PRGS - Progress Software: Risk/Reward Is Not Attractive Right Now

2023-12-13 17:51:58 ET

Summary

- Progress Software's financial performance has been trending down in terms of efficiency and profitability in GAAP terms.

- The company's debt levels are a concern, but it has historically maintained acceptable debt-asset and debt-equity ratios.

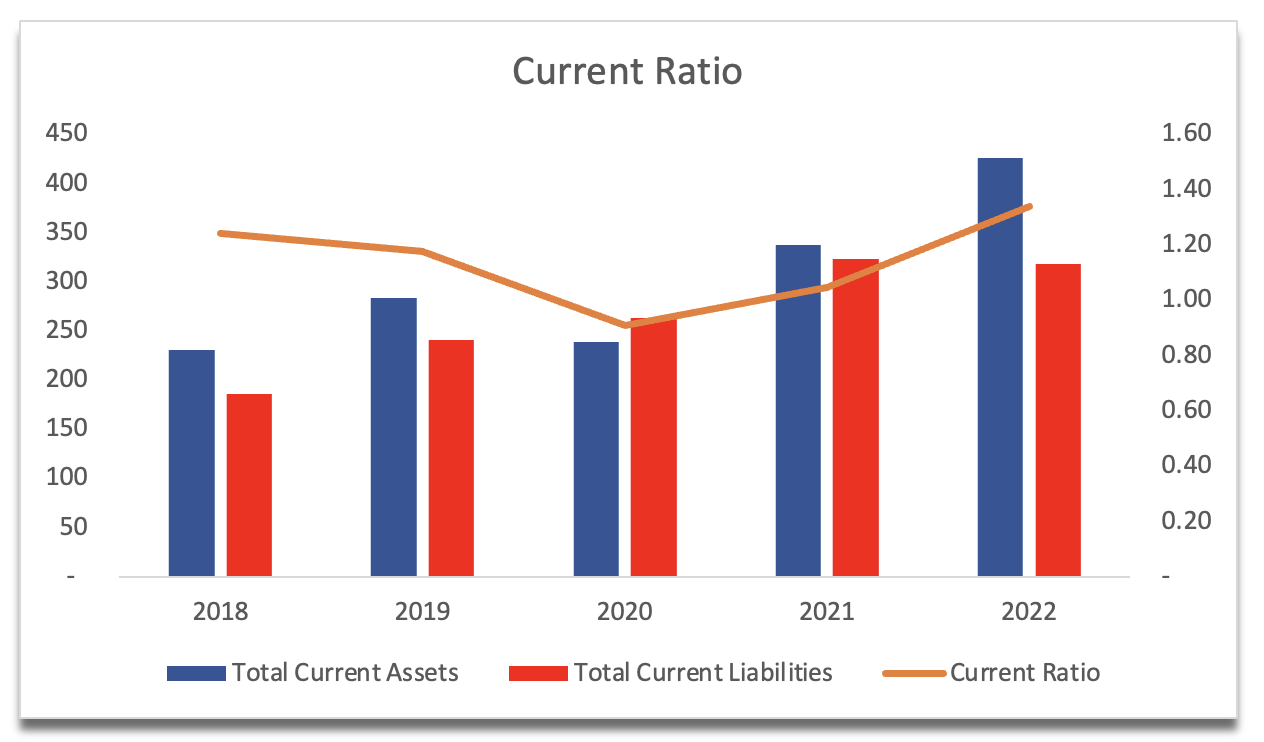

- The company's current ratio is slightly below 1, which may limit its ability to fund future growth initiatives without employing more debt.

Investment Thesis

Progress Software (PRGS) has gone nowhere over the last year, so I wanted to take a look at how the company performed historically by digging deeper into its financials. It seems that the company is trending down in terms of efficiency and profitability in GAAP terms while maintaining similar non-GAAP performance. The company is not very attractive on non-GAAP and GAAP valuations; therefore, I am giving it a hold rating until I see some efficiency and profitability improvements over the next while.

