, leading up the Great Depression (from 1918 to 1926) the Chicago population increased 35% and land values rose 150%, or about 12% a year.

Then in 1926, land values deteriorated, then fell. By 1933, Chicago land values had fallen by around 70% overall; peripheral areas fell even more dramatically.

Remember, my grandmother and great aunt were just kids during the Great Depression, a period when the Fed kept interest rates too high, which strangled the economy.

They both witnessed, even as kids, the impact of the 1929 stock market crash that was triggered by a drastic meltdown in real estate. Their parents (my great grandparents) were farmers and the land they owned became essentially worthless which is how the term “dirt poor” was derived from.

My great grandparents witnessed the crippling of the banking system as panicky depositors withdrew cash, and of course unemployment soared. It was the real estate bubble that Homer Hoyt described that helped set off and then worsen the Great Depression…

…doesn’t this seem familiar?

The Real Estate Crash of 2023

I know my grandmother and great Aunt lived through some very stressful times and I’m so thankful that they were both able to live almost one century. I can only imagine what life would have been like during the Great Depression, a period in which real estate values were in a tailspin…

The same formula they lived thru in 1926 is the same formula today:

Rising rates + high inflation + banking crisis + declining real estate values

That’s right, all four of these in 1929 and we four of them today.

To avoid a bank meltdown like 1929, financial regulators have made some aggressive moves to prevent contagion in the banking system; however, based on our research at iREIT™, we believe that the commercial real estate industry could continue to get worse over the next 12 months and Jamie Dimon agrees,

“…the off-sides (Wall Street jargon for indirect consequence) in this case will probably be real estate. It’ll be certain locations, certain office properties, certain construction loans. It could be very isolated; it won’t be every bank.”

The commercial real estate mortgage market for income-producing properties is roughly $4.5 trillion and around 80% of all bank loans come from regional banks. These “certain” sectors that Dimon is referring to are multifamily loans and office loans that represent over 50% of loans outstanding.

According to the Mortgage Bankers Association around $728 billion (16% of total loans) will mature in 2023, with another $659 billion (15%) maturing in 2024. The banks have pulled back dramatically, and this means that many landlords will have a difficult time refinancing debt maturities.

I was once a real estate developer myself (for over two decades) and I’m glad that I don’t have to worry about refinancing debt in this environment. It’s kind of like an office property “great recession”.

Around $728 billion of loans are set to mature in 2023 and around the same amount in 2024, where will these landlords get money to refinance their properties?

A Safe Way to Own Real Estate

For small to mid-size real estate owners, there will be tough times ahead, especially in the more challenged office and multi-family sectors.

While there are some of the same ingredients as the Great Depression, the banks seem to have it under control (at least for now) and our research suggests that a modest recession is the most likely outcome.

Our team is seeing property REIT valuations decline in the order of 20% to 25% which means there’s an excellent window to own shares in landlords that own some of the most sought-after properties in the world, and without the risk of debt maturities.

Real estate investments trusts (REITs) were created in 1960 for Average Joe and Jane to provide dependable income and my only regret is that I wish my grandmother and aunt Maudelle could have taken advantage of the income that these blue-chip stocks generate.

5 Blue Chip REITs to Sleep Thru The Storm

W. P. Carey ( WPC ) is a diversified net-lease real estate investment trust (“REIT”) that specializes in single-tenant properties. WPC has flexible deal structures and acquires properties through sale-leasebacks, acquisitions of existing net-lease properties, and build-to-suits.

WPC is geographically diversified with properties in North America and Europe and is also diversified by property type. Their portfolio includes 1,446 net-lease properties that encompass approximately 176 million square feet. Additionally they have a portfolio of 84 self-storage properties.

Their net-lease portfolio consists of industrial and warehouse properties, retail properties, office properties, and self-storage properties that are leased on a net-lease basis. As a percentage of their annualized base rent (“ABR”), industrial properties are their largest category contributing 27.3% of their ABR, followed by warehouse properties that contributes 24.2% of their ABR.

Retail makes up 17.4%, office makes up 17.2%, and net-lease self-storage properties make up 4.5% of their ABR. Their net-lease portfolio has a weighted average lease term (“WALT”) of 10.9 years and an occupancy rate of 99.2%. Their self-storage portfolio consists of 84 properties that contain 52,105 units and have an occupancy rate of 91.5%.

