UNLYF - Procter & Gamble: Earnings Growth Seen In FY24 But Fairly Valued For Now

2023-08-14 18:19:06 ET

Summary

- Investors were clearly happy with The Procter & Gamble Company's recent FY23 results, with an uptick in share price. They saw particular rise in sale and EPS during Q4 FY23.

- Its outlook is also largely positive. And with a come-off in inflation, its EPS growth could be higher than forecast.

- But EPS growth already appears to be baked into the price, leading to a Hold rating on the stock.

When the consumer goods giant The Procter & Gamble Company ( PG ) released its financial year 2023 (FY23) results toward the end of July, its share price saw the second-biggest rise year-to-date [YTD] of 2.8%. The biggest increase of over 3.5% came in after it released its third quarter results in April. Clearly, investors are happy with the numbers. The question now is whether there's a case for a further price rise for P&G? Let's first look at the latest numbers to find out.

Price increases drive FY23 growth

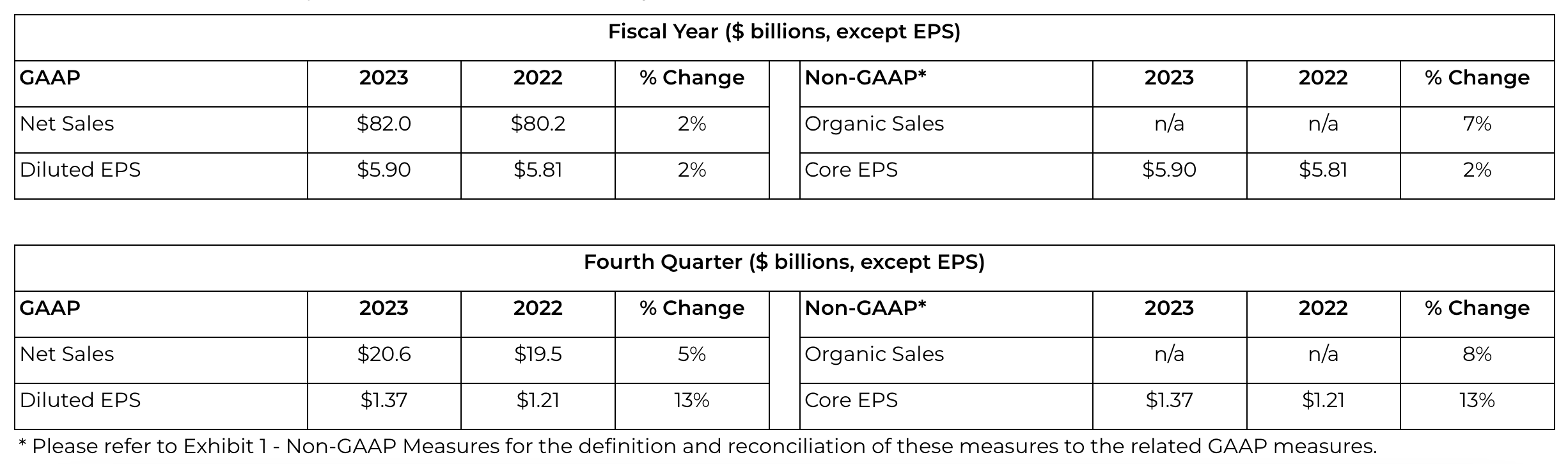

For FY23, the company saw a 2% increase in GAAP net sales (FY22: 5%). The slowing down in GAAP sales isn't as bad as it looks. It's in line with the company's initial guidance for FY23, where it expected a three percentage point headwind from foreign exchange. If it weren't for that, P&G would actually have seen exactly the same growth as last year.

Further, organic growth, which is sales in constant currency and after removing the effect of acquisitions and disposals, performed better, at 7%, the same as last year. This is actually better than the 3-5% that was the initial guidance. It's worth noting, however, that organic growth was largely due to higher prices, with a decline in volumes. The volume decline is in contrast to a 2% increase last year, suggesting weakness in demand.

{kind=link}

The company had already started seeing a volume drop last year, though. It explained that a fall in volumes in the final quarter of last year (Q4 FY22) was "primarily due to pandemic-related lockdowns in Greater China and reduced operations in Russia."

However, the trend of falling volumes has continued even in Q4 2023, despite the otherwise good sales figures, for which no explanation is provided this time. GAAP sales grew at the same rate as last year of 5% year-on-year (YoY) and organic sales actually rose by a percentage point higher of 8%.