Briefly on the Company

The company helps businesses build, deploy, monitor, and manage all their critical applications. Their tools are designed to help with digital experience, DevOps, infrastructure monitoring, secure data connectivity, and make sure that everything is running smoothly.

Financials

As of Q3 2023 , the company had around $138m in cash and equivalents against $389m in long-term debt. the company is not very big so, it has a significant amount of debt in my opinion, however, is it worrisome? There are a few metrics I like to look at to decide whether the management is utilizing debt to fund the company's operations effectively. Historically, the debt-asset ratio has been within the acceptable range of 0.30 -0.60, which is great. This shows us that the company is not over-leveraged. As of Q3 '23, the company's D/A ratio has gone up slightly to 0.47, which is still acceptable. The company's debt-equity ratio has been much better in the past when it had considerably less debt. Anything under the D/E ratio of 1.5 I consider to be decent, however, as of the latest quarter this has increased to 1.7, which isn't the worst. As long as it doesn't increase anymore, the company should be fine, especially considering the next metric I like to look at, which is the interest coverage ratio. In the past, this ratio has been strong, however, over the last while, EBIT has been not as strong as before and there is more debt to pay interest on, which brought down the company's interest coverage ratio to around 4x. For reference, many analysts believe a ratio of 2 is sufficiently healthy, which means that EBIT can cover the annual interest expense on debt twice. I think that is a little too forgiving. There isn’t much leeway for bad years of performance when the EBIT may not be able to cover the interest expenses, therefore, I like to see a coverage ratio of at least 5x, which I think provides a good cushion in case the company has a bad year or two. In the latest quarter, that stood at around 4, which is not that bad, however, if it continues to trend down, it may become a problem.

{kind=link}

The company's current ratio has been close to 1.0 over the years, which is good. At least it can cover its short-term obligations without issues, however, it doesn’t leave my capital for expansion, which means the company may have to employ debt for future acquisitions and other growth initiatives. As of the latest quarter, the current ratio is slightly under 1, driven by a higher current portion of LT debt and a halving of cash on hand from FY22. I will have to add a little extra margin of safety when I'm going through the company's valuation in a later section.

