PRIM - Primoris Services Corporation: Growth Value And Momentum

2023-09-06 05:17:56 ET

Summary

- Primoris' revenue and operating income (LTM) are both at record highs since 2014. Its backlog recently hit a new record as well.

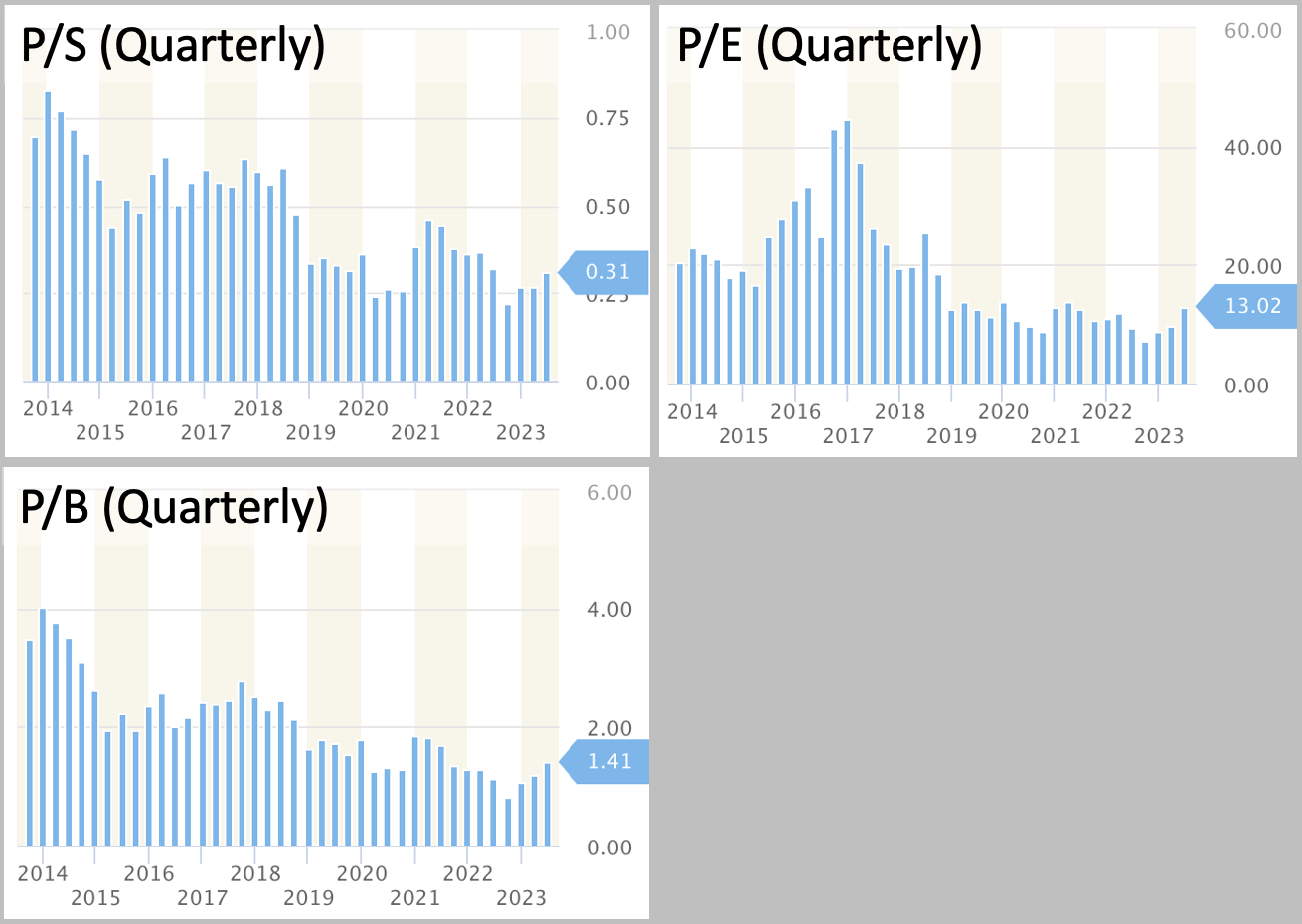

- Its P/S, P/E, and P/B (quarterly) valuation multiples are all near record lows since 2014. The firm’s P/S ratio is below 1, standing at 0.31.

