PRTA - Prothena: 3 Alzheimer's Catalysts Will Likely Define Share Price Performance In 2023

Summary

- Prothena is a protein dysregulation specialist with an intriguing pipeline.

- The company has out-licensed an ATTR Amyloidosis / cardiomyopathy drug to Novo Nordisk, which could win approval after 2024.

- Its wholly-owned drug candidate Birtamimab could win approval in Stage 4 amyloidosis, although again this is unlikely before 2025.

- Prothena has 3 Alzheimer's programs - 2 wholly-owned, and 1 collaboration with Bristol-Myers Squibb - that likely account for >50% of the company's current market cap valuation.

- 2 of these 3 programs will read out in-human clinical data this year, whilst the 3rd - an anti-amyloid / anti-tau vaccine - will try to secure its IND from the FDA. These outcomes will likely dictate the value of Prothena stock at the end of 2023.

Investment Overview

I last covered Prothena Corporation ( PRTA ) in a note for Seeking Alpha at the end of September.

Prothena is a protein dysregulation specialist drug developer with an intriguing clinical pipeline. Its most advanced candidate is Birtamimab, which is progressing through a Phase 3 AFFIRM-AL study in patients with Mayo Stage 4 AL Amyloidosis.

Although an earlier Phase 3 study of Birtamimab was terminated based on a futility analysis, which suggested the primary endpoint of composite of time to all-cause mortality and cardiac hospitalization in patients with AL amyloidosis would not be met, Prothena found a statistically significant benefit in a subset of patients in that 260 patient trial - around 77 patients who had Mayo Stage IV amyloidosis, the most severe form of the disease - and AFFIRM-AL has been designed to target that population.

The AFFIRM-AL study has a primary endpoint of All-Cause Mortality and interim analysis will occur when 50% of events have occurred, which means that top line results aren't expected until 2024. The peak sales opportunity here could be in the region of ~$500m per annum.

Prothena's share price - which briefly traded at a price of >$75 in June 2021 - rose by 100% in value in September last year, hitting a high of $65 in November, largely due to the positive progress of Biogen ( BIIB ) and Japanese Pharma partner Eisai's Alzheimer's therapy Lecanemab, which won approval from the FDA this month under an accelerated approval pathway, although the Pharma's plan to submit for a full approval to try to secure reimbursement coverage from the Centers for Medicaid and Medicare ("CMS").

