PB - Prosperity Bancshares: Likely To Highly Reward Investors In A Lower Rate Environment

2023-12-15 18:12:29 ET

Summary

- Prosperity Bancshares has underperformed the S&P 500 due to negative market sentiment over regional banks and high interest rates.

- The bank's conservative business model and resilient performance during the Great Recession make it a reliable investment.

- Lower interest rates, the booming economy of Texas, and recent acquisitions position Prosperity Bancshares for future growth.

About a year ago, I recommended purchasing Prosperity Bancshares ( PB ) for its exemplary management, its promising growth prospects and its cheap valuation. Since my article, the stock has underperformed the S&P 500 by a wide margin, as it has offered a total return of -5% whereas the S&P 500 has rallied 27%. The pronounced underperformance has resulted primarily from the extremely negative market sentiment over regional banks, as the stock of Prosperity Bancshares has performed in line with the SPDR S&P Regional Banking ETF ( KRE ) s ince my article.

The underperformance has also resulted from the impact of 16-year high interest rates on the net interest margin of most regional banks, including Prosperity Bancshares. However, the Fed recently stated that it expects 3 interest rate reductions in 2024, thus causing the 10-year treasury yield to plunge below 4.0%. Therefore, it seems that the worse is behind the regional bank with respect to interest rates. Given also its reliable business model, its recent acquisitions and its cheap valuation, Prosperity Bancshares is likely to highly reward investors whenever interest rates moderate.

#1 Reason behind the underperformance: Negative market sentiment over regional banks

A major reason behind the underperformance of Prosperity Bancshares is the collapse of Silicon Valley Bank, Credit Suisse and First Republic. The bankruptcy of these banks triggered an indiscriminate sell-off of regional banks, which were viewed by investors as vulnerable to a potential bank run.

However, Prosperity Bancshares has an exemplary management, which follows a conservative, defensive business model. To be sure, in the Great Recession, the worst financial crisis of the last 90 years, when most banks incurred outsized losses and cut their dividends, Prosperity Bancshares remained highly profitable and continued growing its dividend thanks to its resilient business model.

