PUMP - ProPetro Holding Corp.: Revving The Engines

2023-07-29 08:00:00 ET

Summary

- ProPetro Holding is doing a lot of things right, but we think that an earning miss may provide a better entry point.

- PUMP stock has several catalysts for the next few quarters into 2024.

- The macro-environment has us holding ProPetro Holding for now, but at a slightly lower price, we would make a move.

Introduction

Despite the rig count dropping, and the frac spread count staying on a fairly flat trajectory, the shares of land drillers and frackers have been on the rise.

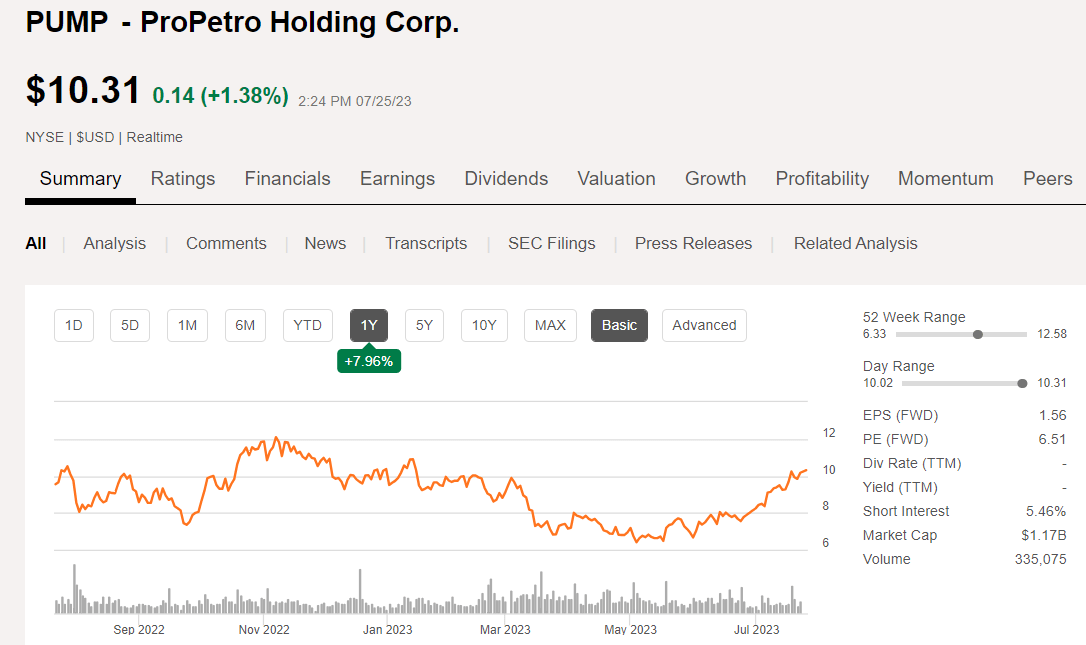

Price Chart for PUMP (Seeking Alpha)

{kind=link}

ProPetro Holding Corp. ( PUMP ) is no exception, up 50% since June, on mostly negative news for its only market, North America. A contrarian move if I ever saw one. Analyst expectations for PUMP are mostly booked at this point, with the remaining upside toward $16.00 being a bit dubious in my estimation. I have written the company up several times previously, the last two times with a buy rating. Please have a look at that older work as well.

PUMP has a history of missing EPS estimates in recent times, including those halcyon days of 2022 when we thought everything oilfield was going to the moon. Remember that? Accordingly expectations for Q-2 are for EPS to come in at $0.40 per share, down from $0.45 in Q-1. Since they missed Q-1 by $0.20 per share, one can't the blame the analysts for their cooling ardor.

In this article we will review the last quarter and make our own estimate of what to expect from the company when they report Q-2 on August, 2nd.

The thesis for PUMP

If you are a believer in the Permian basin, PUMP may be for you, as they are a pure-play, middling sized Permian pumping company. As we discussed in the Technology article earlier this month, frackers are benefitting from increased "completion intensity." What that means is there are more stages being pumped, and more sand per foot of interval being injected into the rock. That's the good stuff.

