PRGS - Progress Software: A Software Roll-Up With Big Ambitions

2023-06-26 14:16:04 ET

Summary

- Progress Software’s resilient results and upbeat mid-term update have given investors plenty to be optimistic about.

- But replicating the success of the last five years won’t be as straightforward in a ‘higher for longer’ rate environment.

- The equity valuation isn’t particularly cheap here and could be vulnerable to P&L headwinds.

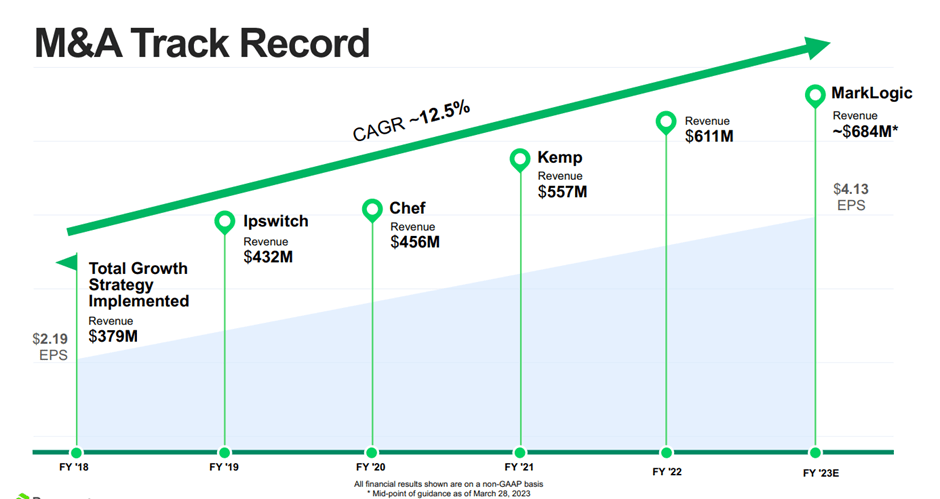

Infrastructure software rollup Progress Software ( PRGS ) has risen since I last covered the stock but largely lagged the software space amid broader macro concerns. Coming off an upbeat investor day outlining further M&A upside in the mid-term (MarkLogic being the most recent example of its roll-up strategy at work), management has done a great job drumming up investor optimism this year. Given its capital allocation track record in recent years, particularly in diversifying the business beyond its flagship OpenEdge platform, management deserves every bit of credit for making its inorganic growth strategy work. But the new financial targets (revenue and EPS to double in five years) are ambitious relative to near-term guidance for flat YoY EPS growth. With the company's net debt balance sheet also constraining its M&A capacity heading into a macro slowdown and higher cost of debt environment, I wouldn't be so quick to underwrite these estimates. Management hasn't penciled in any of PRGS' stock-based compensation (up >20% YoY) coming onto the P&L either, so there isn't much conservatism here. At the current mid to high-teens FCF multiple, PRGS isn't cheap and could still de-rate should IT budgets reset lower in the coming quarters. Taking all of this into account, I remain neutral heading into this week's earnings report.

