PRGS - Progress Software: A Shelter Company For Difficult Times

2023-09-26 23:27:42 ET

Summary

- Progress Software specializes in developing software products and platforms for businesses.

- Around 70% of the income comes from the maintenance of the developed software, which provides recurring revenue and high gross margins.

- Despite being at all-time highs, PRGS expects excellent growth this year, so the valuation could provide a return of 15% annually in the next 5 years.

Investment Thesis

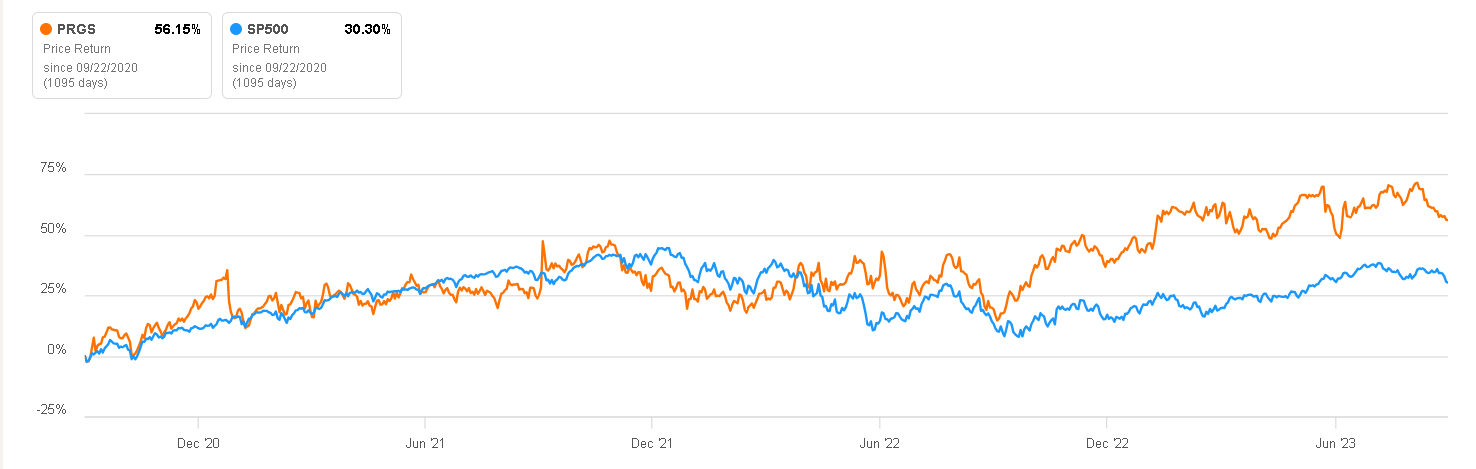

When we think of safe haven companies, we normally associate the consumer staples and healthcare sectors, however, Progress Software Corporation ( PRGS ) has proven to behave stable and better than the S&P500 index when there are times of bear market, such as in the last year.

Despite being in the technology sector, Progress's business enjoys highly recurring revenue from software maintenance, which is also stable thanks to its high customer retention rate. All this means that it is a business that is resistant to crises due to its maintenance services, but also that it has growth thanks to the digitalization that the economy is experiencing.

In this article, we will show its business model, the advantages it has, and I will share the valuation that made me decide on a buy rating.

Price vs S&P500 (Seeking Alpha)

{kind=link}

Business Overview

Progress Software specializes in developing software products and platforms for businesses. The company provides a wide range of products and solutions, including application development tools, data connectivity and integration software, and digital experience and business process management software.

Progress Software is known for its flagship product, Progress OpenEdge, which is a development platform for building business applications. The company also offers other products like Telerik, a suite of developer tools, and DataDirect, a data connectivity and integration solution.

These tools can be highly useful for organizations that need to develop and maintain their own software solutions, especially in industries like finance, healthcare, and manufacturing, where they require specific software to analyze specific data and draw conclusions based on it. For example, healthcare organizations may benefit from tools that help them manage patient data securely and in compliance with regulations.

High Customer Retention

As we saw, for Progress clients these solutions are key to improving customer experiences, automating processes, and optimizing operations. This would explain the high recurrence in admissions and the low churn rate. At Investor Day in April 2023, management stated that the client retention rate is 100%, that is, its clients rarely abandon Progress services because once the software is developed, if maintenance or improvements, customers will only be able to go to the code developer.