{kind=link}

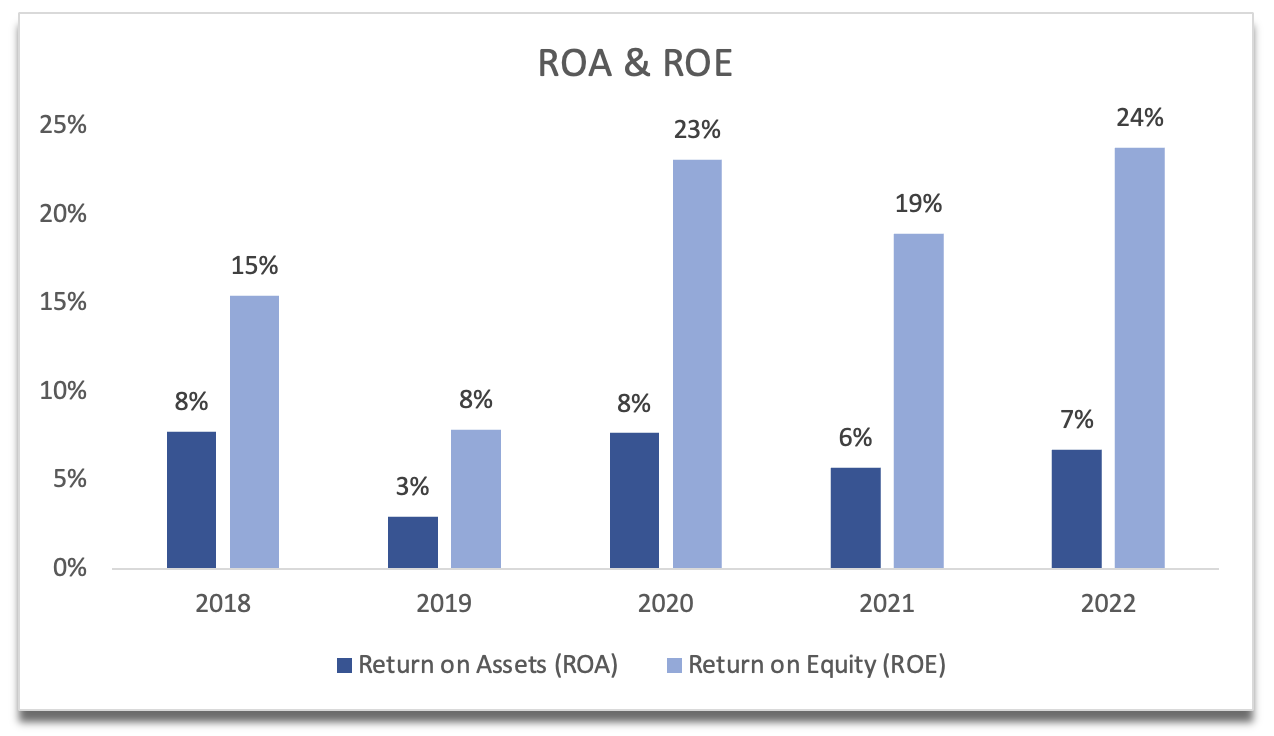

In terms of efficiency and profitability, the company's ROA and ROE have been fluctuating quite a bit over the last while, especially the return on equity, which seems to be inflated because of the debt the company has on its books. It's not a bad way to increase the return on equity with the use of leverage, however, it needs to be careful and use it wisely, to not be overwhelmed by high annual interest expenses on debt. The latest returns are not bad, so as long as the company can keep this up, it should translate to increased value for shareholders.

