PROSF - Prosus: The Premium Is Still Not Justified Especially In This Environment

2023-09-08 04:34:00 ET

Summary

- Prosus is a tricky company to value due to its unique shareholder structure, which disadvantages investors outside of Naspers.

- The recent news of the likely unwinding of the cross-holding structure is a positive development but not significant enough to alter the company's prospects.

- Prosus continues to struggle with profitability, with none of its businesses generating noteworthy bottom-line profit, and its value is still heavily dependent on Tencent.

Dear readers/followers,

My coverage on Prosus ( PROSY ) has been both regular and unerring for the past 12-18 months, and I've been very clear on where I believe this company should be valued and what we should expect from the business. Prosus is a tricky company to value due to its relatively unique shareholder structure guaranteeing that shareholders outside of Naspers will never hold sway in the company. It's an inherently disadvantageous approach for Prosus investors - and the positive news here is that as of this article, we're seeing an improvement here (more on that below!).

In my previous articles, I've been clear about where I believe the premium and the price targets for Prosus should be - higher than €55/share hasn't been logical for me to estimate the company at any time, and looking at the share price performance since I set those targets, I find it hard to argue against the stance that I hold here.

Seeking Alpha Prosus RoR (Seeking Alpha)

In this article, it's time for my regular update. I know at least 5 of you want these updates for when I believe it's time to "go in" to the company, so I'm happy to give these to you.

Let's get going.

Prosus - Plenty to like, just nothing that makes the company a "BUY" Here

I first wrote about this particular company well early in 2022, when a reader contacted me and asked me to take a look at the company. What I found wasn't great - and I made that clear in my article.

However, despite some reader commentary, I maintain that despite we're seeing tech outperform and the NASDAQ move up, we're not seeing Prosus specifically outperform. Since very early on, I've held my discount thesis for Prosus. At this time, the discount I want to see for Prosus in order to invest in the business is over 50%. However, at one time during the coverage spectrum, the company was actually buyable to my share price target. If you had followed that and bought a sub-€55, you would have been at positive RoR now. Please note that €55/share is not my PT at this time, however.

I did not - there were better things to buy last summer and fall - but some did, and to those, I say congratulations.

So, recent Prosus results - and some of the most significant news for Prosus since I started covering it.

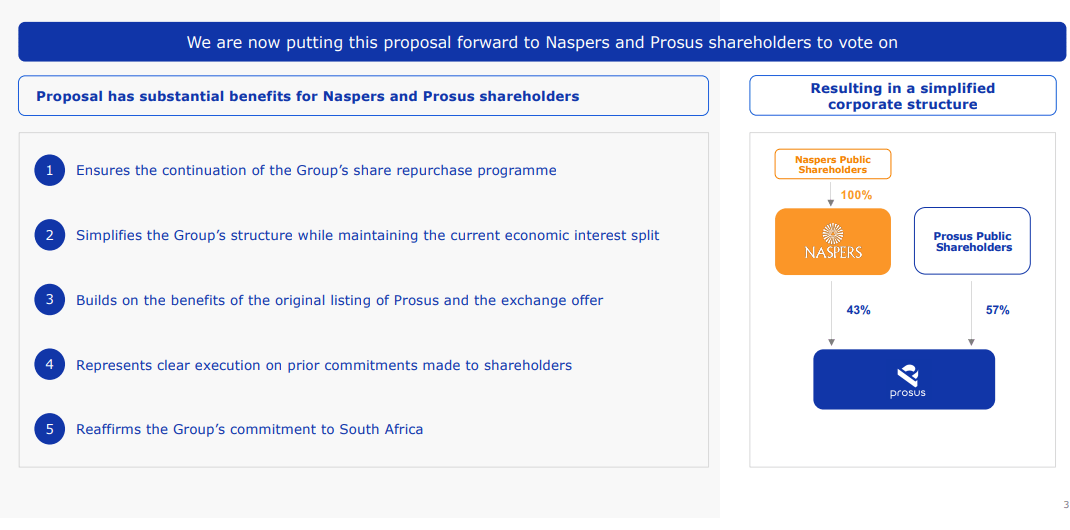

The cross-holding structure seems that it's likely to be unwound.

{kind=link}

The lack of a cross-holding structure will simplify the group's structure while maintaining the interest split, but in a much more traditional manner, with Prosus shareholders owning the majority of shares - but Naspers still at a voting interest majority of 72%. Its super-voting shares will remain, but the removal of cross-holding will simplify things here. This is a significant change, but the amount of "points" the two companies get for the move is next to zero - because it was only introduced to reduce Nasper's weight on the South African stock exchange.

It's basically only a reversal of a bad move. Good, but nothing life-altering.

How are things working on an operational level for Prosus?