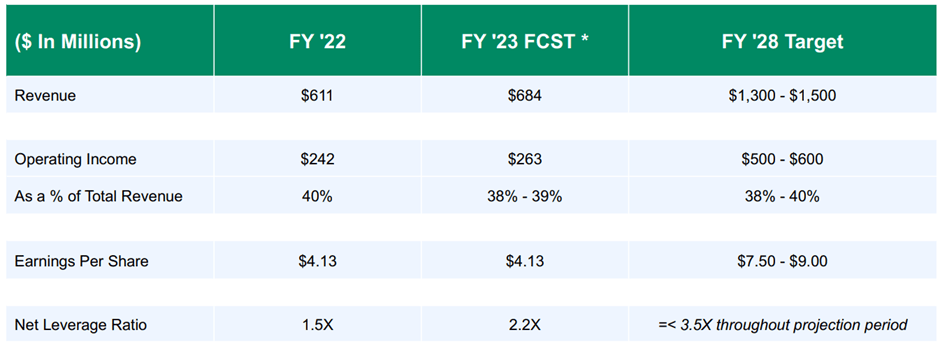

Mid-Term Targets Ambitious, Not a Lot of Buffer

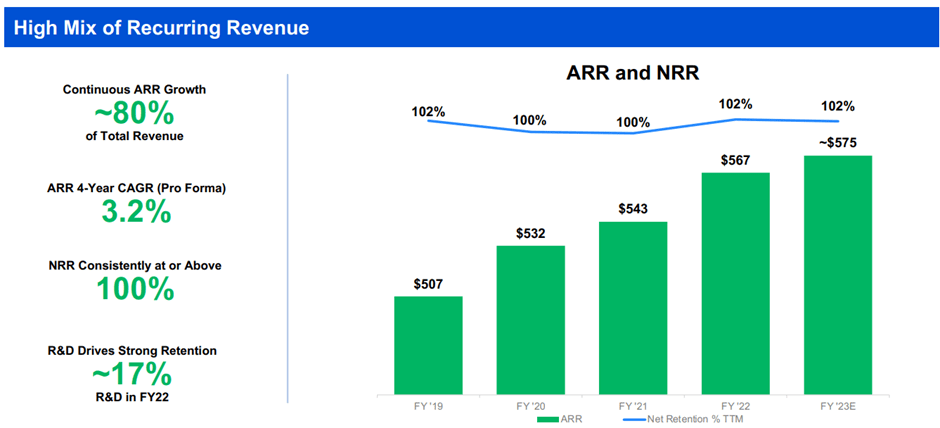

Coming off a robust Q1 2023 (albeit helped by some pull-forward demand), PRGS highlighted ambitious new 2028 financial targets of $1.3-$1.5bn revenue and $7.50-$9.00/share of EPS (+15% CAGR from FY23 guidance at the midpoints), implying a flat to slightly higher operating margin range of 38-40%. Management justified these estimates based on its solid five-year track record, headlined by a combination of >100% net retention rates - even through the challenging 2022 macro backdrop. Another key success has been its expanded recurring revenue base at >80% of total revenue, a testament to PRGS' resilient portfolio of assets. This comes despite diversifying the revenue mix - OpenEdge contribution is now down to ~40% of 2022 revenue (down from ~70%), offset by incremental revenue from acquisitions (poised to cross 40% post-integration of MarkLogic).

{kind=link}

Margins and cash flows have also benefited from the accretive portfolio rebalancing toward 'sticky' infrastructure software products. With the subscription and licensing revenue contribution still at a relatively low ~24%, there remains ample room for margin expansion as subscription-based product acquisitions like MarkLogic and DataDirect gain share. But managing costs will be key - the main expense burden is R&D (high-teens percentage of revenue), where continued product investments and innovation are needed to minimize churn. Sales & marketing expense is another big opex component that has grown at a relatively high pace, so any slowdown in revenue growth risks operating deleverage and downside to the margin target. Elsewhere, rising interest expense costs (some of the company's credit facilities now have a ~6% interest rate) and stock-based compensation (up >20% YoY and at a high-single-digit percentage of revenue) are concerns, particularly with the latter likely to hit the P&L in a 'higher for longer' rate environment. Post-synergy earnings upside from the MarkLogic integration adds some cushion, but ultimately, more synergistic M&A will be needed to fully offset the headwinds, in my view.

{kind=link}

Re-Deploying the M&A Playbook in a More Challenging Environment

Given the important role accretive M&A has played in building up the Progress Software portfolio thus far, it came as no surprise that management continued to emphasize acquisitions over buybacks, dividends, or debt paydown. The PRGS advantage is its institutional relationships, which gives the company an early view of potential opportunities (vs. competing corporate development teams), as well as its capital discipline. The latter has been particularly impressive, with the company sustaining a low-teens return profile in the last five years - well above the high-single-digit cost of capital. Running an ROIC>WACC model will be tougher, though, in a higher-rate environment, and I wouldn't be too quick to underwrite similar M&A success going forward.