{kind=link}

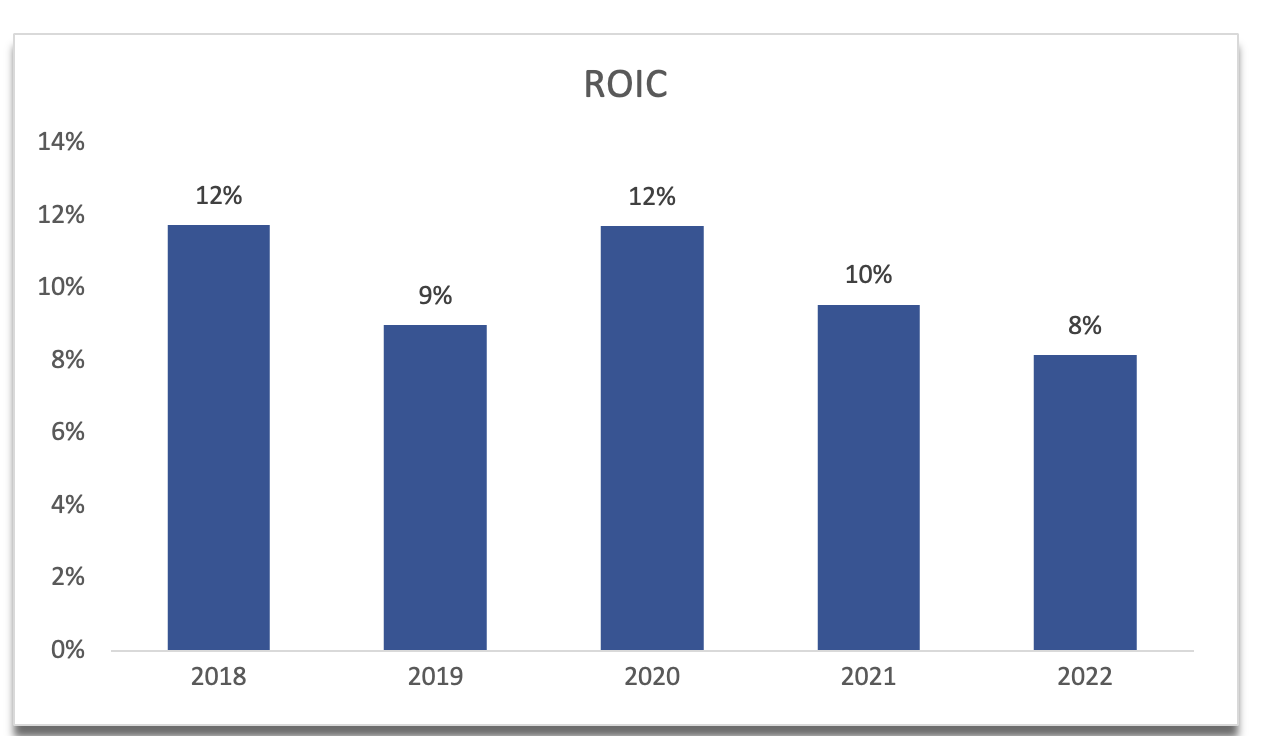

The next important metric that I look at is not very attractive any longer because it has been in a downtrend. Return on invested capital, or ROIC at the end of FY22 went down to around 8%, which is slightly below my target of at least 10%. The company wasn’t able to increase NOPAT significantly y/y which led to a decrease in ROIC. It tells me that the management did not allocate capital very efficiently, and the company may be losing its competitive advantage. Another reason for this is that the management was not able to manage costs effectively. From FY21 to FY22, COGS increased by around 90bps relative to revenues, while operating expenses increased by almost 200bps. In fact, from FY20 to FY22, costs increased by more than the revenue increases, which is not a good sign. I would like to see the company crossing back over 10% once again, but for now, I will have to add more margin of safety to take on such risks.