{kind=link}

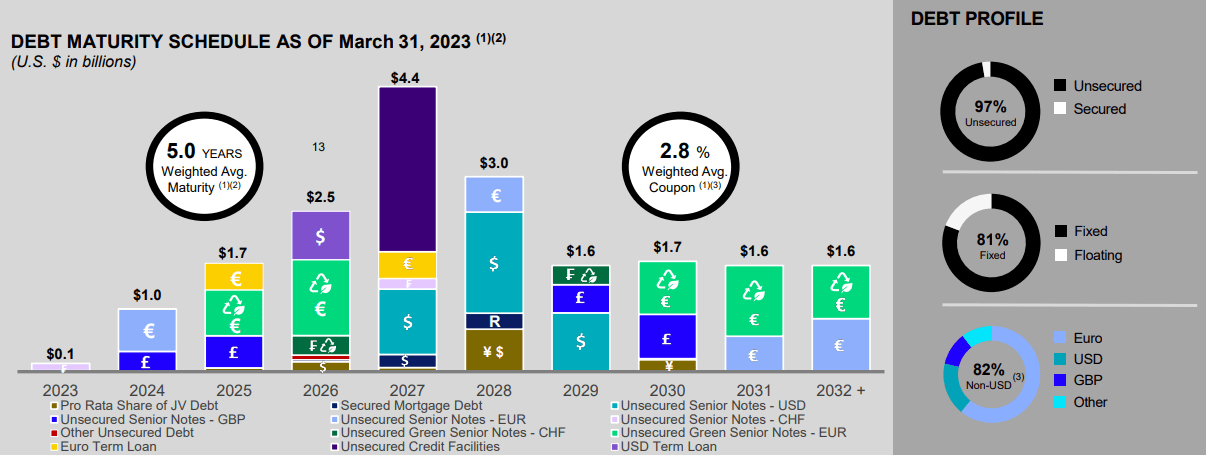

WPC is investment-grade with a BBB+ credit rating from S&P Global and has strong debt metrics including a pro rata net debt to adjusted EBITDA of 5.8x, a consolidated debt to gross assets of 40.3%, and a fixed charge coverage ratio of 5.4x.

Their debt has a pro rata weighted average interest rate of 3.1% and a pro rata weighted average term to maturity of 4.1 years. $306 million or 3.7% of their total debt matures in 2023 and they have $1.7 billion in total liquidity when including $385 million of forward equity.

WPC - IR

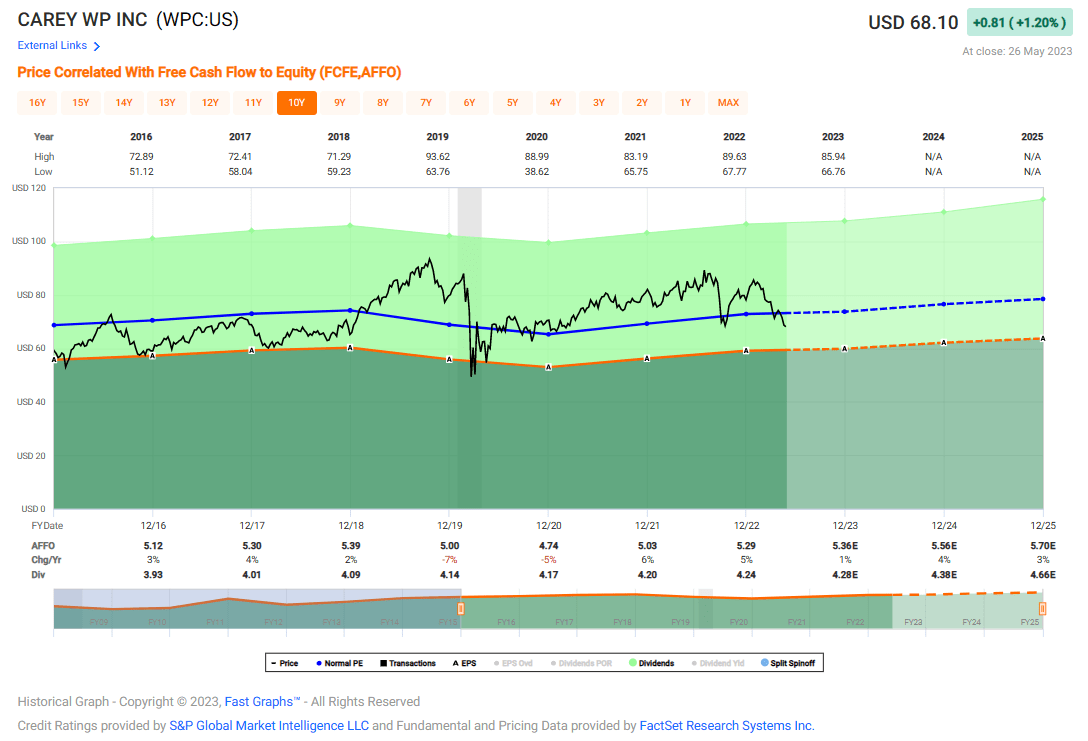

Since 2010, WPC has had an average adjusted funds from operations (“AFFO”) growth rate of 4.22% and an average dividend growth rate of 5.44%.