{kind=link}

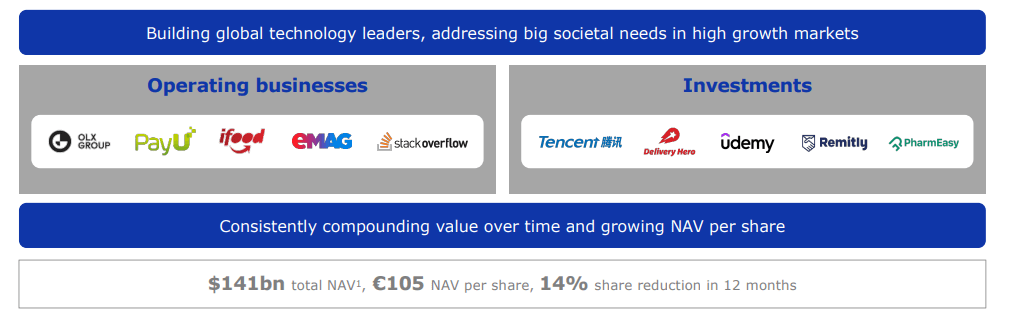

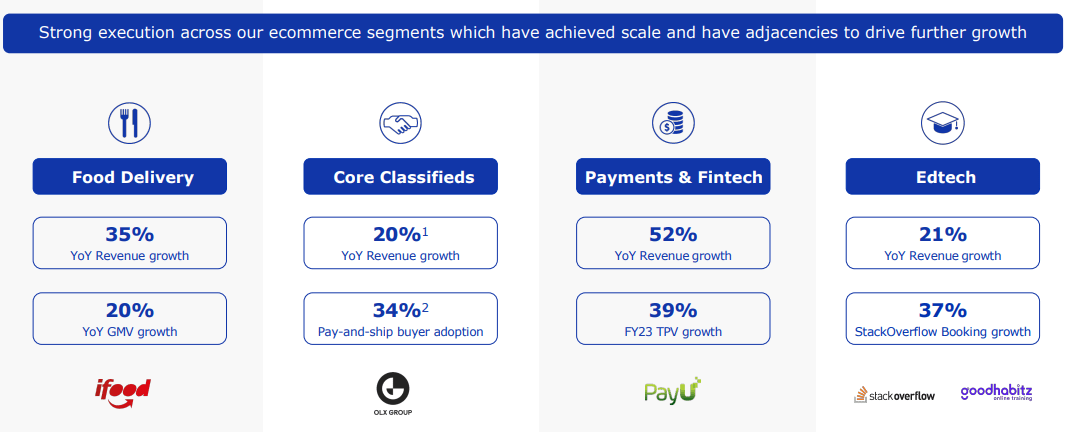

Essentially being a Tencent investment proxy because its other investments are ventures that are currently unprofitable, the company's results need to be taken in context. The company continues to beat the drum for "strong performance" from its food delivery, classified, payment/fintech, and edtech vectors...

{kind=link}

...and can be congratulated for being able to streamline things to some degree. However, as you can see above, the metrics the company focuses on are top-line. None of the businesses you see there manages to generate any noteworthy or any bottom-line profit whatsoever.

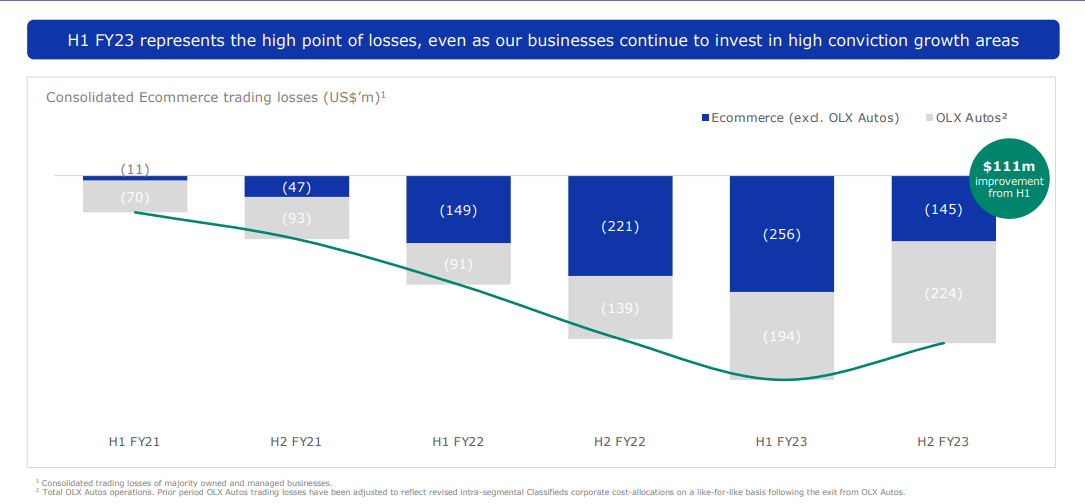

The current estimate for profitability in some of these segments is currently 1H25. And while the company has been able to move up from "trough unprofitability", improving, for instance, classifieds and e-commerce by about $111M on a YoY basis in terms of trading losses, the company is still far from any sort of profitability.

Since early 2021, none of these things has managed net profitability or a positive trading result.