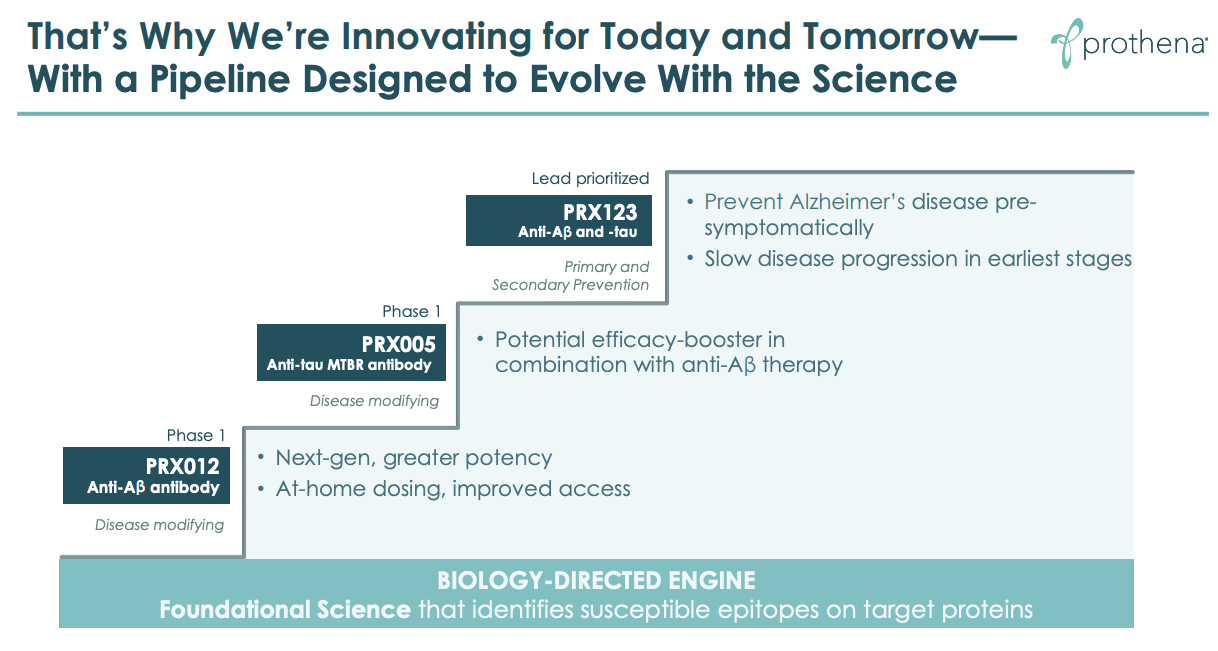

Prothena has its own Alzheimer's therapies in development - two are in Phase 1 clinical studies, with the first being wholly-owned anti-amyloid beta candidate PRX012, and the second being a tau (tau "tangles" are also known to accumulate in the brains of Alzheimer's patients, like the "sticky" substance amyloid does) targeting therapy, PRX005, being developed in partnership with Bristol-Myers Squibb ( BMY ).

PRX005 is seen as having potential efficacy as a booster in combination with an anti-amyloid drug, and data from a Phase 1 study is expected to read out this quarter, providing an intriguing early share price catalyst in 2023. Prothena has already received $230m from BMY in development milestone payments and according to the company's Q322 10Q submission :

...is eligible to receive up to an additional $160 million for U.S. rights, up to $165 million for global rights, and up to $1.7 billion for regulatory and commercial milestone payments for a total of up to $2.2 billion plus potential tiered commercial sales royalties across multiple programs.

Prothena's final Alzheimer's candidate - PRX123, which is a wholly-owned program - is a dual vaccine, which "concomitantly targets key epitopes within both the A? and tau proteins", and which Prothena believes could be used for the prevention and treatment of Alzheimer's. This drug has not yet entered in-human studies.

Besides BMY, Prothena also works alongside the Danish Big Pharma Novo Nordisk (NVO). Novo Nordisk paid Prothena $100m upfront in July 2021 for the rights to Prothena's drug candidate PRX004, now known as NNC6019, and indicated for Transthyretin amyloidosis ("ATTR Amyloidosis") and cardiomyopathy.

Novo is progressing NNC6019 through a Phase 2 study with Prothena eligible for up to $1.23bn in additional development, regulatory and commercial milestones, and receiving a $40m payment in November last year after Novo initiated the Phase 2.

Finally, Prothena is advancing Prasinezumab - a humanized monoclonal antibody that targets alpha-synuclein, a protein found in neurons that can cause neuronal dysfunction. The Swiss Pharma Roche ( RHHBY ) is a partner on this project, paying the majority of development costs of a Phase 2b PADOVA study that is expected to read out data in 2024. Roche paid Prothena a $60m milestone payment upon dosing the first patient in that trial and could pay up to another >$600m based on clinical and commercial progress.

The fact that Prothena's share price movements have been so closely correlated with success for Lecanemab - now marketed and sold as Leqembi - tells investors that the market is primarily interested in PRX012, a drug which Prothena believes can deliver efficacy and safety data that is superior to Leqembi, with a similar mechanism of action, opening up a potential double-digit billion dollar market opportunity.

Top line data from the Phase 1 study of PRX012 - which will involve six cohorts including healthy volunteers and patients with biologically confirmed Alzheimer's - has been promised this year, and probably holds the key to whether Prothena's stock price finishes up or down for the year.

In the meantime, Prothena represents an interesting proposition for investors looking to gain exposure to central nervous system disorder drug developers. In my last note on Prothena in September last year, I argued that the company's market cap valuation of nearly $3bn is quite high given that the company has not won any approvals, meaning it has no source of revenues except collaboration funds.

With that said, however, Prothena says it ended Q322 with >$495m in cash, and although the company made a net loss of $129m across the first 9m of 2022, management completed a public offering of 3.25m shares at $56.50 per share in mid-December, raising a further $172m.

The company certainly has the funds to complete all of its existing studies and provided the Phase 1 Alzheimer's data supports further development, management will likely be able to raise substantially more funding without having to worry about putting pressure on the share price by diluting investors, thanks to the attraction of the highly lucrative Alzheimer's market.

Should trial data disappoint in 2023 my concern would be that the company does not have any sure-fire winners in its pipeline, meaning the stock price could experience a major correction - perhaps back below $10 per share, as it traded prior to the positive Lecanemab data readout - if PRX012 flops in the clinic.

Perhaps the only thing we can say for certain about Prothena at the present time - with shares trading at $57 per share for a market cap of $2.9bn - is that the company is either worth substantially more or substantially less than that figure - mainly based on whether PRX012 can prove itself a genuine alternative to Leqembi.

