PRCT - Procept BioRobotics: Adding For 2023 Rebound

2023-05-30 10:19:49 ET

Summary

- Procept had weak results on adding fewer than expected Aquabeam devices in Q1 of 2023, leading to a fall in the shares.

- Procept has strong potential in urology where its Aquablation technology has many potential indications.

- The company should rebound throughout the year on increased consumable usage and new deployments of its device through IDNs.

PROCEPT BioRobotics ( PRCT ) is an interesting play on the continued trend of lesser invasive procedures for common health problems. The medical device sector has increased in size and importance over time, and investors have embraced its combination of growth and high margins. Compared to other technology stocks it requires lower marketing expense allowing for a faster path to 20%+ operating margins and profitability. PRCT is focused on urology and as of now the main purpose of their Aquabeam system is to fix benign prostatic hyperplasia. Over 12 million men in the US are being treated for this condition, creating a significant need for new and novel therapies. The condition lowers quality of life by closing the urethra and is very common among older men with up to 50% having some symptoms. A total addressable market of over $20 Billion on the surgical side gives significant runway just in the United States. The company has run into weakness recently after Q1 added fewer new systems than expected by the market. The placement of systems is directly related to the ramping of procedures and sent the stock down to 52 week lows recently. However, this should be a great time to pick up the stock on sale, as the management sees these deployments as just pushed out temporarily. Looking at the Q1 results the moving parts begin to become apparent.