Still, opportunities are abundant in the software space. DevOps/DevSecOps, for instance, is one of many fragmented categories, with a long list of platform vendors, multi-product vendors, and application vendors competing for the same pie. But shrinking tech budgets, a result of the weaker macro environment, has driven vendors into consolidation - recent M&A deals such as DataDog-Sqreen and JFrog-Vdoo are cases in point. Expect PRGS to participate at some point, though competition for deals will be stiff against bigger players (e.g., Amazon AWS ( AMZN ), Microsoft Azure ( MSFT ), and Atlassian ( TEAM )) with net cash balance sheets.

{kind=link}

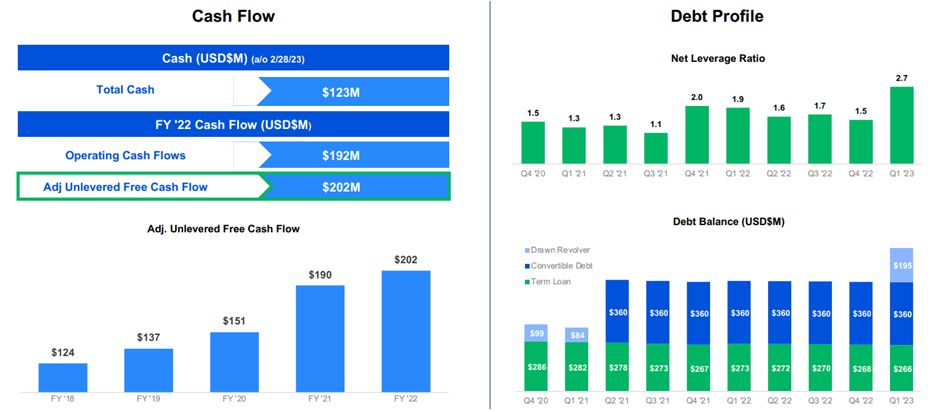

On the flip side, extracting cost-side acquisition synergies could be easier in a higher rate environment. For context, the PRGS playbook is to target software assets with flat to 20% operating margins pre-acquisition before unlocking synergies to get asset margins up to >40% within twelve months of acquisition close. The playbook is mainly focused on costs, so any revenue synergies would represent incremental upside. And given the strong track record through the years in replicating this playbook across software acquisitions, PRGS should have little trouble achieving its synergy targets over time. The key hurdle is balancing this with the M&A pace required to sustain a mid-teens percentage growth algorithm (implying doubling the revenue base in five years). Also challenging will be executing against the net leverage constraint - the 2.7x net debt to 2023 EBITDA ratio means the company is already close to its <3.5x limit, while higher debt costs will weigh on deal economics as well.

{kind=link}

A Software Roll-Up with Big Ambitions

Progress Software has reaped the benefits of its roll-up playbook over the last five years. Whether this tried-and-tested playbook can be replicated over the next five years is less certain, in my view. The recent Fed hikes have reset software valuations significantly, but PRGS' net debt balance sheet will prevent it from fully capitalizing. Yet, the mid-term target to double revenue while maintaining operating margins at 38-40% (implying a doubling of EPS as well) means PRGS doesn't have the luxury of slowing down its M&A pace. Also disappointing was the lack of a buffer for stock compensation, which will likely be replaced by P&L expenses in a downturn, or organic revenue headwinds (e.g., cuts in corporate IT budgets). While the stock deserves some premium for its outsized recurring revenue base, which enables defensive mechanisms through a downcycle, the current mid to high-teens FCF valuation embeds too much optimism for my liking.

For further details see:

Progress Software: A Software Roll-Up With Big Ambitions