PRTA - Prothena: I'm Not A Buyer At A $3 Billion Valuation

Summary

- Prothena has several interesting drug candidates for Alzheimer’s, Parkinson’s and two rare diseases.

- The company has different partnerships, over $3 billion in potential milestone payments, and possibly additional royalties.

- Wholly owned Birtamimab is a Phase 3 drug candidate for stage IV AL amyloidosis, which may get approved some time in 2025 in case of success.

- The company's market cap is flirting with a $3 billion valuation, about one third of which can be attributed to its Phase 1 drug candidate PRX012 for Alzheimer’s.

- Funds are buyers here, insiders have been selling.

Thesis

Prothena's ( PRTA ) market cap has seen a tremendous gain over the past six months on the back of data from another company, Eisai (ESALY), which had reported Phase 3 results in September 2022. That market cap gain was related to its Phase 1 anti-amyloid drug, PRX012.

The company has several other interesting drug candidates in different trial stages. The furthest-advanced is wholly-owned Birtamimab for stage IV AL amyloidosis, which is in a confirmatory Phase 3 trial after having seen an earlier Phase 3 trial aborted. Birtamimab has received fast-track designation, orphan drug designation and has a special protocol assessment. Post-hoc analysis of the earlier Phase 3 trial revealed interesting chances of success. I give this drug a serious chance of approval, probably sometime in 2025.

The company has two Phase 2 drug candidates in trials, Prasinezumab in Parkinson's disease, NNC6019 in ATTR amyloidosis. Both are partnered and are interesting, but not compelling to me.

PRX005 and PRX012 are two Phase 1 candidates. The latter seems to have garnered interest from funds. The Lecanemab news had Prothena's share price jump. Insiders have sold tremendously, and Prothena has used the opportunity to add to its already impressive cash position. I express several doubts as to whether that gain is really justified and sustainable.

PRX123 and PRX019 are preclinical drug candidates which the company marks as lead prioritized. PRX123 is a combined amyloid and tau vaccine. At this point, there is little to assume it can lead to significant results in Alzheimer's disease.

At this time, I will not focus at the drug candidates in the discovery stage, nor on PRX0199 as its target is still undisclosed.

For me, Prothena is a good example of the mindset of several funds as to investing in the neurodegenerative space. I give the company a Sell rating at this time.

Company

Pipeline and potential catalysts

Prothena is a Dublin-based biotech company with several interesting drug candidates in its pipeline, as listed below. Prothena seems to have a business model consisting of partnering drug candidates early in their pipeline, which has led to some impressive-looking partnerships.

Pipeline (Corporate Presentation)

{kind=link}

Amyloidosis is the denominator for a group of rare diseases which are all characterized by the buildup of amyloid proteins in different parts of the body. In AL Amyloidosis, the most common type, amyloid builds up in kidneys and the heart. The condition is caused by the creation of amyloid by plasma cells. There is no known treatment to remove existing amyloid, but some drugs can stop plasma cells from creating amyloid, allowing the body to remove the amyloid buildup. In ATTR amyloidosis , the liver produces faulty transthyretin proteins which may build up in the heart, and may lead to heart failure.

Birtamimab, which is in a confirmatory Phase 3 trial after an earlier Phase 3 trial had been aborted, should deplete toxic aggregates of amyloid in AL amyloidosis.

NNC6019, in a Phase 2 trials, should deplete the non-native transthyretin protein in ATTR amyloidosis. It is licensed to Novo Nordisk.

Prasinezumab, in a Phase 2b trial, is a drug candidate for Parkinson's disease to hopefully remove the buildup of alpha-synuclein. It is partnered with Roche (RHHBY)(RHHBF).

PRX012 is a Phase 1 anti-amyloid antibody for Alzheimer's disease, similar to Leqembi and Aduhelm.

PRX005 is a Phase 1 anti-tau antibody for Alzheimer's disease. It is partnered with Bristol Myers Squibb.

PRX123 is a dual anti-amyloid and anti-tau vaccine candidate. It is in the preclinical stage, and the company has high hopes for it as it considers it one of two drugs that are lead prioritized.

PRX019, with the target still undisclosed, is the other lead prioritized drug candidate.

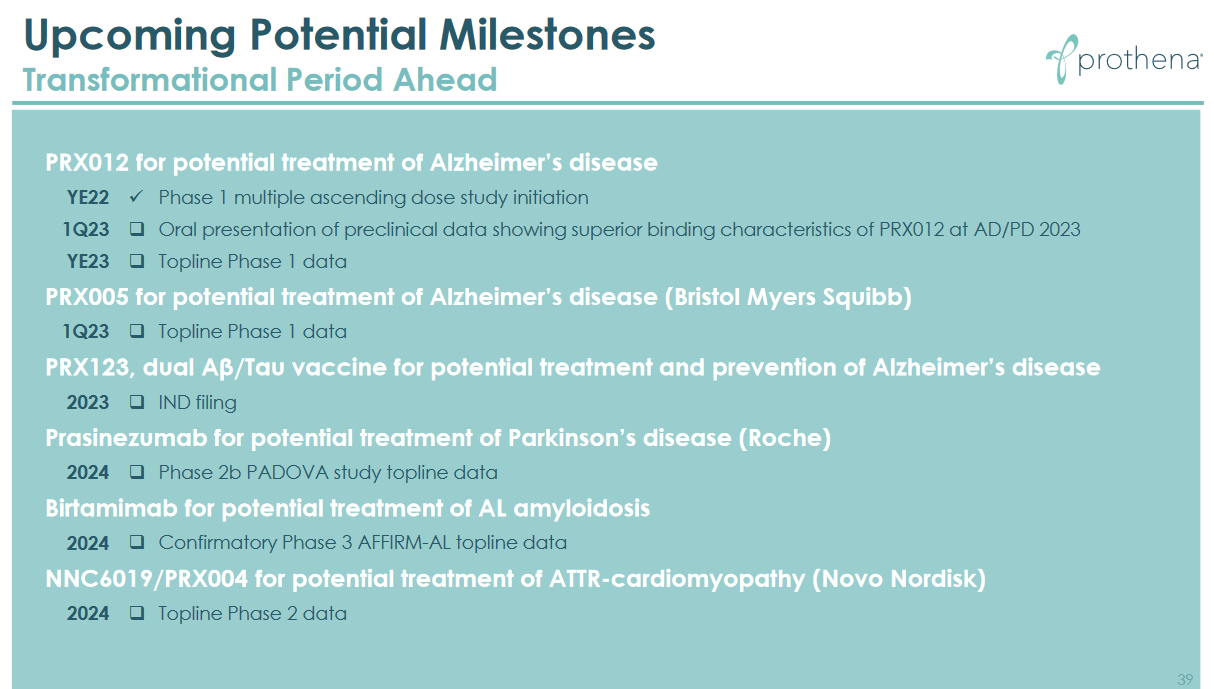

These are the company's potential milestones, four of which relate to the year 2023.

