HBM - Profit From Cyclic Copper With Hudbay Minerals

2024-01-04 07:56:34 ET

Summary

- Analysis recommends a "Hold" rating for Hudbay Minerals stock.

- Hudbay Minerals' share price is primarily influenced by copper production and the volatility of copper prices.

- The company's profitability is expected to improve with the projected upward trend in copper prices.

For Hudbay Minerals, This Analysis Recommends a "Hold" Rating Until Further Notice

This analysis recommends maintaining a Hold rating on Hudbay Minerals (HBM) stock for now.

Hudbay Minerals is a mining company based in Toronto, Canada, but is diversified as its production in the Americas includes copper, mainly, but also other metals such as gold, silver, zinc, and molybdenum.

The main field of activity is the mining, development, and exploration of copper deposits and is virtually the source of income for Hudbay Minerals. For this reason, Hudbay Minerals' share price depends primarily on copper production and the volatility of the copper price in commodity markets.

This analysis confirms the "Hold" rating given to Hudbay Minerals in the previous article . The retail investor was suggested to own shares of Copper Mountain Mining Corporation as they looked well-positioned to benefit from the rosy outlook for copper prices. It was noted that the company was on track to benefit from certain work to optimize operational activities and from the easing of inflationary pressures. The positive effect was expected to be an increase in production and cost improvements.

Hold Shares of Hudbay Minerals, but Not for too Long: Keep an Eye on Copper Cycles

First, let's say what Hudbay Minerals stock is not: Based on the performance of the past few years, it can be concluded that there is no point in buying shares of this copper stock and holding them for a long period.

The price of copper has performed robustly over the past five years, driven by expectations of a significant increase in copper-based applications in green projects and electrification around the world.

{kind=link}

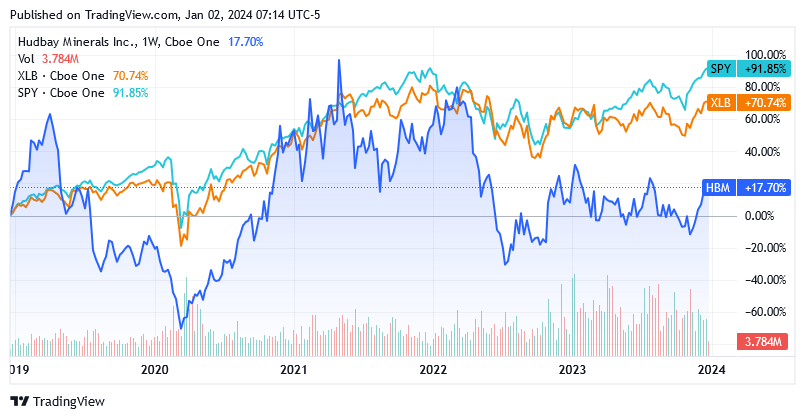

However, the same was not reflected in Hudbay's share price as this stock lost competition against the copper price, the general US stock market, and the basic materials sector.