- The energy segment achieved a strong book-to-bill ratio of 2.3 and saw its booking exceed $1.8b.

- Despite risks including customer concentration, variable-rate debt, and natural disasters, PRIM's impressive growth, depressed valuation multiples, and strong momentum present an interesting opportunity.

About

Primoris Services Corporation ( PRIM ) offers a broad mix of engineering and construction services to customers in the US and Canada. As its FY2022 10-K explains:

The Utilities segment operates throughout the United States… including the installation and maintenance of new and existing natural gas and electric utility distribution and transmission systems, and communications systems. Energy/Renewables segment operates throughout the United States and Canada… include engineering, procurement, construction, retrofits, highway and bridge construction, demolition, site work, soil stabilization… The Pipeline segment operates throughout the United States… including pipeline construction and maintenance, carbon capture and storage services, pipeline facility and integrity services, installation of compressor and pump stations…

Note that in 2023, the company reports just two segments: Utilities and Energy, which now includes operations that used to fall into the Pipeline segment.

In FY2022, ~45% of revenues came from multi-year contracts called Master Services Agreements (MSAs). The firm's customers typically include a mix of energy and utility companies (e.g. Xcel Energy (XEL), Chevron (CVX), and Exxon Mobil (XOM)) and state agencies, such as the Department of Transportation of Texas and Louisiana.

