PGNY - Progyny: Market Underappreciating Excellent Quarter

2023-11-16 19:45:24 ET

Summary

- Progyny's stock has under-performed the S&P this year, but the company's Q3 2023 results show potential for long-term growth.

- Progyny has a significant market opportunity with 8,000 self-insured employers and potential for 75 to 100 million covered lives.

- The company's financials are strong, with revenue growth of 37% in Q3 2023 and a healthy balance sheet.

I first covered Progyny ( PGNY ) roughly a year ago when I gave the company a “Buy” rating and clearly stated my belief that the company would be long-term winner. Since that time the stock is up by less than 3%, and year-to-date Progyny is only up 4% which far below the S&P.

Nonetheless, after reviewing the company’s Q3 2023 results, I still firmly believe this is great organization which will reward long-term investors.

Let’s dig in the details!

Market Opportunity and New Clients

Going back to the company’s most recent 10K statement, Progyny believes in the United States there are roughly 8,000 self-insured employers. Of these 8,000 employers they believe that represents the potential for approximately 75 to 100 million covered lives. At the time of the 10K filing, Progyny had 5.4 million covered lives. As you can see below, Progyny has some significant clientele including Google, 3M and Microsoft.

{kind=link}

Progyny Investor Presentation

As of Q3 2023, Progyny is expecting over 460 clients with covered lives of roughly 6.7 million in 2024. Management noted that during the quarter Progyny won their first professional sports team client and won their first professional sports league (neither of which were specifically disclosed). Additionally, 300,000 covered lives were added from the government. This is a first for the company and represents a new opportunity for the organization.

Despite this continued success management believes the company still has room to grow. During the Q3 2023 earnings conference CEO Pete Anevski stated, “ Even with this sustained track record of success, and once our newest clients have all gone live, we still remain at a very early stage of penetrating our market opportunity with just a mid-single-digit share of either the 8,000 companies or the 100 million covered lives in our current addressable market.”

I think the management team also made some interesting remarks this quarter on the company’s moat and position within the industry. Responding to a question about competition and the current marketplace Anevski had this say, “It was not more competitive. In fact, I would argue it might have been a little less competitive.”

Anevski went on to state, “ Again, each year we continue to grow our market share. And even against our competitors collectively, we believe we do a good job in terms of continuing to penetrate the market and expand and grow market share.”

Overall, I think it was a very positive quarter for the company and believe Progyny continues to be market leader within this niche healthcare space.

Financials and Key Metrics

In Q3 2023 , Progyny had another solid quarter as revenue grew to roughly $281M, which is an increase of 37% compared to Q3 2022. Fertility benefits services revenue accounted for $175M which is an increase of 35% compared to roughly $130 million which was reported in Q3 2022. Pharmacy benefits services revenue accounted for roughly $106 million which is an increase of nearly 40% compared $76 million which was reported in the third quarter of 2022.

Below are some key metrics the company provided on their recent 8K earnings release :

{kind=link}

SEC.gov

As of September 30, 2023 Progyny had 392 clients. This is compared to 282 clients in Q3 2022. As you can clearly see this client increase is driving more ART cycles and increased utilization. Utilization rates may vary management noted, as factors such as new client launches, plan design and time of the year can impact these rates. The 35% increase in ART cycles year-over year however, is certainly impressive.

The company’s balance sheet is extremely healthy with cash and cash equivalents of roughly $158 million. The company has enough current assets to cover all of these current liabilities and has essentially no debt.

These are impressive financial results which I believe will likely continue as demand for these benefits will only continue to rise. During the Q3 earnings call, management raised their guidance and are now expecting revenue between $1.087 billion to $1.095 billion, an increase of nearly 40%. They are projecting net income between $58.3 million to $60 million or EPS of $0.58 and $0.59.