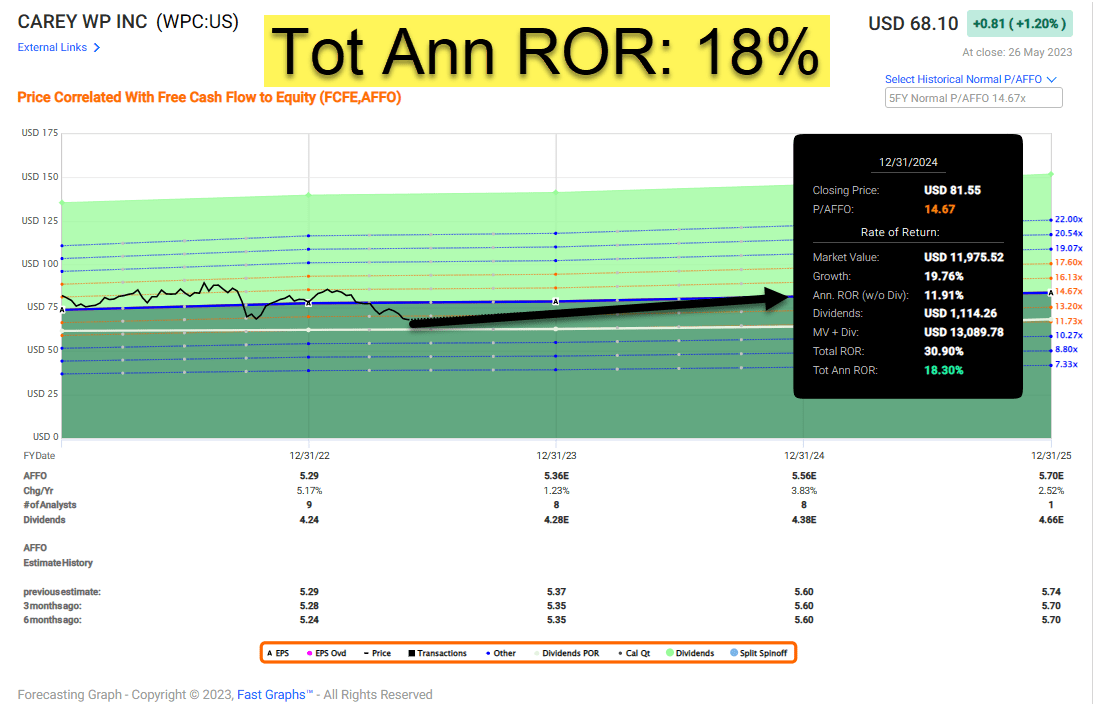

They pay a 6.17% dividend yield that is well covered with an AFFO payout ratio of 80.19% and are currently trading at a P/AFFO of 13.02x which is a discount to their normal AFFO multiple of 14.67x.

{kind=link}

If WPC returns to their normal P/AFFO multiple it would result in a total annual rate of return of 18% by the end of 2024.

At iREIT™ we rate W.P. Carey stock a BUY.

{kind=link}

Digital Realty ( DLR ) is a REIT that specializes in data centers. They have data centers around the globe that serve around 5,000 customers with properties located in the U.S. Latin America, Asia, Australia, Canada, Africa, and Europe.

Their portfolio consists of 314 data centers that cover approximately 38.8 million square feet (excluding development space) and contains 214,000 cross connects. As of the end of the first quarter, Digital Realty had an occupancy rate of 83.7% and a weighted average remaining lease term of 4.8 years.

Data centers store servers and are much more specialized than other types of real estate. They must have heat sensors and cooling systems to keep the servers running smoothly, security systems that include exterior smart fences and cameras and multiple layers of interior access systems.

Additionally, they must be built with the infrastructure in place to pull in large amounts of electricity along with back up sources of power in order to maintain uninterrupted service.

{kind=link}

Digital Realty is investment-grade with a BBB credit rating from S&P Global (negative outlook) and has reasonable debt metrics including a net debt to adjusted EBITDA of 7.1x, a long-term debt to capital ratio of 52.57%, and a fixed charge coverage ratio of 4.4x.

Their debt is 97% unsecured, 81% fixed rate, and has a weighted average term to maturity of 5 years and a weighted average interest rate of 2.8%.

{kind=link}

Digital Realty plans to sell $2 billion in assets to recycle into new development projects (with positive investment spreads). In Q1-23 the company monetized a 10% interest in a data center in Ashburn, Virginia (alongside its VP partner) demonstrating the appetite for well-located data centers and strong valuations.

This asset was sold at a valuation of nearly $17 million per megawatt which represents a substantial premium to development costs today for new data centers in this market and significant value creation. The property was built for 50% of the price around 13 years ago.

Over the past 10 years DLR has had an average AFFO growth rate of 5.74% and a dividend growth rate of 5.29%. They pay a 4.66% dividend yield that is well covered with an AFFO payout ratio of 81.33%.

DLR’s price performance has struggled over the past year and a half but has recently seen meaningful appreciation due to the surge in artificial intelligence (“AI”) and the role data centers will play to support the requirements needed for AI. In the last month alone DLRs stock price has gained 11.24%

{kind=link}

Currently DLR is trading at a P/AFFO of 17.25x which is well below their normal AFFO multiple of 20.61x. If the stock reverts to its normal AFFO multiple it would deliver a total annual rate of return of approximately 20% by the end of 2024.

At iREIT™ we rate Digital Realty stock a STRONG BUY.