Strong Financials & Reasonable Multiples

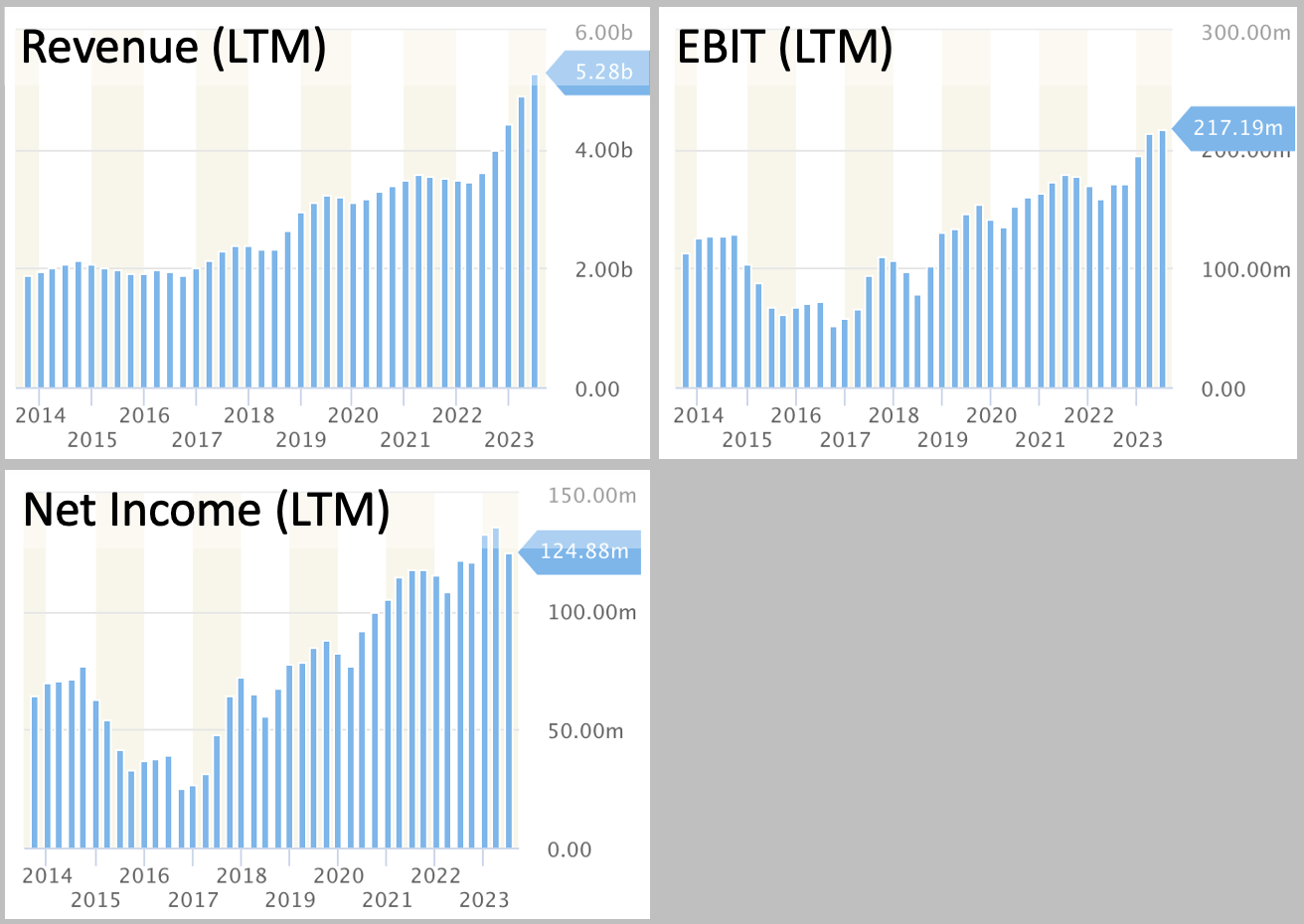

Primoris' revenue and operating income (LTM) are both at record highs since 2014, according to data from StockRow . Net income (LTM) is in an uptrend and is just below record levels.

{kind=link}

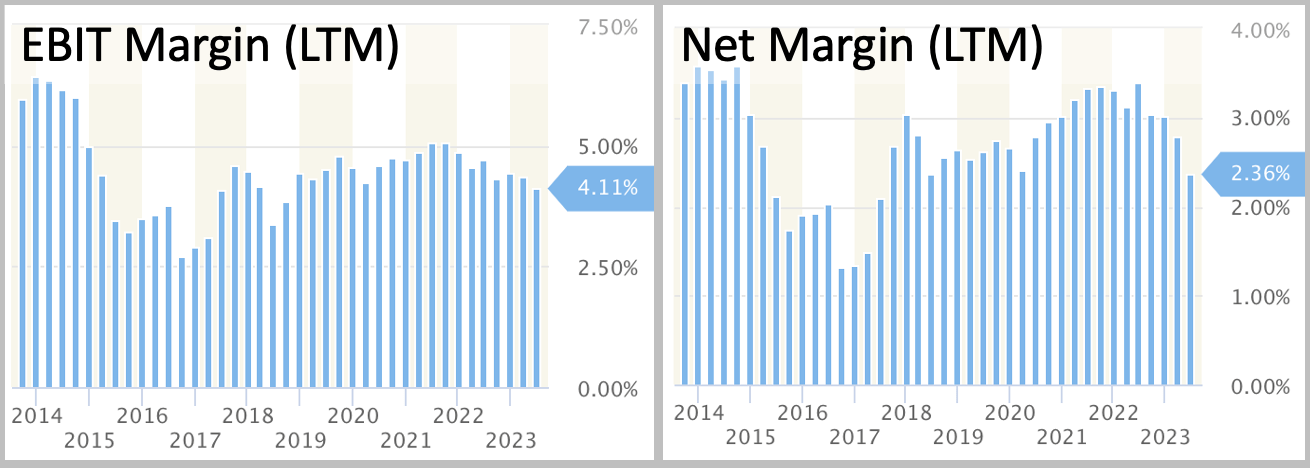

Operating and net margins (LTM) have been fairly stable since 2018 but still have room for improvement.