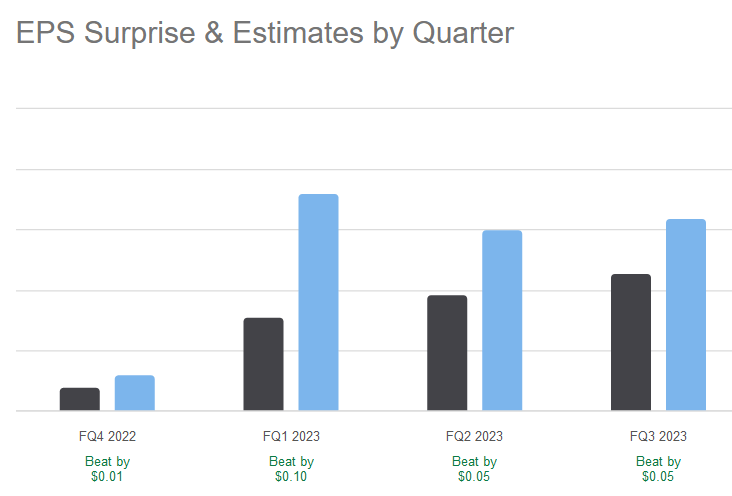

Given the constant beat over the last four quarters, as you can see below, I won’t be surprised to see the company beat EPS estimates come in over $0.60 a share.

{kind=link}

Given the company’s 100% retention rate (for the eighth year in a row) coupled with new clients and perhaps even more covered lives from coming from the government, I can foresee revenue of $1.095 or even $1.1 billion being achievable for the company.

Valuation

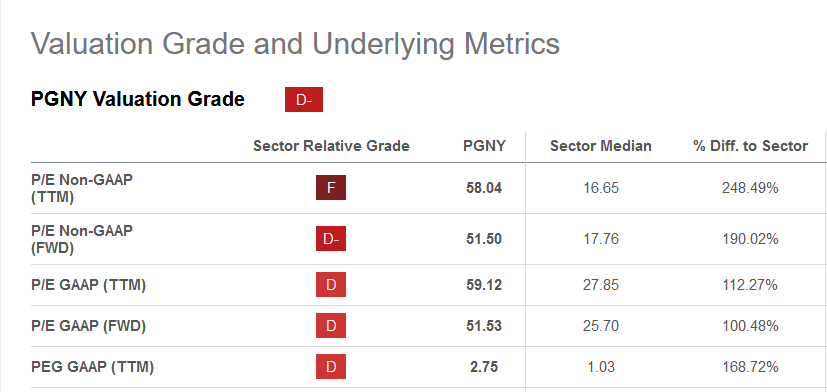

Progyny has valuation grade of a “D-” from SA Quant:

{kind=link}

Seeking Alpha

When I first reviewed this company it had a trailing P/E ratio of roughly 75. As you can see below Progyny’s trailing P/E ratio is less than 75 and much less than it compared to earlier this year:

That being said, from this metric it’s clearly still an expensive stock as both the trailing and forward P/E ratios from Progyny are much greater than the sector median.