{kind=link}

Q1 - Disappointing system additions, Solid usage

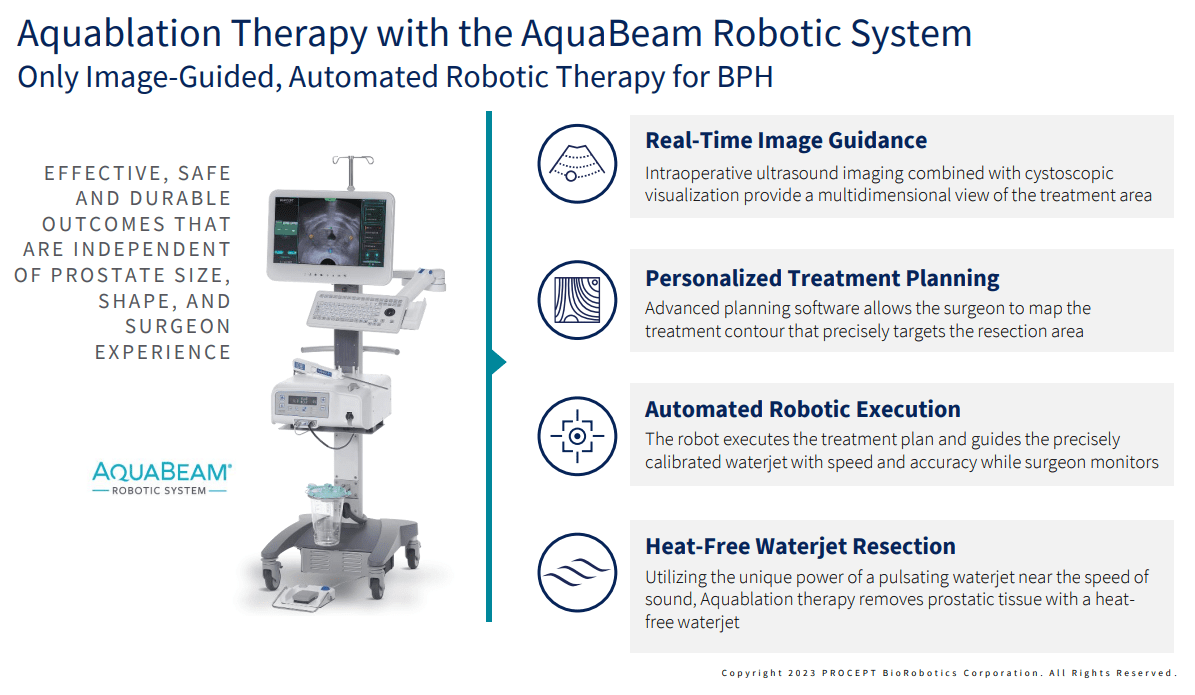

Additions of Aquabeam systems in Q1 were 28 versus 25 in the prior quarter, a disappointing step down in system deployments. However, management said they were confident in getting 140 for the full year, with 45% in the first half. This is directly guiding to 38 for the second quarter and the confidence says they were well on track when the stock had results. Even though the quarter revenue missed at $24.4 million, they actually increased guidance for the full year to $128 million or 71% yearly growth. This is one reason I see a nice buying opportunity in shares between $25-33 per share. PRCT is continuing to focus on large IDN's or Integrated Delivery Networks to drive scale in Aquabeam deployments. They called out strength for IDN's in Q2 after a lull in Q1 allowing sales growth to pick up this year. Large IDN's allow for significant sales all at once and PRCT continues to add IDN's over time to scale its sales capacity. If you look above you can see the technology of Procept is significant with heat free waterjet at the speed of sound removing tissue in the prostates of men with BPH. Ultrasound imaging and visualization gives a multidimensional view and the software allows easy planning for the procedure. This is why utilization is improving with handpiece revenue (1 per procedure) growing to $11.8m in Q1 with 165% y/y growth. Long term this is what will expand margins as the handpiece has a much higher gross margin than the Aquabeam systems installed at hospitals nationwide. Monthly utilization of the system was 6.3, versus 6.0 in Q4 and just 4 in the 2022 yearly guidance. This is a strong rate of growth even as they are adding lots of new systems to areas that may already have access to the procedure somewhere.

The company continues to focus on the 30% of hospitals that do 70% of the BPH procedures in the US to maximize value out of each system placed. The other smaller hospitals are a longer term goal once revenues and placements are ramped to a significant level in the major hospitals. Revenue outside the United States continues to be a small piece of the story with only $10 million in 2023 expected. Long term Japan, United Kingdom, China and the rest of Europe will provide additional sales growth opportunities. Management called out that 90% of surgeons continue using the system once they have given it a try, a good data point for long term utilization. The company has signed deals with United Healthcare and Blue Cross Blue Shield Michigan recently putting them at 95% of men insured across the US. This will help drive adoption further as price won't be as much of a hurdle after these have now come into effect from April and May 1st. The transitional pass through payment of $8429 is good through 2023 meaning pricing of the treatment won't be a significant issue for continued uptake for the year.

Risks

The risk here is substantial and requires understanding that small changes in guidance will play a large role in share movement. The company is burning a decent amount of cash, with $181 million in cash on the balance sheet right now. Burn rate is around $17.5 million per quarter which gives 2.5 years of runway at today's rate. However, as the company scales sales representatives and manufacturing losses may increase in the short term as system sales will increase losses short term. This may mean a capital raise or additional debt required to be taken in late 2024 or early 2025 as prudent managers look to raise significantly ahead of any potential cash crunch. Also the company is a small cap at $1.45 Billion market cap, meaning volatility in any potential recession or large selloff will be magnified. As you can see above the medical device sector has been slightly down over the past year at -3%, trailing the S&P 500's gain of 2%. The company is also competing against other large players such as Intuitive Surgical ( ISRG ), whose Di Vinci system is capable of removing prostates. However, for BPH in particular Aquabeam is purpose built and more efficient while being much less invasive. It is an area with continual new entrants though and without the power of scale PRCT needs to be concerned with long term competition if they make waves in this area.

Buy on overdone selloff

PRCT has trailed its sector heavily, with the recent volatility giving that potential for rebound with a solid year. Management is showing confidence, and the small cap device sector has been bottoming out the past month. Issues with staffing are a thing of the past and procedures are ramping in hospitals across the United States. Valuation is reasonable for a company with significant long term potential and which is a potential acquisition target for a bigger player in the sector. At 11.3x 2023 sales and potential for sales upside, PRCT is a good stock to hold for a return to the $45+ per share level.

For further details see:

Procept BioRobotics: Adding For 2023 Rebound