{kind=link}

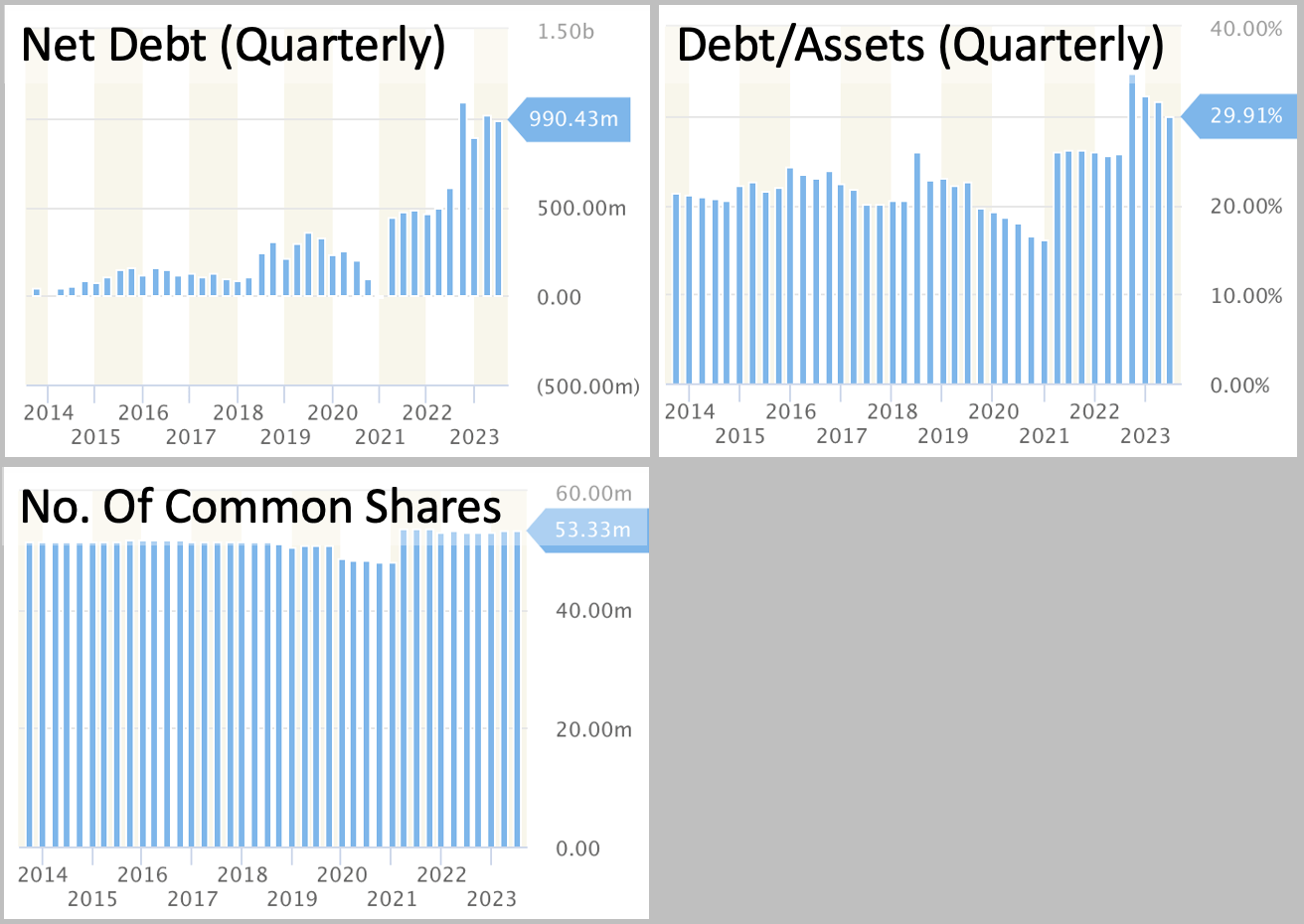

On the other hand, net debt (quarterly) is now more than double its value in Q2-2021, currently standing at $990.4m. Primoris' debt/asset ratio of ~29% is elevated compared to its historical range but is not obviously extreme. The firm's number of common shares has been stable since Q1-2021 and is slightly higher (3%) than its 2014 level.

