PTRA - Proterra: Downside Exists While Issues Persist

Summary

- Proterra is doing quite well from a sales perspective, with revenue continuing to rise.

- The firm has a significant amount of cash on hand to help it, but its fundamental condition is otherwise problematic.

- Profits and cash flows remain challenged and the company looks overvalued as a result.

Investing in companies with the hope and expectation that they will grow into their valuation can be very profitable. On the other hand, when things go south, it can result in a tremendous amount of pain. One company I would point to as an example of this is Proterra (PTRA), an enterprise dedicated to the production and sale of technology solutions centered around proprietary battery technology and electrification solutions for Class 3 to Class 8 vehicles (like delivery trucks, buses, etc…), as well as the production and sale of electric transit buses to North American public transit agencies and other organizations. Even though the company has demonstrated attractive growth in recent years and is likely to see that growth continue for the foreseeable future, bottom line results have continued to be depressing. Even if the company manages to continue its rapid growth over the next few years, the best-case scenario I would see is that shares might become fairly valued. But this does not make for a very attractive investment opportunity in my mind. So although the company has already fallen hard in recent months, I would say that it might have further downside left in it.

A painful ride

It seems these days that I am the only person who is bearish on Proterra. I say this because, after the article I published on the company in August of last year that rated it a 'sell', four subsequent articles came out on the enterprise, with one taking a neutral stance on the firm and the other three rating it a 'buy'. As for my own article, I acknowledged that the company had an interesting business model and that management had done well to grow the company's top line over the prior few years. Near term, I felt like true risk for shareholders was limited because of the significant amount of cash the company had on its books. But on the whole, shares looked very pricey and, I felt, could result in meaningful downside for shareholders moving forward. That led to my aforementioned 'sell' rating. Since then, the company has taken quite a hit. While the S&P 500 is down only 4.6%, shares of Proterra have experienced downside of 36.9%.