Upcoming milestones (Corporate Presentation)

{kind=link}

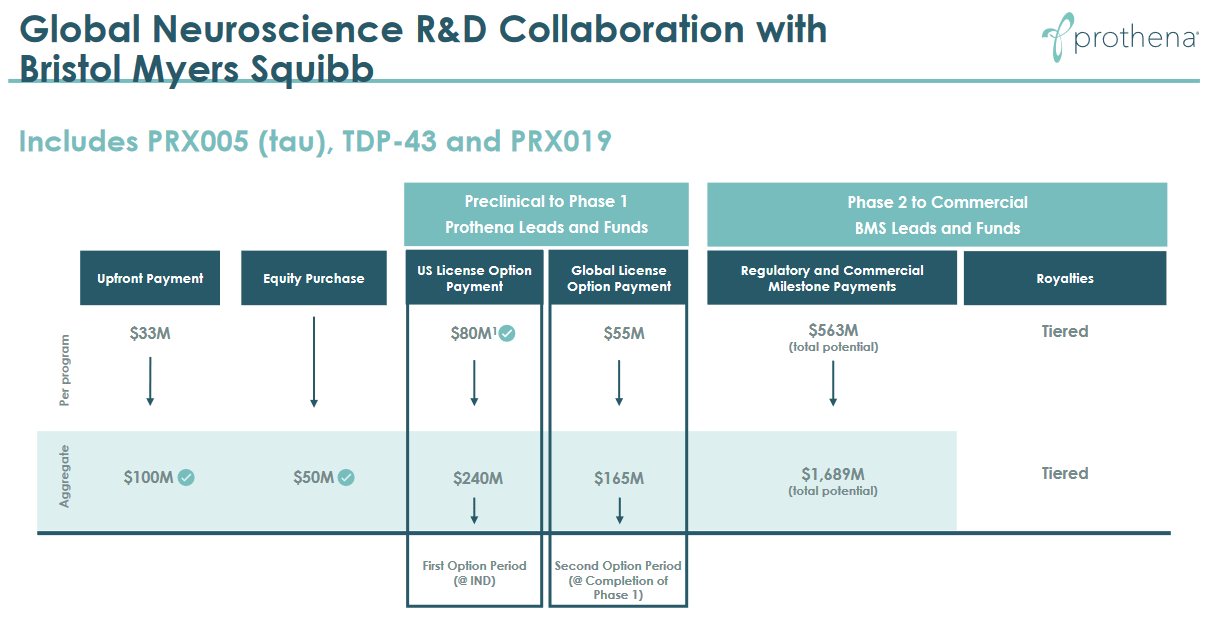

Partnerships make Prothena eligible for over $3 billion in payments

Prothena has impressive partnerships with Bristol Myers Squibb ( BMY ), Roche and Novo Nordisk ( NVO ). The partnership with Bristol Myers Squibb concerns three early-stage drug candidates, including the anti-tau antibody PRX005. The two other ones are PRX019 and TD-43, still earlier stage. The below table sets out which payments Prothena may be eligible for.

BMY collaboration (Corporate Presentation)

{kind=link}

The partnership with Roche for Prasinezumab, in a Phase 2 trial, can lead to total milestone payments of $755 million and royalties, as shown below. Profits in the US are to be split on a 30/70 basis, where Prothena also has the right to promote sales. Outside of the US, Roche bears that responsibility alone, but Prothena is still eligible for royalty payments up to double-digits on net sales.

Roche collaboration (Corporate Presentation)

{kind=link}

NNC6019 for ATTR amyloidosis, previously known as PRX004, has in July 2021 been acquired by Novo Nordisk, after it had shown a good safety profile in a Phase 1 trial. It is currently in a Phase 2 trial, and Prothena is eligible to receive up to $1.23 billion in milestone payments under the agreement. It is unclear, however, when those milestones become due. There was a $60 million upfront payment, and I understand from the July 2021 press release that next to that, there would be another $40 million in near-term clinical milestone payments, as well as profits, on a 30/70 basis (30 percent Prothena, 70 percent Roche).

If one combines all of the potential milestone payments, for the entirety of Prothena's pipeline except for the wholly-owned drug candidates Birtamimab, PRX012 and PRX123, one comes to total possible milestone payments of $3.67 billion. That is the maximum potential, to be clear. It is in no way sure that these milestone payments will ever be due, unlikely that all would be due, and always possible that some of these partnerships get terminated.