{kind=link}

Primoris' P/S, P/E, and P/B (quarterly) valuation multiples are all near record lows since 2014. The firm's P/S ratio is below 1, standing at 0.31.

{kind=link}

Potential Catalysts

On the recent earnings call , management highlighted that the company reached new records for quarterly revenue and gross profit. In their view, the firm's success is aided by elevated customer spending levels and recent gains in market share. Those tailwinds could lead to additional records down the line.

Overall, the firm's quarterly backlog reached a new record, climbing 44% YoY and 133% over the past five years. Management anticipates that all of the utility segment's backlog will materialize as revenue in the next 12 months; for the Energy segment, the firm anticipates 59% of it to materialize by that time.

Primoris' revenues from its utility segment grew 34% YoY, and the segment's gross margin rose to 10.4% vs. 8.5% in the prior year. The power delivery and communication sub-segments benefitted from the firm's recent acquisitions (PLH and B Comm), which provided a boost to revenues. Gas operations experienced margin expansion. Management noted that the power delivery sub-segment is better positioned compared to Q2-2022 when it suffered from fuel and wage inflation; the firm has more flexibility now because many of its MSAs can still be modified via negotiation.

The number of MSA projects is growing, and management says Primoris is bidding and/or assessing ~$2b of projects. The majority of those are with previously established customers. Primoris believes that its efforts to update contracts it obtained via the acquisition of PLH will be "accretive to margins", and they expect those updates to be done by the end of the year. The firm expects to do $60m of high-voltage renewable projects sometime in the next 18 months, believing those projects to be an underserved part of the market that will likely see a rise in demand.

Primoris' energy segment achieved a strong book-to-bill ratio of 2.3 and saw its booking exceed $1.8b. About 36% of those bookings came from a broad group of industrial/civil awards from multiple states and of different sizes. Primoris obtained multiple big awards for its renewables services, amounting to $770m, and management says those solar projects will offer an extra 1.4 gigawatts of energy to the grid. Overall, renewables' revenue and margins increased YoY, and revenue growth is in line with the firm's 30-40% growth target.

The firm believes the renewables market has solid momentum and is unlikely to slow down in the coming years, and management highlighted recent billion-dollar investments taking place in domestic solar module manufacturing as evidence of strong sentiment in that market.

Risks

Primoris has a concentrated customer base, with its ten largest customers generating ~46% of total revenue in FY2022, per the firm's 10-K . On the other hand, the companies that make-up Primoris' largest customers tend to shift significantly from year to year. Still, this concentration increases the risk of downside surprises in the event that the firm loses a key customer.

The firm has $911m of unhedged variable rate borrowings. It estimates that a 1% rise in rates would increase its annual interest expense by around ~$9.1m.

Thanks to its Articles of Incorporation, Primoris has the ability to issue new shares of common and preferred stocks and potentially cause dilution. Around 53.1m common shares could be issued as of FY2022's end. Also, a 2013 plan allows the firm to issue up to ~2.52m common shares for equity awards.

Primoris has operations outside the US, accounting for ~5.6% of revenue in the first half of this year, per the recent 10-Q . Multinational operations introduce additional regulatory requirements and increase the odds of compliance issues.

The firm's customer demand typically fluctuates along with the state of the economy. An economic slowdown could significantly impair Primoris' financial results.

A sizable chunk of Primoris' revenue comes from new projects obtained via competitive bidding, accounting for 26% of revenue in FY2022. The firm has more difficulty predicting the location and timing of these projects, which may increase uncertainty in the firm's forecasts and guidance.

Events like natural disasters, public health emergencies, and political instability can lead to project delays and temporary work pauses that may incur additional costs. If the pandemic intensifies or a new health threat emerges, Primoris' results could deteriorate.

Execution

Buying a stock is a bet on where its price goes, not necessarily the fundamentals of the business. Since there is statistical evidence of trends in equity markets, investors who apply a scientific mindset may benefit from focusing on companies with share prices in uptrends.