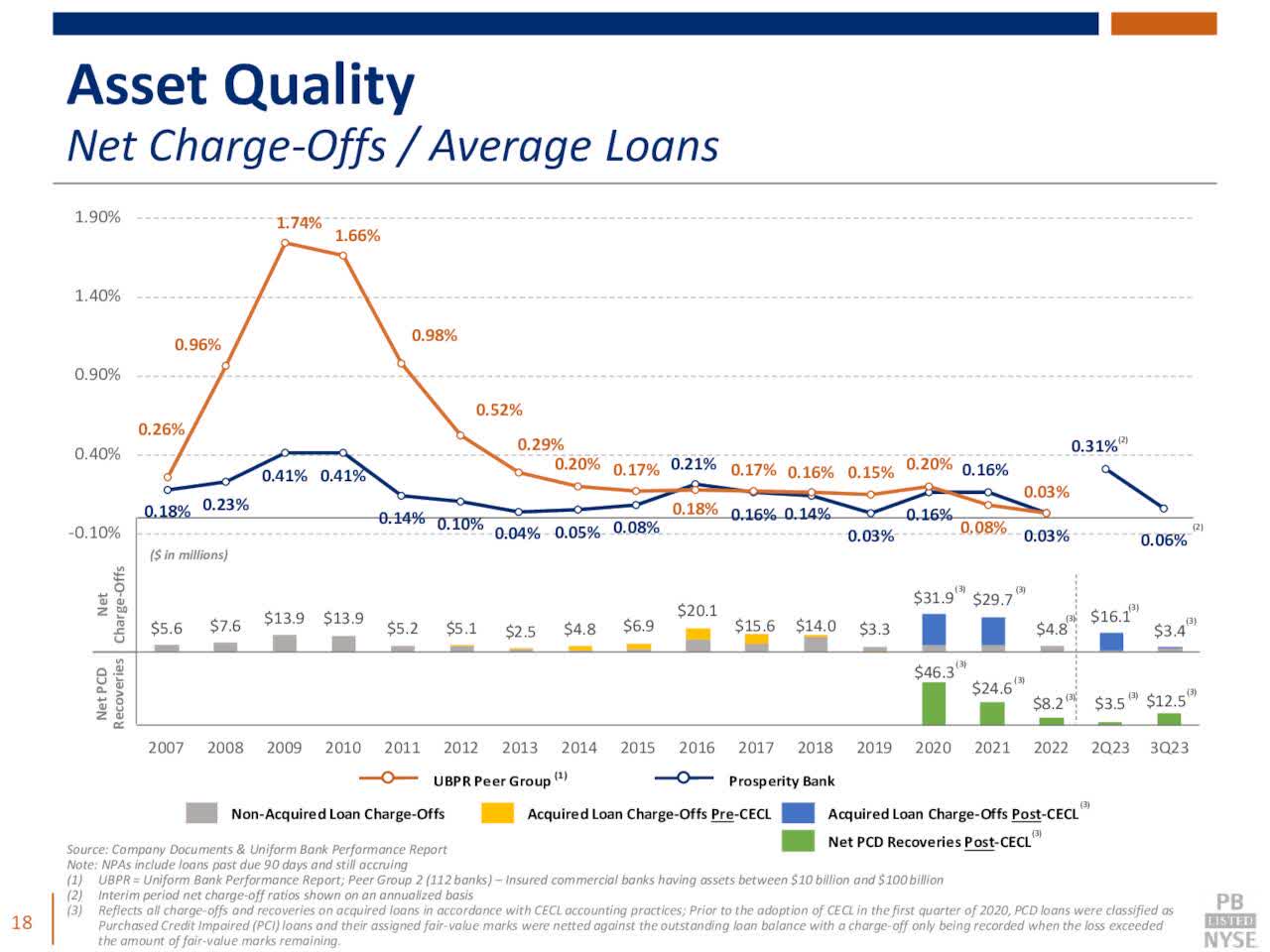

Asset Quality of Prosperity Bancshares (Investor Presentation)

{kind=link}

Source: Investor Presentation

As shown in the above chart, the net charge-offs of most banks surged during the Great Recession but they remained contained in the case of Prosperity Bancshares.

In addition, Prosperity Bancshares is proving resilient to the ongoing downturn of the financial sector as well, as it has a completely different business model from the banks that failed. Those banks incurred severe losses in their investment portfolios due to the surge of interest rates, while they also had some large corporate depositors. When those depositors lost faith in the banks, they withdrew their money and thus caused a liquidity crunch to the banks.

Fortunately, Prosperity Bancshares has characterized 96.6% of its securities as “held to maturity”. Therefore, its losses from the surge of interest rates are only temporary in nature. As soon as its mortgage-backed securities mature, the paper losses will be eliminated. The depositors of the bank seem to have great confidence in its liquidity, as deposits have stabilized in the last two quarters.

