VNQ - Prologis: The Unrecognized Bellwether

2023-04-20 21:53:07 ET

Summary

- PLD's report showed strength across the sector.

- Yet sector peers are trading in line with market.

- This is a bird in hand opportunity where the information is already out but somehow not priced in.

Most industries have a bellwether, but for industrial REITs, Prologis ( PLD ) is the ultimate bellwether.

Prologis’ $196B mass of assets spread across just about every major market means their results are a direct reflection of the strength or weakness in the sector. Additionally, PLD is a researcher of the sector and tracks a variety of remarkably useful statistics. If there is only a single earnings call for industrial REIT investors to listen to, it should be this one.

Unrecognized Predictive Power

Each year PLD reports earnings very early in the earnings season and each year the other industrial REIT results are directly correlated with Prologis’ results. To me this correlation seems causal in nature and it should be obvious. PLD owns a substantial portion of the real estate so their performance is probably going to be similar to overall performance of the sector.

Despite the demonstrated predictive power, the market does not seem to recognize the correlation. For instance, PLD’s first quarter earnings reported on 4/18/23 knocked the cover off the ball yet most industrial REITs were down. It affected PLD stock positively, but did not seem to have much impact on the rest.

E-Trade streamer at 1:34 central 4/18/23

The average industrial REIT, excluding Prologis was down 0.61% at the time of the intraday reading.

At that same time the Vanguard Real Estate ETF ( VNQ ) was only down 0.27%. So somehow, despite the wonderful news for the industrial sector, industrial REITs underperformed their index.

How to take advantage of the unrecognized bellwether

When Prologis reports there is an infusion of fresh information and this information, as seen in the pricing action above, is not priced into industrial REITs.

Thus, there is a window of time in which to trade on this information while still paying market prices as if the information was not yet known.

In this particular instance, I think the trade is quite clear: Buy industrial REITs.

Bullish new information

PLD’s 1Q23 contained both obvious and subtle positives. Let me begin with the obvious.

Occupancy came in high at 98% and the leasing activity was astounding with all time high same store NOI growth.

PLD

2022 rent increases were phenomenal in the 30%-70% range for most industrial REITs, but they were broadly considered to be fleeting. Specifically, there were 2 theories that made the market think the extreme rent growth would not last:

- New supply coming in

- Amazon subleasing being the tip of the iceberg

Thus 2023 rent growth coming in even hotter than 2022 is unexpected. PLD had 68.8% rent roll ups on new leases and the part that is more relevant to the other industrial REITs is the U.S. portion which came in at +78.8%.

This represents growth acceleration rather than the deceleration that was expected.

More subtle bits of information point to a longer runway of growth

The previous industrial boom market ended badly with a glut of speculative supply built right before the financial crisis.

With the extreme rent growth of the past few years many, myself included, have been worried about similar overly ambitious development again this cycle. However, the numbers presented by Prologis indicate that the supply is much more disciplined this time around. First, we can look at PLD specific numbers.

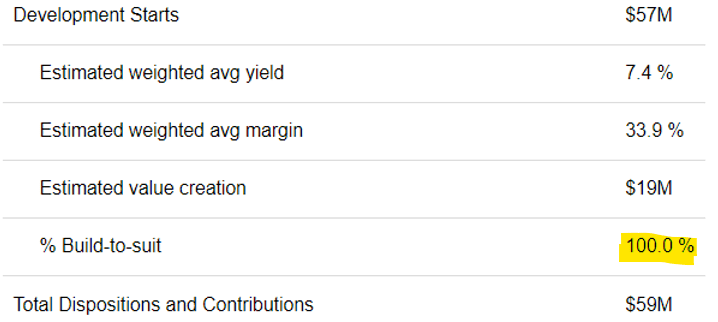

Their square footage delivered in 1Q23 came in slightly better than underwriting with strong yield and margin.

PLD

Note in yellow above that 51.6% of the volume was built to suit. That is the stuff that finished being built in the quarter. Compare that to the properties PLD started building during the quarter.

