GAIN - Private Credit Is Dancing In The Streets: 2 BDCs To Dance Carefully

2024-01-02 06:44:25 ET

Summary

- There are many tailwinds for private credit, including tighter banking regulations, where even Jamie Dimon has asserted that many of these players are currently dancing in the streets.

- There are both significant risks and opportunities in the BDC space.

- Here are two BDCs that should be able to capitalize on the current tailwinds, while keeping the risk level in check.

It is no doubt that the private credit players are experiencing some very favorable tailwinds, which have resulted in notable portfolio growth across the BDC landscape.

There are many factors contributing to rosy prospects of private credit, but I would distinguish these three as one of the most important ones:

- Higher interest rates - elevated SOFR has reduced the base of investments that could be underwritten at conservative covenants, which, in turn, has shifted some of the theoretically lower-quality businesses to more flexible lenders such as BDCs.

- Constrained access to public capital markets - during times like this, when the interest rate path is still relatively uncertain and when there is still a great chatter around the potential recession, it is very difficult and expensive to source capital via public capital markets. As a result, the attractiveness of the private market has improved and in some instances enabled financing that would not otherwise be possible via the public market.

- Tougher bank regulation - on top of this, there is an additional pressure stemming from the conventional banking segment. As the banks get increasingly more regulated, their willingness to channel capital towards more volatile and not very established businesses shrinks, thereby offering another opportunity for BDCs to step in and close the structural gap.

While one could argue that the first two factors are transitory, when it comes to the third point (i.e., bank regulations), it is clear that we are talking about a systematic change.

Even Jamie Dimon asserted that the consequence of stricter banking regulations will be blooming private credit actors and that some of these players are already "dancing in the streets" knowing that the competition from banks will eventually become weaker.

{kind=link}

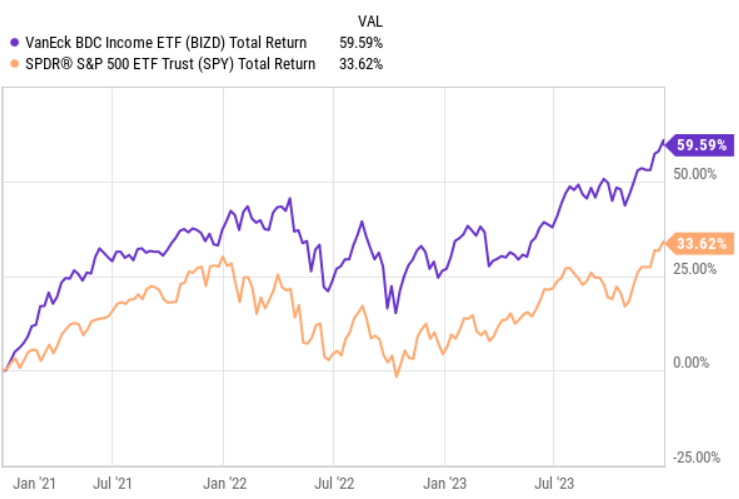

Looking at the 3-year historical performance of the BDC market, it is indeed quite evident how BDCs (in aggregate) have managed to deliver solid returns, even above the S&P 500.

So, now the focus (at least from my position) is really to participate in this dance to benefit from the overall tailwinds while making sure to protect capital from any potential shocks in the system.

With this in mind, let me introduce you to two BDCs, which, in my opinion, should be able to stay consistent to the prevailing dividends and at the same time take full advantage of the current environment.

Ares Capital (ARCC)

ARCC is the largest BDC out there with a market cap of over $11.4 billion and a remarkable track record of delivering superior returns without going too far in the risk curve.

{kind=link}

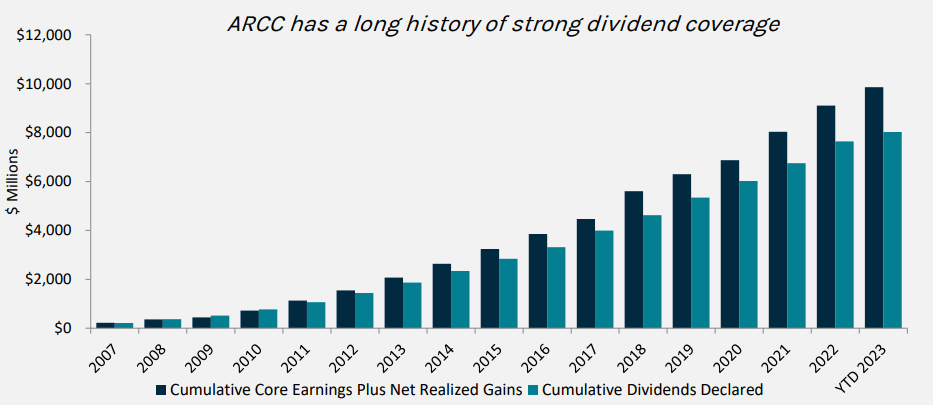

As you can see in the chart above, ARCC has remained very consistent in its commitment to grow the dividend as well as the underlying earnings. Since 2018, core earnings have increased at a faster pace than the dividend, allowing the Fund to reinvest further opportunities and deliver price appreciation gains on top of the attractive income (currently at ~ 9.6%).