{kind=link}

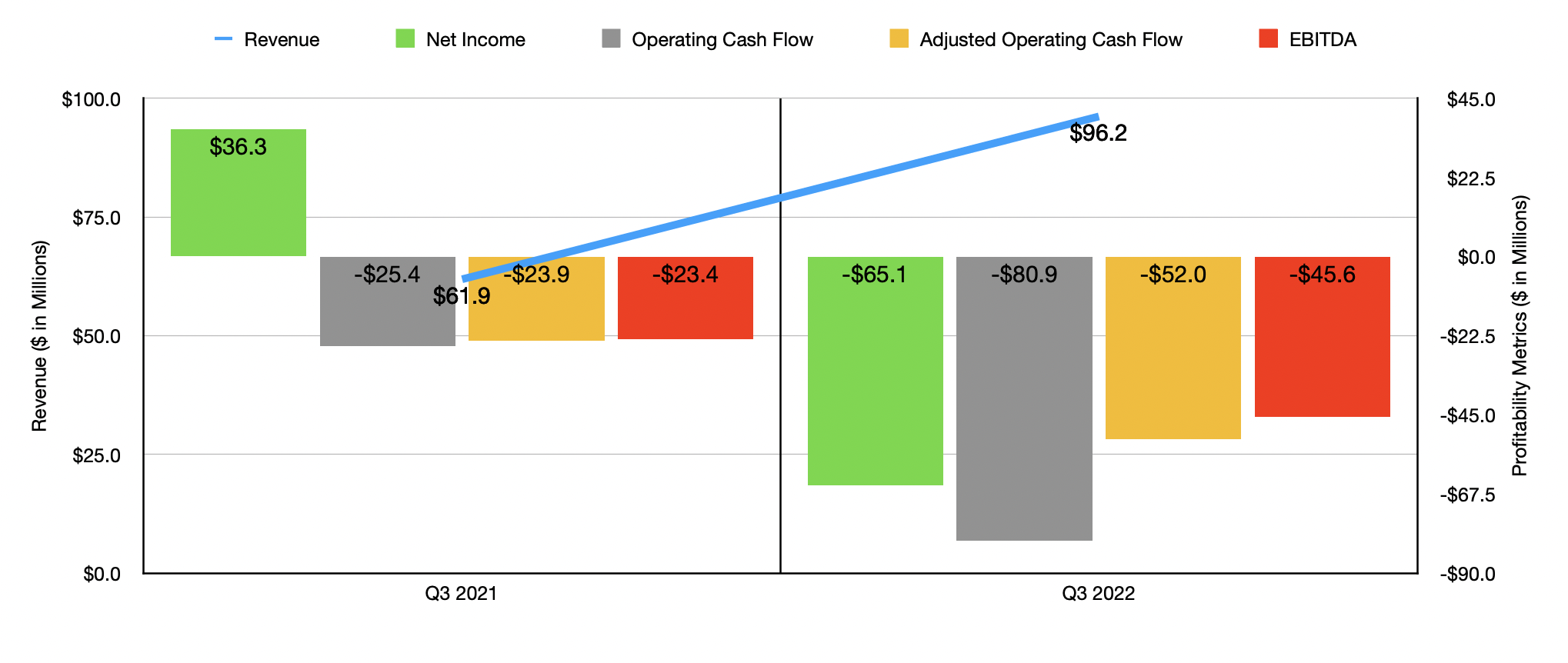

This return disparity has not been, in my opinion, a fluke. Instead, it's in response to some very real problems that the enterprise has. Yes, as of this writing, the firm does have cash in excess of debt of $304.1 million. Considering its market capitalization is only $1.14 billion, that's a tremendous amount of cash to have. On top of this, sales are continuing to grow. Consider results for the third quarter of the company's 2022 fiscal year. This is the only quarter for which new data is available that was not available when I last wrote about the enterprise. During this time, revenue came in at $96.2 million. That's 55.4% higher than the $61.9 million reported one year earlier. During the third quarter, Proterra delivered battery systems for 292 vehicles. That was significantly higher than the 78 deliveries the company reported one year earlier. It also delivered 60 new vehicles and five pre-owned vehicles. By comparison, the same time one year earlier, it delivered only 52 new vehicles and 0 pre-owned ones. As I mentioned in my first article about the company, the electrification of existing vehicles and the move toward an electric vehicle fleet for the global market has tremendous promise. These sales figures, then, don't really surprise me.

The problem is not on the top line but, instead, on the bottom line. During the third quarter, management reported a net loss of $65.1 million. That was significantly worse than the $36.3 million profit generated the same time one year earlier. To be fair, the largest contributor to this disparity actually involved a gain on the valuation of derivative and warrant liabilities that the company reported in the third quarter of 2021. The actual loss from operations for the business went from $29.8 million in the third quarter of 2021 to $58 million during the third quarter of 2022. This doesn't change the fact, however, the other profitability metrics worsened year over year. Operating cash flow went from negative $25.4 million to negative $80.9 million. If we adjust for changes in working capital, it still would have worsened, more than doubling from negative $23.9 million to negative $52 million. Even EBITDA took a hit, turning from negative $23.4 million to negative $45.6 million.