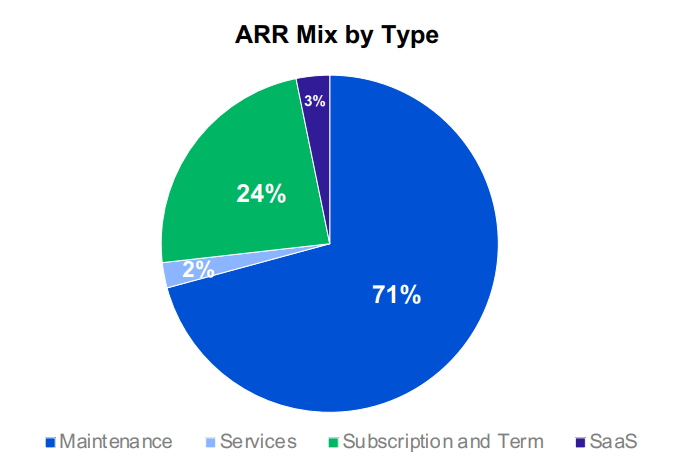

Currently, 71% of the income comes from the maintenance of the developed Software and the customer base is quite extensive and includes all kinds of blue-chip clients such as Meta, Microsoft, Caterpillar or S&P Global.

Progress Software Progress Client Base (Progress Software)