What's not so good is the shrinkage in the rig market that's occurred during the first half of the year. We're down 102 rigs from the start of the year , but we have gained 25 frac spreads , signifying there are still DUCs being turned to sales. Analyst firm Spears and Associates, to whom I frequently refer, sees continued weakness during the year in NorAm fracking. If they are right, and companies pay big money to get their research, frac companies have at least a quarter or two of declining revenues and margins to wade through before the good times roll once more.

The upshot is at some point all these frac spreads are going to run out of holes to stimulate, and the spot market for fracking is going to fire up. That will send some of these 275 frac spreads to the yard as opposed to the next rig site.

Frac King, Halliburton, ( HAL ) has pretty well clued us in here in their Q-2 report. Jeff Miller, CEO comments on North America.

North America revenue grew 11% versus the same period last year, and margins were sequentially flat versus the last quarter. Looking ahead into the second half, I expect overall market activity in North America will be slightly lower than in the first half.

Source .

A Few Catalysts for PUMP

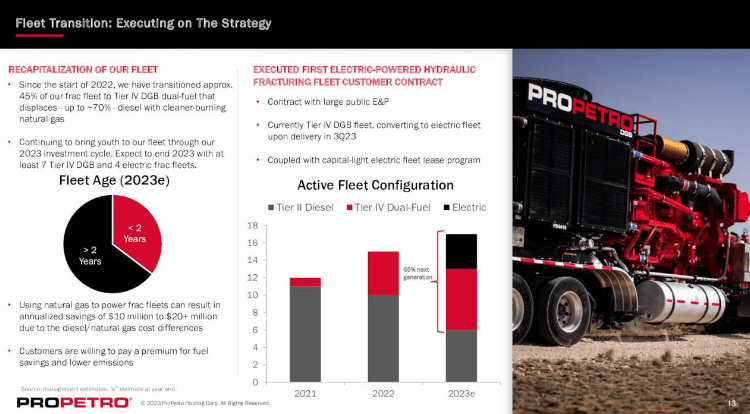

The company has seen the light and understands the future of fracking is gas and electric. With 2 of 4 electric fleets arriving in Q3, and the final two by year's end, PUMP finds itself ahead of the electrification curve. Only slightly down the evolutionary ladder are the Tier IV DGB units that will result in opex savings of $10-20 mm per year over diesel costs. 6-DGB fleets adds up to $60-120 mm per year, a not insignificant sum. Also, with this conversion, 140K horsepower is leaving the market permanently, as noted by CFO David Schlormer in the Q1 call:

We plan to retire approximately 140,000 hydraulic horsepower of Tier 2 conventional diesel frac equipment during 2023. These retirements will be scrapped and will not return to service.

Fleet Transition for PUMP (PUMP)

{kind=link}

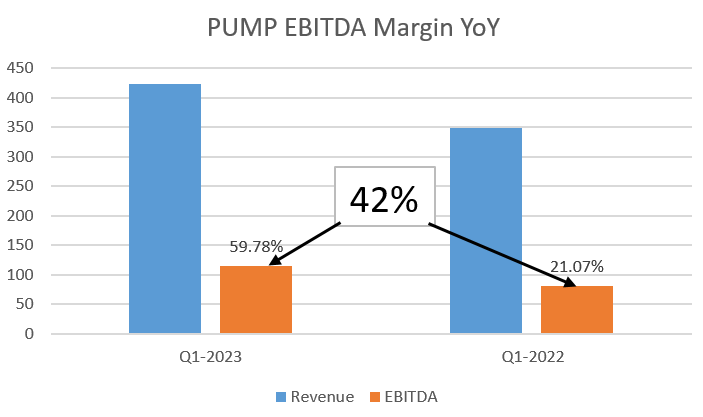

EBITDA margin has risen dramatically YoY to nearly 3X of a larger figure. This only explained by rising prices, and ancillary services.

PUMP EBITDA Margin (Data-Seeking Alpha, Chart-Author)

{kind=link}

Finally, there is the M&A potential. When an acquisition is immediately accretive, it just makes sense in this environment. The Silvertip deal logged in Q4, 2022 is an example of a solid transaction. Details include a drive-out value of ~$150 mm, including 10.1 mm shares of stock, $37 mm in cash and debt. There is strong evidence that PUMP's expectations of increased EBITDA conversion rates to free cash at double their standalone value, are bearing out. As someone who's seen wireline tickets, I was always in awe of what they were able to get away with charging. Schlumberger wireline hands got a percentage of the ticket-2%, and were making a $100K in the field decades ago. I don't know if that practice is still prevalent. Putting on my Forest Gump hat, Logging and Pump Down services go with Stimulation like "Peas and Carrots." Nearly every frac pumper is also in the logging and pump down business for that same reason.