Birtamimab for AL amyloidosis

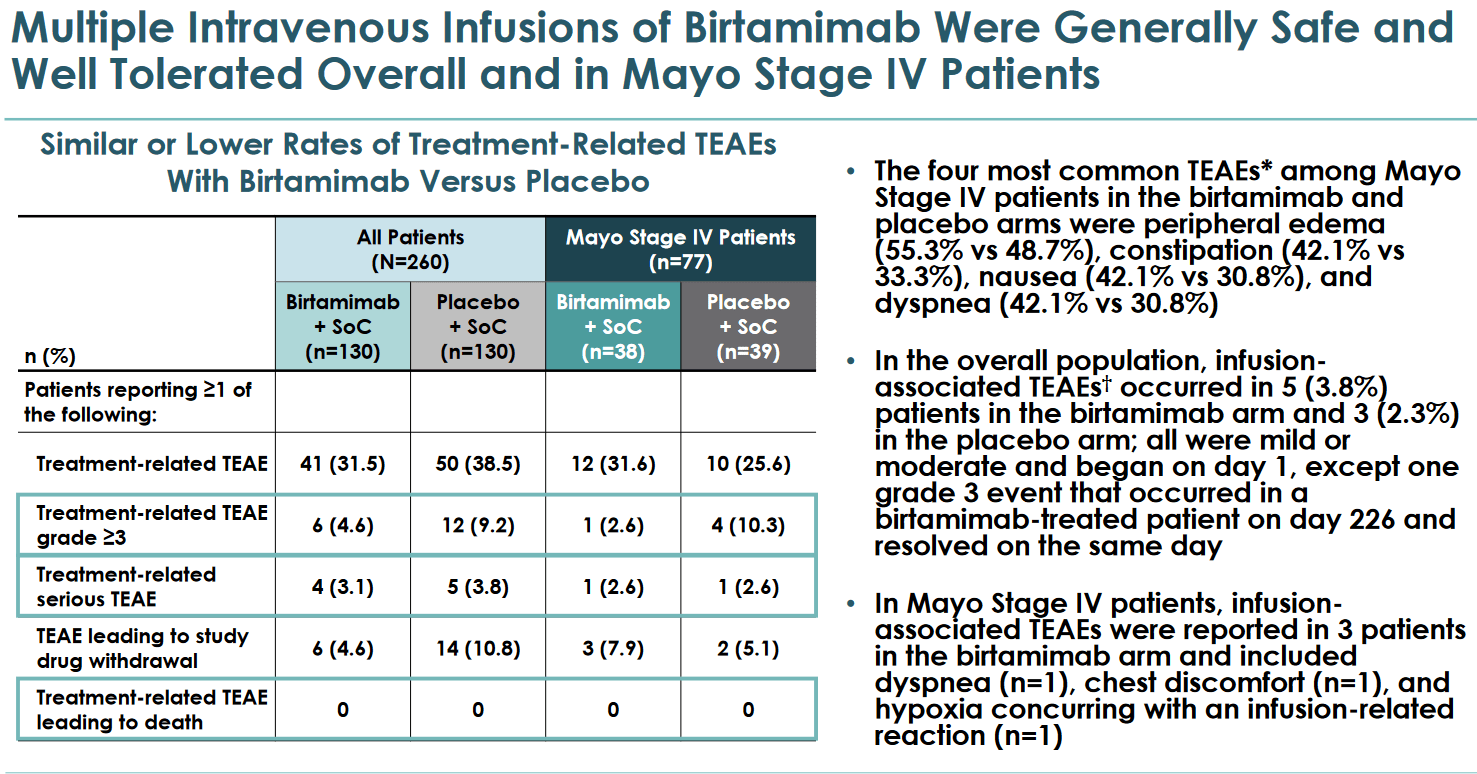

Prothena's drug candidate Birtamimab is in a confirmatory Phase 3 drug trial for AL amyloidosis. The company focuses on stage IV AL amyloidosis, the last stage of the progressive and fatal disease, as a post-hoc analysis of the aborted earlier Phase 3 trial had revealed interesting results there. In fact, the drugs to treat AL amyloidosis have led to good hematologic and organ response rates, but have not shown statistically significant survival advantages at stage IV of the disease, with a median overall survival of less than 6 months. Birtamimab also seems to come with a safer profile.

Birtamimab Safety Slide (Presentations Page on Corporate Website)

{kind=link}

There is an unmet need for these patients. As an amyloid depleting drug candidate, with no competition in that regard insofar as I know, Birtamimab could be an interesting addition to available symptomatic therapies.

The post-hoc analysis revealed a 74% survival benefit in stage IV patients - patients being alive at nine months - compared to 49% on placebo. According to the company, that meant a greater than 50% relative risk improvement at that stage of the disease, which is considerable.

Birtamimab post hoc analysis (Presentations page on corporate website)

{kind=link}

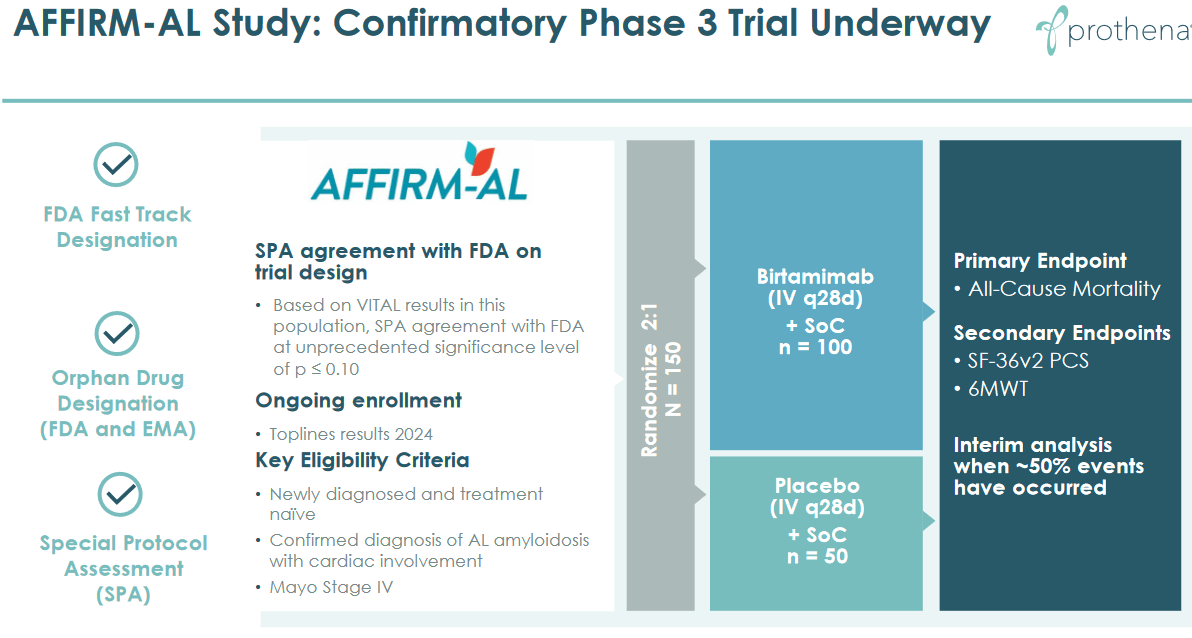

But given the short life expectancy, it could result in a median life benefit of about three months. About 33% of all patients in that previous Phase 3 trial, called Vital, had been stage IV patients. The Affirm-AL trial is specifically in stage IV patients.

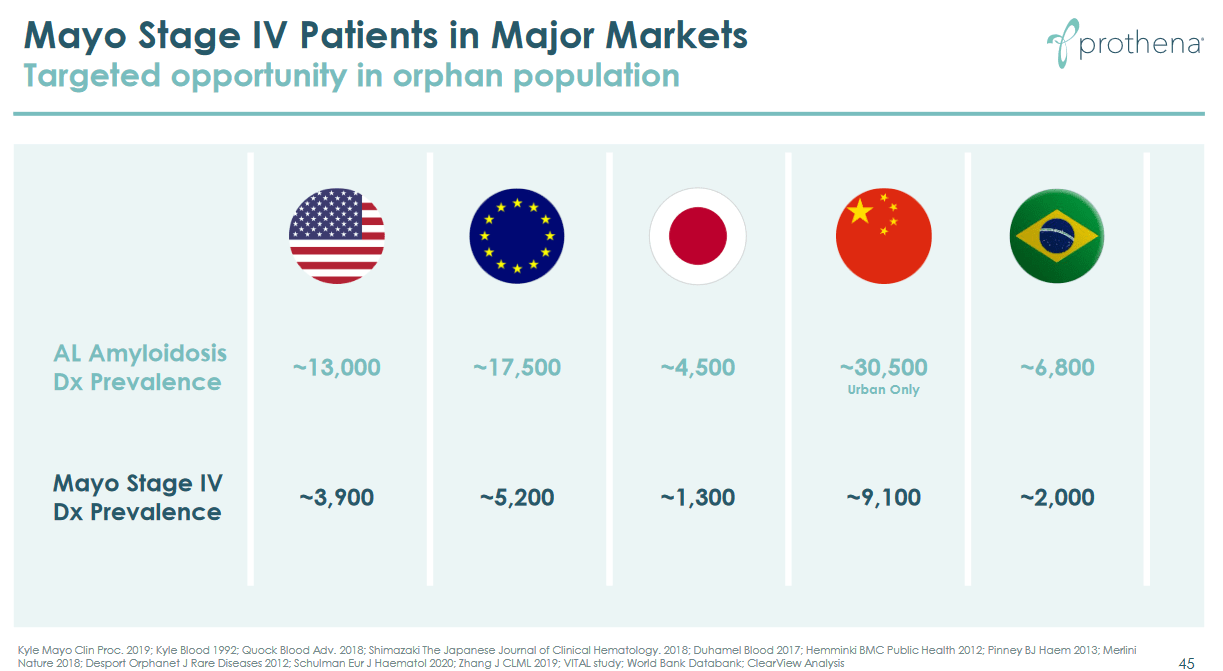

According to Prothena, in the US and the EU, the prevalence of AL amyloidosis is about 13,000 and 17,500 patients respectively. ROW is another 41,800 patients. Stage IV patients in the US and the EU respectively are estimated at about 3,900 and 5,200 patients, with the number for ROW at 12,400.

