SILK - Procept BioRobotics: Adding Value Through Robust Unit Economics Reiterate Buy

2023-08-10 15:24:25 ET

Summary

- PRCT's aquablation therapy has shown strong growth, with revenues of $57.5mm in Q2 FY'23.

- The company's economic levers include new system placements, and growth from its installed base, with a record number of systems placed in Q2.

- Net-net, reiterate buy, eyeing a $40 price objective.

Investment updates

Since my February publication covering PROCEPT BioRobotics Corporation ( PRCT ), the company's equity stock has congested sideways and failed to catch a reasonable bid.

Despite the market's posture, my own posture has not changed on PRCT, considering 1) a long-term view, and 2) thoughtful analysis of the future. The firm's Aquablation therapy is a potential long-term compounder with interesting economics in the mix in my opinion. The economics surrounding this segment provide the key levers to see PRCT's valuation push higher into the future.

As a reminder, PRCT books revenues on the placement of Aquablation units, and then, on the usage of the respective handpieces, ancillary consumables, and maintenance services once installed. It did $57.5mm of business in Q2 after growing system sales by ~50% YoY.

Net-net, I continue to rate PRCT a buy on long-term value, noting the company's exceptional growth percentages, robust unit economics, and clear path to adding value for shareholders. Rate buy at $48 price objective.

Figure 1. PRCT price evolution

{kind=link}

Critical facts to reiterated buy thesis

Whilst several endogenous and exogenous factors are at play, the crux of the investment debate for PRCT boils down to fundamental, sentimental and valuation factors in my view. Chief among these is the company's unit economics and the sentiment in its equity stock. I've outlined the case below.

(1). Fundamental drivers

The company's latest numbers for Q2 FY'23 do an excellent job at providing insights for the full year and beyond. Several talking points are worthy of discussion.

- New placements, growth from installed base

It clipped $33.1 mm in quarterly turnover, up 98% YoY, driven mainly by system revenues, both on existing systems and new system sales. PRCT's rise in robotic sales stems from two pivotal drivers. First, its capital pipeline contributed significantly, allowing it to ship orders on sale. For instance, the Q2 growth was underscored by the placement of 40 robotic systems in the U.S., translating to domestic system revenue of $14.8 mm. This was a company record and up 74% growth over the previous year. The company's U.S. installed base was at 233 at the end of the quarter. The average revenue per system was therefore $66,367 for the quarter [$265,470 annualized].

Second, the Q2 system average selling price ("ASP") reached $370,000, a 5% sequential gain on Q1 FY'23. Both pricing and volume (demand) are responsible for the impressive revenue clip last period.

As a major positive, you can see the company's sales ramp to date in the chart below [Figure 2]. Note that sales are curling at a steep grading whilst its operating assets are thinning. This tells me PRCT is able to produce revenue growth on a capital-light operating model, not requiring a higher capital charge in order to expand. The value this provides to PRCT is discussed later when talking about valuation factors.

Figure 2. PRCT Sales [LHS] vs. Operating Assets [RHS]

Data: Author, PRCT SEC Filings

- Installed base moving up the utilization curve

As mentioned, the second part of the value equation for PRCT is its contribution from consumables and ancillary products related to its installed base. Sales here are indicative of utilization trends. All good to have a bunch of systems placed at various hospitals, but if they aren't being used, that's another thing. Alas, it excelled last quarter in this domain.

Handpiece and consumable sales shot to $13.6 mm, a 138% expansion YoY. You see this via the rise in monthly utilization per account, ~9% higher than the same quarter last year. This large upside once again ties back to PRCT expanding and growing its installed base of systems. In addition, PRCT's active surgeon growth was robust, boasting an active surgeon retention rate ~90% for H1 FY'23.

The surge in U.S. handpiece revenue during Q2 can be attributed to existing accounts and more surgeons embracing Aquablation therapy for all respective procedures. This also tells me PRCT's robotic systems are shifting up the utilization curve. Utilization is a robust indicator of long-term market adoption in this case. Without the procedural volume, you can forget any value-add for us shareholders. It needs to add more surgeons to its books, and get these surgeons doing more surgeries. Simple as that.

To this point:

- The company shipped 3,904 handpieces in the U.S. during Q2, a hefty growth of 124% in units YoY

- The ASP on these was ~$3,110. This gets you to $12.14mm for the period. Thus, ~37% of Q2 revenues were obtained from utilization over new system sales.

- PRCT added around 30 capital sales reps back in Q4 last year. It believes in a productivity ramp of 6—9 months for each of these reps, hence they should be coming into the money around about now. H2 FY'23 could very well be a tailwind for the company if these reps convert.

