MKFG - Printing Money With Markforged?

2023-08-07 16:19:33 ET

Summary

- 3D printers have the ability to disrupt and advance manufacturing capabilities. Markforged is well positioned in the industry.

- Markforged is a leading manufacturer of printers and software. It also generates recurring revenue through the sale of materials.

- The company has recently seen growth slow and gross margins decrease. It hopes these can be remedied in the near future.

- Markforged needs to see strong growth and a return to higher gross margins to reach a level of profitability.

There are certain technologies that come along that are able to disrupt the status quo. It can help improve the way that things have always been done. It also opens up other opportunities that might not have been feasible before due to either cost, capability, or other reasons. I think 3D printers or oftentimes called additive manufacturing and the advances in that technology is and will continue to be an industry disruptor. It has opened up new possibilities in the world of manufacturing. The amount of automation has allowed costs to come down. It also allows for just in time manufacturing and on site manufacturing for many parts. This helps eliminate many supply chain issues, which if you have ever run a business are a serious concern. These and other qualities have allowed it to bring more manufacturing back to the USA as well.

3D printers have advanced the processes and capabilities in a lot of different markets. One of the biggest areas that the effects are being seen is in the aerospace industry. I recently wrote an article about Rocket Lab USA. They mention multiple times throughout their company filings and in conference calls about how 3D printing has allowed them to reduce costs and increase time to market. When you are building a rocket you need things to work as they are supposed to or it will end in a big boom. This shows the reliability of parts made from 3D printers. This is not the only area though. You are seeing the technology used in military and defense, automotive, and healthcare as well. Even your local dentist might have a 3D printer in his office. I believe the use cases will continue to advance with the technology.

There are multiple ways to invest in the area of 3D printing. There are companies that make the hardware, software, provide services, etc. I am most interested in companies that are producing the actual hardware and technology allowing the market to advance. This goes back to the old idea of investing in a shovel company during the gold rush. One of the companies that met my criteria is Markforged Holding Corporation ( MKFG ). I want to take a dive into the company and see if it is worth investing.

Markforged Holding Corporation

MKFG provides a full platform that it calls the Digital Forge. "The Digital Forge, is an easy-to-use, reliable and intelligent additive manufacturing platform powering engineers, designers and manufacturing professionals globally. The Digital Forge combines precise & reliable 3D printers and metal and composite proprietary materials with its cloud-based learning software offering to empower manufacturers to create more resilient and flexible supply chains…. we have our own in-house manufacturing facility where we design industrial 3D printers, software and metal and composite proprietary materials." In essence The Digital Forge consists of the hardware, software and materials. The company generates revenues from the three categories as well.

The company makes three types of printers: (i) desktop printers, (ii) industrial composite printers, and (iii) metal printers. All of the printers operate on the same platform. Through the Digital Forge platform companies can make parts from a variety of metals or a variety of continuous fibers. These parts are strong and can be used in a variety of applications.

The software is also a critical piece to any modern day machinery. It is a cloud based software so you can manage your projects and system from anywhere. It allows the user to design and create a part quickly. The software fully integrates with all of the company's 3D printers. It also sells premium software subscriptions. This is separate from the standard cloud-based software platform offering that is fully integrated with the hardware.

The last piece of the Digital Forge is the materials. The company offers composite, continuous fiber, and metal. I consider this to be a critical part of the business. This is the opportunity for continued sales after the sale of the machine. It can provide a growing revenue stream as well as more machines being used around the world means more materials sold.

The company sells itself on making industrial strength parts. The company patented the Continuous Fiber Reinforcement process. It uses continuous strands of composite fibers to make parts as strong as and capable of replacing aluminum. This is one of the technologies that helps separate MKFG from the competition. It also offers metal printers in conjunction with their fiber