Note- if you are wondering about pump down, remember these wells go 1000's of feet horizontally. If you want to get a plug or gun to bottom on wireline, you have to...wait for it, pump it down .

Sam Sledge, CEO endorsed this M&A thesis in the Q-1 call:

We are evaluating accretive M&A opportunities to strengthen our position as a leading completions focused oilfield services company. We are confident that ProPetro is well positioned to take advantage of this ongoing industry evolution in the Permian Basin, and we continue to take the necessary steps to achieve this industrialization within our own business, especially through moves like our e-fleet transition

The market is hot for M&A of this sort right now - witness Patterson-UTI Energy ( PTEN ) and NexTier Oilfield Solutions ( NEX ). Valuations are still depressed in this sector relative to cash flow being generated, and it won't surprise me at all to see further activity in this sector.

Q1 2023 and Guidance

PUMP generated $424 million of revenue, a 21% increase from the $349 million generated in the fourth quarter of 2022. This increase was largely attributable to increased utilization, improved net pricing across the service lines, the full quarter effect of Silvertip's revenue contribution and the frac fleet repositioning effort that was undertaken in the fourth quarter of 2022.

Effective fleet utilization of 15.5 fleets for the first quarter of '23 was at the top end of their prior guidance of 14.5 to 15.5 fleets, and steady fleet utilization is expected through the second quarter of '23. The company notes that its frac fleet remains effectively sold out for the coming quarter. Guidance for second quarter frac fleet utilization is 15 to 16 fleets with steady activity in the wireline and cementing businesses as well.

Effective January 1, 2023, the company began to record utilization of fluid ends as an operating expense rather than capital expenditure. This change to fluid ends expensing was made after an analysis of the useful life for these components and was implemented prospectively. My guess is that these are being traded out at greater rates due to the longer wells and higher treatment rates occurring now.

The company posted net income of $29 million or $0.25 per diluted share, the company's highest in over 3 years compared to net income of $13 million or $0.12 per diluted share in the prior quarter. Adjusted EBITDA increased 42% sequentially compared to $84 million in the fourth quarter and incremental adjusted EBITDA margins were nearly 50%.

During the quarter, PUMP incurred $97 million of capital expenditures. Actual cash used in investing activities, as shown in the statement of cash flows for capital expenditures, net of proceeds in the first quarter was $114 million, with free cash flow of negative $41 million. CapEx is expected to be between $250 million and $300 million weighted towards the front half of this year.

As of March 31, 2023, total cash was $45 million and the company had borrowings under the ABL credit facility of $30 million. Total liquidity at the end of the first quarter of '23 was $149 million, including cash and $104 million of available capacity under the ABL credit facility. As of May 1, 2023, our cash balance was $82 million and we had $60 million of borrowings under our ABL and $166 million of total liquidity. We expect our liquidity to continue to improve, along with our enhanced profitability and lower capital spend as we move into the second half of this year.

PUMP has instituted a capital-light long-term lease agreement to support their fleet transition strategy to electric and natural gas-powered equipment, coupled with long-term customer contracts that share capital costs for these value-enhancing assets.

Risks

The key risk for a single basin pumper is a fall-off in activity in that basin. That's not likely for the Permian as it is the only basin still logging gains in daily output. But, it's a risk that must be noted.

Your takeaway

Given what we know about the somewhat dour outlook for the broader OFS market in North America, I am not inclined to jump into ProPetro Holding ahead of earnings. That said, it wouldn't take much of a post-earnings down draft for me to pull the trigger on PUMP.

Once we get WTI prices to sustain over $80 for a month or two, expectations are going to ramp up for companies like PUMP. If we are going to move in, it should be prior to that, but there's still some time to monitor the company's progress pre and post earnings.

Accordingly, I think ProPetro Holding is a hold at current levels, but one we will definitely keep an eye on, and perhaps but in a low-ball order on the 2nd.

For further details see:

ProPetro Holding Corp.: Revving The Engines