Mayo Stage IV market potential (Corporate Presentation)

{kind=link}

The ongoing confirmatory Phase 3 trial Affirm-AL, estimated to enroll 150 patients, has all-cause mortality as its primary endpoint. Topline results are due for some time in 2024 which, if positive, could possibly lead to approval some time in 2025. But, as announced in February 2021, an interim analysis will be conducted when approximately 50% of the events have occurred. This interim analysis could allow the independent data monitoring committee to recommend continuing the study, or ending it early in case of overwhelming efficacy. As this trial has been ongoing for quite some time now, I believe this interim analysis could be any time. So there may be a chance for approval faster than 2025.

Affirm AL trial design (Corporate Presentation)

{kind=link}

According to Prothena, in the US and the EU, the prevalence of AL amyloidosis is about 13,000 and 17,500 patients respectively. ROW is another 41,800 patients. Stage IV patients in the US and the EU respectively are estimated at about 3,900 and 5,200 patients, with the number for ROW at 12,400.

Pricing may be key here. If I would assume pricing of $40,000 for US and EU patients only, the total maximal turnover could be $1.2 billion. Assuming maximal market penetration of about 30%, that would lead to 366 million in turnover potential. Approval in the rest of the world will probably not have the same pricing, but one could add another $100-$200 million. That means there is a nice risk/reward here.

Prasinezumab for Parkinson's disease

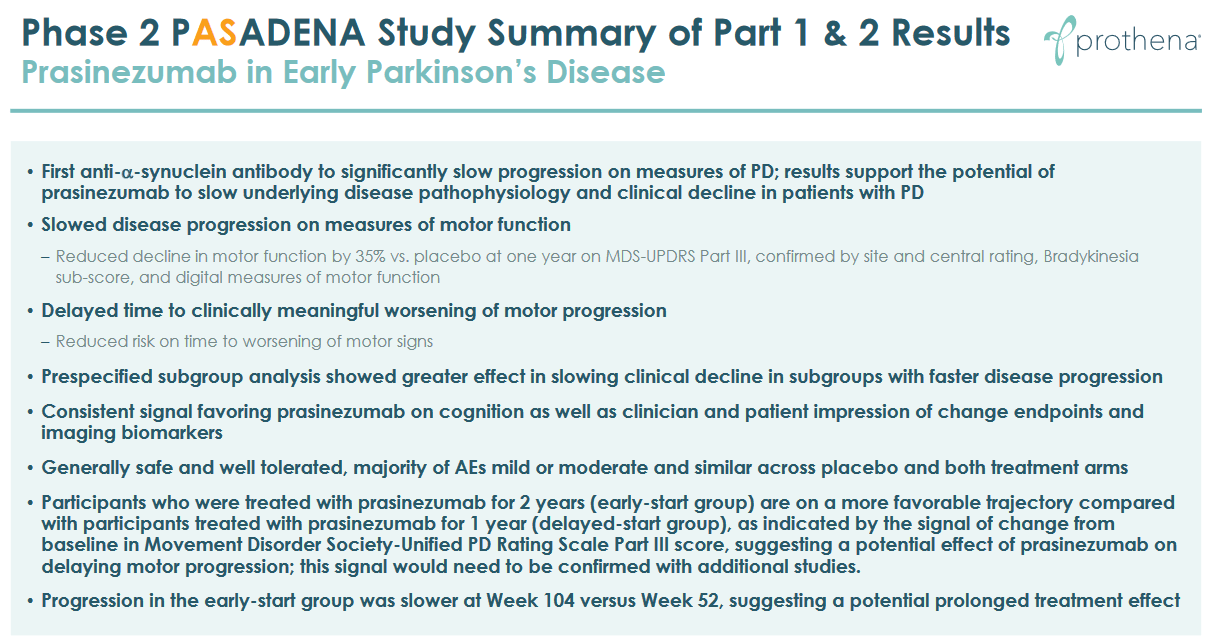

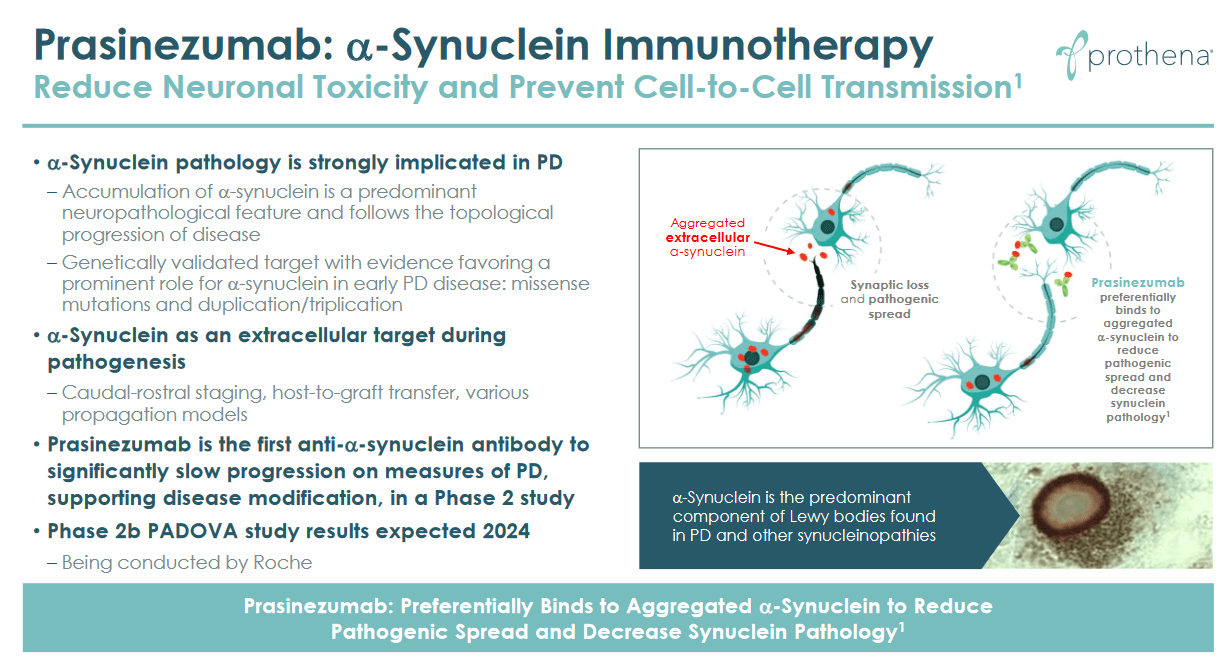

Prasinezumab is the anti-?-Synuclein antibody in Phase 2 trials, for which Prothena partnered with Roche since 2013. Prasinezumab had seen an efficacy signal in an earlier Phase 2 trial entitled Pasadena , after failing to meet its primary endpoint of slowed movement and non-movement symptoms over 52 weeks on Parts I, II and III of the MDS-UPDRS scale.