ARCC Investor Presentation

One of the things that is ARCC-specific is the diversification element, where the strategic capital allocation is made not only across various pockets of the private credit market but also across private equity, real assets, secondary credit, and other auxiliary credit opportunities.

So, the combination of size and diversification de-risks the investment case and warrants a favorable ground from which to seize further growth options.

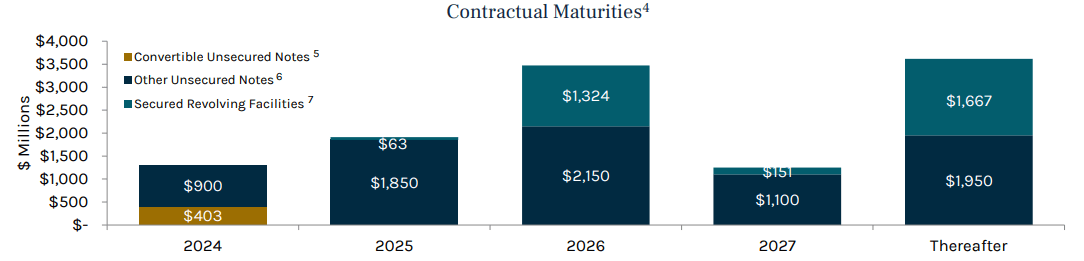

Moreover, ARCC is also well-positioned from the balance sheet's perspective, carrying an investment grade rating, which helps keep the cost of capital down. This is very critical for BDC businesses to have a positive and predictable spread between portfolio yield and cost of capital.

In this context, the fortress balance sheet facilitates lower interest rate costs that can enable ARCC to maximize the captured value from the investment portfolio (including not introducing excessive risk to keep the spread up).

{kind=link}

Lastly, the debt maturity profile is nicely structured, with the weighted average term to maturity of ~5 years. This means the following:

- ARCC will enjoy the benefit of the previously assumed cheap fixed-rate debt for a couple of years in the future.

- There will be a reduced need to refinance in the current environment, when the interest rates are still so high.

Gladstone Investment (GAIN)

Opposite to ARCC, GAIN is a much smaller BDC with a market cap of ~ $480 million. However, there are three reasons why I consider GAIN a safe "partner with whom to dance".

First, GAIN is heavily skewed towards companies, that carry straightforward business models, and operating in rather non-cyclical industries.

10-Q - 11/01/2023 - Gladstone Investment Corporation

{kind=link}

This is not that common for a large chunk of BDCs, which tend to focus on VC-type enterprises that have not yet established cash flow neutrality in their underlying operations (i.e., they are still heavily reliant on external financing including equity).

Second, the portfolio is further enhanced by the presence of preferred shares in businesses with strong cash generation and healthy leverage profiles that account for ~ 30% of the total AuM.

The extra benefit added by these instruments is associated with their sensitivity (through the duration factor) to the interest rate changes. Knowing that interest rates have most likely peaked and that the market is pricing in several cuts already in 2024, GAIN should be able to register outsized gains via preferred share appreciation in value.

Another positive aspect to take into account here is that typically preferred shares embody also an element of fixed rate payments, which puts the GAIN in a more advantageous position to defend its spreads from reducing SOFR.

Third and perhaps the most important one is the GAIN's leverage, which is one of the smallest in the sector.

As of December 2023, the BDC average level of debt to equity stood at 117%. For GAIN, the corresponding measure is at 73.6% or the third lowest in the BDC space.

In my opinion, this is crucial from two angles:

- Such a conservative level of debt in GAIN's books should allow the Management to act opportunistically when attractive deals start to occur.

- In the scenario of an economic downturn and rising corporate defaults, GAIN will be in a better position to shield its dividend and keep the NAV base in balance.

In closing

I agree with Jamie Dimon that there are many reasons for BDC to dance in the streets. I also share the same opinion about the potential risks that are associated with this and that in the case of struggles in the economy, there will be a lot of pain in the BDC sector.

Having said that, if investors remain prudent in their approach and are selective, the prospects of enjoying outsized returns from BDC exposure can be very attractive.

For further details see:

Private Credit Is Dancing In The Streets: 2 BDCs To Dance Carefully