The 7.4% estimated yield indicated PLD tightened its underwriting which is further bolstered by the 100% build-to-suit.

{kind=link}

They stopped building on spec, only building when the property is pre-leased.

This is good news because Prologis was one of the culprits of the oversupply before the financial crisis. Prologis also presented more national numbers on the conference call.

Chris Caton:

“I want to be very clear. So let's talk about net absorption in the 30 markets where Prologis operates in the United States -- Last year, net absorption was 375 million square feet. We call that at 275 this year, and we expect a similar or perhaps higher numbers of macro environment clarifies and some of the decisions that get delayed this year land into '24. So that will be on the demand side. We have a bit of clearer view as we look out to '24. But starting with 2022, 375 million square feet of supply as well, that's deliveries. We expect 445 million square feet of deliveries this year as a supply pipeline empties and that will fall sharply, perhaps by half or more into 2024. And so when you put these numbers together, you'll see the vacancy rising from low 3s last year to 4 or a bit higher later this year and then back into the mid-3s.the mid-3s.”

So supply growth will slightly outpace demand growth in 2023 and demand is slated to outpace supply growth in 2024 resulting in occupancy staying very high relative to history.

The 2023 deliveries are a result of the strength in industrial leasing which incentivized development, but more curious to me is the slowdown of deliveries for 2024.

My hunch is that there are 2 sources of the more disciplined supply:

- Developers remember what happened in the financial crisis and are thus more wary of building on spec

- Amazon announced a slowdown in their e-commerce business

In April of 2022, Amazon released the shot heard throughout the entire industrial sector. They said that they were going to slow their expansion in e-commerce real estate leasing and perhaps even more dangerous was their suggestion that they would sublet existing rented space.

Industrial REITs collapsed upon this single news item.

{kind=link}

Perhaps developers also got scared off resulting in the relatively muted deliveries in 2024.

If that is the case, this was a blessing in disguise as it has extended the highly favorable leasing environment by keeping supply relatively low and occupancy in the high 90s.

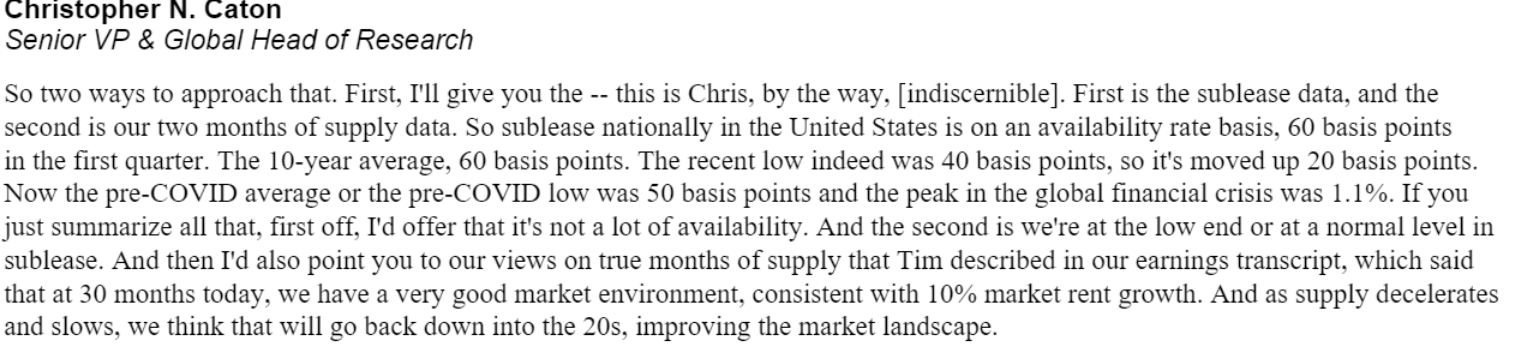

The actual fundamental impact of Amazon’s subleasing seems to be minimal. This can be seen in the actual leasing numbers discussed earlier, but Chris Caton of PLD gives a bit more color on the situation.