Pasadena trial results (Presentations page on corporate website)

{kind=link}

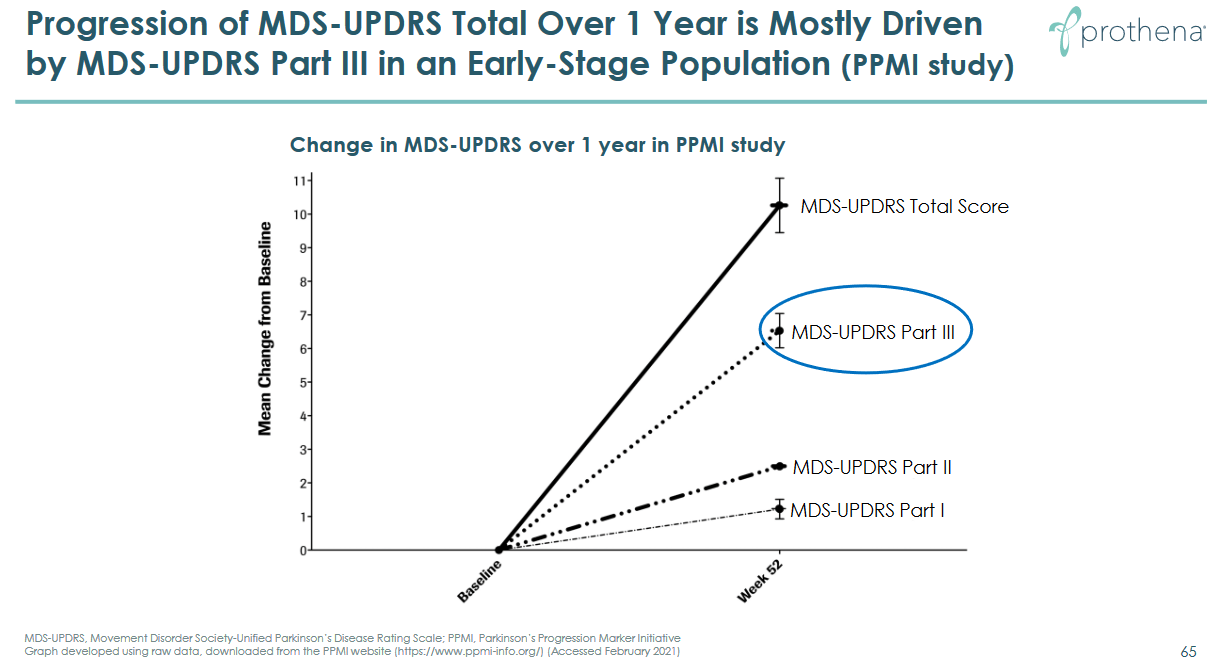

The trial did show slowing of motor progression and improvements on imaging biomarkers consistent with disease modification. And as progression is mostly driven by Part III of the MDS-UPDRS scale, Prothena considers Prasinezumab has an additional potential benefit here.

Prasinezumab slowed motor decline progression (Presentations page on corporate website) MDS-UDPRS Part III driver of progression (Presentations page on corporate website)

{kind=link}

{kind=link}

The current Phase 2b study called Padova will expand to patients with early Parkinson's disease. As the first anti-?-Synuclein antibody to advance to late-stage development, Prasinezumab is an interesting drug candidate, also taking into account the recent developments having led to approval of Aduhelm and Leqembi on the basis of secondary endpoints, namely reduction in amyloid burden in Alzheimer's disease. Both amyloid and tau share one main commonality: they are both misfolded proteins which essentially characterize the disease.

In my opinion, however, disease characterization is not identical to solving the disease. Removing misfolded proteins is probably only a small part of the solution, and this is true across many large neurodegenerative diseases, which are multifactorial in nature. Prasinezumab's Pasadena results are there to prove it, yet again. This has held true for many other failed drug candidates for Parkinson's disease.

Prasinezumab slide (Corporate Presentation)

{kind=link}

Topline data should for the Padova trial are expected some time in 2024.

Drug candidates for Alzheimer's disease

Introduction

Prothena has three drug candidates for the treatment of Alzheimer's disease, two in Phase 1 trials and on in the preclinical phase.

Legacy slide for AD (Corporate Presentation)

{kind=link}

The company ranks these early-stage drug candidates as shown below, with PRX123 being lead prioritized. Whereas the company seems to give most importance to PRX123, the market seems to do so to PRX012 which is the anti-amyloid antibody.

Alzheimer's drug pipeline (Corporate Presentation)

