DBO - Prices For Undercapitalized Crude Oil Limps Along

2023-07-18 20:54:58 ET

Summary

- Crude oil prices remain low despite lack of significant investment expectations.

- Some maintain optimistic outlooks based on investment or its absence.

- Others argue that new technology has altered the necessary investment landscape.

- Inventories continue to fall, leaving a bullish stance.

Crude oil pricing ( CL1:COM ) remains subdued even without significant expectations for investment. Several analysts continue bullish stances based on investment or lack thereof, while at least one claims that technology lowered the investment requirement. The plurality of thought is just that, plurality. Pick a side, find support, and argue the case. In the meantime, oil continues its almost aimless listing in the waters of uncertainty. Like a frustrated, tired employee or athlete dragging crutches associated with the broken extremity from the last competition, crude prices list, sometimes heavier on the downside and sometimes vice versa. Shall we weigh the two in balance? Head with us from the workstation to the scales.

The Bear's Growl

It seems apparent that the bears offer two distinctive growls. The first pitch argues that recent levels of investment are more than adequate. Rystad Energy analysts boldly claimed :

- " [E]fficiency gains, productivity gains, and evolving portfolio strategies . . . significantly increased the upstream['s] efficiency."

- "Cost savings mean operators can produce the same amount of oil at a lower cost, . . .."

With a chart showing world investment levels over the past several years, even with investment down 40% in 2022 over the 2014 peak, Rystad continues arguing enough is enough showing this graph of production vs. produced resources.

Oil Price

The thrust of the argument claims the number of producing resources continues to maintain the production without prior higher investment costs.

The second growl comes from arguing recessions coupled with inventory increases. From U.S. Economy Teetering On The Brink Of A Recession (early May of 2023),

"The analysts estimate that current oil inventories are 200 million barrels higher than at the start of 2022 and a good 268 million barrels higher than the June 2022 minimum."

Continuing from the same article, “ When the world goes into recession and the demand for commodities goes down, the [oil futures] market is unforgiving ,” oil analyst Andy Lipow has told CNN. " We aren't so sure about the validity of the comment outside of a steep economic downturn.

The Bull's Snort

The bulls actually snort a much stronger case. Our discussion begins with comments from David Messier of OilPrice in his U.S. Shale Production Is Set For A Rapid Decline note several weeks ago. His meticulous, detailed approach argues for a steep decline in shale production from failures to invest in new wells. In essence, shale production is living off of untapped yet predrilled wells from the past few years.

Secondly, an additional source adding to weak pricing, comes from inordinate dumping of long contracts .

"The actual influence of soaring funding costs on the oil market is that traders are destocking and selling off physical barrels because the costs to hold crude, and the penalty for keep holding that crude if demand tumbles in a deep recession, have spiked."

This is about to end, leaving traders without adequate levels of buffering.

A third factor, economic growth in certain parts of the world, in particular China, continues to drive excess inventories lower. Many expect excess inventories to disappear by year's end.

A fourth bullish snort loudly fills the air with production risks noted by Irina Slav.

- Supply disruptions in Libya, Saudi Arabia’s production cut, and signs of lower Russian oil exports all gave oil prices a boost this week.

A fifth, Saudi Arabia and a few other counties, now hold the swing card. In the case of the Saudis, oil pricing for its governmental operational needs is approximately $82 or higher. Arabia announced cuts of 1 million barrels per day a month or so ago in order to strengthen pricing. In tight markets, this could be enough to significantly increase prices.

All of these bullish snorts point at continued price increases.