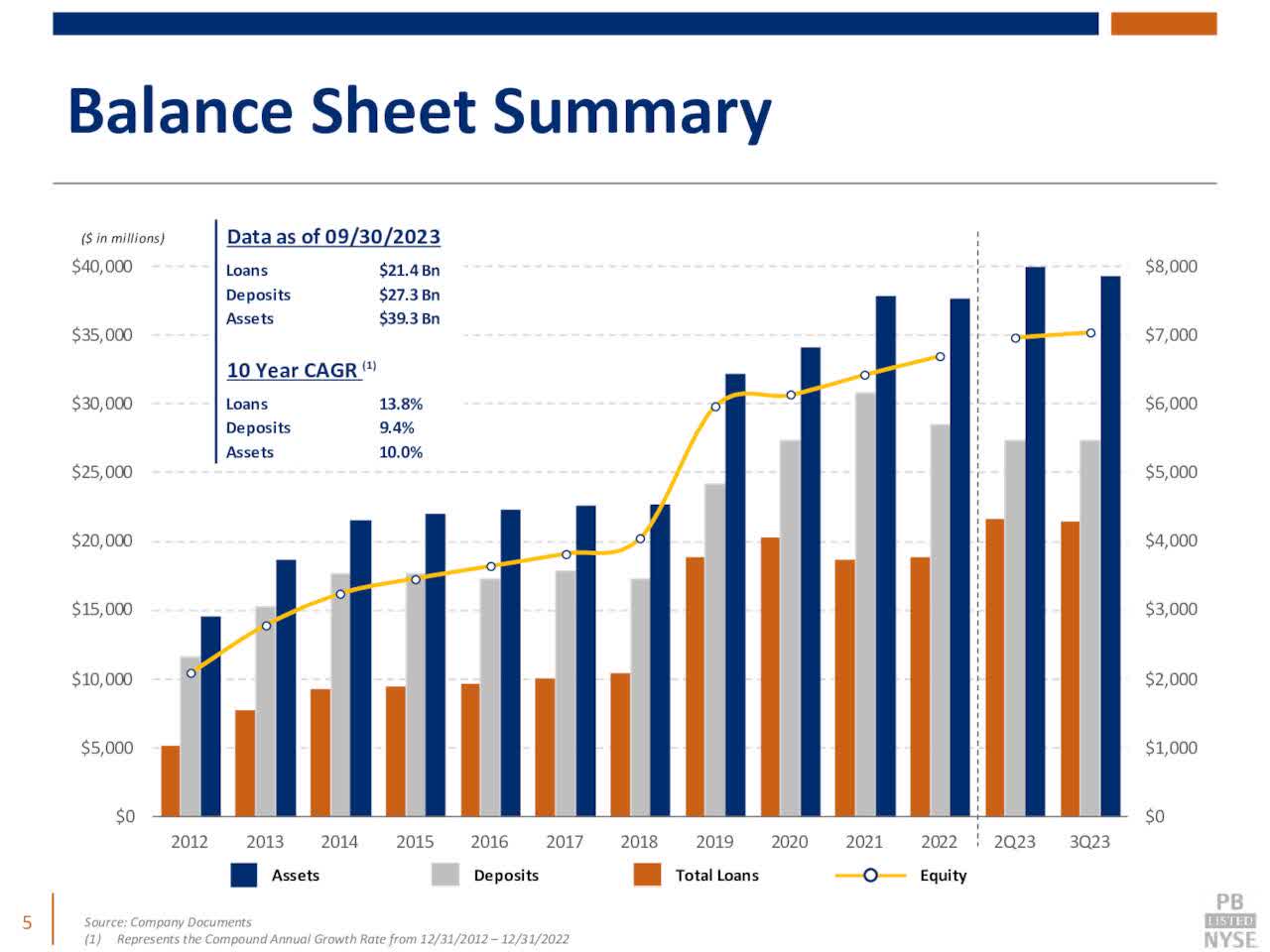

Loans and Deposits of Prosperity Bancshares (Investor Presentation)

{kind=link}

Source: Investor Presentation

Thanks to its conservative investment portfolio and the high-quality nature of its loans, Prosperity Bancshares has endured the ongoing downturn of the financial sector without any problem.

