PRGS - Progress Software: An Outlier In The Infrastructure Software Industry

2023-06-26 12:12:08 ET

Summary

- Progress Software offers a compelling investment opportunity due to its profitable business model, strategic M&A activity, and attractive valuation multiples.

- The company has a strong portfolio of sticky software products, robust financial performance, and a diverse customer base, including blue-chip companies.

- Progress Software's focus on inorganic growth, shareholder-friendly capital allocation, and product innovation positions it well for sustained growth in the software market.

Progress Software Corporation (PRGS) presents a compelling investment opportunity due to its profitable business model, strategic M&A activity, established portfolio of sticky infrastructure software products, and attractive current valuation multiples.

Furthermore, the company is led by an exceptional management team, particularly under CEO Yogesh Gupta. With over three decades of experience in the software industry, Gupta has been a driving force behind the company's total growth strategy, emphasizing an accretive M&A approach supplemented with share buybacks and dividends. Under his leadership, Progress has completed four acquisitions and expanded margins substantially.

Business Model

Progress Software operates a business model that provides products that empower customers to create, deploy, and manage vital business applications. The company's product offerings include application development platforms, relational database management systems, data connectivity software, and infrastructure automation tools.

{kind=link}

The company has an extensive user base, with its software products being utilized by over 3.5 million developers and 100,000 enterprise customers. More than 1,700 software companies and 6 million business users depend on Progress Software's applications to power their software solutions.

A significant characteristic of Progress Software's business model is its emphasis on recurring revenue, which primarily comes from maintenance contracts and the adoption of subscription-based models for both on-premise and cloud ((SAAS)) solutions. This model allows for reliable and durable revenues, leading to earnings growth.

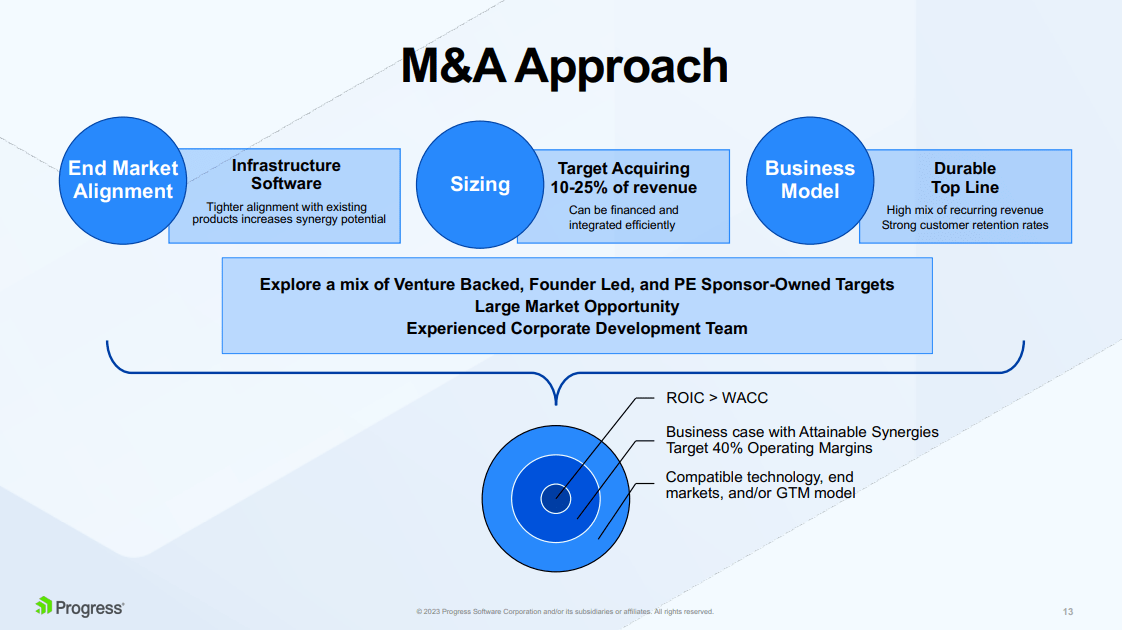

Furthermore, inorganic growth is integral to Progress Software's business model through an active M&A strategy. The company targets infrastructure software companies that generate under $100 million in revenue, have a high degree of recurring revenue, display strong retention metrics, and maintain sound operating margins. By integrating these acquisitions into its broader product portfolio, Progress Software aims to realize cost synergies, which in turn have the potential to elevate operating margins above its average of 40%.