{kind=link}

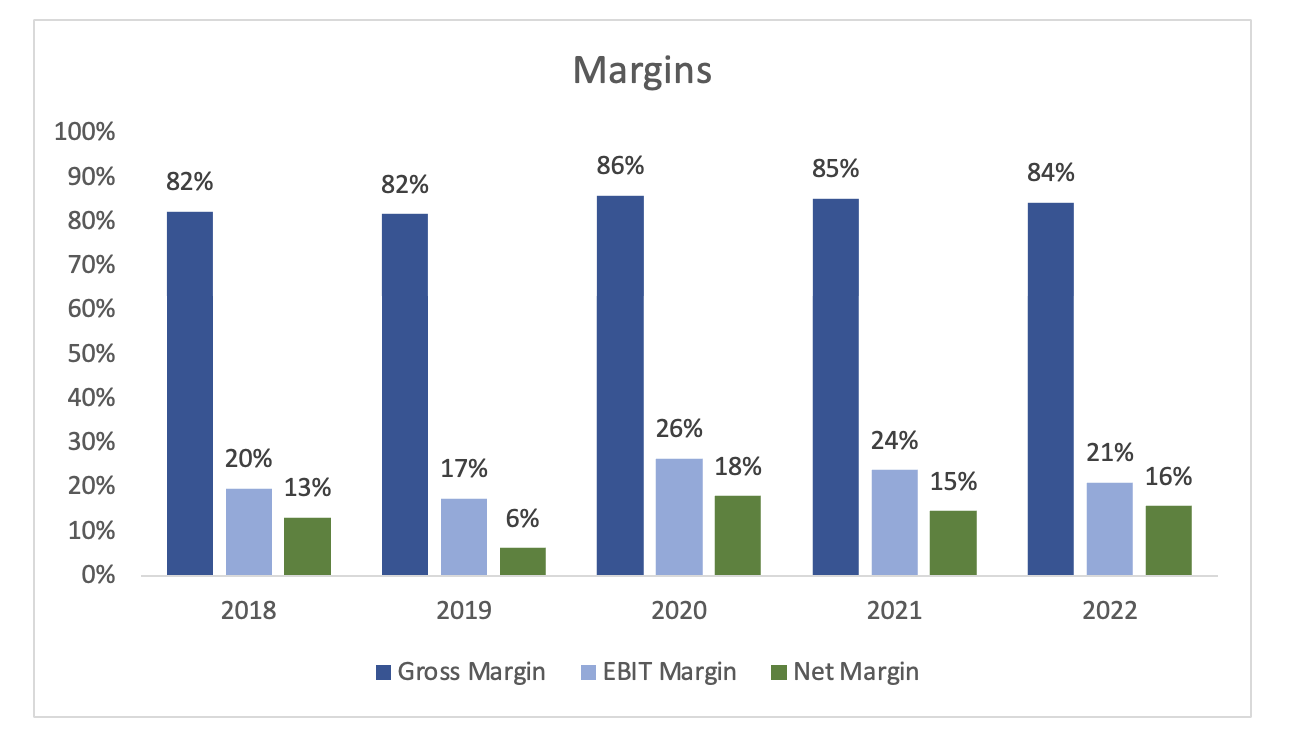

Speaking of efficiency and profitability, the company's GAAP margins have seen better and worse days, however, in the last three years these have been trending down also, which is a little worrisome. As of 9 months ended August, gross margins were at 82%, operating margins at 17%, and net margins at around 10.5%, which means that the downtrend is still alive and well. This will require an even larger margin of safety.

{kind=link}

Overall, there isn't a lot to like here. Profitability and efficiency have taken a massive hit over the last while, and the company seems to be losing its competitive advantage. The company exhibits the opposite characteristics of a good investment.

Comments on the Outlook

The company may catch the buzz wave of AI, as many software companies tend to do. That would be one of the two ways I see the company increasing its revenue growth substantially. The company's CEO is very interested in AI, so I believe that he will continue to push the narrative of GenAI and machine learning that will somehow benefit their customers and the company itself in the end, and hopefully make it much more profitable and efficient. With applications like Sitefinity, and the recent acquisition of MarkLogic, which came with Smartlogic, the company is aiming to provide customers with the help of automating forms, create content at scale, and hopefully provide cost-cutting solutions to their problems. It is still in the early stages of these initiatives, so I wouldn’t expect a massive change to occur right now.

The other way for the company to grow at a faster pace is inorganically through strategic acquisitions. The company has bought at least 5 companies in the last 4 years, so I don’t expect this to change any time soon with the most recent acquisition being MarkLogic . The balance sheet of the company isn't bad, and we can see that the management doesn't mind employing leverage to further the growth of the company, I don't see anything wrong with that so far, as it seems like the debt is being used smartly.

Valuation

I always try to approach valuation assumptions with a conservative outlook, so I can get a good deal on companies that may be trading well below their intrinsic value. This gives me naturally a higher margin of safety if I lowball some of the assumptions. For revenue growth, I went with around 6% CAGR for the base case. This includes the company's guidance of around 14% in FY23. I didn’t want to assume higher than average for the reason I mentioned above. Below are those assumptions for the base case, and to cover all my bases, I also added an optimistic and a conservative case, with their respective CAGRs.

{kind=link}

For margins and EPS, I decided to use non-GAAP metrics because the company seems to be using these over the GAAP ones to show the “true value” of the company. Also, I used these values because I wanted to give the company a chance. You'll see what I meant later. The management guides for around 38%-39% operating margins, but as I said I want to be more conservative; I went with slightly lower margins. Below are those assumptions. The FY22 numbers are GAAP numbers, so there isn’t much comparison, other than how inflated adjusted numbers are.