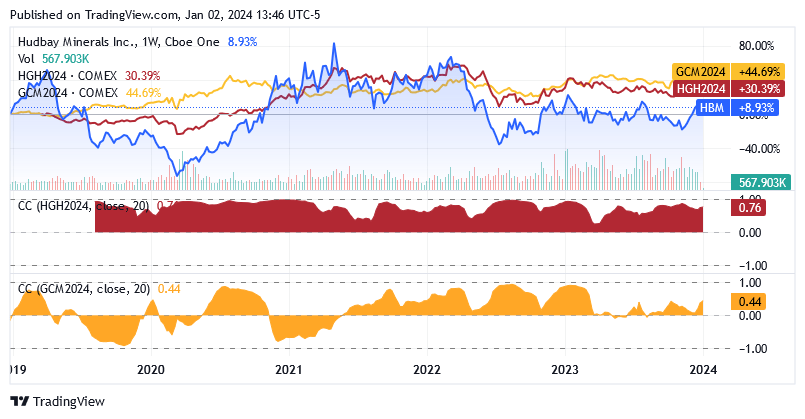

As a benchmark for the price of the commodity, the price of Copper Futures - March 24 (HGH4) has grown 30.39% over the past 5 years. As a benchmark for the US stock market, the market value of SPDR® S&P 500 ETF Trust ( SPY ) has grown 91.85%, and as a benchmark for the basic materials sector, the market value of Materials Select Sector SPDR® Fund ETF ( XLB ) has grown 70.74%. Against this backdrop of generally robust growth in the market value of U.S.-listed securities, shares of Hudbay Minerals under the symbol HBM experienced a modest increase of 17.7% over the past five years.

{kind=link}

This stock did not justify a "Buy and Hold" investment strategy from the perspective of the semi-annual dividend either.

Not only is the dividend a very small amount of only CA$0.01/share every six months, but it has not even increased over the past 13 years, though paid continuously to shareholders.

{kind=link}

Instead, Hudbay Minerals is primarily a stock that can benefit from copper price cycles, with which HBM appears to have a strong positive correlation. The following graph shows that the price of HBM's shares, and the price of copper futures are positively correlated. This suggests that when the shares are affected by bullish sentiment, copper futures are also bullish, while when sentiment is bearish for the shares of Hudbay, the same negative sentiment is most likely affecting copper futures as well. If the securities had been negatively correlated, then if one had been bearish, the other would most likely have been bullish and vice versa, but this type of relationship was not the case with Hudbay and copper futures.

{kind=link}

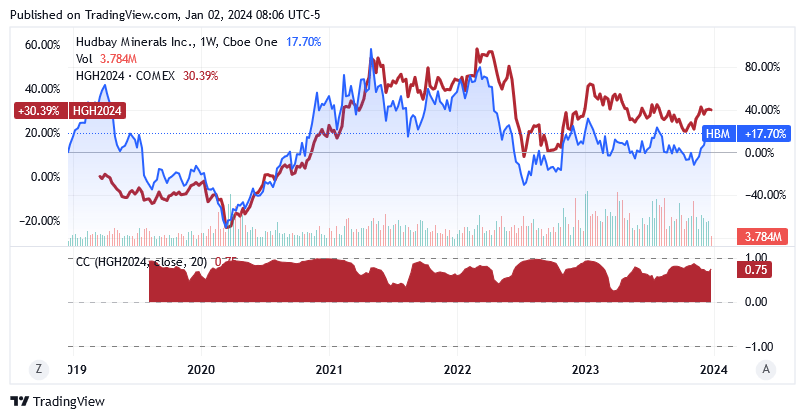

While the securities had different return margins, this aspect is alien to the concept of correlation: two securities can be correlated over time, regardless of their performance. The positive correlation is also very strong, as the red area at the bottom of the chart has never been in negative territory in the last 5 years, but always above the zero line.

This type of relationship implies that Hudbay's shares should generally follow suit given the projected upward trend in copper prices in the coming months.

The Short-Term Outlook for Copper Prices

Copper prices were at $3.875 per pound at the time of writing, slightly above the average price of $3.864 in 2023. Copper prices rebounded from 2022 levels, with the latter weighed down by the Federal Reserve's tight interest rate policy to combat elevated inflation. Higher financial costs coupled with a rapid rise in the prices of goods and services did not bode well for the consumption outlook for the red metal as it is used to produce almost all types of goods that people use daily. After a difficult 2022, copper prices received some support in 2023 from analysts' view that the economy will experience a soft landing, as well as expectations that the Federal Reserve will begin cutting interest rates sometime in 2024 as the inflation continues to cool. Lower interest rates tend to have a positive impact on economic activity, including copper consumption as well as investments in infrastructure and projects to make the economy sustainable from an environmental perspective through the electrification of human activities (e.g. the introduction of electric furnaces in metallurgy and electric vehicles in transportation). Therefore, analysts at Trading Economics expect the price of copper to be around $4/pound by the end of the first quarter of 2024 and around $4.2/pound in 12 months.

