BABAF - Project $1M: 2023 Review

2024-01-03 10:37:30 ET

Summary

- Project $1M is a long-term buy-and-hold portfolio aiming to turn $275k into $1M within a 10-year period.

- 2023 saw a good bounce back from the disappointment of 2022.

- The portfolio exited Meta during the year and added 2 new positions in its place.

For the benefit of any new readers, Project $1M is a long-term buy-and-hold portfolio started in 2015 . The portfolio's objective was to turn a fixed amount of approximately $275k into $1M at the project's planned completion in 2025.

This would be primarily accomplished by purchasing financially disciplined, high-quality companies with large barriers to entry that had the benefit of secular tailwinds behind them. To minimize taxes and transaction costs, the portfolio would have minimal trading and accrue the benefits of long-term compounding.

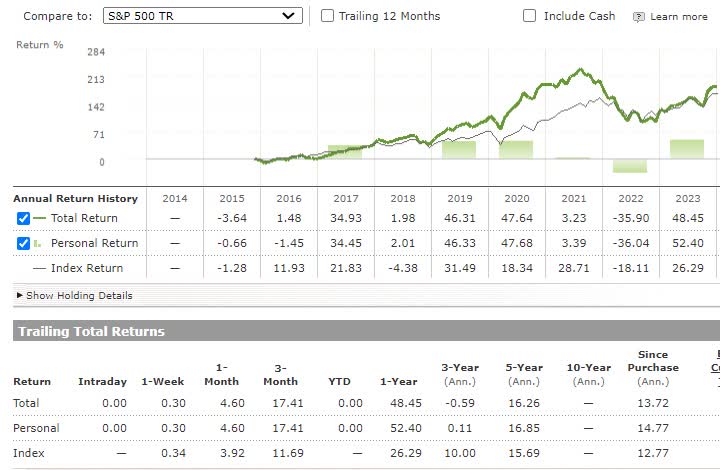

The portfolio recently concluded eight years and remains well on track to achieve its initial objective. After a pretty bleak 2022 , nearly all losses have been recovered in 2023. While I took it on the chin in 2022, I didn't make any knee-jerk reactions regarding portfolio allocation for 2023. Ultimately, I had faith that the market would return to its senses and that the underlying quality of the portfolio's businesses would be recognized.

{kind=link}

Portfolio concentration was an incidental byproduct of my approach to portfolio allocation. I allow winners to continue winning without attempts to reduce allocations. This was the case again in 2023, with the top 5 positions accounting for 50% of the portfolio.

Concentration improved a little during 2023 with the recovery of many positions. I'd like to see the combined Visa ( V ) and Mastercard ( MA ) concentration continue to fall toward 20% combined as other positions outperform them.

2023 Review

Unlike 2022, the largest positions within the portfolio generally performed equal to or better than the S&P 500 Index. That led to a good outcome vs the S&P500 this year.

{kind=link}

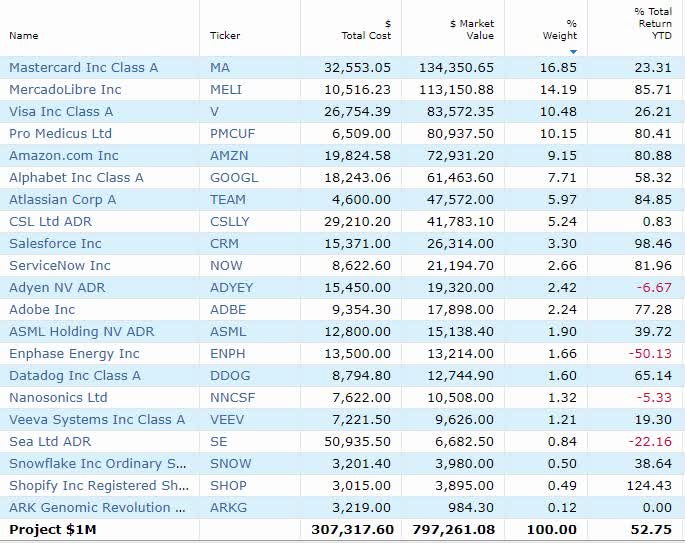

Table created by Author includes Veeva ( VEEV ), ServiceNow ( NOW ), Alphabet ( GOOGL ), Snowflake ( SNOW ), Adobe ( ADBE ), Amazon ( AMZN ), Salesforce ( CRM ), Nanosonics ( OTCPK:NNCSF ), ARK Genomic ( ARKG ), Datadog ( DDOG ), Atlassian ( TEAM ), Shopify ( SHOP ).

Exiting Meta, adding Adyen and Enphase

After holding Meta ( META ) since its aggressive sell-off in 2018, I finally decided to exit the business in 2023. Meta had a charmed run in 2023, almost tripling over the year. Unfortunately, I didn't ride this to the top and exited the business at around $240 a share.

Still, I was comfortable leaving the position at that point. I didn’t feel Meta’s efforts towards user attribution on mobile were progressing at a pace I was happy with.

I also had broader concerns about this long-term growth trajectory and didn’t feel as comfortable with its prospects for double-digit revenue growth moving forward. I may have got this one wrong. Meta balanced good top-line growth with aggressive cost reduction and was a star performer in 2023. Still, I have no regrets about this outcome.

The business was a good contributor to returns over the years. I may look at this one again if the valuation makes sense. However, at current levels, I don’t foresee myself re-entering here.

I switched out of Meta for two other fallen angels in 2023.