{kind=link}

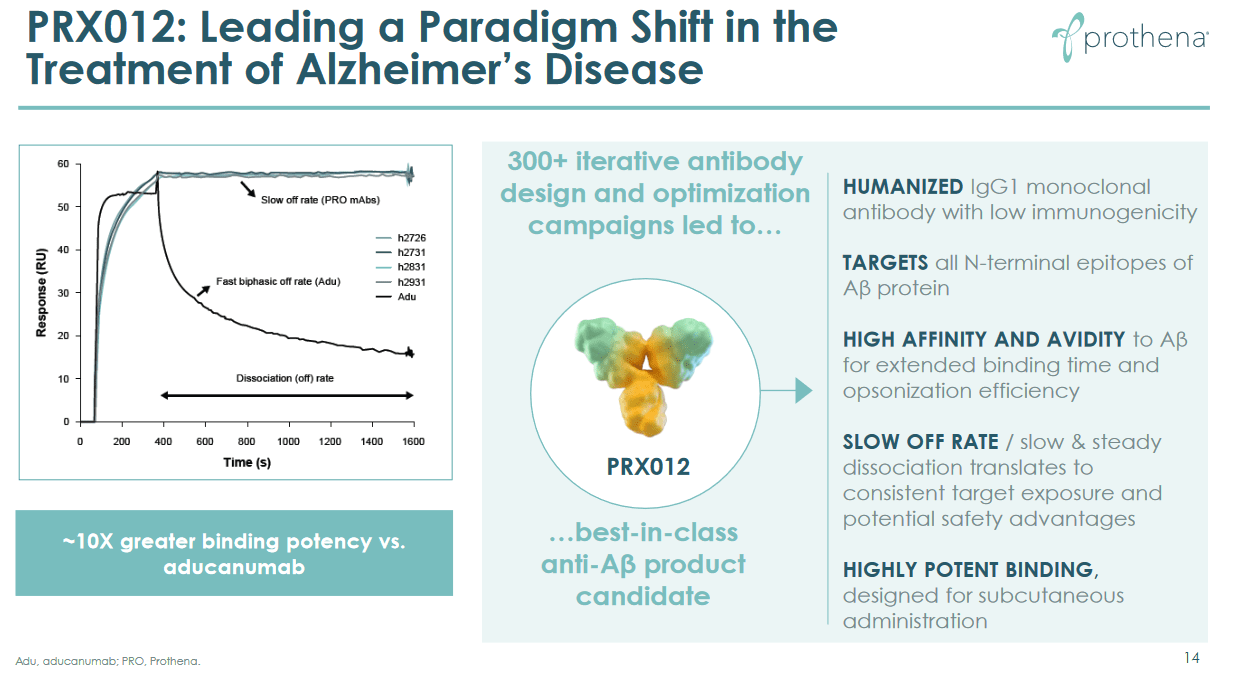

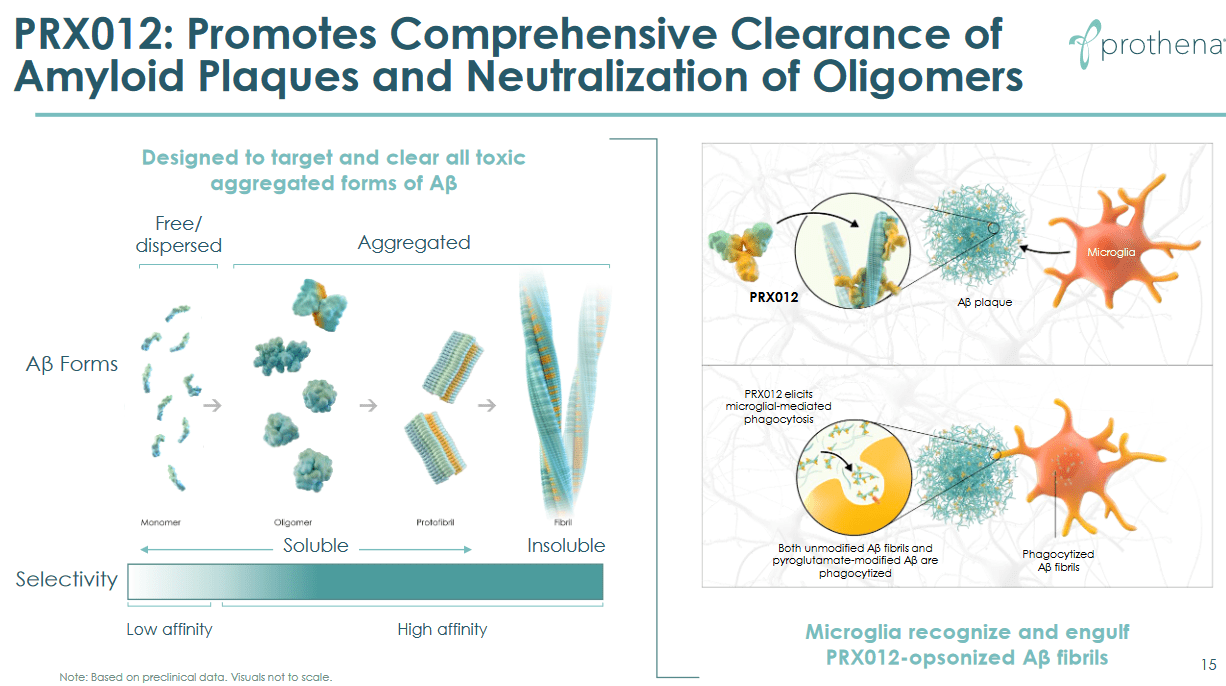

PRX012, an anti-amyloid antibody, as the value driver

PRX012 is a wholly-owned anti-antibody with high binding affinity, allegedly up to 10x higher than Aduhelm.

PRX012 slide (Corporate Presentation) PRX012 slide 2 (Corporate Presentation)

{kind=link}

{kind=link}

This drug candidate apparently also accounted for about $1 billion in sustained market value, gained after Eisai's announcement on September 28, 2022 that its anti-amyloid antibody Leqembi led to a 27% slowing of cognitive decline in Alzheimer's patients. Jefferies had remarked at that time that PRX012 was the only wholly owned antibody that reduced significant plaque and was not already owned by large pharma.

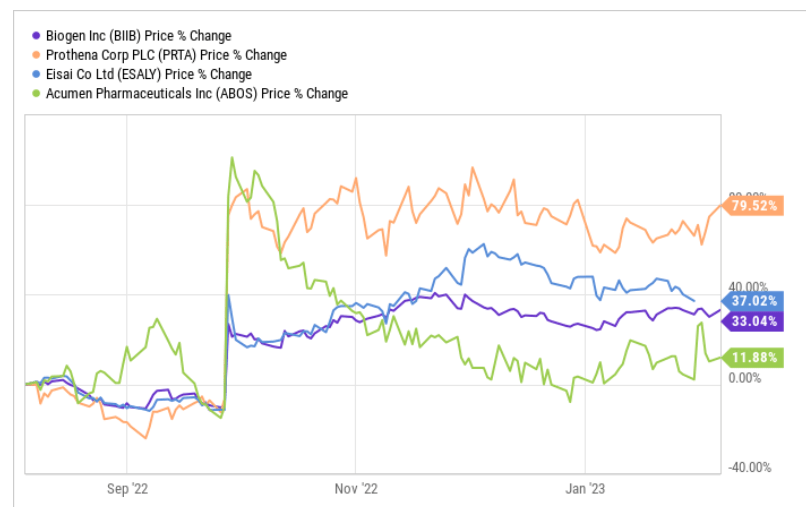

The market's reaction to Eisai's news has led to significant changes in related companies' market caps, some of which are shown below.