Primoris' stock is in an uptrend and has recently made new highs. In early January, it broke above its 200-day rolling average, and it has climbed 59% since that time, per Finviz .

{kind=link}

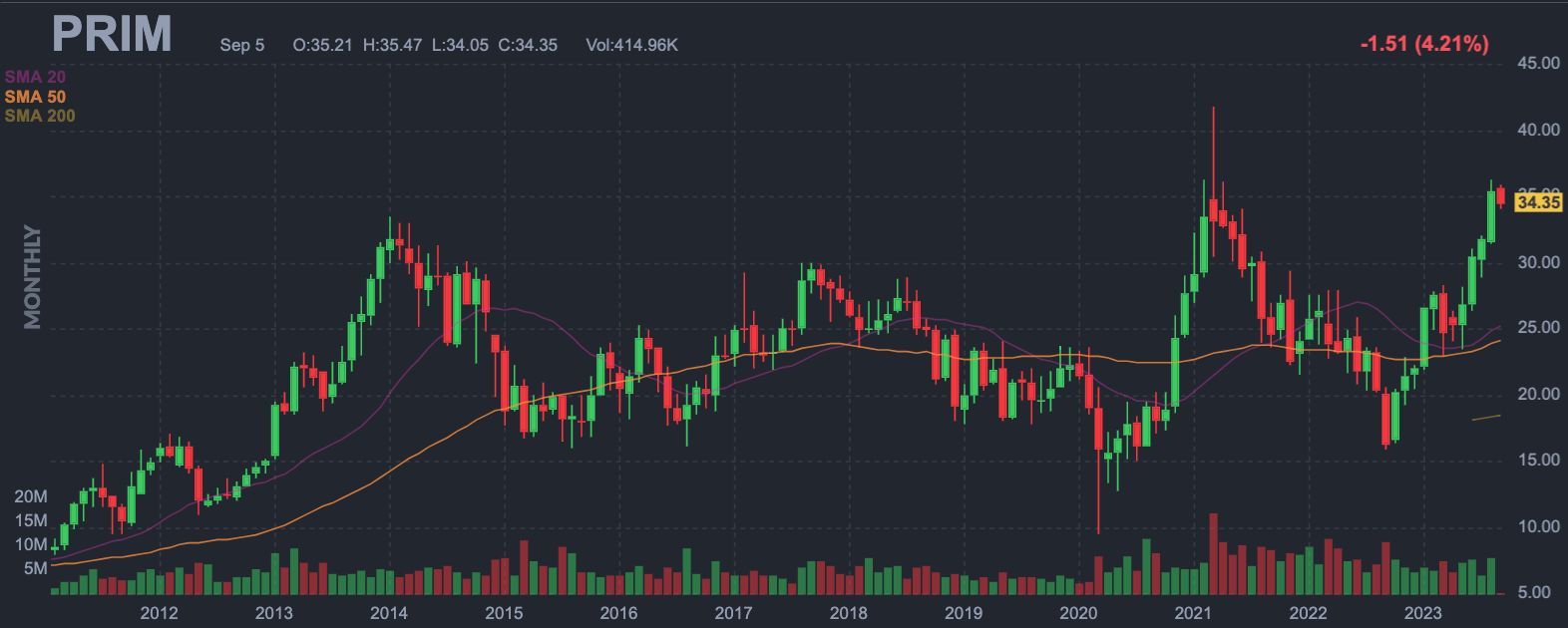

Zooming out, the stock's monthly closing price recently broke above its local peaks from 2021 and 2014.

{kind=link}

It may be sensible to consider a bet on this stock only while the uptrend remains in play, perhaps by requiring that a simple trend signal is active; for example, requiring that the price be above its rolling average (50, 100, 200-day, whichever has stronger evidence).

Bottom Line

Primoris' record revenues, healthy margins, record backlog, depressed valuation multiples, and strong price trends make it an interesting opportunity for investors. While its price continues to trend, the stock could be a reasonable bet for investors with a momentum-inspired strategy to consider.

For further details see:

Primoris Services Corporation: Growth, Value, And Momentum