{kind=link}

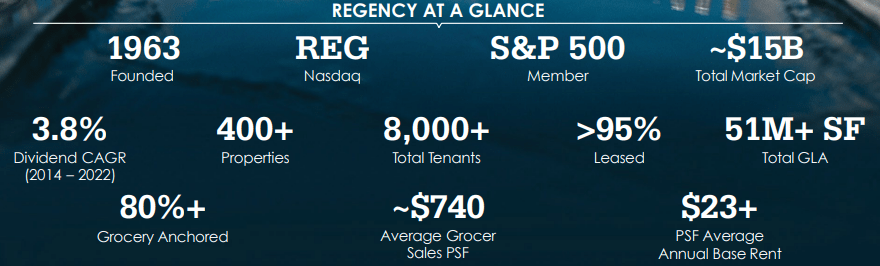

Regency Centers ( REG ) is a REIT that specializes in grocery-anchored shopping centers. Their portfolio consists of more than 400 shopping centers (~ 80% anchored by a grocery store) that cover 51 million gross leasable square feet and serve more than 8,000 tenants with a lease rate of approximately 95%.

Their properties are primarily located in Florida, California, and Texas, as well as having a heavy presence in the Mid-Atlantic and Northeast regions of the country.

Recently REG announced the acquisition of Urstadt Biddle Properties ( UBA ) that is expected to close later this year (late Q3 or early Q4) and is expected to be immediately accretive to their core operating earnings.

Urstadt Biddle owns open-air, grocery-anchored shopping centers that are primarily located in New York, New Jersey, and Connecticut. UBA has 77 properties covering 5.3 million square feet of gross leasable area (“GLA”) and are 94.2% leased.

Once the acquisition has been closed, REGs pro forma portfolio will consist of 481 properties covering 56.4 million square feet of GLA and is estimated to be 95% leased.

{kind=link}

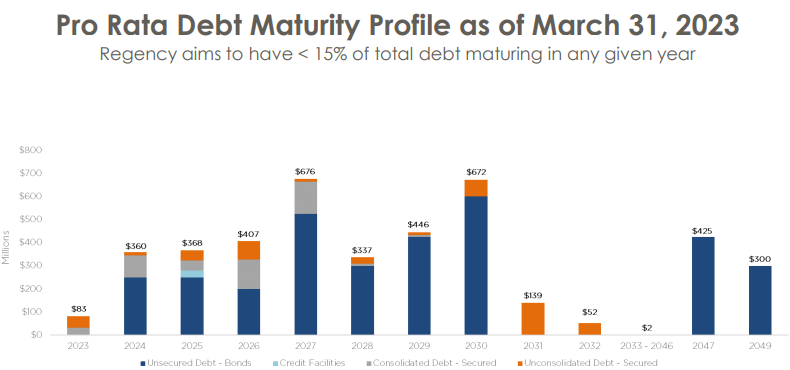

Regency Centers has a BBB+ credit rating and strong debt metrics including a net debt to operating EBITDAre of 4.9x, a long-term debt to capital of 41.15%, and a fixed charge coverage ratio of 4.7x.

Their debt has a weighted average interest rate of 3.9% and a weighted average term to maturity of 8.1 years. Additionally they have minimal maturities in 2023 and have a total of $1.2 billion in liquidity.

{kind=link}

Over the last 10 years REG has delivered an average AFFO growth rate of 6.34% and an average dividend growth rate of 3.18%. They pay a 4.61% dividend yield that is well covered with an AFFO payout ratio of 75.87%.