{kind=link}

{kind=link}

Key Ratios

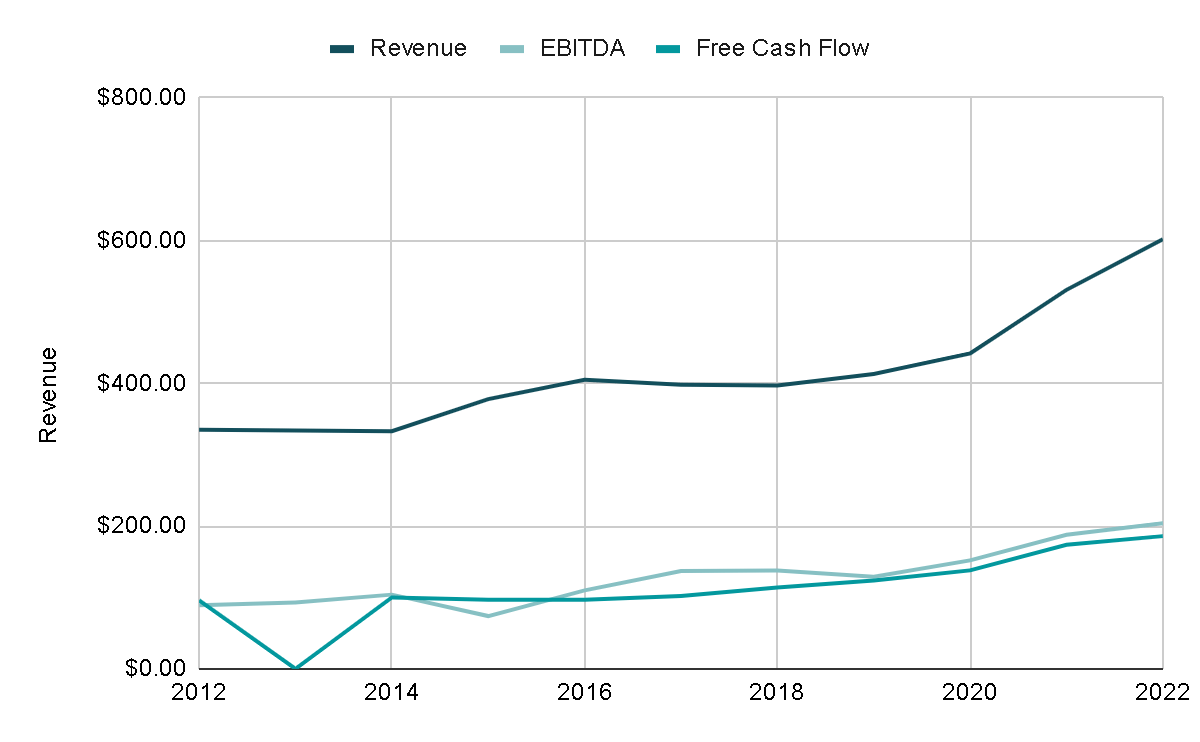

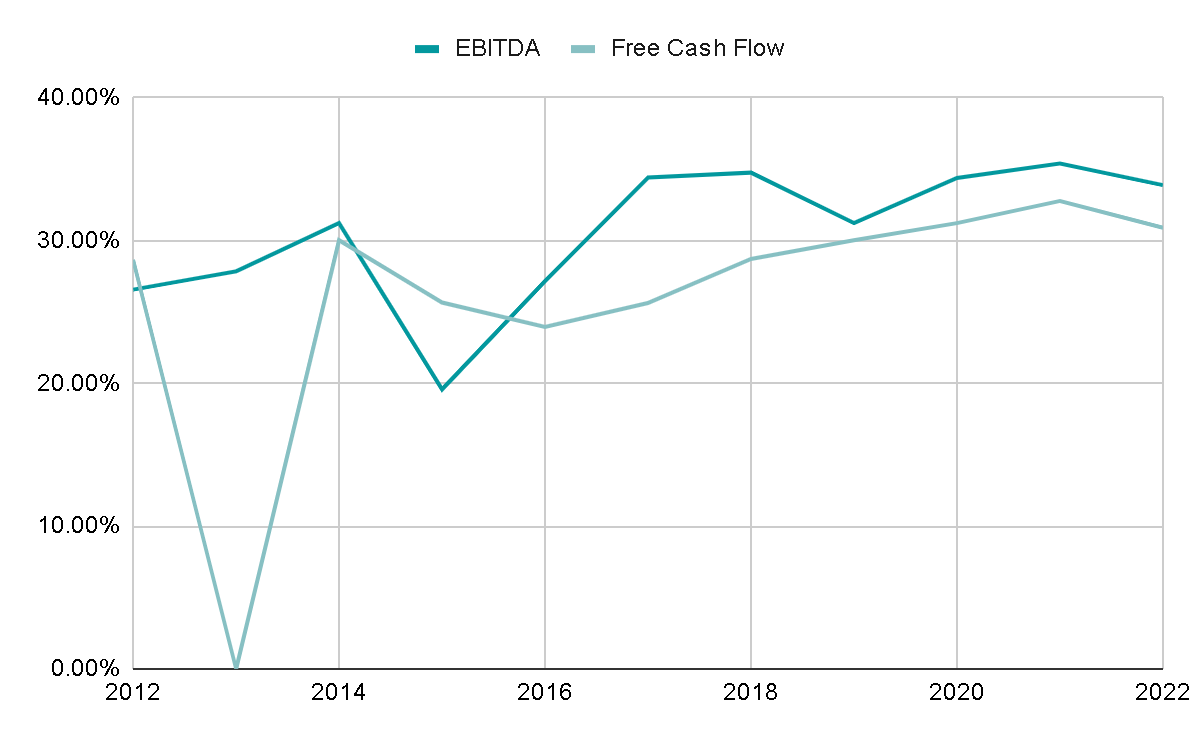

Revenue has grown 6% annually in the last decade, a growth rate quite similar to that of FCF and EBITDA. So we cannot consider Progress as a high-growth company by any means, but it is a fairly stable growth.

