PTRA - Proterra: Issues Abound

- Proterra has an interesting business model, and management has done well to grow the company's topline recently.

- Although the near-term risk is low because of the firm having excess cash on hand, the long-term picture is also questionable.

- Shares look very pricey right now and could lead to pain for investors moving forward.

Whether you want to admit it or not, the future of all vehicles is electric. These days, there are a number of players in this space, but not all of them are created equal. Some will certainly go on to generate a significant amount of value for their investors. But others, such as Proterra ( PTRA ), look to be drastically overpriced and incredibly risky. Overall, I believe that investors in this company should tread carefully because, while the firm is likely to continue expanding from a revenue perspective, its fundamental condition is far from great. On the whole, I believe it makes for a worthy 'sell' candidate at this time.

A play on electric vehicles

According to the management team at Proterra, the company is focused on electric vehicle technology. Conceptually, this represents a tremendous opportunity for investors. The IEA, for instance, has provided some guidance on what the future might hold. Globally, the number of electric vehicles across all road transport modes is forecasted to grow from roughly 18 million in 2021 to 200 million by 2030. That implies an annualized growth rate of 30%. Total annual vehicle sales under the electric category are expected to hit 18 million in 2025 before hitting 30 million in 2030. At that point, they will represent over 20% of all road vehicle sales. Of course, other forecasts do vary. Under the most aggressive forecast, the total number of vehicles that are electric across the globe could hit 350 million by 2030, with annual sales of 65 million translating to a 60% market share of all vehicles sold.

Naturally, this should prove bullish for the companies and the investors that operate in this space. One such prospect is Proterra. To best understand the company, we should break it up into its two key operating segments . The first of these is referred to as Proterra Powered and Energy. This unit provides technology solutions to commercial vehicle producers and owners of commercial fleets. It, in turn, is broken up into two separate business lines. The first of these, Proterra Powered produces and integrates proprietary battery technology and electrification solutions into vehicles for global commercial vehicle OEM customers. At present, this business line only serves vehicles in the Class 3 to Class 8 categories such as delivery trucks, school buses, and coach buses. It is also involved in these same activities for construction and mining equipment. The other business line is called Proterra Energy. Through this, the company provides turn-key fleet-scale, high-power charging solutions and software services. Activities that the company focuses on here include fleet and energy management software as a service, fleet planning, installation, charging optimization, and more. The other segment the company has is called Proterra Transit. Through this, the company sells electric transit buses as an OEM for North American public transit agencies, airports, universities, and other commercial transit fleets.