#2 Reason behind the underperformance: Lower net interest margin

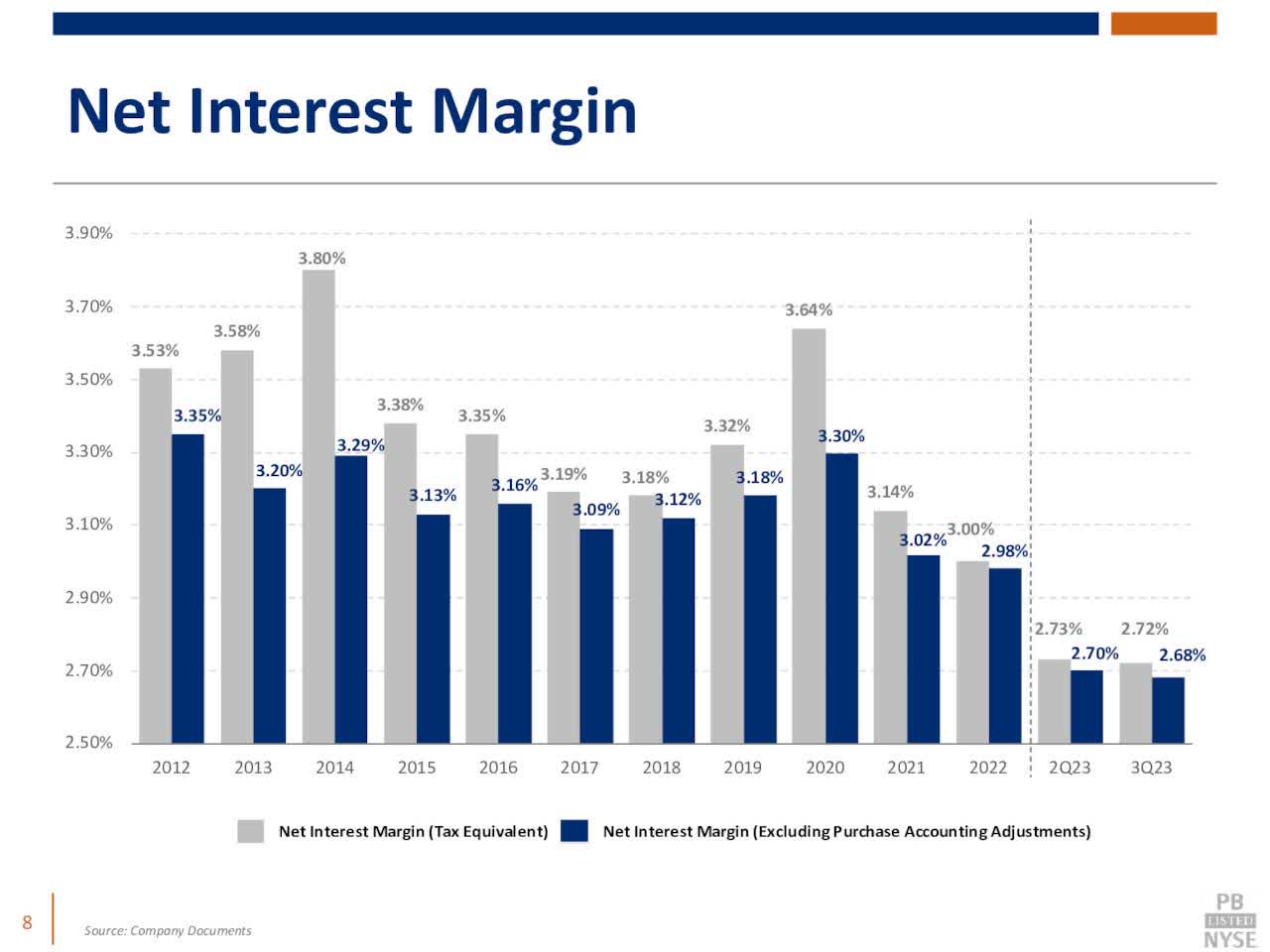

Due to the surge of inflation to a 40-year high, the Fed has raised interest rates aggressively since early last year. As a result, interest rates have climbed to 16-year highs and thus consumers have begun to demand high interest rates on their deposits. This has caused the competition among banks for deposits to intensify. Even worse, due to the tightening policy of the Fed, the total deposits in the entire financial system have decreased. As shown in the chart below, the heating competition among banks for deposits has caused the net interest margin of Prosperity Bancshares to shrink from 3.64% in 2020 to 2.72% in the most recent quarter.

