EB - Price Hikes Should Power Eventbrite

Summary

- EB recently raised prices for the first time.

- The return of corporate events bodes well for company.

- Higher interest rates are a potential positive.

Editor's note: Seeking Alpha is proud to welcome Geoffrey Seiler as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Self-service ticketing platform Eventbrite ( EB ) has several catalysts that should help the stock outperform in 2023. The most important is a recent price hike that is not currently accounted for in analyst estimates. The company should also benefit from a return of corporate events, the continued shift of spending habits toward experiences, higher ticket prices, and higher interest rates given its large cash position.

Company Overview

EB's ticketing platform focuses on mid-market experiences that fall somewhere between small gatherings and stadium events. Its platform allows hosts to create and sell tickets to live experiences. This could be anything from music to sports, food and drink events, business gatherings, performing arts, education, or religious outings, among others. The company lets creators of free events use its platform for free, while it charges creators of paid events a per-ticket fee based on tickets sold.

In 2020, EB introduced Eventbrite Boost, a marketing and engagement tool for users. This gives creators one integrated tool for ticketing, analytics, social media ads, and email marketing.

Historically, the company derived approximately half its revenue from creators who signed themselves up to use its platform and approximately half from creators acquired through sales channels, many of whom expect significant customer support. However, due to the pandemic, the company has heavily shifted more toward self-service; last year it began implementing support service in India.

Frequent creators are its most important customer base. These creators host more than three events per quarter, represent a third of its paid customer base, and account for ~65% of paid ticket volumes. The U.S. represents about 69% of paid tickets, the U.K. 14%, Australia 7%, and the rest of the world 10%.

Opportunities

EB is still in the early innings of growth, and earlier this year it raised prices for the first time in its history. Previously, the company offered three paid plans. Its Essentials package charged 2% + 79 cents per ticker, while its Professional Package charged 3.5% + $1.59 per ticket, and allowed for different ticket types and for users to sell on their own websites, along with other perks. It also had a Premium tier with custom pricing. All the plans had a 2.5% processing fee.

Starting this year, EB eliminated its Essential package in the U.S. and in some other English-speaking countries and began charging 3.7% + $1.79 service fee per ticket, along with a 2.9% payment processing fee. Given that the company charges a percentage of the ticket price, higher ticket prices should also be a tailwind.

The company also has opportunities on the promotions side of the business with products like Boost and Eventbrite Ads. The ad budgets for events are much greater than the budgets for ticketing, and the cost of these products as part of overall ad budgets is small.

With Boost, EB helps creators manage their ad campaigns and tie them directly to the ticketing process. EB not only gets the benefits from the subscription sale to Boost, but it also helps sell more tickets. Meanwhile, about 25% of the tickets EB sells usually comes directly from its own website. With Eventbrite Ads, it can now get paid to promote local events from its own website. These products also help it monetize free events that need some marketing behind them.

And, of course, a one-stop product suite for ticketing and marketing can also drive more creators to the platform, which the company has been seeing. Management is focusing its investment dollars on improving the platform's ease of use along with functions to help drive ticket sales. On this front, the company recently hired Ted Dworkin to be its new chief product officer. Dworkin has experience in product management and development at Sonos ( SONO ) and Microsoft ( MSFT ).

During the pandemic, EB also instituted a much leaner structure with a focus on self-service. This can be seen in its sales and marketing costs going from $102.9 million in 2019 to only $35.9 million in 2021. S&M is on track to be about $56 million in 2022, so, while up, it is still much lower than pre-pandemic levels. It has recently funneled some of those savings into R&D.

It's also worth noting that EB's revenue is still a bit below the pre-pandemic revenue of $326.8 million it recorded in 2019. Part of that can be attributed to its second-largest ticketing category: business and professional. Thus, another potential opportunity for EB is the return of corporate events, which has been one area that has lagged coming back from the pandemic.

However, both airlines and rental car companies have noted that momentum is starting to return for corporate travel, events, and trade shows. Meanwhile, a report from In-House Corporate Events ((ICE)) in October projected that event spending within the corporate sector would increase 83% in 2023, although some of that was due to inflation. Meanwhile, Amex GBT's Global Meetings & Events Forecast said that two-thirds of respondents thought that the number of in-person events will return to pre-pandemic levels within one to two years . This could be a nice boost for EB.

Higher interest rates could also potentially be an opportunity for EB. Given that the company has a high float business through carrying creator money, it could presumably benefit from higher interest rates on this cash it holds. Currently it doesn't invest it, but the cash is unrestricted, so it could. A 4% interest rate on its over $650 million in cash on the balance sheet could add over 25 cents in EPS.

Risks

The pandemic saw most events canceled and was a major blow to EB; a similar outbreak that causes lockdown restrictions and events to be cancelled would be a huge risk. More pertinent might be how a weakening economy or recession would have an impact on the number of local events, prices, and attendance.

While EB operates in a pretty niche market, there are a lot of ticket companies out there. Ticketmaster, owned by LiveNation ( LYV ), controls the large event market, and likely wouldn't move downstream. However, there are other well-known players like SeatGeek, VividSeats ( SEAT ), StubHub ( EBAY ), and even Spotify ( SPOT ) in the primary and secondary ticketing markets that could move downstream. There are also a lot of a lot of smaller ticketing and event management firms trying to compete with EB on things like price and functionality. However, the company does seem to have a pretty strong market share in this space from the various sources I've seen, which usually pegs its market share around the 40% range.

Eventbrite Market Share (Slintel)

Dilution is another potential risk. The company has 8.5 million non-option restricted stock awards, which is about 8.6% of the shares outstanding. Its vested options are all currently underwater, but there are nearly 9 million with an average strike price of $11.79.