{kind=link}

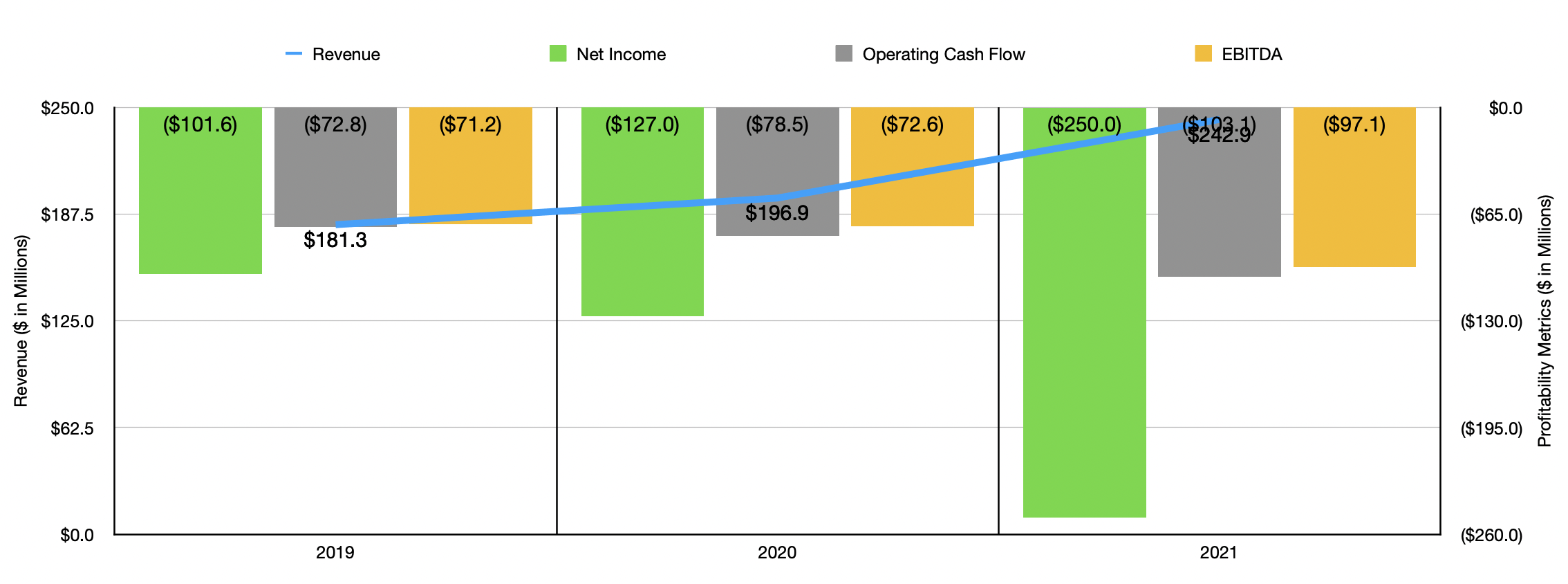

Over the past three years, Proterra has done a really good job to grow its topline. Revenue has risen from $181.3 million in 2019 to $242.9 million last year. Unfortunately, the company has also experienced a great deal of pain in its bottom line. Even with revenue growing, profitability has been an issue. The company generated a net loss of $101.6 million in 2019. This loss increased to $127 million in 2020 before ballooning to $250 million last year. If it were just the company's net loss, the picture might not be so bad. But the pain also extends to cash flow. Between 2019 and 2021, operating cash flow went from a negative $97.3 million to a negative $126.3 million. If we adjust for changes in working capital, it still would have worsened from negative $72.8 million to negative $103.1 million. Even EBITDA for the company worsened during this time frame, going from a negative $71.2 million to a negative $97.1 million.