{kind=link}

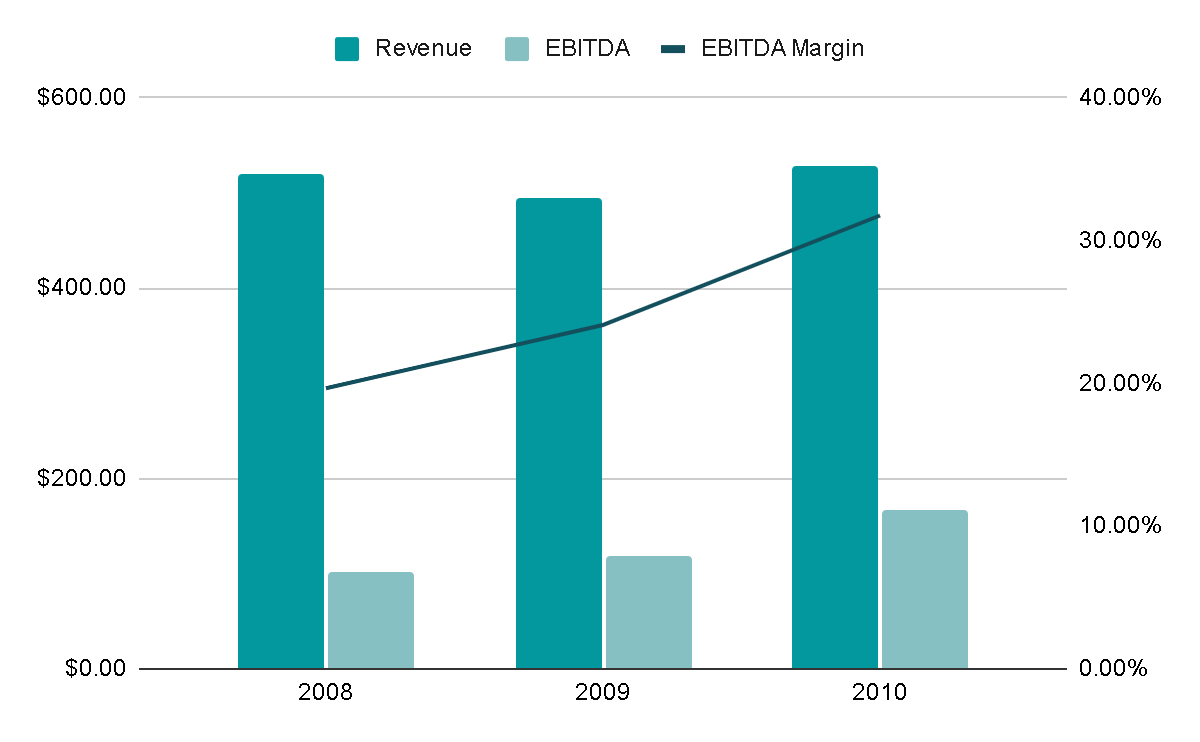

Even during the worst of the 2008 crisis, the company only decreased its revenue by 5% and quickly recovered it the following year, while the EBITDA margin was maintained and even grew.

{kind=link}

There has been an improvement in margins year after year thanks to the fact that once the software is developed, the maintenance charged has very high gross margins and only requires paying the technician or software developer to review and fix it.