The expected increase in copper prices will be accompanied by progress in Hudbay Minerals' copper production and copper costs, and these two factors should lead to an improvement in profitability, which usually acts as an upward catalyst for the stock price.

The latter will potentially result in higher market values than current ones, supporting the recommendation to Hold the shares now and benefit from further upside in the ongoing upswing. Despite the rosy near-term outlook, stocks don't deserve a recommendation rating better than Hold because of the following: At current levels, shares are not a buy as they do not appear attractively valued compared to recent trends. The comparison implies the likelihood of a significantly smaller return margin than if they were much lower in the price cycle. Buying the shares at current prices would be even less justified if the transaction involved holding the shares for a long period of time, since, as shown above, on average they tend to underperform the market and industry over the long term.

Stock Valuation: There Doesn't Appear to be Much Room Left Until the Peak of the Cycle

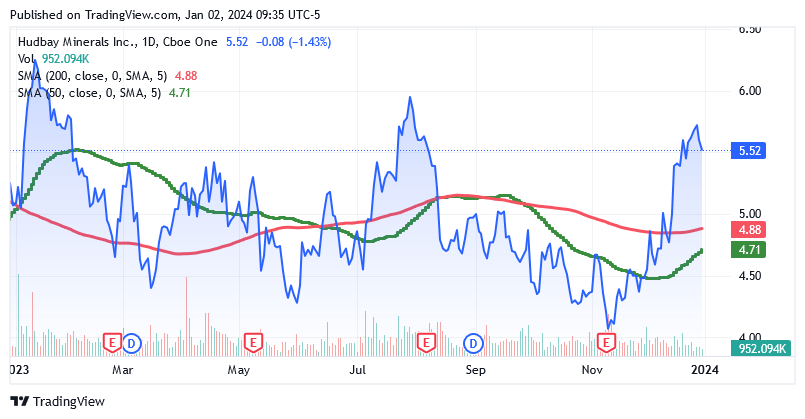

According to the chart below, shares were trading well above recent trends: Shares were trading at $5.52 per unit, giving it a market cap of $1.92 billion, and they were above the 200 simple moving average of $4.88 and the 50-SMA of $4.71.

{kind=link}

Even compared to the 52-week range of $3.94 to $6.34, current shares are well above the interval's midpoint of $5.14.

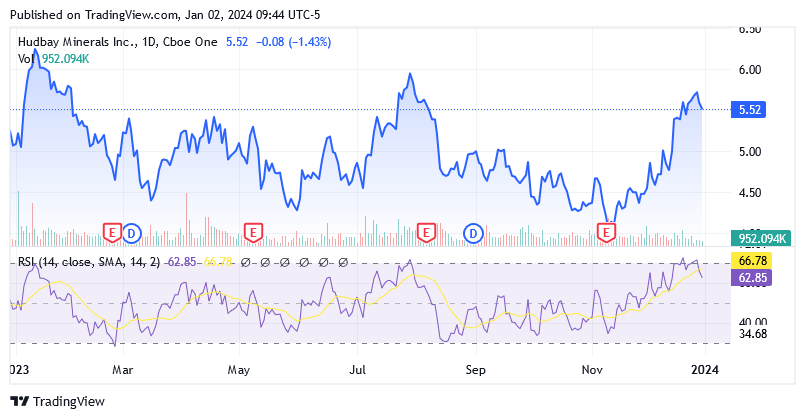

The 14-day Relative Strength Indicator is at 62.85 indicating that shares are neither oversold nor overbought at the time of writing, but it also indicates that the scope for further growth during the ongoing rally in the copper price is no longer as large as it was a few months ago.

