OCSL - Prospect Capital: Why I Am Doubling Down On This 12% BDC Yield Before The End Of 2023

2023-12-21 03:03:08 ET

Summary

- The central bank's announcement of interest rate cuts in 2024 caused stock prices to fluctuate.

- Prospect Capital is a business development company that may benefit from the change in interest rates.

- PSEC has a lower percentage of floating-rate loans and solid credit quality, making it an attractive passive income investment.

The central bank caused stock prices to surge last week after it made known at its December policy meeting that it sees key interest rates come down by 75 basis points in 2024 which marks a major pivot away from its current interest rate policy.

Business development companies that could profit from a change in interest rates are those BDCs that have relatively low floating-rate loan percentages included in their investment portfolios, like Prospect Capital Corp. (PSEC).

Prospect Capital has a lower percentage of floating-rate loans in its portfolio than other BDCs, yet sells for a much larger net asset value discount. Prospect Capital's credit quality also remained rather solid in the last quarter.

Furthermore, the BDC covered its dividend with net investment income comfortably in 2023 and, taking into account Prospect Capital's substantial excess dividend coverage, I would think that the $0.06 per share per month dividend is sustainable for at least a couple more quarters.

My Rating History

Prospect Capital was a Buy for me, considering the presence of a large discount to net asset value in the market.

The BDC covered its dividend with net investment income well and had decent credit quality overall. Prospect Capital's stock price tanked ahead of earnings but has since recovered. With that said, though, a large NAV discount is still available for passive income investors and Prospect Capital's credit quality improved QoQ.

Now that the central bank has announced it will pivot away from its high interest rate policy, pure floating-rate BDCs have become less attractive for passive income investors.

Taking into account Prospect Capital's solid dividend support, provided by the company's net investment income, I think PSEC might be a passive income instrument that is attractive for investors even in a low-rate environment.

A Deeply-Discounted Passive Income Play With A 12% Yield

Prospect Capital was and is not my favorite BDC and I rated it a Sell last year primarily because the BDC has a poor record in growing its net asset value in the long term. As a consequence, Prospect Capital's common stock has been priced at a much larger-than-average discount to net asset value.

With that being said, though, the portfolio contains enough first lien debt and a low amount of floating-rate loans, relative to other BDCs, that I think PSEC could be an attractive passive income investment for 2024.

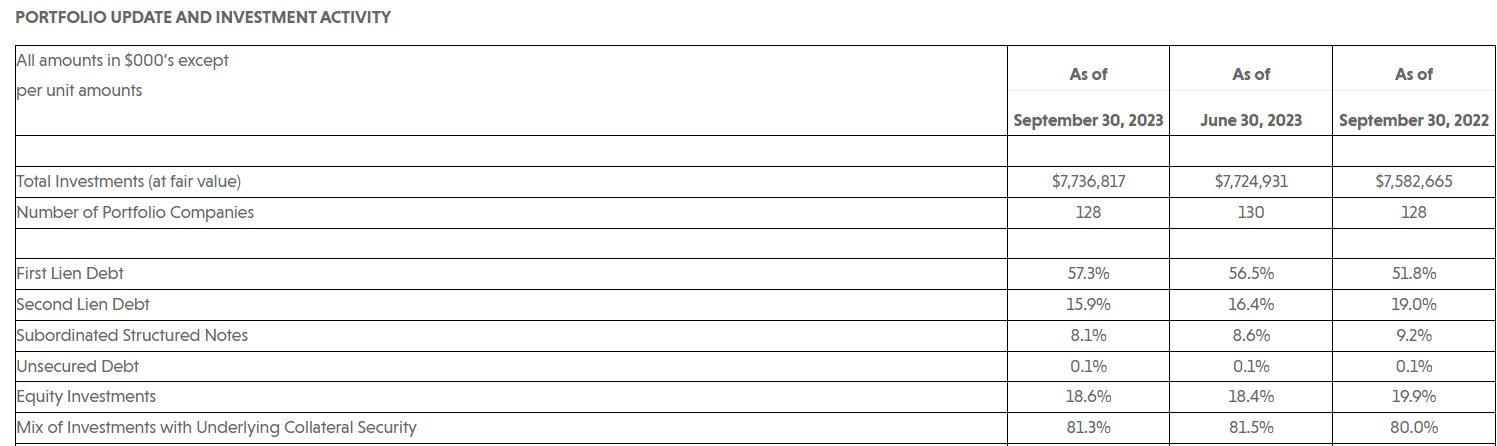

The three largest investment categories in Prospect Capital's portfolio are first lien debt (57.3%), second lien debt (15.9%), and equity (18.6%). The large equity representation has the potential to boost Prospect Capital's total return potential but does not add regular income to the company's cash accounts. The core focus still is, and will probably remain senior secured debt.

