PRIM - Primoris Services: Looking Solid For FY23

2023-06-02 03:15:51 ET

Summary

- Primoris Services reported record Q1 FY23 revenues of $1.2 billion, a 60.2% increase compared to Q1 FY22, with growth in its energy and utilities segments.

- The company is undervalued with a forward P/E ratio of 10.43x compared to the sector ratio of 16.13x, and a Price/Sales forward ratio of 0.27x compared to the sector ratio of 1.27x.

- With a solid growth trajectory, favorable market environment, strong financials, and low valuations, PRIM is considered a great buy right now, potentially providing significant returns to investors in 2023.

- I assign a buy rating on PRIM stock.

Primoris Services Corporation ( PRIM ) is a specialty contractor company that offers specialty fabrication, replacement, construction, and engineering services in North America. They work in three segments: Pipeline services, Energy/Renewables, and Utilities. In the pipeline services segment, they provide a range of services like pipeline construction and maintenance and pipeline facility and integrity services. In the Energy/Renewables segment, they offer services including procurement, retrofits, demolition, excavation, repairs, and maintenance services. In the utilities segment, they provide maintenance and installation services for new natural gas distribution systems and communications systems. PRIM announced its Q1 FY23 results with record first-quarter revenues. They are undervalued with a solid growth trajectory. I think it can provide handsome returns to its investors in 2023. Hence I assign a buy rating on PRIM stock.

Financial Analysis

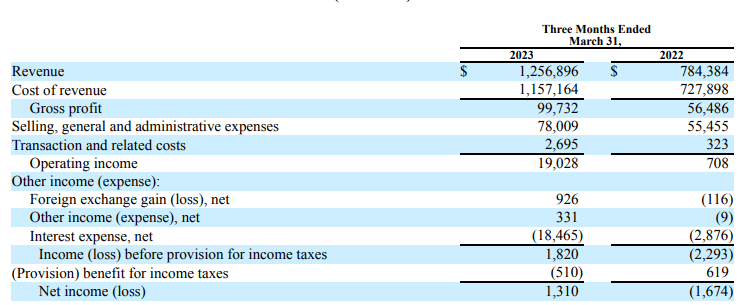

PRIM posted its Q1 FY23 results . The revenue for Q1 FY23 was $1.2 billion, a rise of 60.2% compared to Q1 FY22. The revenues increased in its energy and utilities segments due to, which saw a significant rise in its revenues. The revenues from the energy segment rose by 71% in Q1 FY23 compared to Q1 FY22. I believe increased industrial activity in the Gulf Coast and increased pipeline project work and renewable activity were the main reasons behind the revenue increase in the energy segment. The gross profit margin in the energy segment was 9.1% in Q1 FY23, which was 8% in Q1 FY22. I believe an improved mix of renewables work and improved margins in its pipeline businesses were the main reason behind improved gross margins in the energy segment. Now talking, the revenues from the utilities segment rose by 47% in Q1 FY23 compared to Q1 FY22. I believe strong growth in its power delivery and communications businesses and the acquisition of B Comm and PLH were the main reasons behind the utilities segment's revenue increase. The gross margins saw a slight improvement in the utilities segment; the gross margins were 6.3% in Q1 FY23 compared to 6.2% in Q1 FY22. I think improved rates in their power delivery services were responsible for improved gross margins in the utilities segment.

{kind=link}

Due to the improved gross profit margins in both segments, their overall gross profit margins increased to 7.9% in Q1 FY23, which was 7.2% in Q1 FY22. The net income for Q1 FY23 was $1.3 million compared to a net loss of $1.6 million in Q1 FY22. In my opinion, they performed really well. They significantly improved from Q1 FY22 and clocked record first-quarter revenues in Q1 FY23. If they manage to maintain solid growth, then I believe we might see a positive impact on its share price.