{kind=link}

If retail investors were to buy the shares now, these levels would not allow for a sufficient gain before the current driving force of the copper price rise loses steam. Although analysts at Trading Economics predict a higher price for the copper pound in the coming months, the rise will not be stable but cyclical and the downward phase will be fueled by fears of the economy slipping into recession. These concerns will inevitably create headwinds for US-listed stocks and given the 24-month market beta of 2.10x (on this Seeking Alpha page , scroll down to the "Risk section" to find the information), retail investors can also expect strong downward pressure on Hudbay Minerals shares, fueling the share price's downward phase.

This analysis assumes that a Fed rate cut, which will instead have a positive impact on copper and Hudbay Minerals shares, should occur not at the next meeting in January, but at the follow-up meeting scheduled for March 20 . However, the market will begin incorporating the event into securities prices several days in advance. The current month should also provide a tailwind for copper and US equity markets, as the Christmas shopping season will once again have a positive impact on consumers' assessment of the economic outlook, following the positive assessment in December 2023 of current business and labor market sentiment and the six-month outlook for income, business, and labor market conditions.

However, these positive effects will not last beyond January as the economy ultimately continues to suffer from high financial costs and increased core inflation, and companies are aware of this when considering future sales estimates and current corporate investment trends.

Bear Market from Recessionary Issues Between mid-January and mid-February

Recession is supported by the following negative trends in consumption, investment, and soon also in the labor market.

As a strong benchmark, these top retailers reported lower year-over-year sales in the third quarter of 2023 and offered a generally dismal sales outlook: Best Buy Co., Inc. (BBY), Burlington Stores , Inc. (BURL), and DICK'S Sporting Goods (DKS). Also, Kohl's Corporation (KSS), Nordstrom , Inc. (JWN), and Lowe's Companies, Inc. (LOW). Nike (NKE) also spooked investors in the week before Christmas 2023 when management warned of near-term revenue growth, sending ripples through consumer discretionary stocks. Additionally, Walmart's (WMT) integration of Affirm's (AFRM) "buy-now, pay-later" technology into its self-checkout lines also signals weaker near-term sales growth and therefore trying not to miss even one of those sales that in smaller numbers are predicted to come in. The technology is designed to mitigate the effects of a last-minute change that could cause the customer to drift away just a few steps before completing the order. This risk is higher now that US household finances are under pressure from slow wage growth, elevated core inflation, the return of the repayment of student debt, and expensive credit card interest rates. Weaker demand is expected in the near future due to the gloomy sales outlook. Due to the very high cost of financing, companies have little incentive for investment activities, as these require the purchase of expensive capital. One trend in this sense is that the number and value of initial public offerings (IPOs) in 2023 were still significantly muted compared to deals made in 2021. While these trends are far from reassuring in terms of growth in the short term, they reflect a much broader sentiment that includes more companies and sectors of the economy. Companies are now considering job cuts to adapt operational capacity to changing demand conditions as a measure to defend profit margins. Otherwise, analysts would not predict robust profit margins in the current economic scenario.

With the labor market also showing signs of damage caused by the factors described above, consistent with Andrew Challenger (labor expert and senior vice president of Challenger, Gray & Christmas, Inc.) who expect more layoffs to continue this year as well, the tailwinds of the recession will be more noticeable in US-listed stocks and Hudbay Minerals shares. The inverted yield curve predictor of the spread between the 10-year Treasury yield and the 3-month Treasury yield also signals an impending recession. Currently, the 10-year yield is 3.935% versus a 3-month yield of 5.376% compared to a normal situation where the spread should be positive. This signals that investors have little confidence in the economy and, in this context, in particular in the ability of borrowers to pay when the loan expires. Lenders are demanding significantly higher repayments than before to compensate for the borrowers' increased risk of insolvency.

This analysis assumes that Hudbay's share price could fall significantly between mid-January and mid-February before the company reports full-year 2023 earnings results after market close on Thursday, February 22. Around this time, a new uptrend in Hudbay Minerals' share price is likely as strong earnings and cash flow results are expected to continue due to disciplined capital allocation in the growth project, while copper prices remain robust thanks to support measures from the Chinese government.