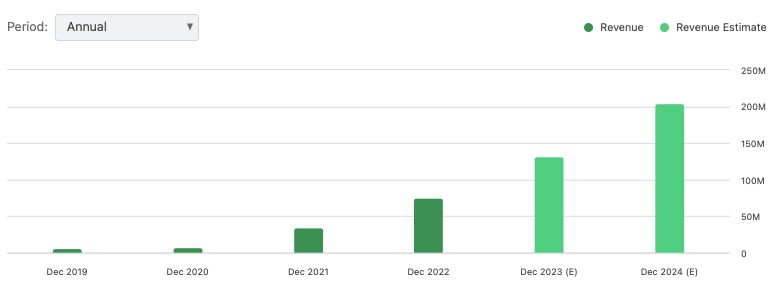

The company raised its FY'23 total revenue guidance to $131 mm, calling for 75% growth over 2022. PRCT anticipates ~55% of system sales in H2, or roughly 144 placements for the year.

It looks to a handpiece ASP of ~$3,100, and projected other consumables revenue of $5.9mm, getting to the $131mm. It hopes to pull 55% gross on this with OpEx of $174mm, leading to an operating loss of $43mm. You can see the ramp on Wall Street's revenue estimates for PRCT below [Figure 2a].

Figure 2a.

{kind=link}

Regulatory tailwinds

I touched on this last publication, but it's important to rehash the numbers to provide insights into FY'23 expectations. Critically, United Healthcare, the largest commercial payer in the U.S., updated its policy to include Aquablation therapy.

The benefits of this to PRCT and its Aquablation candidate pool are threefold:

- It significantly enhances accessibility for individuals with benign prostatic hyperplasia ("BPH"), the condition that Aquablation therapy looks to resolve. For a deep dive on BPH and the treatment market, catch my original PRCT coverage in November last year . More access = more surgeries = more men treated = more income. It is symbiotic; both patient and company are beneficiaries to this move.

- The explicit impact to PRCT is substantial with an estimated coverage for around 95% of men in the U.S.

- CMS's FY'24 proposed rule for hospital outpatients also enhances the economic landscape for PRCT. CMS proposes a 3% increase in payment for Aquablation procedures, entitling $8,847 per procedure to each hospital performing Aquablation.

These are tailwinds that shouldn't be ignored. We've seen the impacts of CMS rule changes in names like Silk Road Medical ( SILK ) [see here ], which can cause large changes in market value to the upside or downside.

(2) Sentimental factors

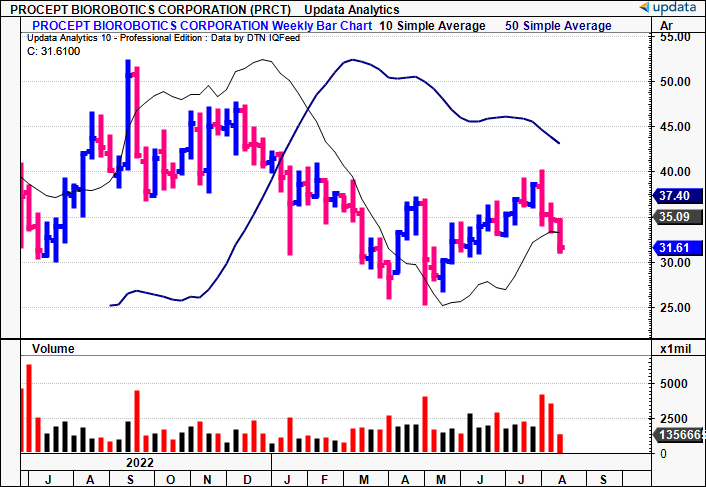

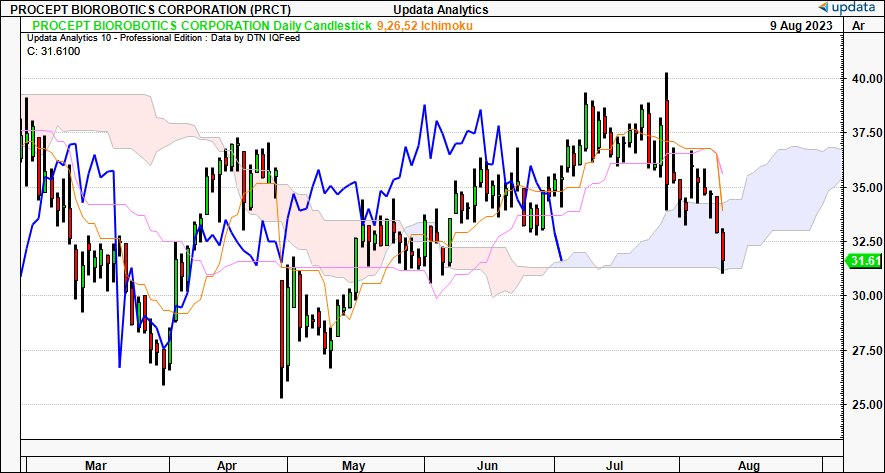

Three points are relevant in the discussion on sentiment in PRCT's equity stock. One, trends are more or less neutral at the moment on pricing studies. Using the cloud charts below, the daily chart looks to the coming weeks, the weekly chart to the coming months. On the daily, you've got the stock testing the cloud base with both price and lagging lines. This is a critical juncture. A break lower would likely reverse sentiment more to the downside in my view. A break higher is therefore critical from here.