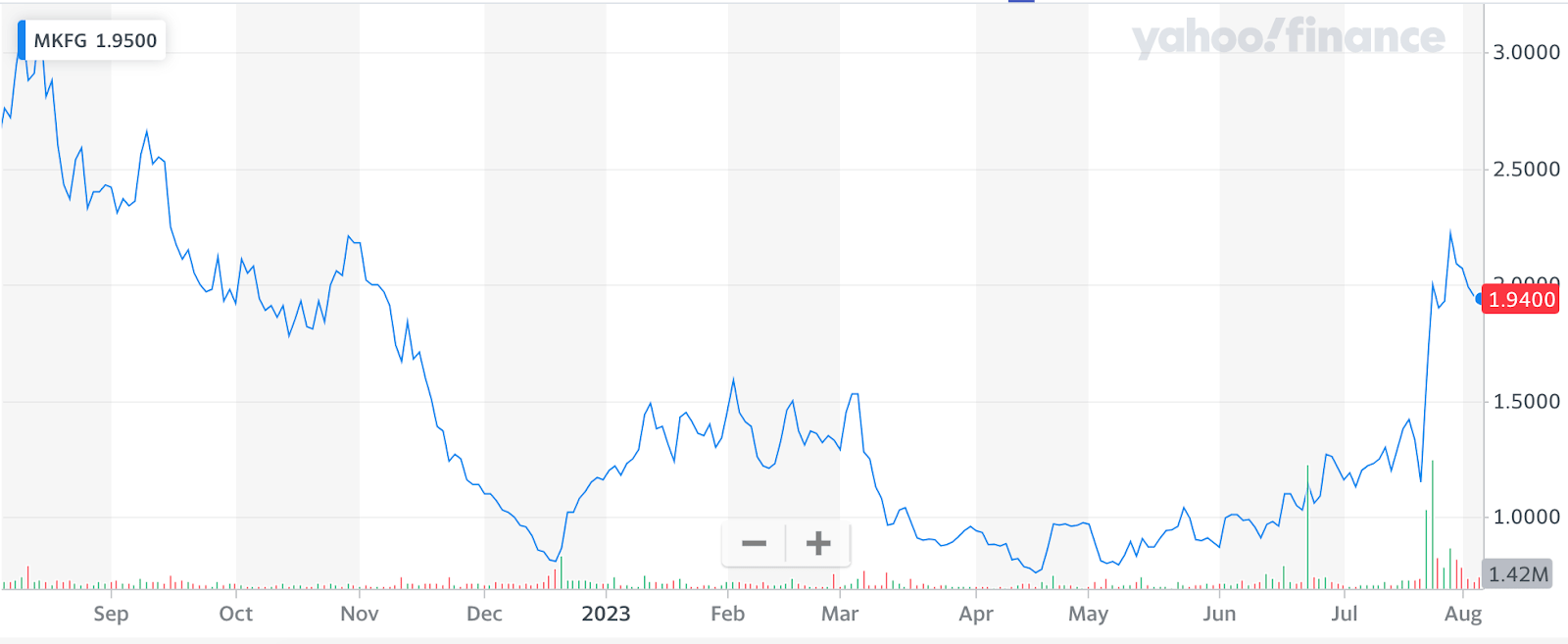

Price History

Like many smaller companies that are operating at a loss, MKFG is a volatile stock. The company was founded in 2013 and went public via SPAC in 2021. It valued the company at $2.1 billion at the time of going public. Things have for the most part gone downhill since then. The company was valued at $380 million as the most recent close.

The stock hit a high of $11 a share in July after completing its merger. It then proceeded to fall from there. It hit a low of $.71 in March of 2023. That is a 93.5% loss on your money. The company has seen a strong rebound since then with the price climbing to a recent close of $1.94 a share. That is an increase of over 173% in 5 months time. The stock is still down over 80% from its high. The chart below shows the overall negative trend in the stock price. It does not look good for those who purchased recently after the merger. On the other hand if you were a buyer early this year, then you would be very happy.

{kind=link}

The stock has been volatile. The recent spike seems to have mostly come from the recent purchases made by Cathie Wood and her ARK investment funds. This news seems to be the main driving force behind the rally. It will be interesting to see if that rally is sustainable or not. It has already pulled back from the high of $2.22 it reached on 7/28. The underlying fundamentals did not change for the company. That does not necessarily mean it will not sustain though, market sentiment is enough to keep the stock price elevated.

Financial Analysis

I think we can agree the company makes cool stuff (if not then that is a shame for you). That does not mean they make money selling that cool stuff. You don't invest in a company because they make cool stuff. What I really want to see them make is money. We will take a look into the financials of MKFG and see where the company is at and what the potential is or is not for the company.