{kind=link}

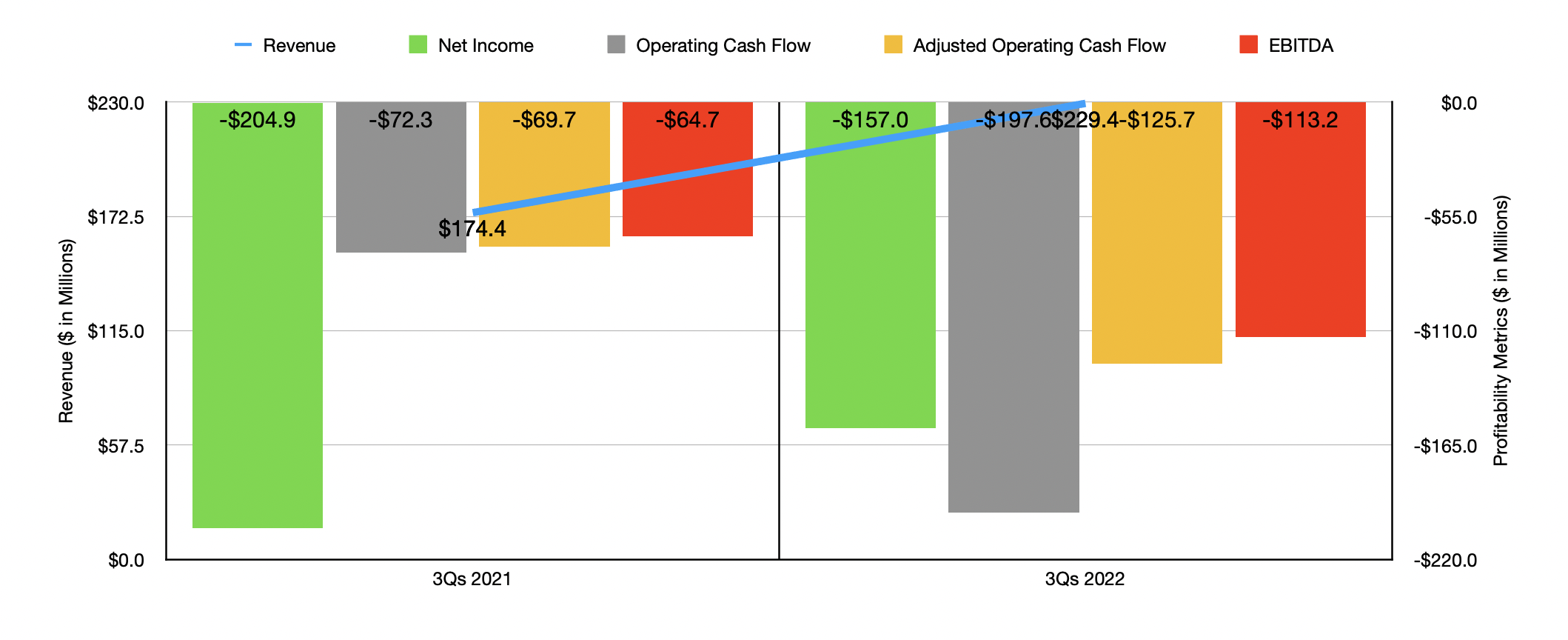

The third quarter was not a one-time thing for the company. For the first nine months of 2022, sales of $229.4 million dwarfed the $174.4 million reported the same time one year earlier. In this case, net profits actually improved, with the company's loss narrowing from $204.9 million to $157 million. But in this case, the company actually contended with a loss on valuation of derivative and warrant liabilities for the nine-month window of 2021. The actual loss from operations for the business went from $86.8 million to $147.2 million. Operating cash flow went from negative $72.3 million to negative $197.6 million, while the adjusted figure for this went from negative $69.7 million to negative $125.7 million. And finally, EBITDA turned from negative $64.7 million to negative $113.2 million.

When it comes to the 2022 fiscal year in its entirety, management said that revenue should be between $300 million and $325 million. At the midpoint, that would translate to a year-over-year increase of about 24%. Unfortunately, we have no idea what to expect from a profitability and cash flow perspective. But based on the data provided already, the situation is looking far from good. In short, Proterra is hemorrhaging cash and generating significant net losses along the way. And these cash flow figures don't even factor in what the business is putting toward capital expenditures in order to grow further.