In the remainder of this post I highlight the three catalysts - all related to Prothena's Alzheimer's pipeline - that will tell us most about the progress the company is making - and the direction of its share price in 2023.

I am focusing specifically on Prothena's Alzheimer's franchise because as mentioned I believe these drugs support the current high share price, as opposed to Birtamimab, the Roche partnered Prasinezumab and Novo Nordisk partnered NNC6019. As important as these therapies are, firstly, pivotal trial data will not be available until 2024, and secondly, the market opportunities are more limited.

Whilst Prasinezumab has been tentatively pegged for sales of up to $1.5bn if approved - and the ATTR amyloidosis / cardiomyopathy opportunity could be another blockbuster (>$1bn sales per annum) opportunity - Prothena itself will only receive a small percentage of net sales as a royalty payment, plus one-off milestone payments.

These, plus up to $500m per annum from Birtamimab would support a market cap valuation of up to $2bn, if all three prove successful, in my view - the unlikelihood of Prothena generating revenues >$1bn per annum restricting the overall valuation.

As such, Prothena's Alzheimer's franchise is the difference maker for Prothena, and the company needs to show its drugs can work in the clinic in 2023, or risk a sizeable downgrade. Success in the clinic with PRX012 could support a market cap of anything up to $5bn, in my view, provided the anti-amyloid approach is reinforced by the success of Biogen's Leqembi, and Eli Lilly's Donanemab over the course of this year.

Catalyst 1 - The PRX012 Phase 1 Data Due YE23

2023 could end up being remembered as a momentous one for Alzheimer's Disease drugs. As mentioned, Leqembi has been approved, after its pivotal, 1,800 patient study showed the drug slowed progression of Alzheimer's by 27% over an 18-month period - based on a "gold standard" scale measuring cognition and function, Clinical Dementia Rating-Sum of Boxes ("CDR-SB").

The data has been cited as the first definite proof that reducing build-up of Amyloid Beta in the brains of Alzheimer's patients reduces the pace of cognitive decline. Biogen and Eisai's previously approved amyloid beta targeting drug, Aduhelm, could only show marginal efficacy in a particular subset of patients in one of its two pivotal studies, but was nevertheless approved by the FDA, only for the CMS to refuse to provide reimbursement for the drug, which came with a price tag of $56k per annum.

Biogen / Eisai will be desperate for CMS to agree to reimburse Leqembi, and have given the drug a much lower price of $26.5k per annum. Safety concerns are another issue, however, with the FDA including a warning about amyloid-related imaging abnormalities ("ARIA"), a type of brain swelling that can have fatal consequences - three patients from the pivotal study have apparently died from brain-swelling related incidents.

All this is important to note in relation to Prothena for several reasons. The first is obviously that PRX012 has a similar mechanism of action to both Leqembi, and another therapy with the same MoA, Eli Lilly's Donanemab. Lilly has shared head-to-head data that showed it is superior to Aduhelm in clearing amyloid plaque and analysts believe it can win accelerated approval in 2023, with Lilly sounding very confident about an upcoming Phase 3 data readout.

Prothena says that PRX012 has shown 10x greater binding potency than Aduhelm in preclinical studies and the drug is designed to "promote comprehensive clearance of amyloid plaques and neutralisation of oligomers" according to a recent investor presentation . Another advantage is that PRX012 is administered subcutaneously, which is more convenient than the intravenous administration required for Leqembi and Donanemab, although Biogen says it is working on a subcutaneous version of Lecanemab.

Prothena's Phase 1 data readout for PRX012 - with endpoints of the study based on safety - to evaluate the safety and tolerability of PRX012 when administered as a single dose - and a secondary endpoint - to characterize the plasma PK profile of PRX012 and cerebrospinal fluid PK profile of PRX012 after subcutaneous administration - will not arrive until much later this year. By that time, the picture around whether CMS will agree to reimburse Donanemab and Leqembi ought to be clearer.

The CMS may face pressure to change its current stance that it will only fund supplies of the drug for use in clinical trials, or, Leqembi or Donanemab could secure a full approval from the FDA. If either of those things happen it will be encouraging for Prothena and add value to the company, But ultimately Prothena still needs to show that its drug works in the clinic - at least as well as D onanemab and Leqembi.

The Phase 1 results may not prove the case one way or the other, given its safety focused endpoints - meaning investors may have to wait until a Phase 2 is complete for confirmatory data - but encouraging data signals may be enough to trigger frenzied buying given how few Alzheimer's focused therapies have been successful.