2023 Progress Software Investor Day Presentation

{kind=link}

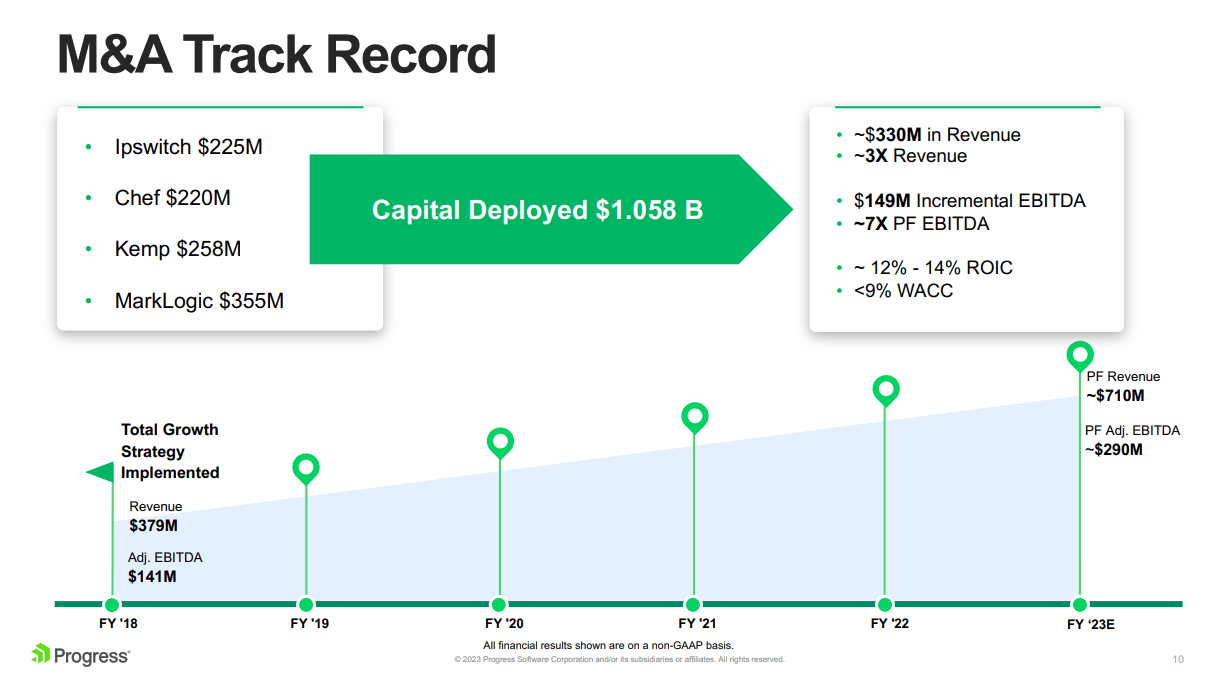

By embracing this M&A blueprint, Progress has deployed over $1 billion in capital since 2018 and completed four key acquisitions that contributed to revenues and EBITDA growing threefold and sevenfold, respectively. The success emanates from a disciplined capital allocation approach that ensures the weighted average cost of capital ((WACC)), of 9%, is lower than the Return on Invested Capital ((ROIC)), between 12% and 14%, thus producing accretive returns for shareholders. Progress sees an ample opportunity for additional acquisitions in the future as they've identified a pipeline of over 350 companies with revenue greater than $25 million.