{kind=link}

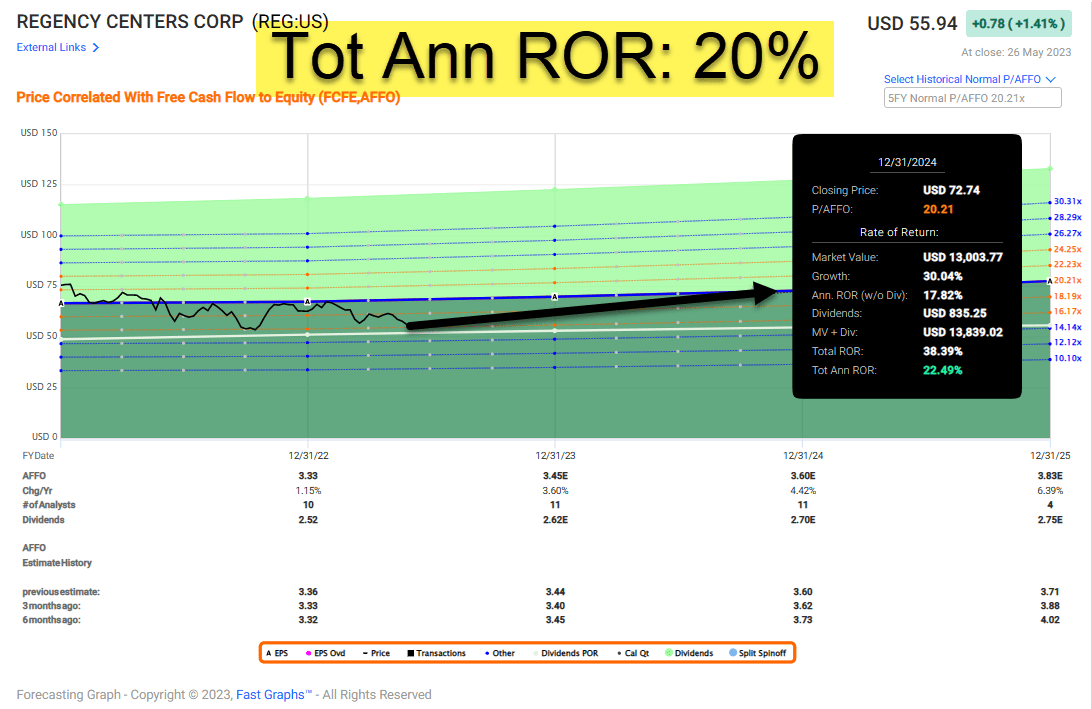

Currently Regency Centers is trading at a P/AFFO of 16.70x which is well below their normal AFFO multiple of 20.21x. If REG can get back to its normal AFFO multiple by the end of 2024 it would translate into a total annual rate of return of approximately 20%.

At iREIT™ we rate Regency Centers stock a BUY.

{kind=link}

Realty Income ( O ) is a REIT that specializes in single tenant, free-standing properties that are leased on a long term, triple net basis. While they primarily own e-commerce resistant retail properties, they also own industrial properties and a gaming property.

In total they own or have an ownership interest in 12,237 properties with an occupancy rate of 99% that covers approximately 236.8 million square feet of leasable space. Their properties serve 1,259 tenants operating in 84 separate industries and have a weighted average remaining lease term of approximately 9.5 years.

Realty Income is one of the few REITs that can claim the title of a Dividend Aristocrat with 29 consecutive years of dividend increases. They pay monthly dividends and typically raise the dividend each quarter. In all they have declared 634 monthly dividends and have delivered 102 consecutive quarterly increases.

{kind=link}

Realty Income has an A- credit rating from S&P Global and a strong balance sheet with a net debt to annualized pro forma adjusted EBITDAre of 5.4x, a long-term debt to capital ratio of 41.21%, and a 4.6x fixed charge coverage ratio.

Their debt is 90% fixed rate, 95% unsecured, and has a weighted average term to maturity of 5.9 years. Realty Income has minimal maturities in 2023 and $3.1 billion in total liquidity as of March 31, 2023. Additionally they have approximately $1.5 billion of unsettled forward equity and $1.0 billion from a bond offering that closed in April.

{kind=link}

Realty Income has had an AFFO growth rate of 6.99% and a dividend growth rate of 5.76% over the past decade. In addition to their solid growth rates, they have been very consistent with 26 out of 27 years of positive AFFO earnings growth. They pay a 5.17% dividend yield that is well covered with an AFFO payout ratio of 75.69% and are currently priced at a discount.