{kind=link}

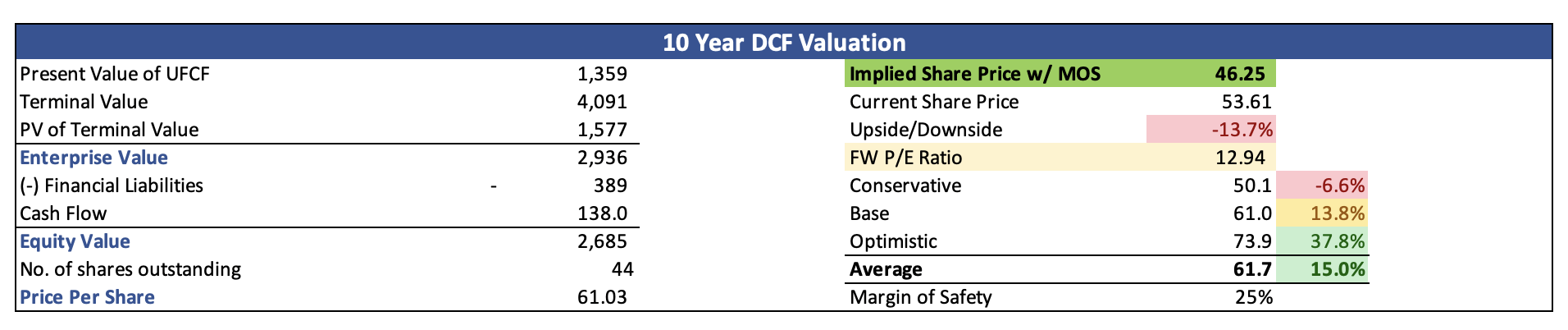

For my DCF analysis, I also went with a 10% discount rate instead of the company's WACC of 7.5%. This way, I'm getting more margin of safety because of the downtrends in the metrics above. I also went with a 2.5% terminal growth rate. Furthermore, I went with another 25% margin of safety, just so I could beat the estimates down and try to get the company for as cheap as possible. This way I also get a lot more room for error. With that said, PRGS's intrinsic value is around $46 a share, which means the company is trading at a slight premium to its fair value.

{kind=link}

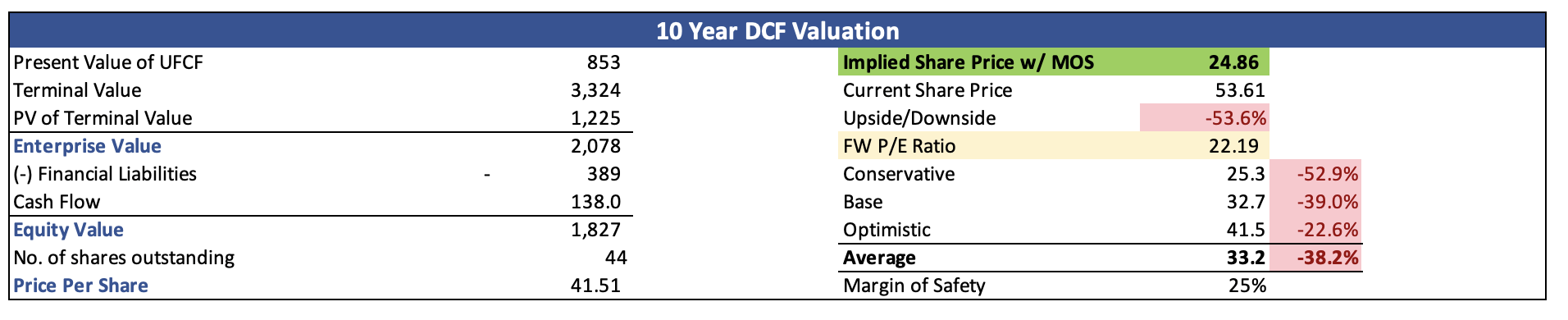

Remember when I said I wanted to give the company a chance? Well, the above PT is using adjusted metrics, where operating expenses are much lower than the reported GAAP ones. If we used the GAAP numbers and over time improved them by around 300bps, we would get quite a different outcome.

{kind=link}

Closing Comments

So, it is up to you what you want to do with this information. Either way, the company seems to be overvalued currently, and would not be a good time to start an investment right now. Therefore, I assign PRGS a hold rating, until I see more improvements in margins or if the company can do much higher revenue growth than what I had modeled.

I would like to see the company's GAAP figures improve considerably before I would consider investing in the company. The downtrends in the company's efficiency and profitability are not screaming this is a good investment right now.

Nevertheless, there is a price at which I would be willing to take on those risks, and it is at around $35-$40 a share, therefore, I will be setting up a price alert for those prices and forget about it until the upcoming earnings calls just to see if anything has been improving.

For further details see:

Progress Software: Risk/Reward Is Not Attractive Right Now