Net Interest Margin of Prosperity Bancshares (Investor Presentation)

{kind=link}

Source: Investor Presentation

Due to the significant decrease in its net interest margin, Prosperity Bancshares is expected by analysts to incur a 14% decrease in its earnings per share this year, from an all-time high of $5.73 in 2022 to $4.93 this year.

However, it is critical for investors to realize that the worst is probably behind the bank with respect to interest rates. Inflation has decreased from a 40-year high of 9.2% in June 2022 to 3.1% now. As a result, in its latest meeting, the Fed stated that it expects 3 interest rate reductions (instead of one in its previous guidance) in 2024. Given also the well-known cyclical nature of interest rates, it is safe to expect them to deflate off their 16-year highs in the upcoming years.

Whenever interest rates moderate, the net interest margin of Prosperity Bancshares is likely to expand, as shown in the above chart. For instance, when interest rates were much lower than they are now, during 2012-2021, the net interest margin of the bank was 3.14%-3.80%. Therefore, the company has ample room to enhance its net interest margin off its current depressed level of 2.72% when interest rates revert to normal levels.

Growth prospects

Apart from the tailwind from the expected decrease of interest rates, Prosperity Bancshares has another growth driver, namely the booming economy of Texas, which is the second-largest state in the country, with more than 30 million residents. Texas has the fastest-growing population and one of the fastest-growing economies in the U.S.