Portfolio Update And Investment Activity (Prospect Capital Corp)

{kind=link}

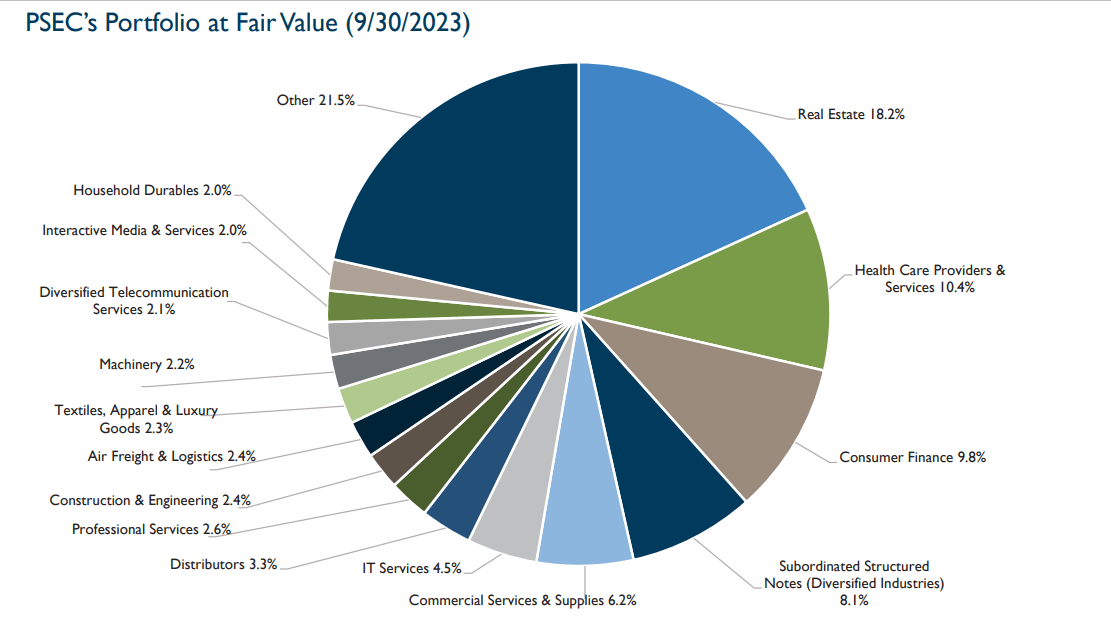

Prospect Capital is well-diversified and the portfolio includes loan investments in 36 different industries, mostly real estate, health care, and consumer finance. Some of the industries, like real estate and consumer finance, have cyclical earnings risks which could affect the BDC's dividend coverage detrimentally during an economic downturn.

{kind=link}

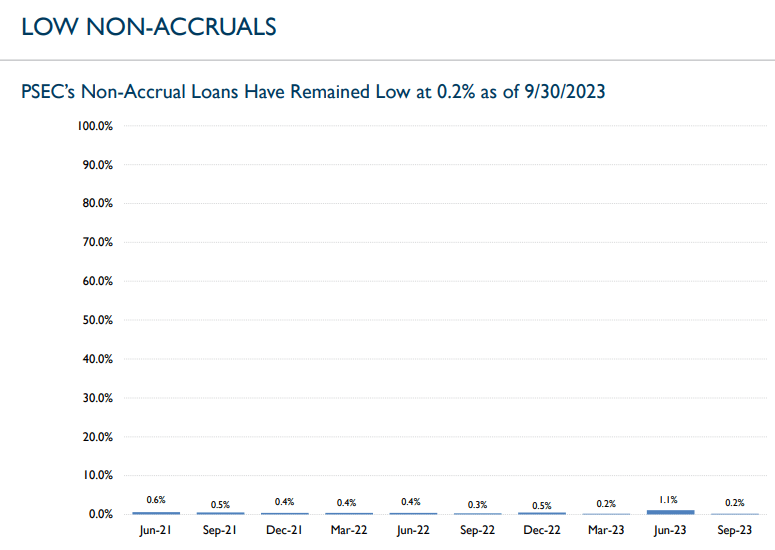

As far as portfolio quality is concerned, Prospect Capital's collection of investment loans looks reasonably good: The non-accrual ratio in the last quarter dropped to 0.2% meaning the BDC has almost perfect credit quality (and the non-accrual ratio improved rather substantially QoQ). The average non-accrual ratio in the last ten quarters was below 0.5%, implying a reasonably high degree of overall loan quality in Prospect Capital's debt investment portfolio.