The Phase 1 results ought to at least reveal whether Prothena has a genuine contender in the anti-amyloid space, which is what makes them such a critical catalyst. Quick progress into a Phase 2 study based on strong safety and efficacy signals would lead to speculation about an approval shot, timings, addressable markets etc. Signs that PRX012 is ineffective in a real world setting, however, would raise serious doubts about Prothena's most valuable asset.

Catalyst 2 - The BMY Partnered Alzheimer's Data Due This Quarter

Although in my opinion the PRX012 Phase 1 data is the most important catalyst of the year, the Phase 1 results from the BMY partnered asset - due this quarter - shouldn't be ignored.

Prothena's Alzheimer's Franchise Ambitions (investor presentation)

{kind=link}

As we can see from the above slide Prothena is looking to create an Alzheimer's franchise, with an anti-amyloid antibody doing the heavy lifting, and the anti-tau therapy PRX-005 potentially working as part of a combo. PRX123 is seen as a preventative therapy that could be used in earlier stage patients.

Prothena describes PRX005 as a "potential best-in-class microtubule binding region ("MTBR") specific anti-tau antibody to reduce pathogenic tau spread", and claims that it has shown superiority in "blocking cellular internalisation of Tau and downstream neurotoxicity compared to other anti-tau antibodies".

The problem is that there is very little detail available about the Phase 1 study. We know that BMY paid Prothena ~$80m for the option to develop PRX005, but that is really all we know, hence, as with the PRX012 data, investors should not expect the data to instantly validate the project.

On the other hand, there's no doubt that BMY would like to have a successful drug candidate in Alzheimer's, with rival Pharmas expected to make billions from a field that had not approved a new Alzheimer's drug in more than 20 years, as it finally may begin opening up. Peak sales expectations for Leqembi and Donanemab range from $5-$10bn.

BMY would probably be more than satisfied if PRX005 became a blockbuster-selling drug, given its expected use as an adjuvant therapy, alongside an anti-amyloid - and there are many hurdles to be overcome before that becomes a possibility - but such a scenario would also work out very well for Prothena, triggering the kinds of development milestone payments that will fund its operations going forward.

If successful, PRX005 may persuade BMY to opt into other candidates too, or even consider buying up Prothena and its Alzheimer's franchise. The fact that the tau-targeting drug has a non-amyloid MoA is also important - should the standoff between the CMS and the anti-amyloid drugs persist, PRX005 may be in a position to capitalise.

Catalyst 3 - A?/Tau vaccine IND Filing

A vaccine that targets both anti-amyloid and tau, and one that is used in earlier stage Alzheimer's patients with prevention of disease worsening in mind, would obviously be extremely valuable, if it can be proven to work.

First Prothena needs to ensure that PRX123 is permitted to enter in-human trials - by securing an Investigational New Drug ("IND") approval from the FDA. The company's thesis is that amyloid beta and tau "may work synergistically in the development of AD", and preclinical data has shown, according to Prothena that:

The immune animal sera reacted to A? and tau, induced Ab phagocytosis, and blocked tau interaction with a key mediator of cellular release and cell-to-cell transmission.