2023 Progress Software Investor Day Presentation

{kind=link}

Financial Overview

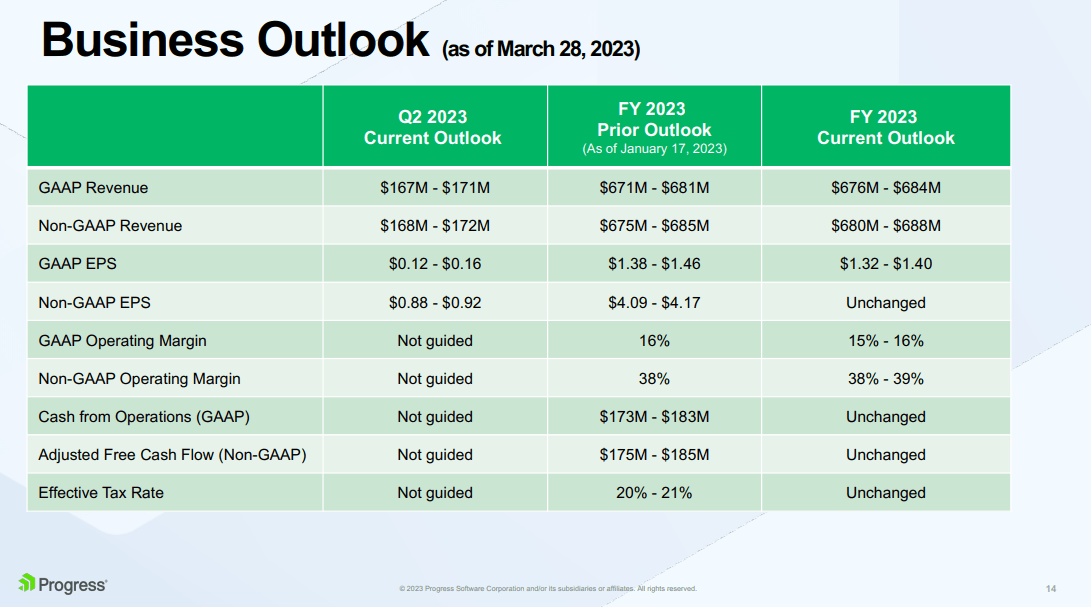

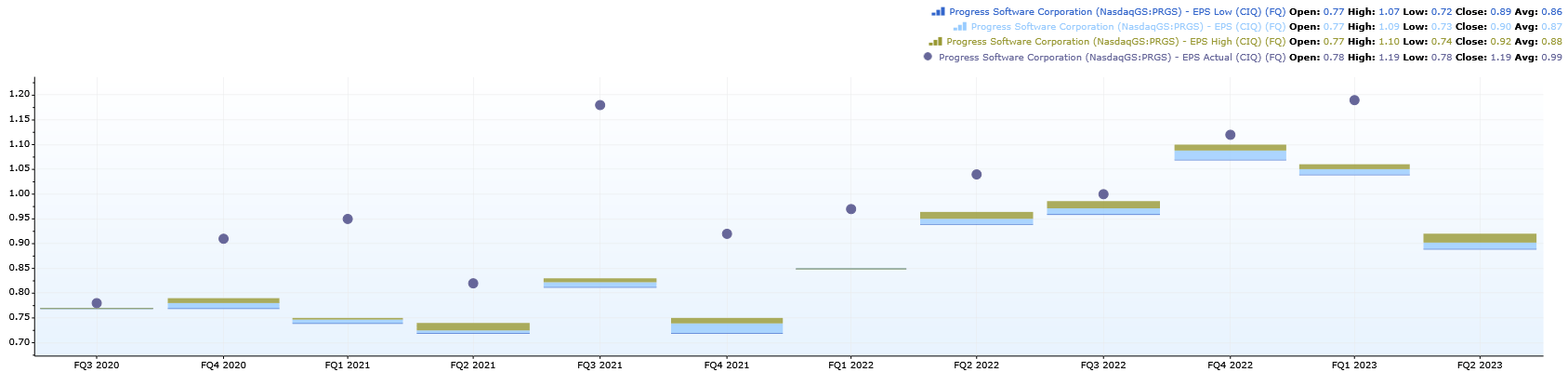

Progress Software's financial performance demonstrates solid growth and profitability, albeit with slight deceleration in certain areas. In 2023 Q1, the company's revenue grew by 14% year-over-year in constant currency ((CC)), which aligns with its CAGR of 14.4% since 2018. This growth surpassed expectations primarily due to robust demand for products including OpenEdge, DataDirect, MoveIt, and LoadMaster.

The operating margin for the same period was approximately 44%, beating estimates by four percentage points. However, operating margins are expected to be the lowest in Q2 and Q3 due to revenue pulled into Q1 and a lower margin mix from the early phase integration of MarkLogic. Management expects FY2023 operating margins to be in the range of 38% - 39%.

Regarding revenue retention, Progress Software maintained a stable net retention rate ((NRR)) of 102%, consistent with the previous quarter, and falls within management's historical range of 101-103%. Despite challenging macroeconomic conditions, this stability in revenue retention highlights the resilience of Progress Software's product portfolio.

Annual recurring revenue ((ARR)) grew by around 4% year over year on a pro-forma basis, slightly down from 4.4% in the prior quarter. The net new ARR addition for the quarter was $2 million, which is down from an average of $6 million during 2022. MarkLogic's ARR contribution for FY23 is now expected to be $80 million, up $5 million from prior guidance.

Looking ahead, the company has modestly raised its revenue and operating margin guidance for FY2023. Specifically, revenue guidance has been increased by 0.5%, or $4 million, at the midpoint, and the operating margin is now expected to be 38.5%, up 50 basis points compared to prior guidance. Non-GAAP EPS remains unchanged at the midpoint of $4.13, which is flat compared to FY2022.

Q1 2023 Earnings Call Supplement

{kind=link}

Investors can expect a mild dip in 2023 Q2 EPS, with an expected range of $0.88-$0.92 vs $1.19 actual normalized EPS in 2023 Q1. The primary cause for this decrease is the shift of more revenue into Q1 from Q2; however, this doesn't affect the full-year 2023 outlook. Also, it's worth noting that Progress has beaten EPS estimates for the last 11 quarters.