{kind=link}

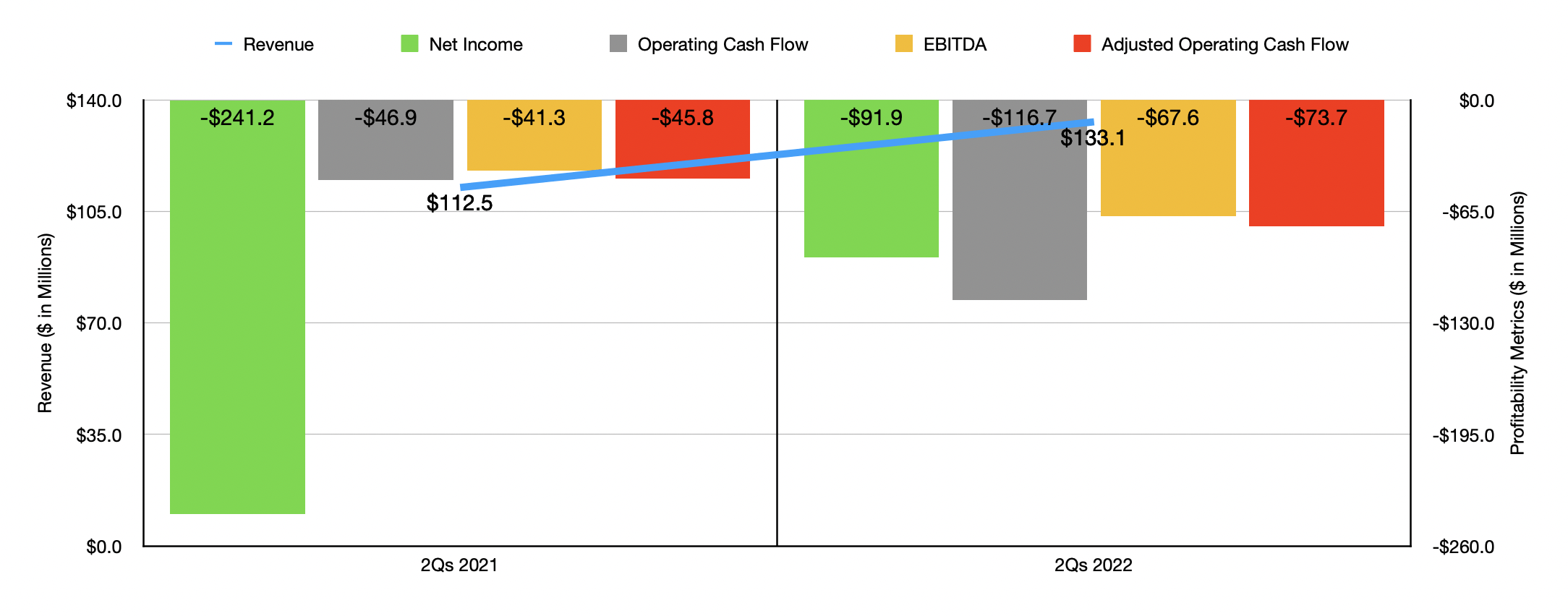

To compound problems even further, the pain has extended into the current fiscal year. In the first half of the year, revenue came in at $133.1 million. That's 18.3% above the $112.5 million generated just one year earlier. Net income did improve, going from a loss of $241.2 million to a more modest loss of $91.9 million. At the same time, however, operating cash flow went from negative $46.9 million to negative $116.7 million. On an adjusted basis, it went from negative $45.8 million to negative $73.7 million. And EBITDA turned from negative $41.3 million to negative $67.6 million.

When it comes to the 2022 fiscal year as a whole, management expects sales to come in about 24% to 34% higher than they were last year. This implies revenue of between $300 million and $325 million. Unfortunately, there is no guidance when it comes to profitability. But it's clear that profits and cash flows will be negative. Potentially significantly so. At least the good part is that the company has cash in excess of debt in the amount of $423.9 million. That provides it some wiggle room and reduces the risk for shareholders. But at the same time, it's clear that something needs to change.

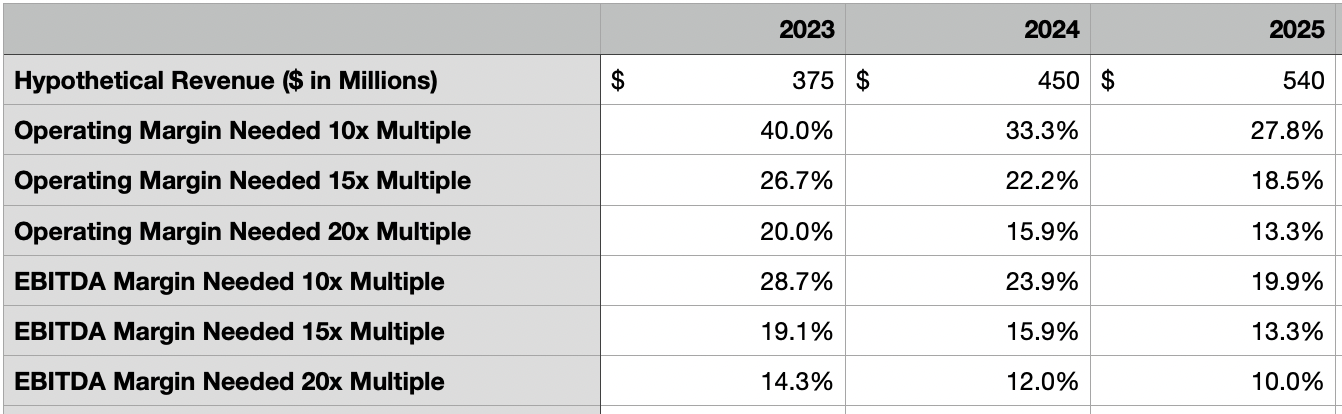

Truth be told, you can't really value a company with negative profits and cash flows. But what you can do is ask what kind of profitability would be needed to justify the current valuation, and then ask yourself if that kind of profitability is probable. Given the company's historical growth rate, I assumed that growth would continue to come in at around 20% per year for the next three years. I then looked at the price to operating cash flow multiples and EV to EBITDA multiples of 10, 15, and 20, calculating what kind of operating cash flow and EBITDA the company would need to generate in order to trade at those levels. At each respective multiple, operating cash flow would need to be $150 million, $100 million, and $75 million, respectively, while EBITDA would need to be at $107.6 million, $71.7 million, and $53.8 million, respectively. Meanwhile, in the table below, you can see what kind of operating cash flow margin and EBITDA margin would be required in order to achieve these targets. The bottom line is that, while the margins may not be ridiculous if we assume a higher trading multiple and project this out a couple of years from now, that's a lot of speculation just for the company to be fairly priced. It's also worth noting that its current profitability metrics are significantly removed from what these numbers would ultimately be. Making up that difference in such a short time frame, and with what would be relatively minor sales increases in the grand scheme of things, is highly improbable.

{kind=link}

Takeaway

Moving forward, I fully expect that Proterra will continue to grow. But that doesn't mean that the company makes for a great investment opportunity at this time. This is a highly speculative play, and investors would be wise to view it as such. Given industry conditions, it is possible that the company could continue to expand at a nice clip. To me, shares look drastically overpriced and deserve a 'sell' designation until something changes for the better.

For further details see:

Proterra: Issues Abound