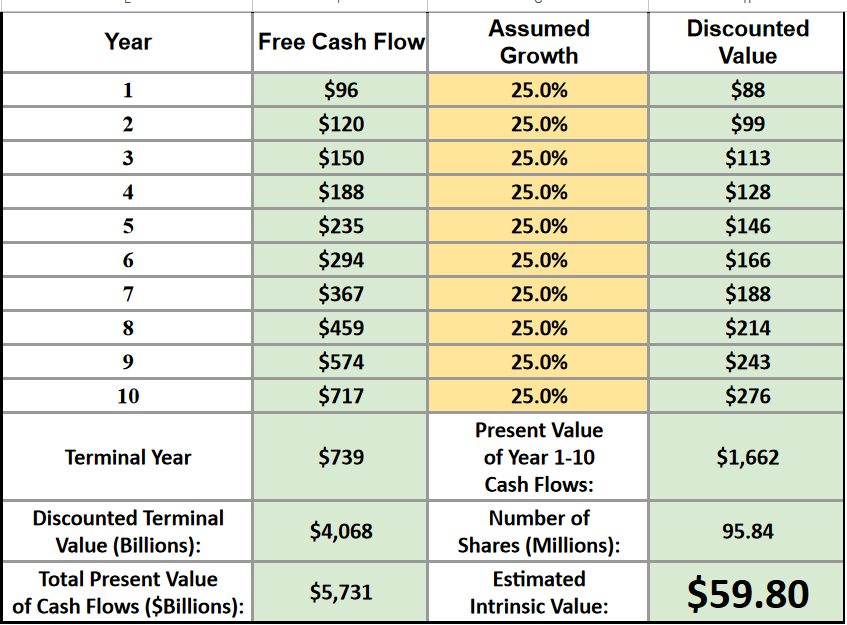

However, taking a different approach, the stock doesn't appear so overvalued. Using a reverse discounted cash flow model with a discounted rate of 10% and a terminal rate of 3% and assumed growth of 25% I come to estimated intrinsic value of roughly $60 a share.

{kind=link}

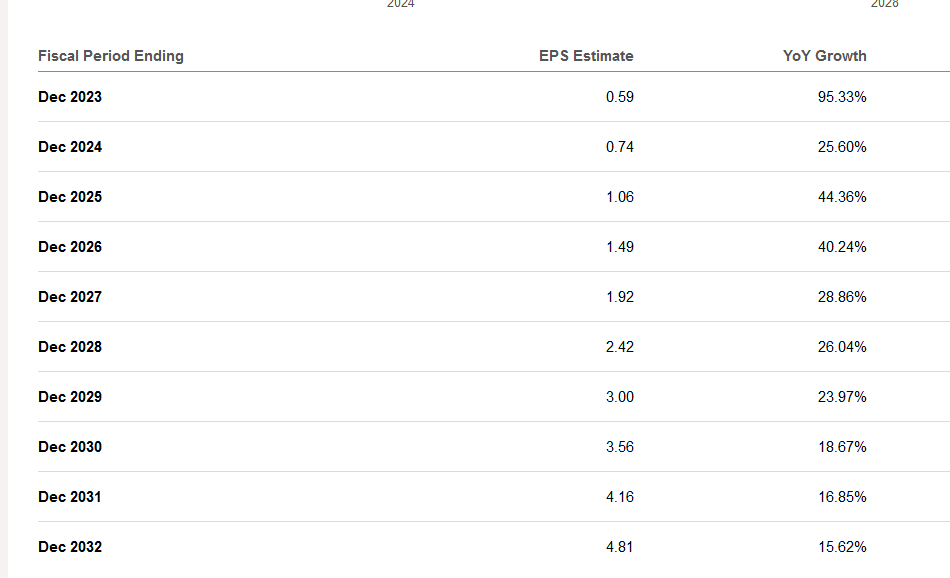

I think 25% is a reasonable, if not conservative, growth rate as you see these estimated growth rates from Seeking Alpha are in that same ballpark:

{kind=link}

I still strongly believe this is an exceptional company and at these levels I think any long-term investor can feel comfortable creating a position or adding to their existing position.

Conclusion

I continue to believe Progyny is a providing a much need service for families. I think this quote from Anevski perfectly sums up the, “ As the prevalence of infertility continues to rise, with more people now needing assistance than ever before, and with millennials routinely citing family building benefits as one of the most relevant factors when deciding where they want to work, we've seen how fertility and family building solutions have increasingly become important to employers as they look to meet their recruitment, satisfaction, and retention goals.”

More and more individuals care about health and family benefits such as paid family leave and certainly fertility treatments as well. Progyny is the leader in this space and is playing a vital role in fulfilling this need.

As the key metrics above illustrate Progyny continues to add more and more clients, meaning the number of covered lives continues to grow as well. Progyny believes they still have a large addressable market and recent comments from this quarter indicate the management team believes Progyny is growing their market share.

Financially Progyny has a stellar balance sheet with amble cash and no debt. Revenue and net income continue to rise, and the management continues to be rather efficient with the organization’s capital as return on invested capital is at nearly 19% with return on equity at over 11%.

Lastly, I believe valuation is more reasonable compared to earlier in the year, and the stock could be purchased at these levels.

This a great business continuing to grow both clients and revenue and I’ll be adding to my position as I continue to believe this stock will reward patient long-term investors.

For further details see:

Progyny: Market Underappreciating Excellent Quarter