Hudbay Minerals' Activities Increase Production and Somewhat Reduce Costs

Hudbay Minerals' investments in metal mineral projects currently enable production at the Constancia mine in Cusco (Peru), the Snow Lake mineral operations in Manitoba (Canada) and the Copper Mountain mine in British Columbia (Canada). The latter asset was added to the company's portfolio through acquisition in early summer 2023.

Hudbay Minerals' profitability metrics benefit from positive metal ore grade trends at the Pampacancha deposit in Peru and the Lalor mine in Manitoba, as well as the inclusion of Copper Mountain, resulting in copper production increasing 93% sequentially and 71.3% year-over-year to 41,964 tons in the third quarter of 2023 .

Note that Hudbay also produces gold at its mines and these mines are leveraging the same operational improvements and collectively achieved a 107% quarter-on-quarter and 90.7% year-over-year increase to 101,417 ounces of gold in Q3-2023.

Hudbay Minerals also produces silver (up 74% sequentially and 48.2% yoy to 1,063,032 ounces), zinc (up 17.5% sequentially and 5.5% yoy to 10,291 metric tons), and some molybdenum.

However, based on the analysis of the correlation coefficient represented by the red area for copper and the yellow area for gold, it can be concluded that Hudbay Minerals' stock price is much more anchored in copper than in precious metals.

{kind=link}

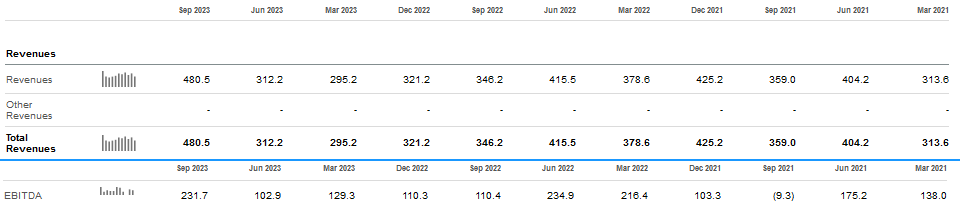

This situation is reflected in the fact that the company's profitability depends to a greater percentage on the copper business than on the gold business: the company sold 39,371 tons of copper (about 86.8 million pounds) and 74,799 ounces of gold, while the prices of copper and gold averaged at $3.7965 per pound and $1,949.30/oz respectively. Thus, in the third quarter of 2023, copper accounted for almost 70% of the total revenue of $480.5 million, while gold accounted for 30%.

The increase in production is cost-effective as it offsets higher milling and throughput costs and other costs associated with incorporating the Copper Mountain mine into its portfolio of mineral activities: consolidated cash costs per pound of copper went down 31.3% sequentially (net of by-product credits) to $1.10 in the third quarter of 2023 though still 89.7% higher on year over year basis. Consolidated sustainable cash costs per pound of copper produced, net of byproduct credits, decreased 11.2% sequentially and decreased 1.1% to $1.89 in the third quarter of 2023.

Consolidated total sustainable cash costs per pound of copper produced, net of by-product credits, decreased 31.5% sequentially and decreased 5.6% year-over-year to $2.04 in the third quarter of 2023.

Higher production and robust pricing resulted in third quarter cash flow from operating activities increasing 225% sequentially and 122% year-over-year to $182 million in Q3-2023.