{kind=link}

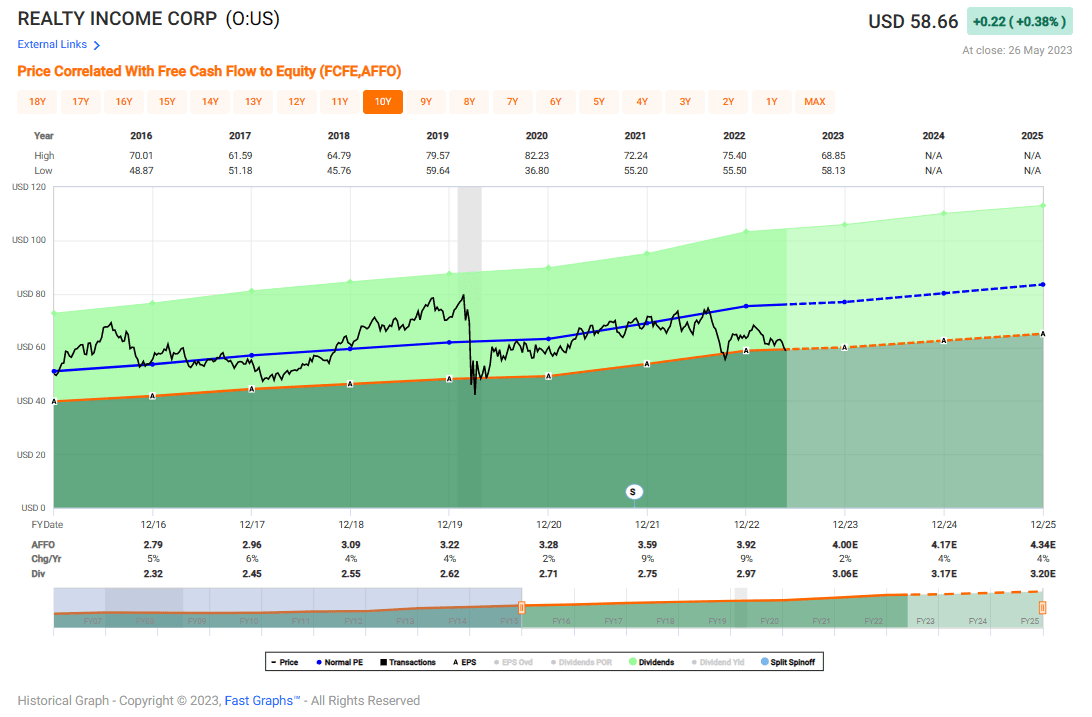

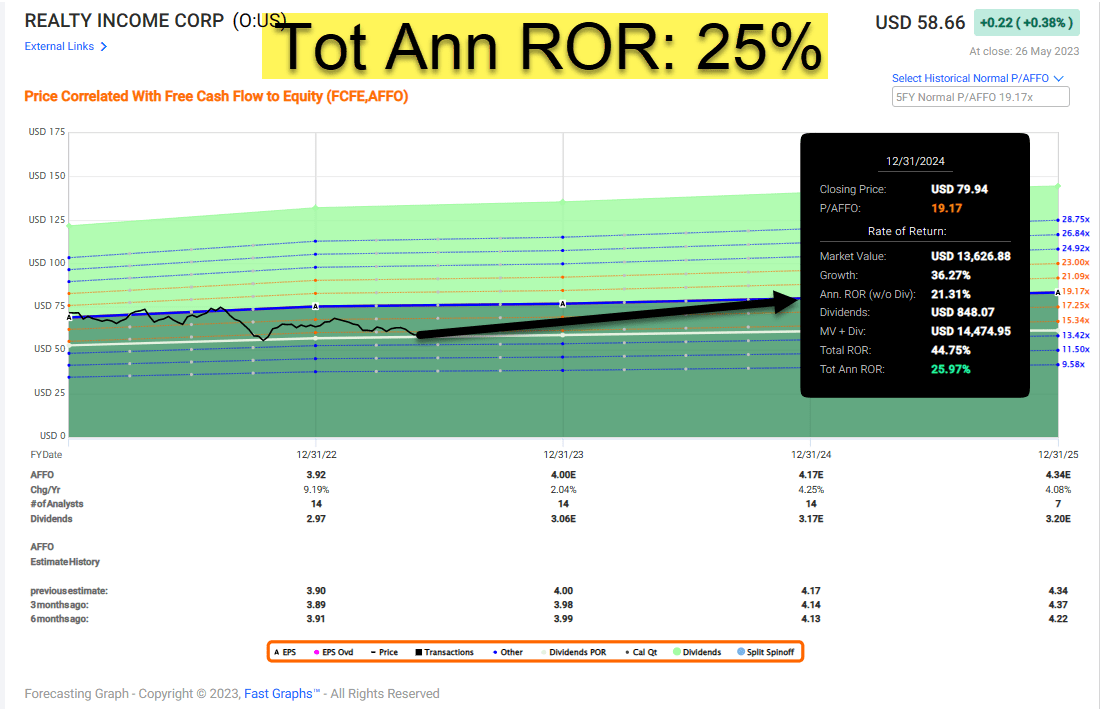

Currently Realty Income trades at a P/AFFO of 14.98x which is a significant discount to their normal AFFO multiple of 19.17x. Investors could expect a total annual rate of return of 25% if Realty Income trades back up to its normal AFFO multiple by the end of 2024.

At iREIT™ we rate Realty Income stock a BUY.

{kind=link}

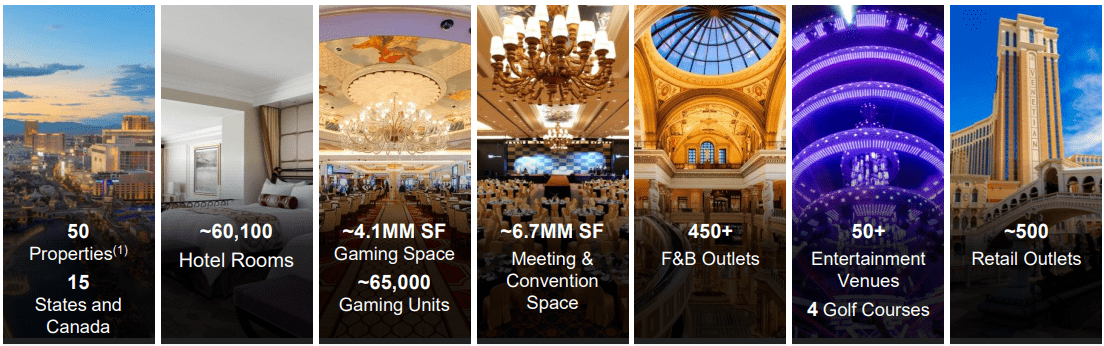

VICI Properties ( VICI ) is a experiential REIT that specializes in casino gaming properties. They own iconic trophy properties including Caesars Palace Las Vegas, Venetian Resort Las Vegas, and the MGM Grand.

Their portfolio consists of 50 gaming facilities in the U.S. and Canada that cover around 124 million square feet and that feature roughly 60,100 hotel rooms, around 500 retail shops, and more than 450 bars, restaurants and nightclubs.