{kind=link}

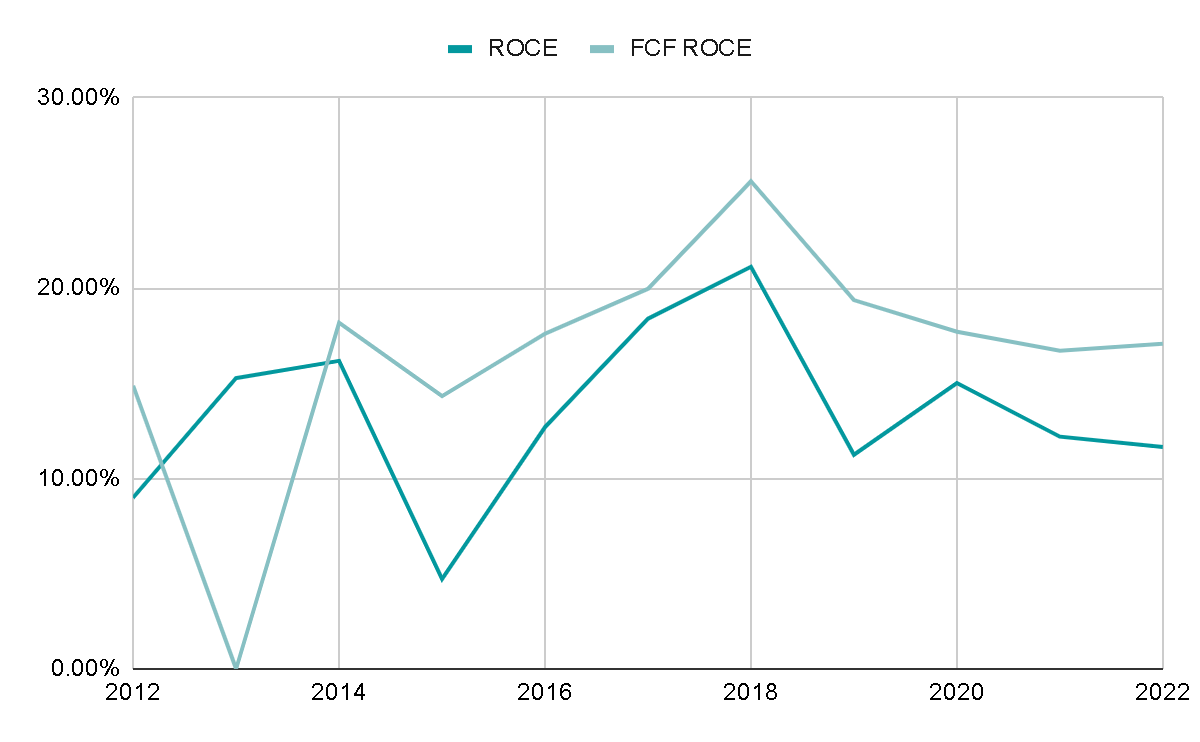

The returns on capital employed and free cash flow used are around 15%. This seems important to me because, as we will see later, most of the capital has been allocated to making acquisitions.

{kind=link}

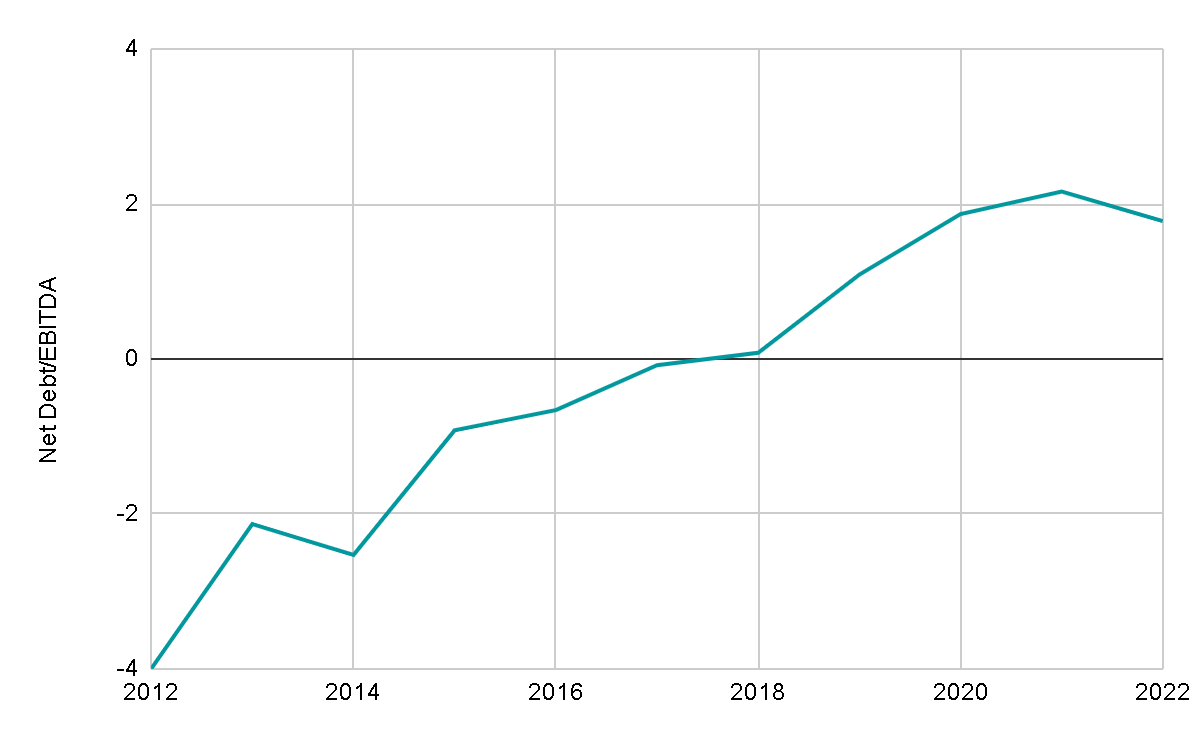

The Net Debt/EBITDA ratio is at levels of 1.8x if we consider the figures for FY2022, however, I find it somewhat worrying that it has been rising year after year in the last decade, especially in the current environment where interest rates have risen a lot and they are not fully represented in the 2022 annual report. As of November 30, 2022, the company had a total debt of $628M, which was distributed in $360M in Convertible Senior Notes with dates for 2026 and the remainder was in a Revolving Credit Facility of which $206M has a payment date for 2027. So, although The debt is high, it is also true that the important payment dates are 3 or 4 years away.