{kind=link}

Progress Software's financials exhibit solid performance with revenue growth and strong operating margins. Although there is a slight deceleration in ARR growth, the company's stable net revenue retention reflects the essential nature of its products. The higher revision in full-year guidance and the expected contribution from MarkLogic are also positive indicators for future performance.

SWOT Analysis

Strengths

- Progress Software possesses a portfolio of tools that support critical applications, which is essential for its customer base.

- The company maintains a shareholder-friendly capital allocation strategy, which includes paying dividends, stock buybacks, and engaging in accretive acquisitions.

- With a diverse and reputable customer base, including over 100,000 blue-chip companies across various industries like Boeing (BA), Merck (MRK), Wells Fargo (WFC), and Walmart (WMT), they have established a strong market presence.

- The company demonstrates healthy free cash flow conversion, consistently achieving over 30% conversion rates.

Opportunities

- Progress Software's M&A strategy equips it to leverage both existing and emerging trends within the software market, potentially driving growth.

- The company has numerous investment opportunities to pursue, further enhancing its growth potential.

- The expanding market in the DevSecOps space presents a growth avenue for Progress to explore and capitalize on.

Weaknesses

- Progress Software primarily relies on inorganic growth through acquisitions, which necessitates stringent financial discipline and operational acumen to realize cost synergies. Failure in this regard could adversely affect revenue growth and profitability.

- The company is significantly dependent on OpenEdge products, which account for 42% of revenues in 2022. This heavy reliance on a single product line could pose risks.

Threats

- Progress operates in a highly competitive landscape with well-funded competitors with both on-premises and modern cloud-native solutions. Increased competition or competitors offering products at more competitive prices could impact customer retention.

- Macroeconomic fluctuations can affect the valuations of software companies, including Progress. Though the company's strong free cash flow may mitigate the impact, macroeconomic instabilities, such as potential recession, remain a threat.

- There is a risk that if Progress Software’s products become outdated compared to newer competitive alternatives, customers may opt for different solutions, leading to higher churn rates and negatively affecting retention.

Valuation

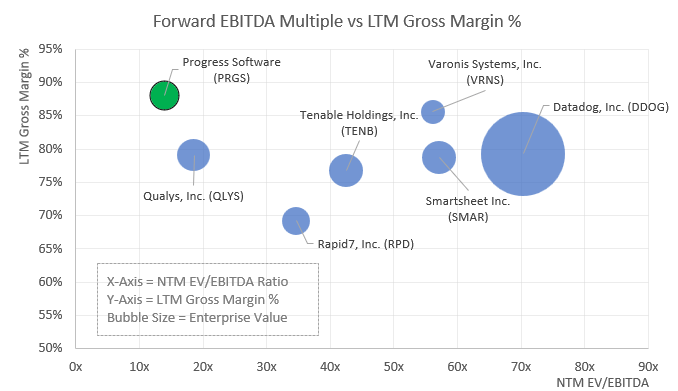

Progress Software stands out as an outlier within its peer group of software companies based on Capital IQ estimates. The company trades at a forward EBITDA multiple of 13.93x, significantly lower than the peer group median of 49.31x, indicating that Progress is undervalued relative to other software companies. Progress Software's gross margins of 88% compared to the peer group median of 79%, suggesting that they are more efficient at managing costs to produce revenues.

{kind=link}

Progress Software presents a more balanced financial profile, with an attractive valuation (low EBITDA multiple) and superior gross margins in contrast to some of their peers, such as Smartsheet ( SMAR ) and Datadog ( DDOG ), which have forward EBITDA multiples of 57.11x and 70.34x respectively.

Furthermore, if Progress Software were to trade at the System Software U.S. Industry median multiple of 19x, its implied enterprise value would be around $4.3 billion. Accounting for cash and short-term investments of $122.9 million and deducting total debt of $838.7 million, we would be left with an implied equity value of approximately $3.6 billion.

Given that 44 million shares are outstanding, resulting in an implied share price of $88.72. This implies an upside of 34% compared to its current share price of $55.66. While this example is hypothetical, it is meant to highlight the tremendous potential if Progress traded in line with the industry.

Capital IQ

In conclusion, Progress Software is a promising investment opportunity due to its portfolio of sticky software products, a strong customer base, and robust financial performance. Its strategic focus on inorganic growth through M&A, shareholder-friendly capital allocation, and continued investment in product innovation position it well for sustained growth. Additionally, with an attractive valuation relative to the industry and a leadership team with a proven track record, Progress Software is a compelling buy for investors seeking a highly profitable player in the software market.

For further details see:

Progress Software: An Outlier In The Infrastructure Software Industry