{kind=link}

Essentially subleasing activity is sitting right at the 10 year average of 60 basis points. Amazon was loud with their announcement but not much has come of it.

Market Rent Growth

PLD anticipates market rent growth of 10% in the U.S. and 9% globally. They expect this number to accelerate into 2024.

Since market rent is already substantially above current lease rates, the growth in market rent will take mark to market to about 80% for PLD in 2024.

Clear relevance to other industrial REITs

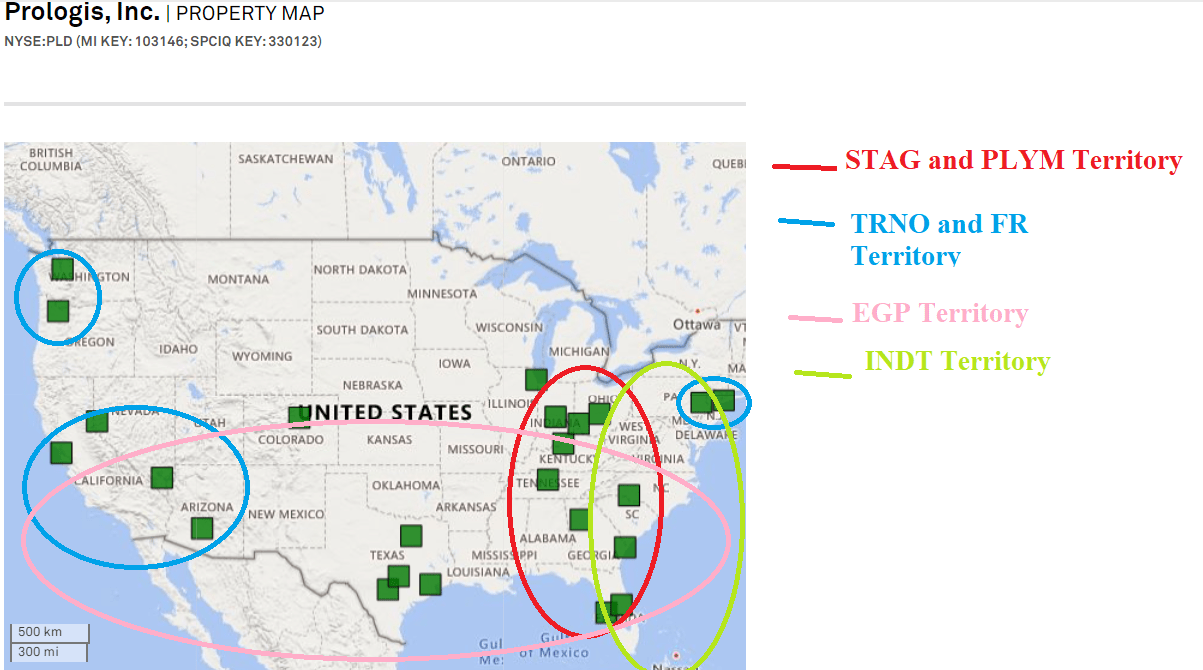

In the U.S. alone, Prologis owns 3803 buildings. They report these in portfolios of buildings which sit as follows on the map.

Source: Map by S&P Global Market Intelligence – circles added by Dane Bowler

{kind=link}

Each of the major industrial REITs has full overlap between their main areas of business and submarkets in which PLD has substantial ownership.

This isn’t Apple versus Samsung where one gaining market share is bad for the other. Industrial properties are not all that different from one another. These properties are fungible so if Prologis had huge rent rollups in its markets, I think it is very likely these other REITs are experiencing the same thing.