The Financial Situation is not Particularly Solid, but the Company Reduces Debt and Spending on Current and Future Assets

The increase in cash flow was used to improve cash balances and short-term investments of $246.5 million (up from $225.7 million as of December 30, 2022 ). Combined with $294.4 million in undrawn funds available in revolving lines of credit, total liquidity amounted to $539.6 million as of September 30, 2023. Instead, total debt (including the current portion of debt) increased from $1.25 billion to $1.48 billion, resulting in net debt of $1.24 billion as of September 30, 2023, versus net debt of $1.02 billion as of December 30, 2022. On a 12-month basis, operating income of $196.2 million versus interest expense of $75.9 million results in an interest coverage ratio of 2.58, meaning Hudbay Minerals has no issues paying interest expense on the outstanding debt, but the Altman Z-Score value of 0.64x indicates that the balance sheet is in a distress zone, meaning that there is a risk of bankruptcy within a few years. For the Altman Z-Score, scroll down this Seeking Alpha page to the "Risk" section. The company believes the balance sheet is strong enough to support higher production initiatives in Peru and Canada working on improvements in mineral quality, processing facilities, and extraction. For the full year 2023, the company targets to produce 118,500 to 148,500 tons of copper; 266,000 to 323,000 ounces of gold; 3.15 million to 3.86 million ounces of silver; 28,000 to 36,000 tons of zinc; and 1,300 to 1,600 tons of molybdenum. The cash cost will be in the range of $0.80 to $1.10/lb, while the sustaining cash cost will be in the range of $1.80 to $2.25/lb. Also, the company is allocating financial resources to the two primary growth projects of Copper Mountain operations in British Columbia and Copper World's Phase I pre-feasibility study in Arizona. Copper Mountain is focused on activities to expand the mining fleet, accelerate mining, and increase mill plant reliability, while Copper World will produce 92,000 tonnes of copper per year for the first 10 years of the total mine life of 20 years after the receipt of two operating permits early in the current year. In addition to the funds the company plans to provide to maintain and expand operations in British Columbia, which will amount to approximately $35 million for the full year 2023, Hudbay Minerals will provide $270 million for supporting and growing operations in Canada and Peru. This will be below the past five-year average of $307 million, in line with its deleveraging strategy.

Hudbay Minerals' Operations have Reached a Turning Point

Adjusted earnings were $0.07 per share for a positive change compared to a loss of $0.07/share in Q2-2023 and versus a loss of $0.05/share in the third quarter of 2022.

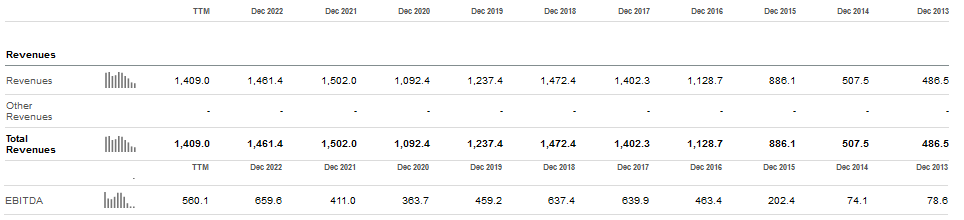

Adjusted EBITDA improved from $81.2 million in the second quarter of 2023 to $190.7 million in the third quarter of 2023 and from $99.3 million in the third quarter of 2022, which also improved the adjusted EBITDA margin as follows: by 1,370 basis points sequentially and by 1,100 basis points year-on-year to 39.7% in the third quarter of 2023.

Unlike fixed-income securities such as U.S. bonds, U.S.-listed stocks feature variable income. While the market value of bonds depends on interest rates, the value of U.S.-listed stocks is a function of earnings, which fluctuate over time.

This also applies to the shares of Hudbay Minerals. However, since the company is a metal mining stock, EBITDA margin is the primary driver of stock price in the US market, as in a capital-intensive industry it is the profitability metric that the stock market ultimately follows most closely.

In fact, following the release of Q3 results on November 9, 2023, Hudbay Minerals shares saw a strong recovery from the 52-week low of $3.94 on November 10, 2023, driving the share price up 40%. On top of this, tailwinds from additional Chinese government bond issuance and an increase in the budget deficit ratio as support measures to improve the outlook for metal demand may also have influenced the recovery in the stock price. After all, the news was about the world's largest consumer of refined copper, causing a shock in copper prices, which suddenly changed course from a 52-week low of $3.5195 on October 22, 2023. Copper prices have recovered more than 10% at the time of writing, which in light of the strong positive correlation, Hudbay Minerals stock must have been helped enormously.