{kind=link}

As I went through in my last article, any divestments the company has made as of late have come at a negative profit relative to what the company has invested and bought it for. Prosus's sole success story on a high level remains Tencent. And don't get me wrong, this is an absolute "monster" of a success story, but the notion that one success means a repeat performance is flawed.

The company focuses on "financial alchemy", such as buybacks, which enhances the NAV, which is important for the company. I won't argue that it doesn't make sense to buy back shares if the company believes its own equity to be undervalued - but I do argue and question the state of undervaluation of this equity. To be clear, I don't agree with the notion that it is undervalued.

The company's non-stopping focus on "soft" values such as the integration and development of AI...

{kind=link}

...all tells me that the company doesn't focus on net profitability. And to those that still argue, years after tech mania, that "net profitability isn't the point", I say that net profitability is the point for any company that wants to survive.

The company positives, including e-commerce revenue growth and operational streamlining, only have relevance in the sense that where we can see a path to net profitability.

We know that the company doesn't have issues with liquidity. Prosus can keep investing for years - probably even a decade - simply by tapping Tencent. That does not make it a profitable or an investable business, however, if all it does is waste money - and the declining contributions from Tencent also tell us that eventually, this will dry up as well.

To be clear, I am not saying that Prosus or its portfolio couldn't go net-positive eventually. It could.

The bullish thesis for this company, as I've come to understand it, is based on the notion of "eventual profitability". It's also based on the notion of continued "NAV discount". None of those notions are wrong per se, or even all that problematic. I just don't agree with them, or with the notion that net profitability will be easy. And if net profitability sans Tencent isn't easy, then Prosus is just shelling sacks of money into unprofitable ventures, many of which it has also sold at losses for a variety of reasons (though Russia/Ukraine core among them).

Recent management guidance does point to an earlier breakeven in terms of its "Managed companies" than expected, with no selling or shutdown of further assets to bring about this goal - but this, again, is not "good enough" for me. The fact that Prosus is now also jumping on AI, which it seems that all companies are doing one way or another seems like a mix of desperation and "we have to do this"-move to me - not a net positive in any way.

Prosus value is still decided based on what happens to Tencent. None of the developments I've seen in the last set of earnings, or that I've read about for the company has the potential to move the needle significantly. With China between a rock and a hard place from an economic perspective, I don't see significant improvements in Tencent's valuation in a near-term perspective. I also don't see any of the company's holdings easily going into positive.

Based on this, I would give you the following valuation for Prosus.

Valuation for Prosus remains tricky

As things go "worse", as I see it given the interest rate increases and lower contributions from Tencent, I'm actually reconsidering if I should be impairing the NAV to a higher degree for Prosus, not lower.

In my latest update in June, I had my PT at €35/share, which represented a 70% discount to NAV. Given the last bout of buybacks, this would usually result in a situation where this would become a "BUY", but in this case, I don't consider the NAV increases based on share buybacks to better the thesis or the outlook for Prosus one bit. The one factor is the end of at least part of the disadvantageous ownership/listing structure.

Prosus is:

1.) A collection of unprofitable businesses and segments that the company is going to have a herculean challenge in monetizing/making profitable, and

2.) Tencent.

Based on that, I would invest in the company to invest in Tencent - because companies that "Might" become profitable to me, without me actually considering that outlook realistic, do not have value to me. It's as simple as that. The sale of Avito with a $678M loss shows us just how bad things can get for a company like this.

I believe a 60-70% NAV discount is the very least you need to apply to Prosus.

At the current updated NAV, this discount comes to around €31/share at the most extreme discount. I can go to the average here, and I decided in the end not to move my PT from the €35/share that I have, and where I would consider Prosus attractive. This gives you an idea of why I consider this company to be interesting. At the current valuation, it's around a 40% NAV discount. That is not enough for me.

If it's enough for you, then ask yourself what your expectations are - because you're not getting dividends, and the company itself is clear that profitability in managed companies in 2023 and 2024 won't happen. With Tencent contributions declining, where is your upside?

Those are the problems I see here, and that's why I remain fairly negative on this company.

Thesis

My thesis on Prosus is as follows:

- Prosus stock remains a somewhat unattractive investment due to the specifics of how the company operates and what it has. This lack of appeal has increased, as I see it, as we've moved into a higher interest rate environment where the demand upon the company's investments in terms of profitability - which rely on cheap capital and being able to operate at a loss for some time - has increased. This view has not changed in June of 2022.

- The shareholder structure is unappealing and inherently disadvantageous to Prosus investors. While the company is fundamentally sound and has a good track record due to the Tencent investment, there are too many fundamental question marks to really make this an option for me.

- I would be interested in Prosus if the market decided to discount it more than 70% to its current NAV.

- I consider it a "HOLD" here. My PT is €35/share.

Remember, I'm all about

1. Buying undervalued companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime. Even if that undervaluation is slight and not mind-numbingly massive.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

I can't call this anything except a "HOLD".

For further details see:

Prosus: The Premium Is Still Not Justified, Especially In This Environment