Technical Analysis

{kind=link}

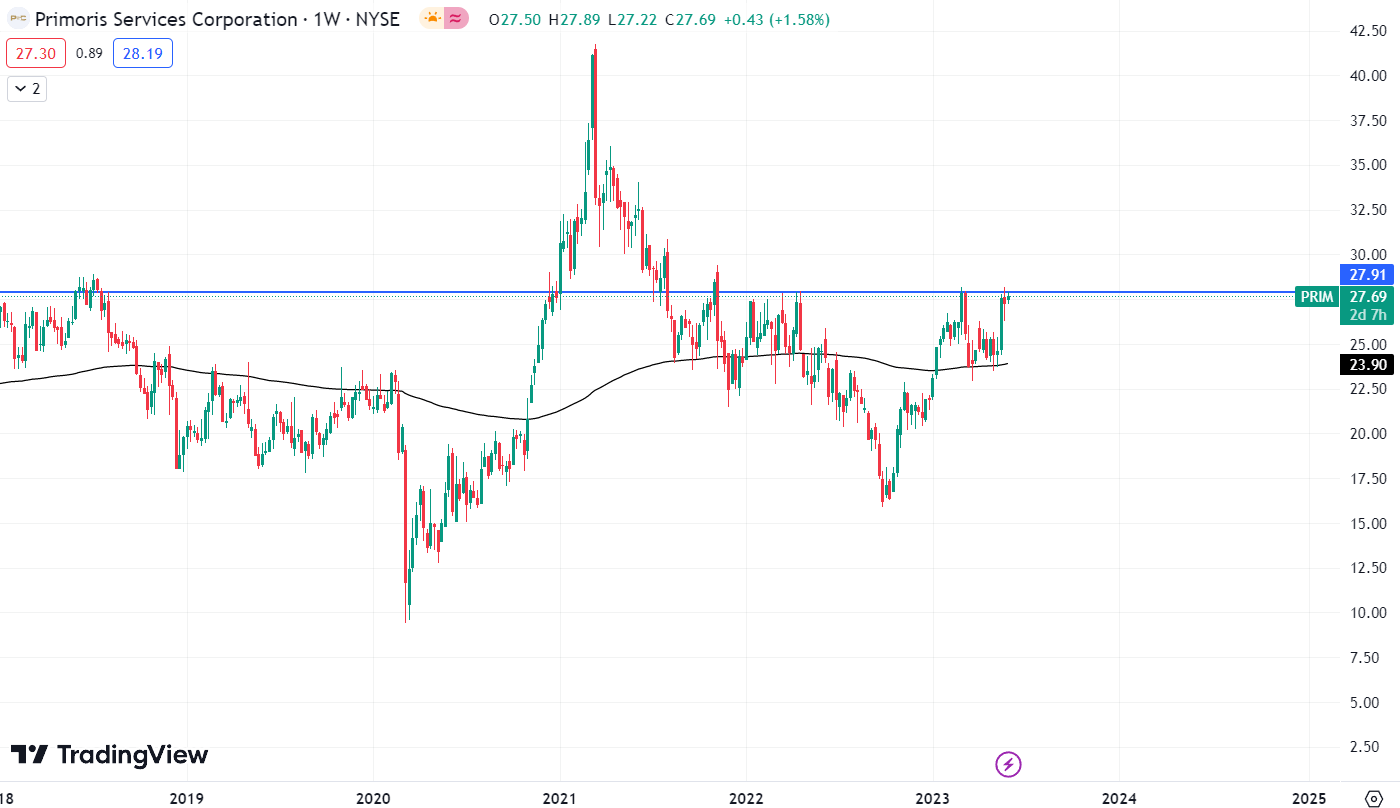

PRIM is trading at the $27.7 level. For the past two months, the stock was trading between the range of $24-$25.5, but recently it broke out of the range and is now trading near the resistance zone of $28. I believe PRIM stock is now at a crucial level because if the stock breaks the level of $28, then we might see an upward rally in the stock, but if the stock fails to break the $28 level, then the stock might fall up to the level of $24. So I believe one should only buy the stock if the weekly candle closes above $28.

Should One Invest In PRIM Stock?

The revenue of $1.2 billion is their record first-quarter revenue, and just to remind you, that first quarter is usually the lowest for them in terms of revenues due to delays from weather conditions in winter. So the significant revenue growth is encouraging, and I believe they are on the path of setting a new record in terms of revenue. I believe FY23 can be their best financial year. The backlog at the end of Q1 FY23 was around $5.6 billion, which is the highest backlog recorded by the company, and when compared to Q1 FY22, their backlog has increased by 38%, which is an optimistic sign. In addition, the federal legislation has increased infrastructure investments in highways and bridges, communications, and electric grid improvements. So I believe the overall trend might favor the markets in which they have a presence. So I believe PRIM might perform excellent financially in FY23, and due to this, I believe we might see a significant rise in its share price because I believe price follows profit. Hence I think this can be a great buying opportunity.

Now looking at its valuation. PRIM has a P/E ((FWD)) ratio of 10.43x compared to the sector ratio of 16.13x, and it has a Price / Sales ((FWD)) ratio of 0.27x compared to the sector ratio of 1.27x. So after looking at both financial ratios, I believe PRIM is undervalued and has a lot of growth potential.

{kind=link}

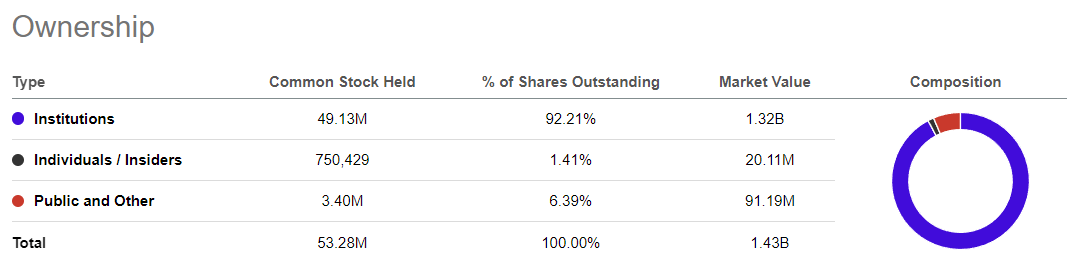

The shareholding pattern of PRIM looks solid, with institutions owning 92.2% of the shares of PRIM. I believe a company where institutions own more than 60% of the shares then the company is generally safe to invest in.

So after looking at its solid growth trajectory, favorable market environment, solid financials, and low valuations, I think PRIM is a great buy right now, and it might provide significant returns to its investors from current levels.

Risk

Their top ten clients account for roughly 46.1% of their revenue in 2022, 42.9% in 2021, and 47.0% in 2020, indicating that their customer base is reasonably concentrated. However, the top ten consumers on its list change from year to year in most cases. Their income is based on the success of both more substantial construction projects and comparatively minor projects funded by MSAs. The end of a large construction project does not necessarily mean that a client is permanently lost; nonetheless, the money generated in the future from work performed for that client may vary greatly. Additionally, they receive a recurring income from their MSA clients, which are often regulated gas and power companies. Their revenue might drop noticeably if they lose one of these clients. As a result, its business could suffer from decreased demand for its services from larger construction clients or from the loss of a significant MSA client.

Bottom Line

I have come to the conclusion that PRIM stock is a solid buy right now. They are undervalued with great growth potential and have performed significantly well financially. Moreover, I think it might provide significant returns to its investors in 2023. Hence, I assign a buy rating on PRIM.

For further details see:

Primoris Services: Looking Solid For FY23