Market cap percentage change anti-amyloid companies (Ycharts)

{kind=link}

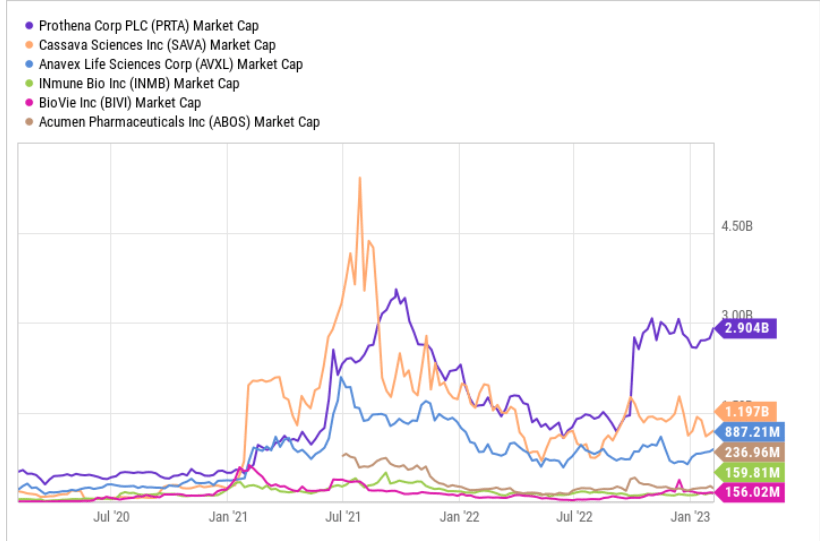

Biogen ( BIIB ), which I have covered before with a bullish note , is Eisai's partner. Acumen ( ABOS ), which I have covered before with a bearish article , is a small-cap biotech company with an anti-amyloid drug in its pipeline which saw its market cap grow 100% by about $200 million . Prothena gained 88% after the Lecanemab news, which led to a market cap addition of $1.3 billion, and that gain has remained sustained over the past three months.

Compared to other companies involved in the Alzheimer's space with drug candidates which are further along, some of which also have a diversified pipeline, the market cap gain which occurred in a bearish biotech environment is tremendous.

Comparative market cap evolution chart (Ycharts)

{kind=link}

Prothena's gains on the back of Eisai's news led to a sustained reaction that is even large in the perspective of Cassava Sciences ( SAVA ), a highly popular stock with a Phase 3 asset for Alzheimer's disease in its pipeline. Contrary to Cassava Sciences, however, Prothena has garnered interest from funds mostly as institutional ownership stands at 90%. Though short interest is at 11%, no short sellers have yet taken any interest in seriously discrediting PRX012's potential.

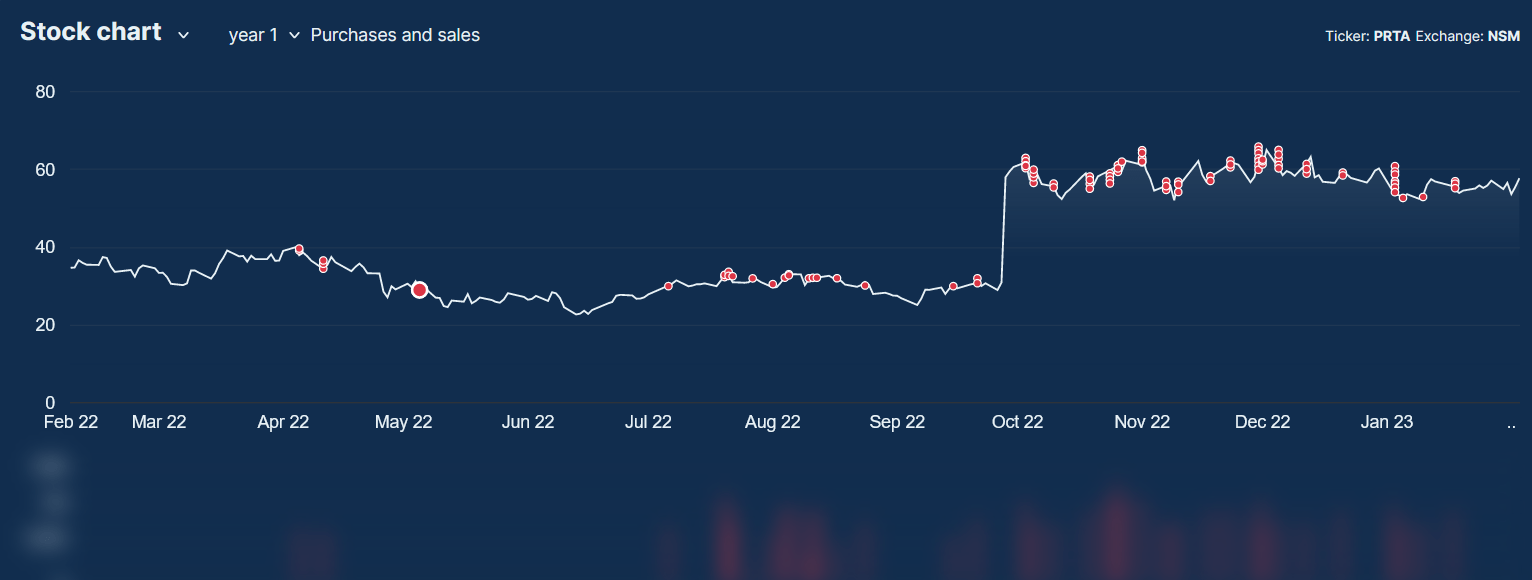

Prothena, has taken advantage of that gain. Insiders have sold massively, and Prothena has picked up $172.4 million in a public offering of 3,250,000 shares at $56.50 per share.

Insider Sales (Insider Screener)

{kind=link}

My thoughts here are similar to those that I have shared on Acumen. Realism dictates that the most an amyloid antibody has been seen to do so far is either nothing or moderately slowing of cognitive decline. If Acumen's $200 million market cap gain was already huge, Prothena's $1.3 billion gain was in no way justified. If history can serve as a reminder, it took Leqembi more than ten years to get to market, after its Phase 1 trial start in 2010. That long duration is due, in part, to very lengthy trials which are considered necessary to show statistical significance in a drug that only slows cognitive decline by 27%. Meanwhile, PRX012 has not proven to be safe, in light of issues with ARIA that typically coincide with anti-amyloid drugs. ARIA is the brain's immune cell's or microglia's inflammatory response to these antibodies' actions. In neurodegenerative diseases brain, these microglia deviate from their normal phenotype, and have moved to an inflammatory M1 phenotype , creating an inflammatory loop , which is probably the biggest issue in neurodegenerative diseases.

PRX012 may have stronger binding affinity to amyloid, but it is not uniquely binding to a subset of amyloid fibrils which are considered toxic.

In that sense, I would give PRX012 less chance of success than Acumen's ACU193, which targets A? oligomers solely, in line with a 2022 publication in Frontiers. As reducing amyloid load is only part of treatment of the disease, proven by Prothena's diversified AD pipeline itself, reducing the entirety of amyloid may not lead to much more slowing of cognitive decline than Leqembi did.

The path to commercialization is another issue; Aduhelm failed tremendously , and there is no telling Leqembi will do much better. CMS coverage was denied for Aduhelm, and this may change for Leqembi once, but that change is not upon us according to the latest CMS communication . It is impossible to look how the commercial landscape will look like by the time PRX012 may hit the market, if it ever will.

The fact that the drug candidate is wholly owned by Acumen does not mean it will necessarily be licensed or sold to large pharma at a given time point, nor that if it will, that deal will represent a large amount in light of Prothena's current market cap. Assuming in five to ten years from now, PRX012's Phase 3 trial will have ended up showing stronger efficacy than Lecanemab, the question to me is where the other high-potential Alzheimer's treatments will be. My best guess would be that, at that time, there may be much more potent treatments for the disease, several of which I have covered before. Companies like Athira Pharma ( ATHA ) and BioVie ( BIVI ), with much smaller market caps, have drug candidates in potentially registrational trials, with apparently safer drugs, and have already reported efficacy of their drug candidates.