{kind=link}

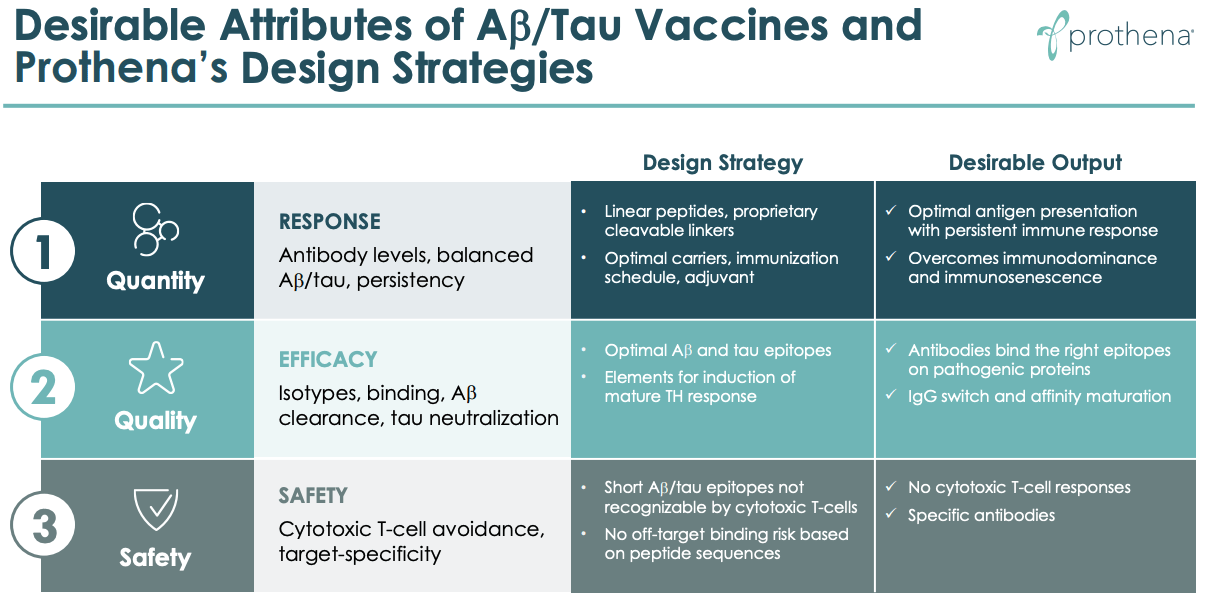

The slide above provides an intriguing overview of how PRX123 may be both effective and safe as a result of clever engineering, and recent innovations in vaccination certainly support Prothena's ambition to develop a potent therapy that is effective, durable and safe.

With that said, when we consider the years it has taken the likes of MRNA vaccination giants Moderna ( MRNA ) and BioNTech ( BNTX ) to get to Phase 1 results stage with their "personalised cancer vaccines", we can be sure that Prothena will have its work cut out to get its IND for PRX123 approved, let alone showing positive in-human data.

The rewards are potentially huge however - teaching a patient's immune system to recognise antigens from a particular disease so it can be ready should they present themselves is the same approach that Moderna / BioNTech are using with circulating tumor DNA in solid tumor cancers, and Moderna's market valuation recently increased >$10bn after the company published data showing its PCV cut the risk of death by 44% versus standard of care therapy Keytruda in melanoma.

Prothena will be hoping it can enjoy similar success with PRX123 and the first step is to secure an IND. Should that IND be accepted, and approved, I would expect the company's share price to respond positively.

Conclusion - Prothena's Year Ought To Be Dictated By Progress of Alzheimer's projects - Keep a Close Eye On Progress

As mentioned, Prothena has an intriguing pipeline, which includes a later stage approval shot with Birtamimab, and one partnered program with Novo Nordisk that I would expect to be successful, providing Prothena with more milestone payouts and a future small revenue stream likely after 2024.

With Prasinezumab a longer shot for approval - the a-Synuclein thesis in Parkinson's has foundered before , with French Pharma Sanofi ( SNY ) recently abandoning development of a drug in this class and Biogen also admitting defeat - I would argue that at least half of the market cap valuation of Prothena is supported by its Alzheimer's franchise.

It's rare to find a company with a drug that has any shot of an approval in Alzheimer's. Amongst biotechs, Cassava Sciences ( SAVA ) has a drug in two Phase 3 trials with a unique mechanism of action, whilst Anavex Life Sciences ( AVXL ) recently claimed success in a Phase 2b/3 trial, meeting endpoints of improvement in ADAS-COG and ADCS-ADL cognitive scoring.

Both companies are derided as much as they are celebrated, however, with many observers believing the drugs are worthless. Prothena has three separate Alzheimer's projects, with two in the clinic and one chasing approval to begin clinical trials, but Prothena has arguably less proof that its drugs work in a real-life setting than either Cassava or Anavex, whilst enjoying a much higher market cap valuation of nearly $3bn compared to Cassava's $1.4bn, or Anavex' ~$825m.

In order to sustain such a high valuation either PRX123, PRX005, or PRX012 must deliver some positive data in the clinic, or Prothena's stock price will inevitably plummet. Preferably, the success story would be PRX012, given that Prothena holds all of the rights to this drug, and that anti-amyloid drugs stand the greatest chance of being approved for Alzheimer's by the FDA based on recent evidence.

The data we will see in 2023 from Prothena will still leave many questions unanswered, but it should at least provide an indication of which of the three drugs is worth persevering with. If Prothena is still moving forward with all three projects at the end of this year, then I would expect the stock's valuation to be matching or exceeding its all-time high of >$75.

If the company instead detects flaws within its programmes in the clinic that were not obvious in preclinical studies, however, it will lead to difficult questions around Prothena's technology platforms and candidate selections. The jury will be out on Prothena's Alzheimer's programs in 2023 and early data releases ought to dictate whether the share price increases or decreases by as much as 50%, I believe, in 2023.

For further details see:

Prothena: 3 Alzheimer's Catalysts Will Likely Define Share Price Performance In 2023