Peter Kukielski, President and Chief Executive Officer, speaks of a turning point in terms of operational and profitability progress:

"We delivered on our plan for significantly higher production, revenue and cash flow in the third quarter, marking an inflection point as we generate strong returns from our recent brownfield and growth investments across the business,"

But it must be said that the positive impact of the strong recovery in copper prices is undeniable and that the third quarter of 2023 was not exceptional in terms of EBITDA margin improvement. The EBITDA margin has historically been at the forefront of corporate profitability, peaking at over 45% both post- and pre-COVID.

Hudbay Minerals Inc. quarterly EBITDA margin (EBITDA/revenues) for the last 11 quarters:

{kind=link}

Annual EBITDA margin (EBITDA/revenues) of Hudbay Minerals Inc. for the last 11 years:

{kind=link}

While the share price throughout the period was characterized by both ups and downs. This is the type of market for Hudbay Minerals shares when these are purchased and held in the portfolio for the long term.

{kind=link}

A rating higher than "Hold" for Hudbay Minerals stock at current levels (not even the most attractive) implies significant investment risk, which is also exposed to a volatile context like the present one.

So while waiting for the market to prove with facts that the turning point for Hudbay Minerals shares has been reached, the most reasonable investment strategy for the retail investor is to stick with the 'Hold' rating for the time being, which, among other things, will support him in limiting the investment risk.

A 'Hold' rating allows the retail investor to continue to benefit from the ongoing upside due to positive copper price dynamics and, when it comes to softening the position, achieve a higher margin of return compared to the 'Buy' stance at current levels. As seen earlier, this analysis forecasts that profit-taking will occur between mid-January and mid-February 2024.

Then the entry point formed due to the bearish sentiment amid the profit-taking could potentially also serve to strengthen the position for a long-term investment horizon, but only on the condition that the dips are significant compared to the previous ones.

The stock is characterized by a good trading volume: an average of 2.04 million shares were traded on the stock exchange in the past three months (on this Seeking Alpha page , scroll down to the "Trading Data section" to find the information). The stock has 348.76 million shares outstanding, of which 88.8% are the float and 63.54% of the float is held by institutions .

The same consideration can broadly apply to the shares traded in the Canadian market in Toronto.

Shares also trade on the Toronto Stock Exchange under the symbol ( HBM:CA ). Shares were trading at CA$7.19 per unit on the TSX as of this writing for a market cap of CA$2.55 billion. Shares are trading above the 200-day simple moving average of CA$ 6.58, and above the 50-day simple moving average of CA$ 6.42.

Shares are also above the middle point of CA$ 6.965 in the 52 52-week range of CA$ 5.46 to CA$ 8.47. Also, the 14-day Relative Strength Indicator of 57.35 suggests that shares are much closer to overbought levels than oversold levels.

Hudbay Minerals offers a dividend yield (forward) of 0.28%, as of this writing.

Over the past 3 months, an average of 1.11 million shares were traded.

Conclusion

Retail investors should Hold shares of Hudbay Minerals to continue benefiting from robust copper prices thanks to Chinese support measures and improving operational activities.

Shares are not far from reaching the peak of the cycle. Between mid-January and mid-February, given the headwinds of the expected recession, investors should consider taking some profits.

Hudbay Minerals is not suitable for a long-term investment horizon as the stock tends to underperform the stock market and sector, plus the dividend payment is low. Owning shares in Hudbay Minerals involves significant investment risk, which the retail investor may wish to offset by taking advantage of copper price cycles and increasing holdings whenever the share price declines significantly.

The stock market must now reflect the inflation point that the company claims to have reached. The company continues to deleverage because the balance sheet doesn't really look like a fortress.

For further details see:

Profit From Cyclic Copper With Hudbay Minerals