MKFG has operated at a loss since its inception. That does not necessarily mean the business model is broken or the company is a failure. Younger companies will often operate at a loss until they hit a scale point. If it is operating at a loss then I want to see growing revenues and also a positive gross margin (hopefully a good gross margin). This means that it can most likely scale into profitability with its operating costs becoming a smaller percentage of revenues as the revenue line item grows.

The company has seen growth in its revenue and it operates with a strong gross margin.

| (in millions) |

| 2022 |

| 2021 |

| 2020 |

| Revenue |

| 101 |

| 91.2 |

| 71.9 |

| COGS |

| 50.3 |

| 38.4 |

| 29.9 |

| Gross Profit |

| 50.7 |

| 52.8 |

| 42.0 |

| Gross Margin |

| 50.2% |

| 57.9% |

| 58.4% |

There are some things to be concerned about right off when looking at the last three years' financials. First is that the growth slowed in the most recent year. After growing revenues by almost 27% in 2021 they only saw growth of 11% in 2022. That is a steep drop in revenue growth. Also while it is growing, it is not as high as I would hope in a smaller and younger company. The second concern is the declining gross margin. After having a fairly consistent gross margin in 2020 and 2021 it dropped 8% in 2022. That is a massive change in your gross margin. A 50% gross margin is still a good gross margin but losing 8% off your gross margin makes it hard to become profitable.

We can take a look at the quarterly data to get an idea about where things are trending recently. It gets us a layer lower in granularity and better understand how the business is doing.

| (in millions) |

| Q1 2023 |

| Q4 2022 |

| Q3 2022 |

| Q2 2022 |

| Q1 2022 |

| Q4 2021 |

| Q3 2021 |

| Q2 2021 |

| Q1 2021 |

| Revenue |

| 24.1 |

| 29.7 |

| 25.2 |

| 24.2 |

| 21.9 |

| 26.6 |

| 24 |

| 20.4 |

| 20.1 |

| COGS |

| 12.5 |

| 15.7 |

| 13 |

| 11.3 |

| 10.3 |

| 11.6 |

| 10.3 |

| 8.5 |

| 7.9 |

| Gross Profit |

| 11.6 |

| 13.9 |

| 12.2 |

| 12.9 |

| 11.6 |

| 15 |

| 13.7 |

| 11.9 |

| 12.2 |

| Gross Margin |

| 48.1% |

| 46.8% |

| 48.4% |

| 53.3% |

| 53.0% |

| 56.4% |

| 57.1% |

| 58.3% |

| 60.7% |

This shows the steady decline in gross margin. The gross margin seems to have stabilized, albeit at a much lower percentage. Also revenues are showing a steady year over year growth but once again not growth that gets one too excited.

The company addressed the gross margin issue and noted that they expect the gross margin to return to historical averages. Although it does not expect it to happen overnight. They are estimating a 47-49% gross margin for the second half of the year. The decrease in gross margin was mostly blamed on COVID-19 and the issues it has caused in the supply chain. This is a fairly common theme among companies that manufacture anything electronic. I would expect those issues to ease over the next year, as does the company. The other part that plays into this is that the company released a new product, the FX20. It is a larger printer. The company has been working through ramping up production on that printer. They said on the conference call that they have been able to shave costs off this process and expect the costs to continue to decline going forward. This should improve the gross margin going into the second half of this year and going forward.

In terms of revenue growth, the company expects revenue of $101-110 million for 2023. That would be almost no growth on the low end and 10% on the upper end of guidance. The company did see growth of 10% in the first quarter and I do expect the company to hit the higher end of this range. Once again it appears to be slowing slightly from the prior year growth of 11%. The slowing growth is a concern for me. Also the low growth rate off a small base is a bit concerning.

The company has three revenue channels that are based upon its Digital Forge platform. Those are Hardware, Consumables, and Services. Hardware revenue consists of the 3D printers and equipment. Consumables revenue includes fiber materials, metals and continuous fiber used by customers. Services revenue consists of warranty and maintenance contracts and software subscriptions. I would expect all three of these revenue streams to increase as there is more demand for the actual 3D printers in the market.