Valuation

{kind=link}

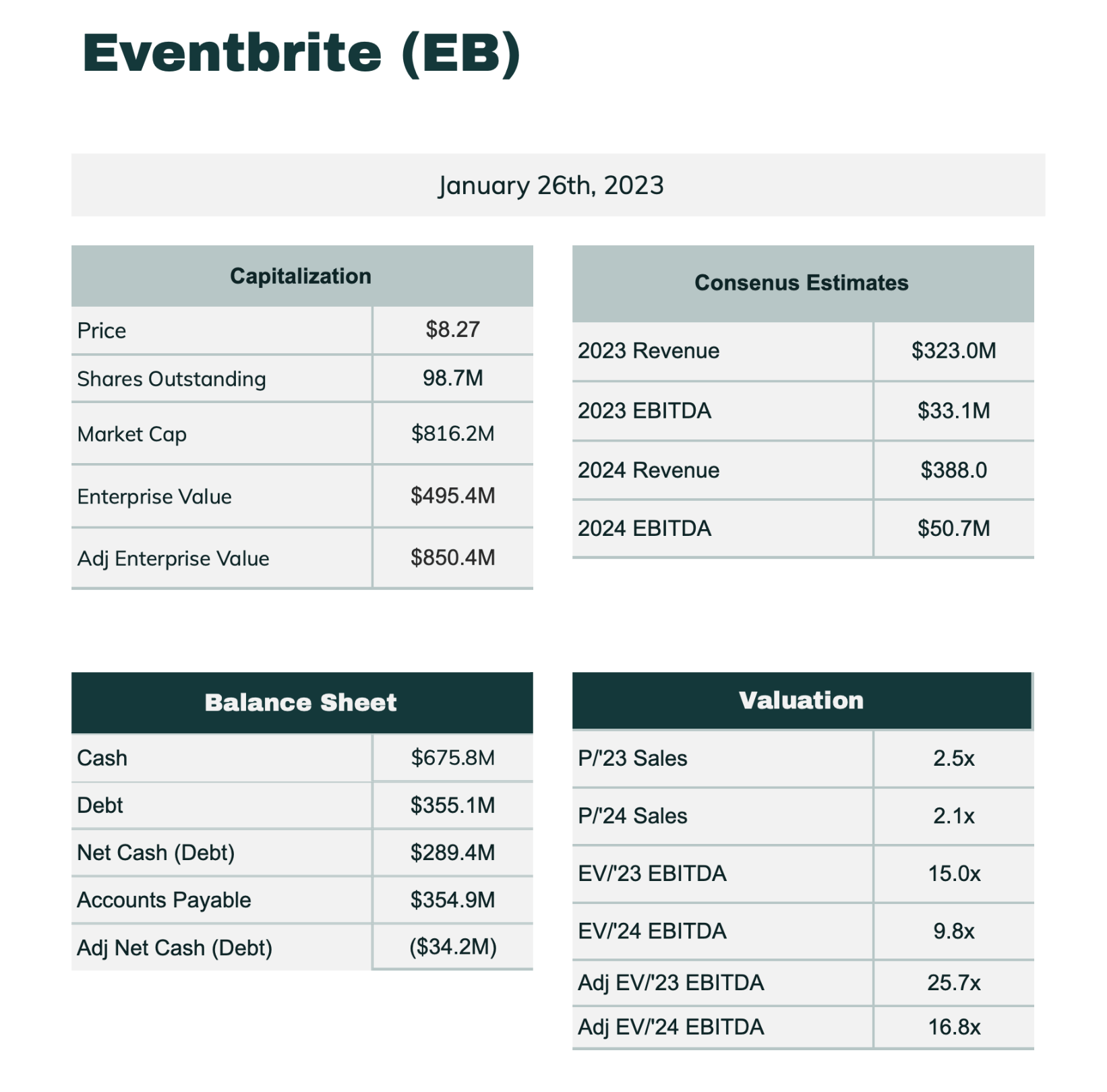

EB trades at about 15x the 2023 EBITDA consensus of $33.1 million, and 9.8x the 2024 consensus of $50.7 million. However, because of the large amount of accounts payable it holds for creators, I think its enterprise value is a bit deceiving. If you pay off those accounts payable, it trades closer to 25.7x and 16.8x 2023 and 2024 EBITDA, respectively.

On a revenue basis, the stock trades at a price to 2023 sales ratio of 2.5x based on consensus revenue of $323.0 million, and a 2.1x multiple on forecast 2024 revenue of $388.0 million. Its revenue is projected to grow 24% in 2023 and over 20% in 2024. Given that the company is still in the early innings of growth and because of its strong gross margins (~65%), I think a P/S is the best way to value the company at present.

Conclusion

EB was a hot IPO back in 2018, closing its first day of trading up nearly 60% at $36.50. Today, it's a broken stock whose business came out of the pandemic with a leaner cost structure and a management team more focused on product innovation and catering to its best revenue-generating customers. The company has yet to return to pre-pandemic revenue numbers largely due to the slow recovery of its second-largest category, corporate/business events. However, there are some signs that this category is finally set to awaken from its COVID-19 cocoon.

The combination of adding users (creators), providing marketing functionality, increased pricing, and higher ticket prices should bode well for solid future growth. Notably, EB raised prices without notice to the investment community, so the price hike is not currently accounted for in the 2023 or 2024 numbers. Thus, EB could be set up to issue strong 2023 guidance.

In all, EB looks like a better company than it was before the pandemic, trading at a third of the price. Meanwhile, it's a pretty high gross margin business (~65%) with moderate S&M spend (~20% of revenue), and nice revenue growth (over 20% projected) trading at around 2x sales.

While a higher risk/reward stock, EB could have upside to ~$14 based on boosted revenue projections and a higher P/S multiple.

For further details see:

Price Hikes Should Power Eventbrite