Figure 3.

{kind=link}

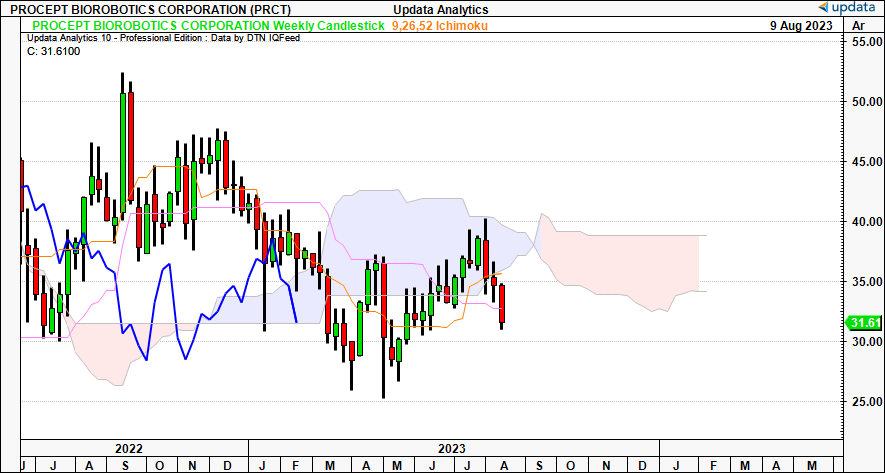

Similarly, on the weekly, the lagging line is testing the cloud base and we must see a break higher for hear to garner technical support. This is one major risk to my investment thesis albeit in the medium term. Hence, I'd be looking to a move toward ~$35 in the coming weeks to suggest there's near-term accumulation.

Figure 4.

{kind=link}

Two, Wall Street analysts have revised their top-line estimates higher by 6 times in the last 3 months, with no down revisions. Consensus now calls for $131mm this year, stretching 55% in FY'24 and another 42% the year after. These are notable forecasts that suggest a potential divergence in equity value to business growth in my view. You have the opinion of a whole substrata of market players with these estimates, thus, that they are turning upward is a potential bullish factor.

Three, options-generated data shows investors are bullishly positioned out to August and September, with heavy demand for calls at the $40-$45 strike depth. We even have contracts in the money at $55, thus telling me there's actual money at risk looking for these targets. There's no matching of put demand on the other side of the ledger. Hence, my estimate is that investors are looking to a move towards the $40 mark to start.

Collectively, these three drivers indicate that sentiment is positive in the stock, however, pricing studies require a more constructive setup to see market values lift back to previous highs.

(3). Valuation factors

Investors aren't parting with their PRCT stock easily and will sell to you at 12x forward sales as I write. The market's also priced its a 9.5x net asset value, indicating the premium it places on the company's robotic systems. PRCT has in effect created $9.50 for every $1 in market value with this multiple, tremendous value for its shareholders. It makes sense, too, given that the company's capital is what produces the profits, via direct sales and the tail of income produced on each placement. Further, at 12x forward, it tells me the market has tremendously high expectations of the company's revenue prospects going forward.

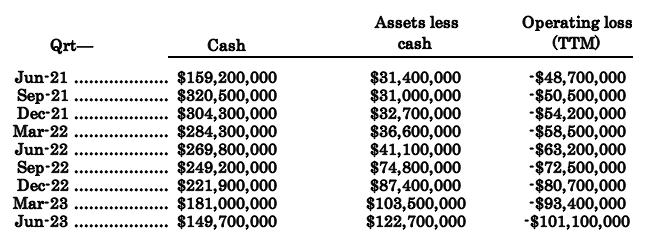

Looking at what the 12x might get you today, consider management's 75% FY'23 growth forecasts. Whilst it is a crude measure, you can see this as a 'price-sales-growth' type of figure. This gets you to a "PSG" of 0.16 (12/75% = 0.16), indicating there is potential value for the growth on offer. Paying 9.5x in net asset value also gets you $3.44 in book value per share, down substantially from periods gone by. However, this is due to the fact the company's NWC density has narrowed in sharply as well. Looking at the rolling asset values less cash, you can see the company's substantial growth of 290% in the last 2 years. This, as cash on hand tightened by 53% from the high point [Figure 5]. At 12x FY'24 sales estimates of $203mm, this gets you to $2.43Bn in market value, otherwise $48.20/share, 53% value gap, thus supporting a buy rating [Figure 6].

Figure 5.

{kind=link}

Figure 6.

Data: Author

In short

The numbers keep ratcheting higher for PRCT as time rolls on. Critically, it is showing robust growth in its core unit economics, by selling more robotics systems, and booking more ancillary revenues from its installed base. This is imperative for it to add shareholder value, by lengthening the tail of asset returns from each sale. Net-net, I continue to rate PRCT a buy, eyeing $48 as the next price objective. Reiterate buy.

For further details see:

Procept BioRobotics: Adding Value Through Robust Unit Economics, Reiterate Buy