The continued revenue streams are very compelling. The company not only sells the machine but then also the materials that you use to operate the machine. This is a great recurring revenue channel for the company. The more machines that are in operation then the more revenue should be generated from the Consumable and Services business. Even if growth flat lines on the Hardware side it should still see growth on the Consumables and Services business. This can be seen in the financials. The Consumables and Services business lines are growing at a faster pace than Hardware.

| (in thousands) |

| 2022 |

| 2021 |

| Growth |

| Hardware |

| 69,112 |

| 64,974 |

| 6.4% |

| Consumables |

| 23,423 |

| 19,567 |

| 19.7% |

| Services |

| 8,423 |

| 6,680 |

| 26.1% |

| Total |

| 100,958 |

| 91,221 |

| 10.7% |

This trend in growth rates is consistent for Q1 2023 as well. This is an area that I think is a strong positive for the company. These two business lines should continue to see strong growth. It also shows that their printers are being used. Customers are returning for more and more consumables which means their printers are being used by customers. I know that sounds silly but it is not always the case that a piece of equipment is bought and it is continually used. Equipment purchases by companies can turn out to be not what they were looking for and they end up not using the equipment. This is not the case with MKFG. The company did state that the gross margin on these business lines are not much different from the Hardware side of the business. So the fact that these business lines are growing faster will not necessarily mean the gross margin will see an improvement.

I think the company has a chance to increase their revenue growth rate. Their new machine the FX20 has been exceeding demand. It is a higher priced printer as well, so the company can expect more revenue per sale. The Consumables and Services revenues are growing much faster than the projected growth rate for the company as a whole. They will continue to make up a larger portion of total revenue which would drive total revenue growth higher as well. This connects with analysts' projections as well. They expect growth of 15+% in 2024. This would be a strong positive to see the company increase their revenue growth.

Cash Position

This is one area that is always a concern with loss making companies. Will the company be able to reach a stage of profitability before running out of cash. The company expects to lower its cash burn in 2023 to under $50 million. It has a good cash position and expects to end 2023 with a balance of $120 million.

I think the estimate of less than $50 million is reasonable. The company burned $15.5 million in cash from operations during Q1 2023. This is the lowest revenue quarter for the company. The other three quarters will have higher revenue figures. The company will see growth throughout the year. Based upon this I think the cash burn figure is very reasonable. If the company can get an improvement in its gross margin then I think it could come in under the estimate.

Either way if the company ends the year with $120 million and they are burning cash at less than $50 million a year. It gives them at least 2 years to grow out their losses. I would expect that cash burn to decrease each year as well with growth in the company. I do not consider the cash position to be a concern in the short term.

Risks

The company is a loss making entity. It has not turned a profit since its inception. This will always bring about more risk on an investment. Will the company be able to grow into profitability? Or is it going to be a continual loss maker? My biggest concern is the slowing revenue growth of the company. It is not a high revenue growth rate and it has been decreasing over the past few years. It also fell well under its own estimates. When going public it had projected revenues to grow tenfold to reach $706 million in annual revenue by 2025. The company is expecting $110 million in 2023. There is not a path for the company to even reach half that projected number. The company was way off on their estimates before and could be going forward as well.

Declining gross margins is also a big concern and risk. I think this has a reasonable explanation and do expect this to improve. That is not to say it will though. If the company continues to operate at a lower gross margin it will make it very difficult to become profitable as a whole.

Conclusion

I think the 3D printer market is going to see strong growth and demand. MKFG is a company that makes a quality product. It also owns the supply chain by providing the materials to be used in the printers. This recurring revenue has been growing steadily, and is a great source of revenues.

The company has had some margin issues which I think will be resolved. The growth in revenues has not been what was expected. The growth has also been declining. This is a concern for me on the stock.

The stock has experienced a strong run up in price recently. It has made the company as a whole much more expensive. The 4x P/S ratio does not feel too high for a company in early stages. That being said, one would expect some solid growth to meet that valuation. I think MKFG is going to continue to compete strongly in this growing market. I would like to see their revenue growth increase, it is expected to do so in 2024. I think there is potential with their recurring revenues and also their newer more expensive product, the FX20. This is a stock I will keep watching for now. I would be a potential buyer if the price were to see a dip. I also will watch to see if the company can execute at a higher level, return gross margins to over 50% and see some more revenue growth in their new products. For now I rate the stock a hold. This one is worth keeping an eye on though.

For further details see:

Printing Money With Markforged?