I’ve been interested in digital payment for quite a while since my initial investments in Visa and Mastercard. I have long admired Adyen ( ADYEY ) , but could never get comfortable paying the lofty multiples that the business commanded.

That changed in 2023 when the business crashed after recent earnings, making building a modest position very interesting. I see a lot of the characteristics in Adyen that attracted me to Visa and MasterCard in the first place. In my opinion, the business has the best payments processing platform for Omni channel merchants with complex retail operations, both online and in-store.

Adyen provides merchant acquisition and payment processing functions with a single platform. It’s also built from a unified common code base, unlike other competitors that have had to integrate a patchwork of different acquired platforms, which have lowered their authorization rates. That gives Adyen a competitive advantage because it can authorize more transactions at lower levels of fraud than virtually all its competitors.

The business also has excellent financial discipline, with returns on equity and invested capital well north of 20%. During Adyen's recent investor update, the company indicated it could grow in the low to mid 20% range for the rest of the decade. I also believe that this is very likely.

Enphase ( ENPH ) was another position I picked up with the Meta sale proceeds. The business is in the rooftop solar space and provides inverters and batteries for these deployments. Along with Solar Edge, Enphase dominates this market globally. Tesla is another recent entrant into the solar battery space.

Solar, particularly rooftop solar, has fallen off a cliff this year as interest rates have skyrocketed, and the demand from consumers for new rooftop solar installations has collapsed. Additionally, there’s been a regime change. In many instances, utility payments for excess energy production have been reset, most notably in California and several other states.

I am convinced there will be an energy crisis over the next few years, with the governments increasingly pushing back on dirty energy and desiring to go carbon neutral over the medium to long term. I think solar is the only viable alternative to conventional energy production, with falling output and costs per unit of energy production likely to continue to make this energy increasingly economical.

Not only is Enphase part of the comfortable duopoly with Solar Edge for residential inverters, but the business is also very financially disciplined and has a return on invested capital above 20%.

The business also has a history of excellent profitability and cash flow production. With long-term rates now on the way down, I think it’s a question of whether solar energy continues on the rebound. I’m happy to bide my time with this one over the next few years and feel comfortable with my entry point here.

Pro Medicus Shines

Pro Medicus ( PMCUF ) is a business I’ve held here for five years. It just continues to do its thing with little fuss or attention. It’s the dominant provider in digitizing imaging for radiologists and other healthcare specialties. 2023 was a banner year for the business. Not only did it win a clutch of new high-profile clients, but it also successfully renewed many of its more significant deals for bigger dollars.

Finally, the business showed signs of success in penetrating other healthcare specialties beyond radiology, with a deal that also covers cardiology imaging. This is an essential milestone in Pro Medicus' mission to be the digital imaging provider of choice for all medical subspecialties.

Owning Pro Medicus for the full duration of the time within the Project $1M portfolio has been an exciting journey for me. There have been many occasions when I have believed the business to be too expensive. Yet because of its relatively small size, and it keeps putting runs on the board, I’ve been more than happy to continue owning the business within my portfolio.

The actual investment size itself was very modest, and I’ve been more than happy to let the market set the valuation for the business wherever it thinks it makes sense. As long as the company continues to execute, I will remain an owner.

Sea is still no MercadoLibre… yet

Of all my decisions and investments in Project $1M over the last eight years, it’s probably fair to say that I look back at the Sea ( SE ) investment with mixed feelings. That’s not just because the position is the most significantly down.

It’s also because I made a strategic error in assuming that just because you had a motivated founder pursuing a similar vision with good strategic assets, the outcomes could be equal when translated to a different region. I felt it would also offer better investment outcomes than my previous holdings in China, which I exited to invest in Sea. However, the experience in owning Sea hasn’t been as expected.

MercadoLibre ( MELI ) has deep assets and multiple moats in Latin America by building out a comprehensive logistics network and consolidating on the strengths of its e-commerce dominance. It capitalized on e-commerce success by building a payments network, MercadoPago, now preeminent in the region, and a good advertising platform, which will mean impressive things for its future cash flow generation.

Unfortunately, Sea failed to capitalize on its considerable gaming and e-commerce advantages and instead pursued global domination, which it pulled back from recently. I like more of what I’ve seen from the business in 2023.

It’s shown that it can flex levers to become independent and profitable. It’s also taking steps to turn its last-mile logistics into a competitive advantage for the business. The steps are a little late, but there is a long race to be run in the Southeast Asian region.

While other competitors are knocking on the door, most notably TikTok, Sea has stared down Lazada and Alibaba ( BABA ) for much of the last few years. Ultimately, I believe it can do so again with TikTok. There’s room for multiple winners in the region, and I think Sea is not priced here for long-term success.

So, while the business is not yet another MercadoLibre, it certainly has the potential to get there. Owning e-commerce is a gateway to stacking on high engagement and high-margin services that can improve customer stickiness and long-term business creation. It remains to be seen whether Sea can execute that vision.

2024 outlook

With just two years left to run for the Project's $1M objectives, I believe the portfolio still has a reasonable shot at achieving the goal I first set out in 2015. If the portfolio returns what it has since inception, this goal will be comfortably reached.

With interest rates falling and inflation showing signs of melting away, the macro environment looks much better than in recent years. My estimate for 2024 is that most of the businesses in the portfolio should grow at least low double digits for the next couple of years. Time will tell if they can do this or even better.

I look forward to taking you through to the eventual outcome Project $1M next year. Happy investing to you all!

For further details see:

Project $1M: 2023 Review