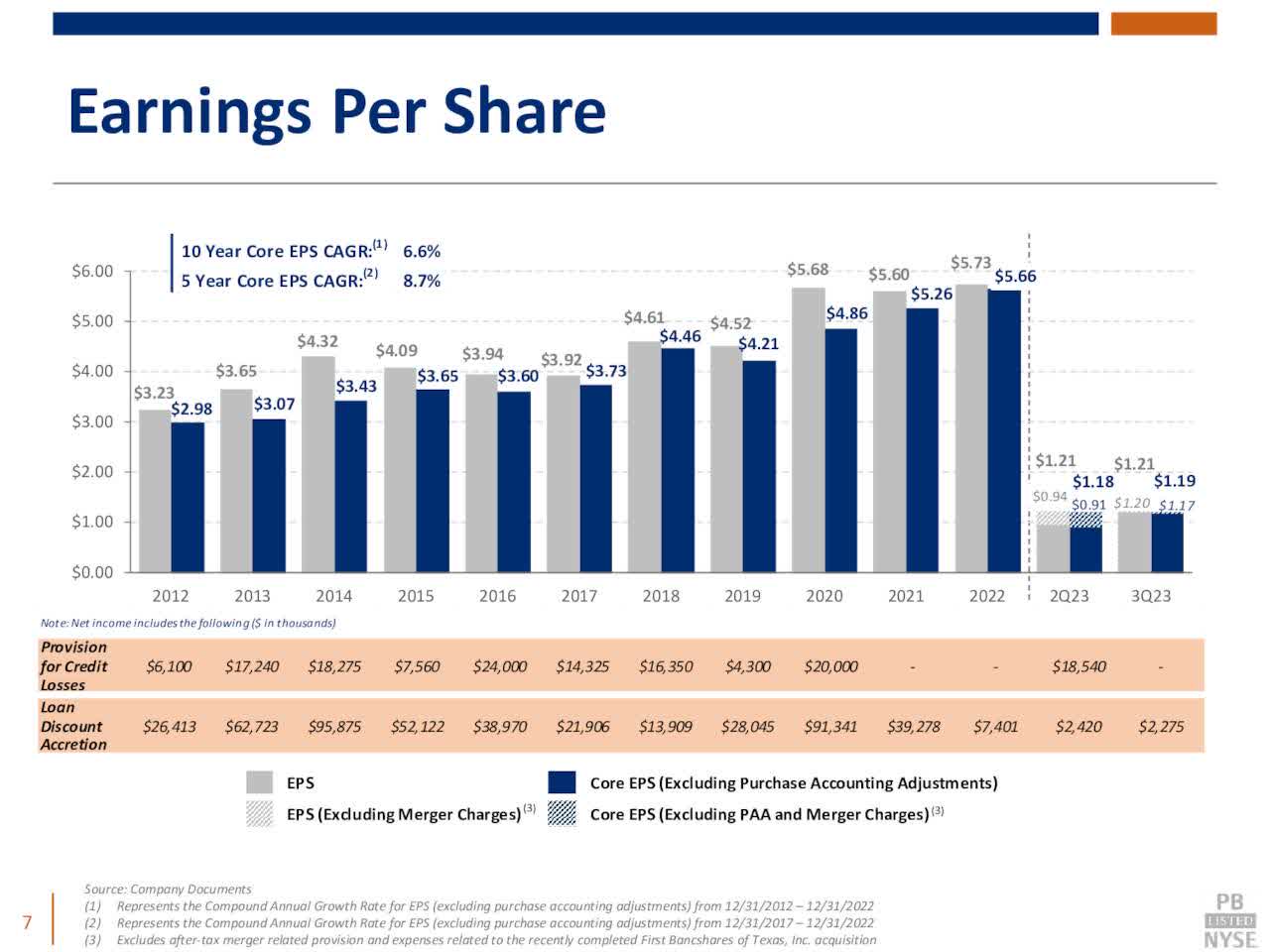

Thanks to this tailwind and its proven ability to acquire and assimilate smaller banks, Prosperity Bancshares has a solid performance record. It has acquired a total of 44 smaller banks and has grown its core earnings per share by 6.6% per year on average over the last decade.

EPS Growth Record of Prosperity Bancshares (Investor Presentation)

{kind=link}

Source: Investor Presentation

It is also wort h noting that Prosperity Bancshares acquired First Bancshares in April and Lone Star State Bancshares last year. Thanks to these acquisitions, Prosperity Bancshares has more than $6 billion of assets in West Texas and has become the largest bank in Midland and Odessa markets.

Overall, Prosperity Bancshares has promising growth prospects ahead thanks to the expected positive effect of lower interest rates, the booming economy of Texas and the recent acquisitions of the bank. Analysts agree on the promising prospects of the bank, as they expect it to grow its earnings per share by 5% in 2024 and by 16% in 2025, to a new all-time high of $6.00.

Valuation

Prosperity Bancshares is currently trading at 13.1 times its expected earnings in 2024. This valuation level is lower than the historical 10-year average of 14.3 of the stock. Moreover, the stock is trading at only 11.3 times its expected earnings in 2025. Furthermore, Prosperity Bancshares has missed the analysts’ earnings-per-share estimates only once in the last 20 quarters. Therefore, one can reasonably expect the company to meet or exceed the analysts’ estimates in 2024 and 2025.

The stock is trading at a cheaper valuation level than its historical average, primarily due to the negative market sentiment over regional banks and concerns about the impact of high interest rates on the net interest margin of the bank. As soon as interest rates begin to moderate, the valuation of the stock will probably revert towards its historical average. In fact, this is the reason behind the 35% rally of the stock in less than two months. Investors should purchase the stock before the market prices a greater portion of future growth in the stock.

Final thoughts

Prosperity Bancshares passes under the radar of most investors due to its conservative business model. It has also fallen out of favor in the investment community due to the exceptionally negative market sentiment over regional banks and the impact of 16-year high interest rates on the net interest margin of the bank. However, the recent pivot in the policy of the Fed is probably a game changer for the bank. Thanks to the expected benefit from lower interest rates, its solid growth potential and its cheap valuation, the stock is likely to highly reward investors in the upcoming years.

For further details see:

Prosperity Bancshares: Likely To Highly Reward Investors In A Lower Rate Environment