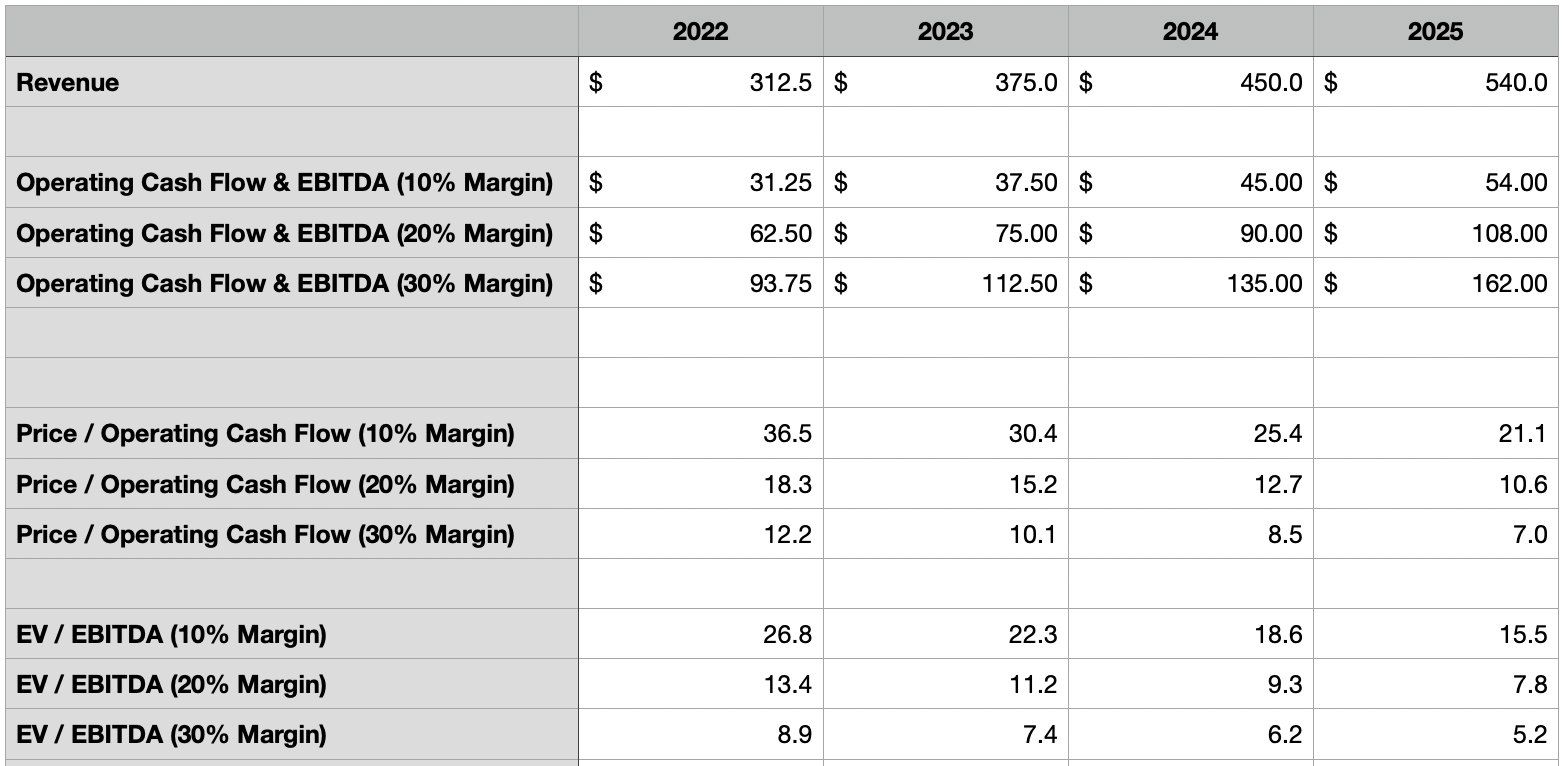

Truth be told, you can't really value a business like this. But what you can do is ask if it's reasonable to expect the company to at least grow into its current valuation. In the table below, you can see a hypothetical scenario where revenue for the company continues to grow at an annualized rate of 20% through the 2025 fiscal year. I then looked at three different scenarios for both adjusted operating cash flow and EBITDA, equating both of them to one another and assuming margins of between 10% and 30%. In this scenario, it is possible that the company could go on to be fundamentally attractive. But when you consider that, for the first nine months of 2022, its adjusted operating cash flow margin was negative to the tune of 54.8%, while the EV to EBITDA margin was negative by 49.3%, I see little to no hope of that gap being bridged.

{kind=link}

Takeaway

Assuming Proterra can eventually use the cash on its books to grow into a state where it's cash flow positive, I see the future for the company as being bright. Sales are certainly growing at an impressive pace. But this does not mean that the company will make a good return on the investments that investors are putting in. At this time, the company looks significantly overvalued in my opinion and I see little hope of that changing in the near term. For somebody who holds on for the next 10 years or so, the upside very well could be appealing. But this is not the kind of company I would like to have extended exposure to. And because of all of these factors, I still feel that a 'sell' rating is appropriate at this time.

For further details see:

Proterra: Downside Exists While Issues Persist