Their properties are operated by leading hospitality and gaming operators and are leased on a triple-net basis. In addition to their gaming facilities VICI owns 4 championship golf courses and 34 acres of land next to the Vegas Strip that can be used for future development.

{kind=link}

VICI was formed in 2018 and has shown exponential growth since that time.

They have been very active in acquisitions with some recent examples including the acquisition of the remaining 49.9% interest in the MGM Grand and Mandalay Bay joint venture that they had with Blackstone Real Estate Income Trust (“BREIT”), the acquisition of 4 gaming properties in Canada through a sale-leaseback transaction with Pure Canadian Gaming, and the acquisition of the Gold Strike Casino that is located in Tunica, Mississippi.

{kind=link}

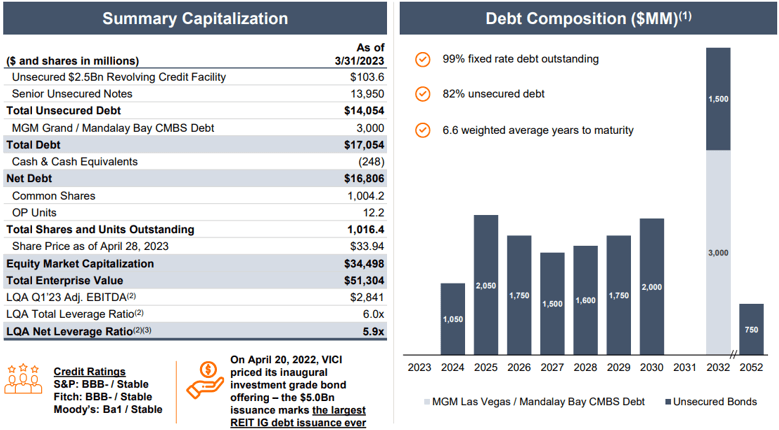

VICI is investment-grade with a credit rating of BBB- from S&P Global and has solid debt metrics including a net leverage ratio of 5.9x, a long-term debt to capital ratio of 42.68%, and an interest coverage ratio of 3.12x.

Their debt is 82% unsecured, 99% fixed rate and has a weighted average term to maturity of 6.6 years. Additionally, no debt maturities occur in 2023 and VICI has $3.6 billion in total liquidity as of the end of the first quarter.