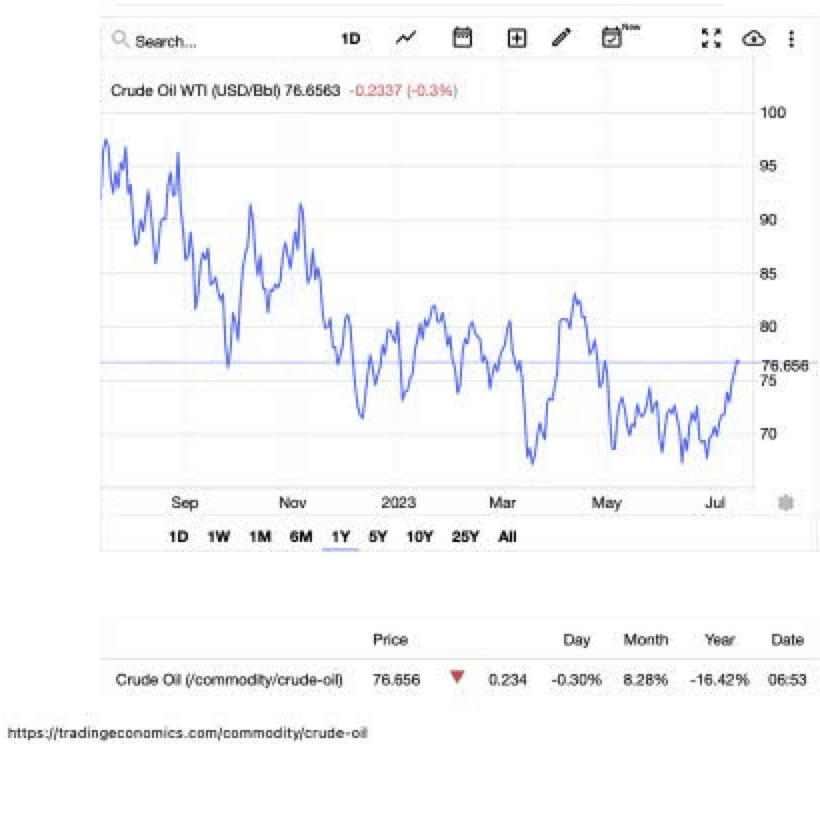

The Listing Ship

Even with the bullish slanting factors, the ship continues to list oscillating from side to side frustrating investors almost to tears.

{kind=link}

Trading Economics

Where Is That Pesky Leak?

So is there a recession? The answer, yes and actually a quite steep one in parts of the market. Beginning with the larger part of the economy, consumer spending, corrected for inflation, has fallen every quarter for the past several. Continuing, from Reuters,

"Historically, GDP has grown in tandem with manufacturing activity and diesel consumption as more goods orders increase the need for freight transport, the main driver of diesel demand. . . Historically, GDP has grown in tandem with manufacturing activity and diesel consumption as more goods orders increase the need for freight transport, the main driver of diesel demand."

Diesel demand is truly in recession, which holds the price of crude in check. The PMI also reflects the marketplace being near 46 or under 50 in contraction. The real argument must focus for how long. The EIA claims though next year, which isn't normal.

Inventories

When trying to understand real market status, looking at changes in inventory is always a necessity. A table shows major inflection points over the past several months using EIA weekly data .

| Crude (thousands) |

| Storage |

| June 2020 |

| 1200000 |

| December 2022 |

| 793000 |

| February 14, 2023 |

| 852000 |

| June 30, 2023 |

| 799000 |

| July 7,2023 |

| 805000 |

From the table, crude storage dropped to a low of 793000 in December of last year, climbed 60 million barrels into February with a drop back to the December low during the last week of June. We understand that usage has a cyclical component, but clearly usage is out stripping production. Watching this change through the next some weeks seems critical. Should the downward trend continue with a break to a new storage low, this bodes extremely positive for longer-term price support.

It's Heading Higher for Now; Maybe for Good, But with a Level of Risk

In the past few weeks, crude prices rose dramatically shown above in the chart. Several factors are driving the direction noted above also, i.e. production coming off line and demand continuing strong. The marketplace may have seen the lows in the past month or two. Risks on a steeper recession remain leaving markets venerable to the downside, but strong upward pressure continues. What is certain is that the depletion in long contracts adds a significant level of volatility. Going forward, expect stronger movements upward and downward. They are coming. In our view, crude oil pricing limps along with a bullish stance. It might last for more than a few months. We remain cautiously bullish. A final note: Crude production in the U.S., looking at data from the same EIA report, shows that it's stunted.

For further details see:

Prices For Undercapitalized Crude Oil Limps Along