{kind=link}

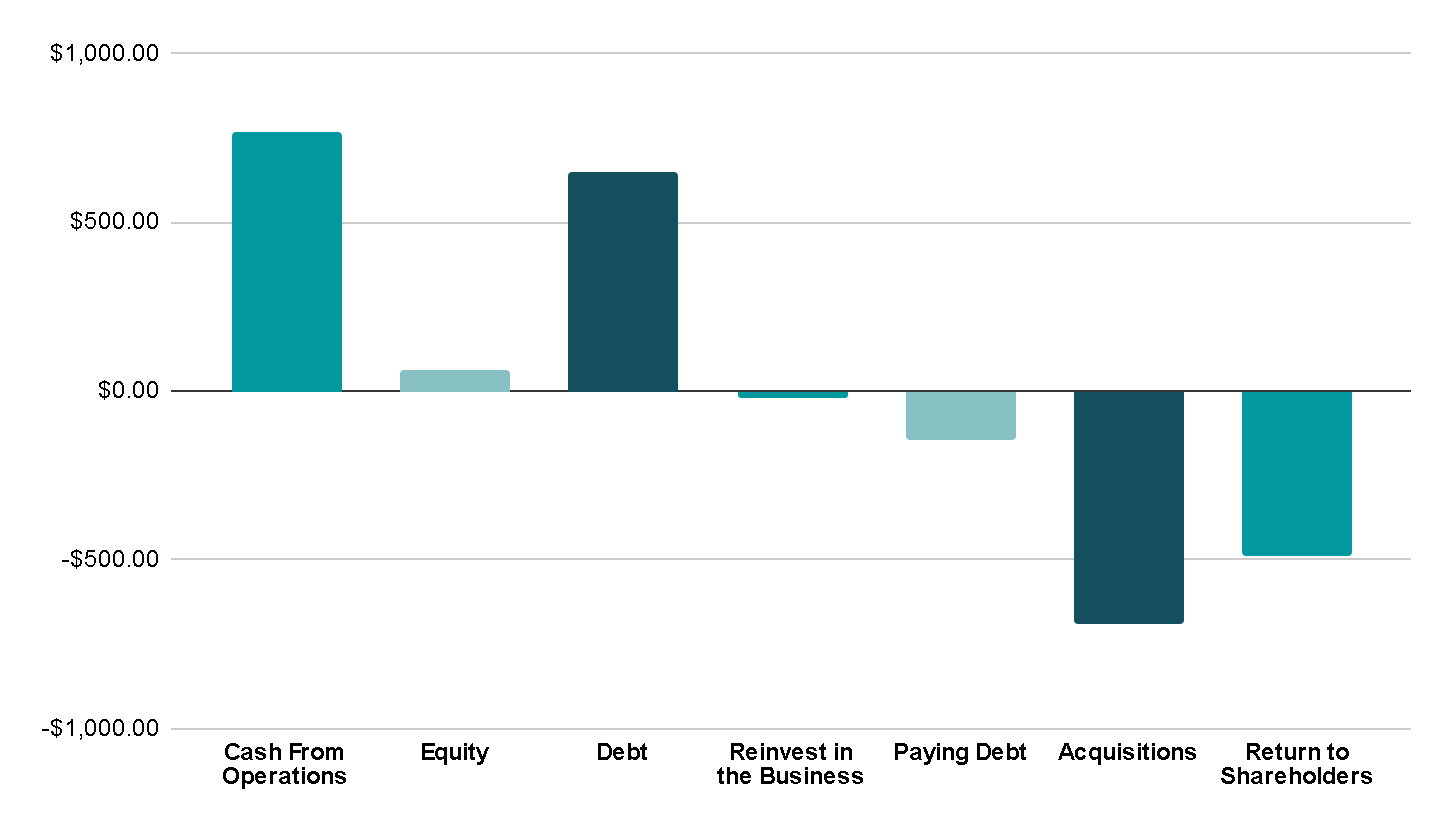

In the last 5 years, 52% of the capital has come from the company's own cash from operations, while another 44% has been financed by the debt mentioned above. This capital has been used largely to make acquisitions and to remunerate shareholders through buybacks and dividends.

I consider that the company is prudent since its target for acquisitions are companies that are already profitable, with good ROIC, with high recurring income, and whose sales represent between 10 and 25% of Progress's sales.