{kind=link}

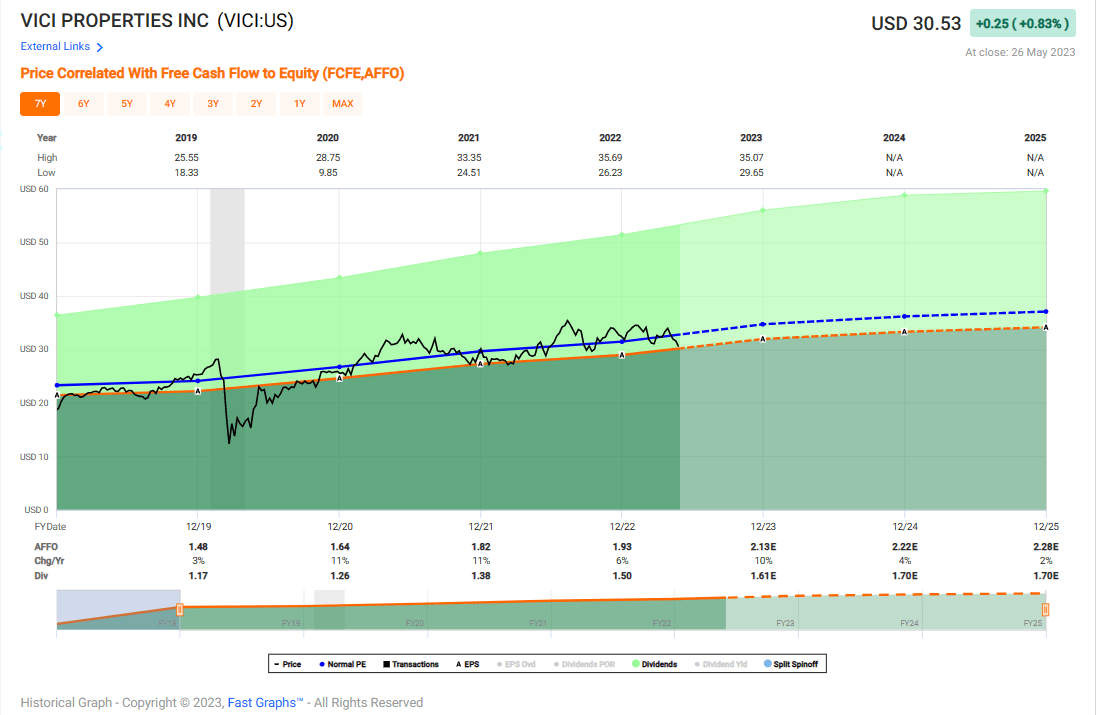

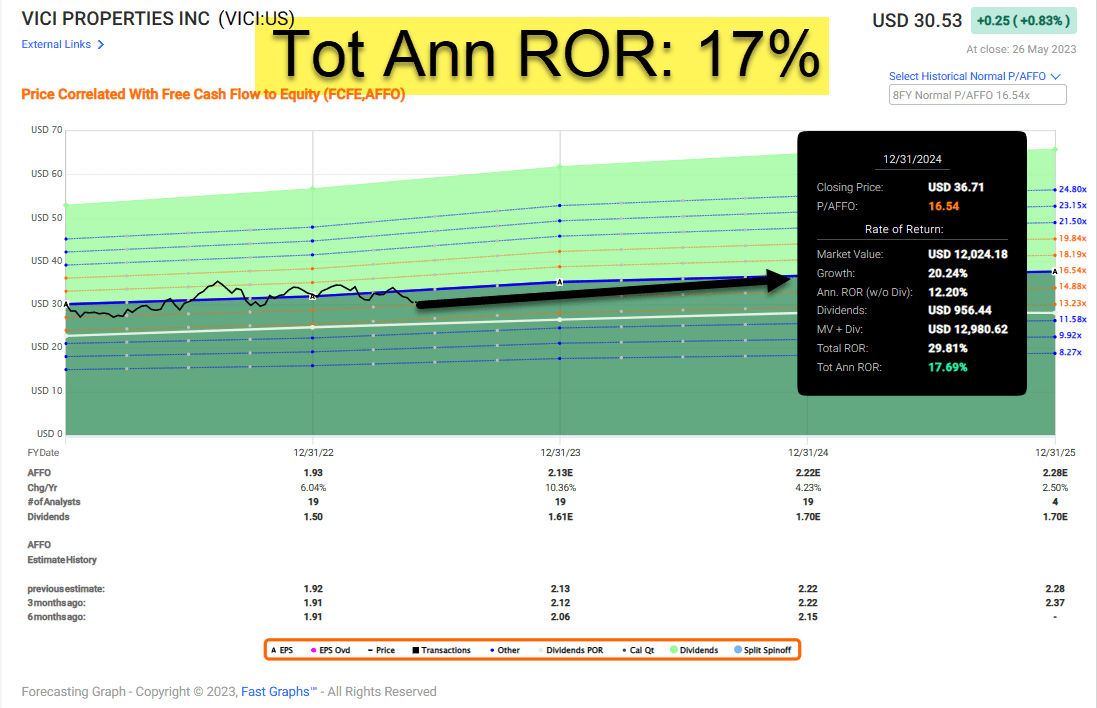

Since 2019 VICI has had an average AFFO growth rate of 7.60% and an average dividend growth rate of 10.80%. They pay a 5.04% dividend yield that is well covered with an AFFO payout ratio of 77.72%. Additionally VICI is trading at a slight discount to their normal valuation.

{kind=link}

VICI is currently trading at a P/AFFO of 15.37x which compares favorably to their normal AFFO multiple of 16.54x. If VICI trades back up to its normal AFFO multiple it would result in a 17% total annual rate of return by the end of 2024.

At iREIT™ we rate VICI stock a BUY.

{kind=link}

In Summary…

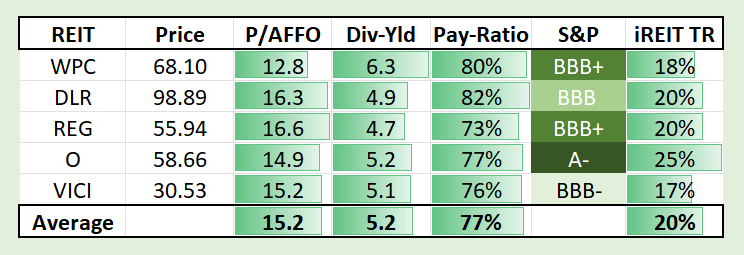

As viewed below, we consider all five of these blue-chip REITs to be solid picks right now. The average dividend yield of these five REITs is 5.2% (payout ratio of 77%) and the average total return forecast (by iREIT™) is 20% annually.

{kind=link}

All five REITs are included in our iREIT™ 100 High Quality Equity REIT Index and are also constituents in the iREIT-MarketVector ™ Quality REIT Index .

We recommend owning a core position in these high-quality REITs that are screened regularly based on quality and value at iREIT™ on Alpha.

Given my grandmother and great aunt's extreme conservatism, I'm sure they would agree with these recommendations, especially at this stage in the cycle.

“The years of poverty since Father’s death had touched me only lightly. They had developed in my character a serious concern for money , a willingness to work hard for small sums, and an extreme conservatism in all my spending habits .” Ben Graham

As always, thank you for the opportunity to be of service.

Author's note : Brad Thomas is a Wall Street writer, which means he's not always right with his predictions or recommendations. Since that also applies to his grammar, please excuse any typos you may find. Also, this article is free: Written and distributed only to assist in research while providing a forum for second-level thinking. for reading and commenting and I look forward to your comments below.

For further details see:

Preparing And Profiting From Another Real Estate Meltdown