Profits improve

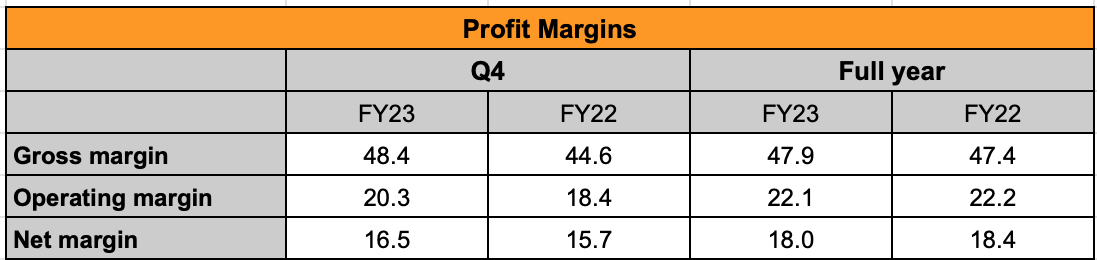

P&G's operating margin remained essentially unchanged at 22.1% for FY23, but there is a definite improvement in Q4 FY23 20.3% (Q4 FY22: 18.4%). This is a trickle down from an improvement in gross margin (see table below), which the company attributes to both higher pricing and productivity improvements.

{kind=link}

With rising sales and expanding margins in Q4 FY23, the company's EPS saw a markedly higher rise in the quarter than during the full year. The quarter saw an increase of 13% for both GAAP and Core EPS, currency-neutral EPS actually rose by a significant 22%. For the full year, by comparison, there was a muted 2% rise in both GAAP and core EPS, on account of unchanged net earnings offset by a decline in the number of shares outstanding because of share buybacks earlier in the year.

Positive outlook

P&G's outlook for FY24 is largely positive. On the positive side, it expects GAAP sales to rise by 3-4%, as the foreign exchange blow softens from FY23. But organic sales are expected to slow down to 4-5%, which is imaginable considering the cooling off in inflation and the smaller likelihood of a passing of costs therefore.

At the same time, it expects diluted EPS to increase by 6-9%. Again, with the current inflation trends, this isn't hard to imagine. In my recent article on its peer company Unilever ( UL ), I pointed to the gap between producer prices and consumer prices as an indication of a future rise in margins. P&G itself also mentions a "…net benefit of around $400 million after-tax from favorable commodity costs net of unfavorable foreign exchange." And this is already becoming visible, with margin expansion in Q4 2022.

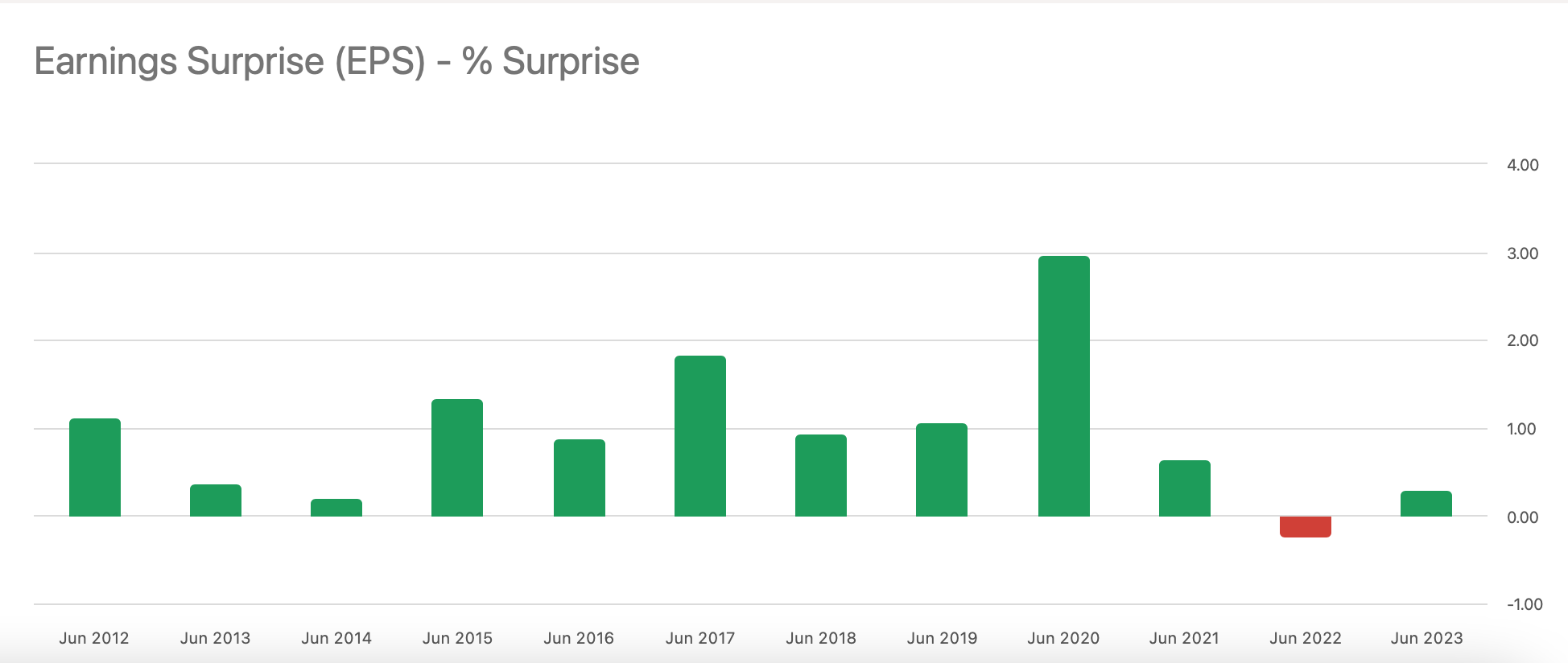

The company estimates diluted EPS to come in between USD $6.25 to USD $6.43 in FY24. Based on the above inflation discussion, I wouldn't be surprised by an upside to this. Note that analysts already expect EPS to be at USD $6.4 for the year, which is at the high end of the range. And P&G's earnings have surprised on the upside in 9 of the last 10 years (see chart below).