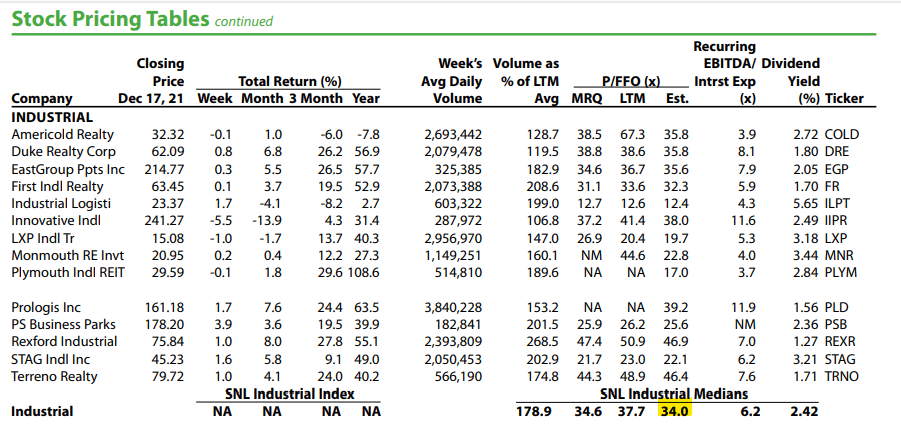

Back at the end of 2021 when industrial was viewed as having strong growth ahead the sector traded at a median multiple of 34X.

{kind=link}

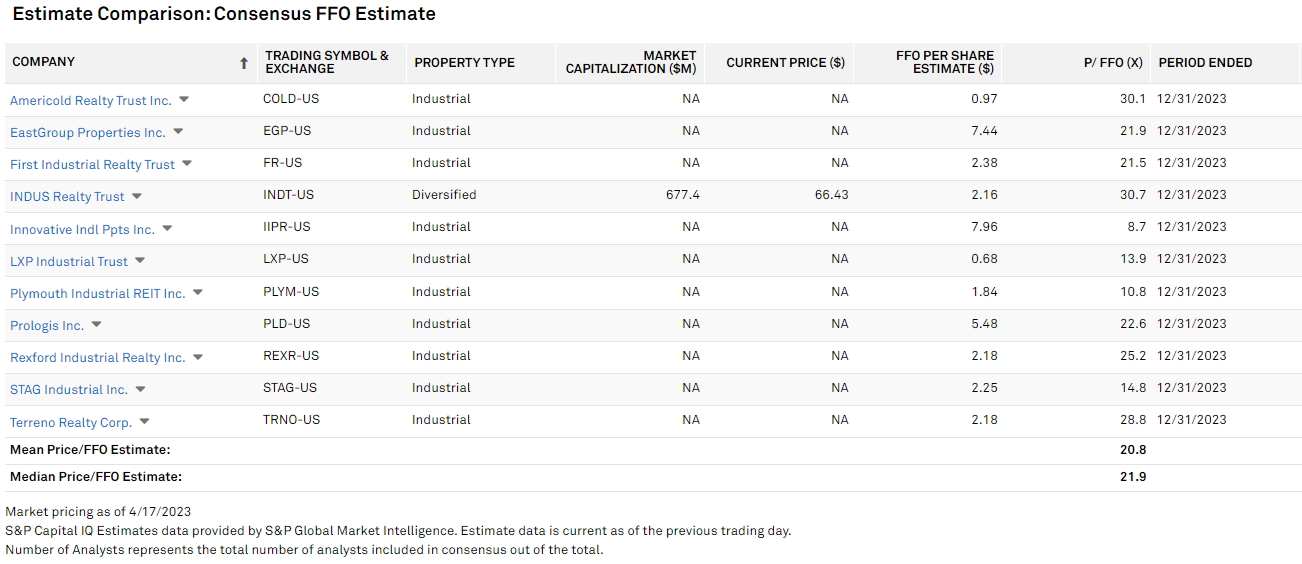

Today, industrial REITs are sitting at a median multiple of 21.9X.

{kind=link}

As far as I can tell, the growth outlook is similar.

34X was probably too high of a multiple, but 21.9X strikes me as a bit too cheap given the rent growth ahead. The mark to market opportunity alone creates growth for the next 7 years.

For further details see:

Prologis: The Unrecognized Bellwether