Low Non-Accruals (Prospect Capital Corp)

{kind=link}

Relatively Limited Floating-Rate Exposure

Most BDCs saw the rate-hiking cycle coming and invested according, by pushing investments in floating-rate loans. Most BDCs, as a consequence, have now very concentrated floating-rate loans including companies like Golub Capital BDC ( GBDC ) , whose portfolio is 99% floating-rate, Goldman Sachs BDC ( GSBD ) , 100% floating-rate, and Blue Owl Capital Corporation (OBDC) , which is 98% floating-rate.

Prospect Capital, on the contrary, had 83% floating-rate exposure meaning the BDC's debt investment portfolio has less interest rate and net investment income risks than other BDCs with higher representations of floating-rate investments.

With the central bank now essentially guiding for 3 rate decreases in 2024, BDCs with less capital tied up in floating-rate debt investments and substantial equity positions are preferred BDCs for me to invest in before the New Year.

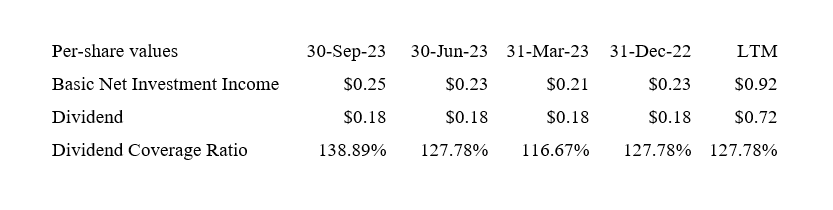

Dividend Coverage Suggests The $0.06 Per Share Dividend Is Sustainable

Prospect Capital's dividend metrics look good enough to me to suggest that the BDC can sustain its $0.06 per share per month dividend payout even in an environment of slipping interest rates. The BDC earned 139% of its dividend in the last quarter and 128% in the last year.

Dividend (Author Created Table Using BDC Information)

{kind=link}

Spotty Dividend Record Makes Prospect Capital A Higher-Risk BDC

Prospect Capital managed to pay a decent dividend in times when its net investment income exceeded its dividend. Prospect Capital has been a serial dividend cutter, however, and the BDC does not deserve as much trust as other BDCs which have a less spotty dividend record.

During times of temporary net investment income declines, Prospect Capital was quick to adjust its pay-out which is reflected in the BDC's long-term dividend growth chart.

Exaggerated Discount To NAV

Prospect Capital presently sells for a 35% discount to net assets whereas the other BDCs that I have mentioned here sell for either discount to net asset value or for a tiny premium (in the case of Goldman Sachs BDC). The 35% discount does not property reflect, in my view, that Prospect Capital's credit quality improved in the last quarter.

All things considered, Prospect Capital sells for an exaggerated discount to net asset value, a fact that makes buying PSEC even easier.

A solid gauge of a BDC's intrinsic or fair value is the reported net asset value. Prospect Capital's net asset value as of September 30, 2023, was $9.25, which reflected a $0.01 per share increase QoQ. In the long run, I do think it is reasonable to propose that Prospect Capital's stock could re-rate to its net asset value, as long as its credit quality remains top, that is.

Another BDC that I think can profit from the Fed's interest rate shift is Oaktree Specialty Lending ( OCSL ) which had a floating-rate percentage of 86% as of the end of the third quarter. Oaktree Specialty Lending, however, is selling for a 3% NAV premium. Taking into account Prospect Capital's larger net asset value discount and higher margin of safety, I'd choose PSEC for its re-rating potential. I do have a Hold opinion on Oaktree Specialty Lending.

The Central Bank Is Saying Goodbye To High Rates

Prospect Capital still has net investment income risks since the BDC is overweight floating-rate loans, an exposure that I would think management will want to scale back moving forward.

Falling net investment income, however, is a headwind that affects all BDCs with those BDCs that have less capital invested in floating-rate loans having a better chance to outperform other BDCs, in my view.

My Conclusion

The central bank lit a fire under the stock market on Wednesday after it said that the market could expect 75 basis points worth of interest rate cuts next year which makes pure floating-rate BDCs less attractive for passive income investors.

Lower interest rates are good for the economy and Prospect Capital might see a restart of its loan origination business as well which suffered in the last year from slowing loan demand in a high-rate environment. Since Prospect Capital has less floating-rate exposure than other BDCs, I would think the BDC has less risk with regard to its net investment income.

The dividend so far has been well-covered by net investment income and the present dividend of $0.06 per share per month appears sustainable to me.

Taking into account that Prospect Capital continues to trade at a much wider discount to net asset value than those BDCs with more substantial floating-rate exposure, I think Prospect Capital may have a chance to outperform its peers in 2024.

For further details see:

Prospect Capital: Why I Am Doubling Down On This 12% BDC Yield Before The End Of 2023