Regarding buybacks, in the last 5 years, they have repurchased an average of 1% of the shares annually. For dividends, the company has a healthy payout ratio of 38.6% of LTM net income and represents a modest dividend yield of 1.2%.

Debt Structure (Author's Representation)

{kind=link}

Valuation

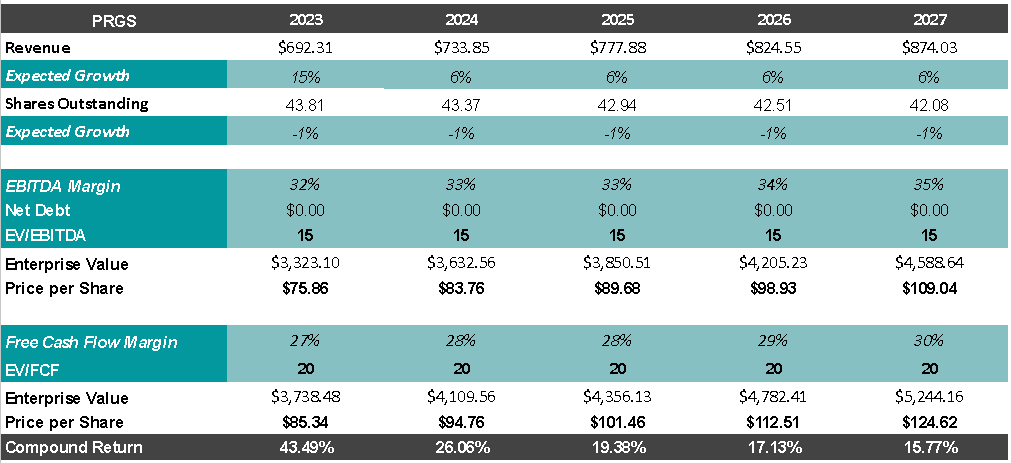

For the valuation, I will take into account management's guidance for this year, which expects a revenue growth of 15%. After this year, I will assume annual growth in line with the historical average of the last 10 years, which is 6% for revenue. The company typically buys back 1% of its shares annually, so I will also factor that into the valuation.

I believe that the margins, both EBITDA and Free Cash Flow, can reach approximately 35% and 30%, respectively. In fact, the company has achieved these margins in previous years, so it doesn't seem unlikely. Finally, I will consider exit multiples of 15x EBITDA and 20x FCF, based on the average of recent years. This makes sense given the high recurrence of revenues and the usual stability of the share price.

With these assumptions, we could anticipate a return of 15% per year from the current share price. This may appear unusual, considering that the company is currently trading at historical highs. However, it's worth noting that if management's guidance is met, the company would be trading at approximately 12x FCF, so the company would be somewhat cheap.

{kind=link}

Risks

Although I do not consider that there is an imminent risk for Progress, due to the competitive advantages that its business model has, I would like to mention some somewhat more general risks that could still affect the growth of the company if they materialize. These risks are the following:

Market Competition: Intense competition in the software industry is a significant risk. Progress Software competes with other established players, as well as emerging startups. Changes in market dynamics or the introduction of innovative technologies by competitors could impact Progress Software's market share and pricing power.

Technology Advancements: Rapid advancements in technology can quickly make existing software products and solutions obsolete. Progress Software needs to stay at the forefront of technology trends and continuously innovate to ensure its products remain relevant and competitive.

Economic and Market Conditions: Economic downturns or fluctuations in global and regional markets can affect software companies. Reduced IT budgets by businesses during economic hardships may lead to decreased software sales and licensing revenues, although this would be partially offset by the recurring income from maintenance that must be carried out no matter what.

Final Thoughts

As I mentioned at the beginning, we are dealing with a highly predictable business with little volatility, making it ideal for providing stability to a portfolio. In fact, its Beta is 0.9, and during the 2000 crisis, the most significant downturn for technology companies, its correction was 52% from peak to trough, while the NASDAQ index fell by 80% during that period.

Although it may not offer exciting growth, it is stable and sustainable over time. Moreover, it is not trading as expensively as it might appear initially, considering its LTM P/E ratio of 30x and the historical highs I mentioned earlier. Therefore, I would recommend a ' buy ' rating, although it's clear that a correction of 10% or 15% would make it even more attractive and a better opportunity.

For further details see:

Progress Software: A Shelter Company For Difficult Times