{kind=link}

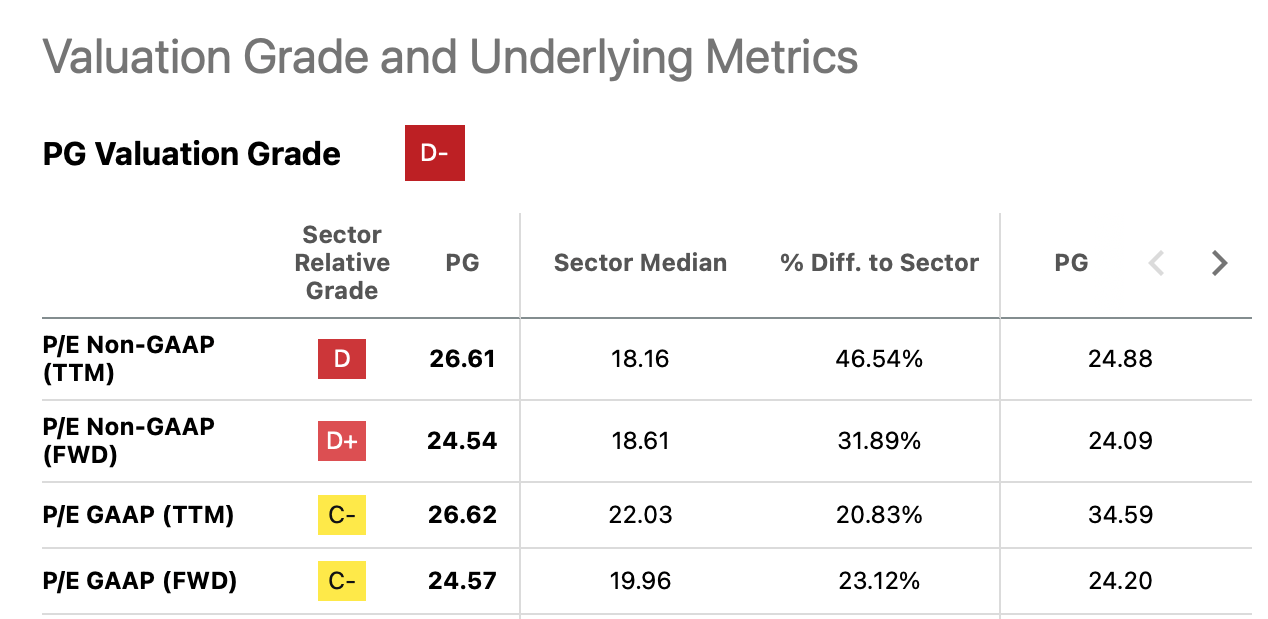

What the market multiples say

However, the increase in earnings already seems to be priced in considering that the forward price-to-earnings (P/E) ratio is already a shade higher than the five-year average ratio (see table below). For that matter, so is the trailing twelve months [TTM] non-GAAP P/E ratio.

Note: The rightmost column represents the 5-year average ratio (Source: Seeking Alpha)

{kind=link}

Only the TTM GAAP P/E ratio is lower, but GAAP earnings are susceptible to variations that aren't indicative of the underlying business. So I'd de-emphasize it for now. Essentially, the stock is fairly valued considering only the price returns.

Dividends and long-term returns

However, there are dividends to consider too. At 2.4%, the TTM dividend yield isn't particularly attractive, but it adds up going by the consistency with which P&G pays them. Over the last 10 years, price returns have been at 96%, while total returns rise to 162%.

I also want to point out its healthy 93.5% returns over the past five years, which outstrip the S&P 500 ( SP500 ), which has seen a 58% increase over this time. 2023 hasn't been P&G's year, with just a 3.6% rise so far, but the longer-term returns are worth bearing in mind. This is especially so considering it has a beta value of 0.6, which makes it less volatile than the overall markets.

What next?

To go back to the original question then, it doesn't look like the price is likely to rise significantly for now, despite healthy results. Even if FY23's figures are somewhat muted, Q4 FY23 shows promise in terms of sales growth, margin expansion, and EPS increase. The company's outlook is also positive, and with inflation trends favoring producers right now, its profits can particularly look good this year.

However, The Procter & Gamble Company stock is fairly valued, and going by its muted share price momentum this year, there really isn't a case to Buy it. At the same time, I reckon if the markets were to get uncertain, this defensive stock, with a low beta value and predictable dividends would look quite a bit more attractive. So I'll go with a Hold for now, but all else remaining the same, I'd change to a Buy if the broader market weakens for good reason.

For further details see:

Procter & Gamble: Earnings Growth Seen In FY24, But Fairly Valued For Now