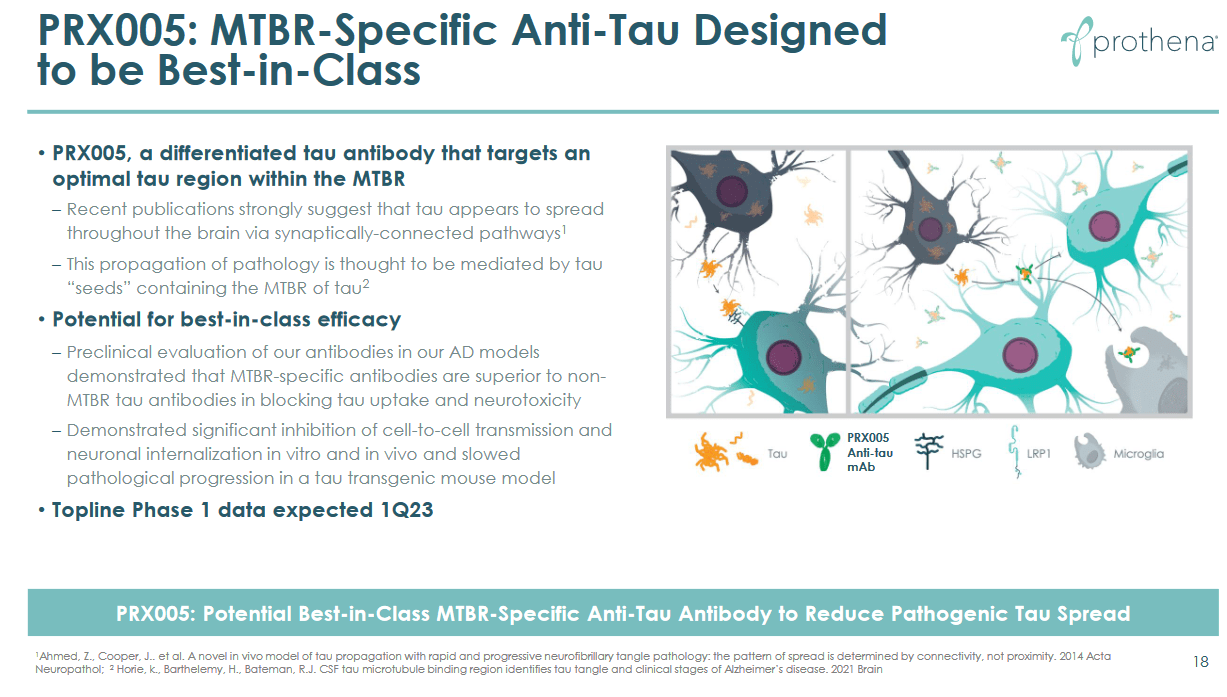

PRX005, an anti-tau antibody

PRX005 is an anti-tau antibody for Alzheimer's disease, in a Phase 1 trial in collaboration with Bristol Myers Squibb. Tau neurofibrillary tangles are traditionally considered to be the second traditional hallmark of Alzheimer's disease, but efforts to treat the disease from this angle have so far not led to compelling results.

PRX005 slide (Corporate Presentation)

{kind=link}

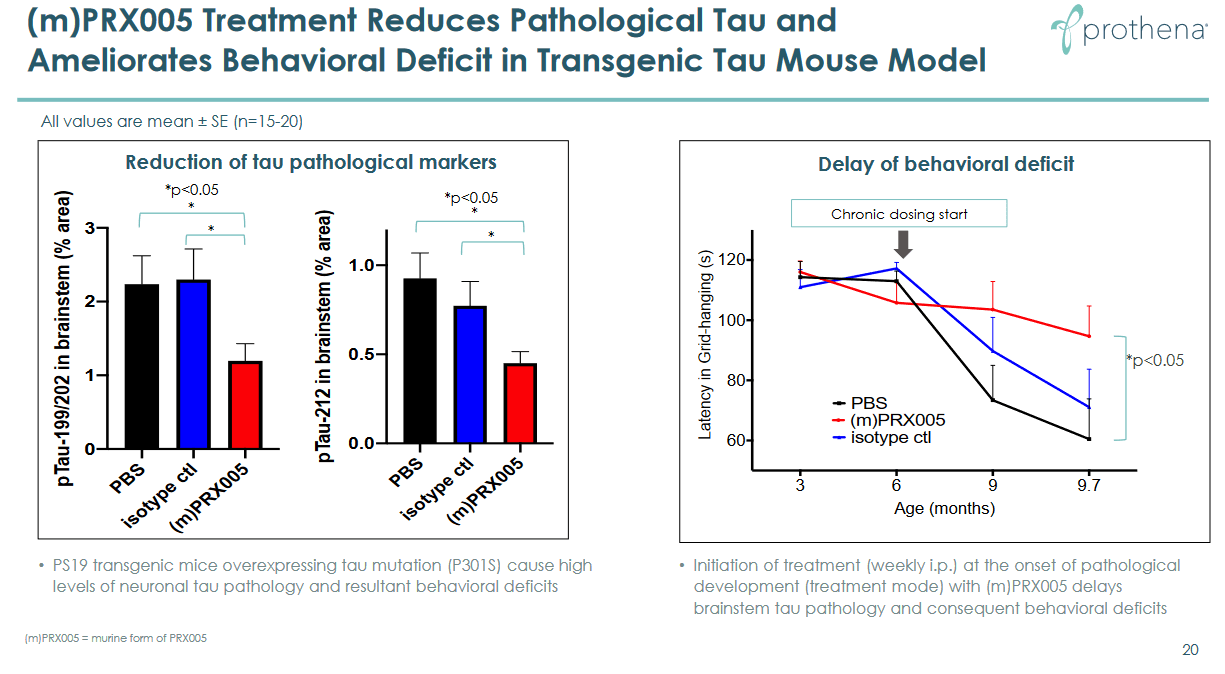

The drug candidate had shown some efficacy in reducing tau and slightly ameliorating behavior in a mouse model.

PRX005 preclinical results (Prothena presentations page)

{kind=link}

Prothena has just reported topline data from the single ascending dose part of the Phase 1 study, showing the drug candidate to be safe and well tolerated, and being able to cross the blood-brain-barrier. The Phase 1 multiple ascending dose part is still ongoing, and topline results here are expected by year-end 2023.

PRX123, an amyloid and tau vaccine candidate

PRX123 is a preclinical amyloid and tau vaccine candidate to prevent Alzheimer's disease.

PRX123 slide (Corporate Presentation)

{kind=link}

Prothena should file an IND for this drug candidate in the course of this year.

NNC6019 for ATTR amyloidosis

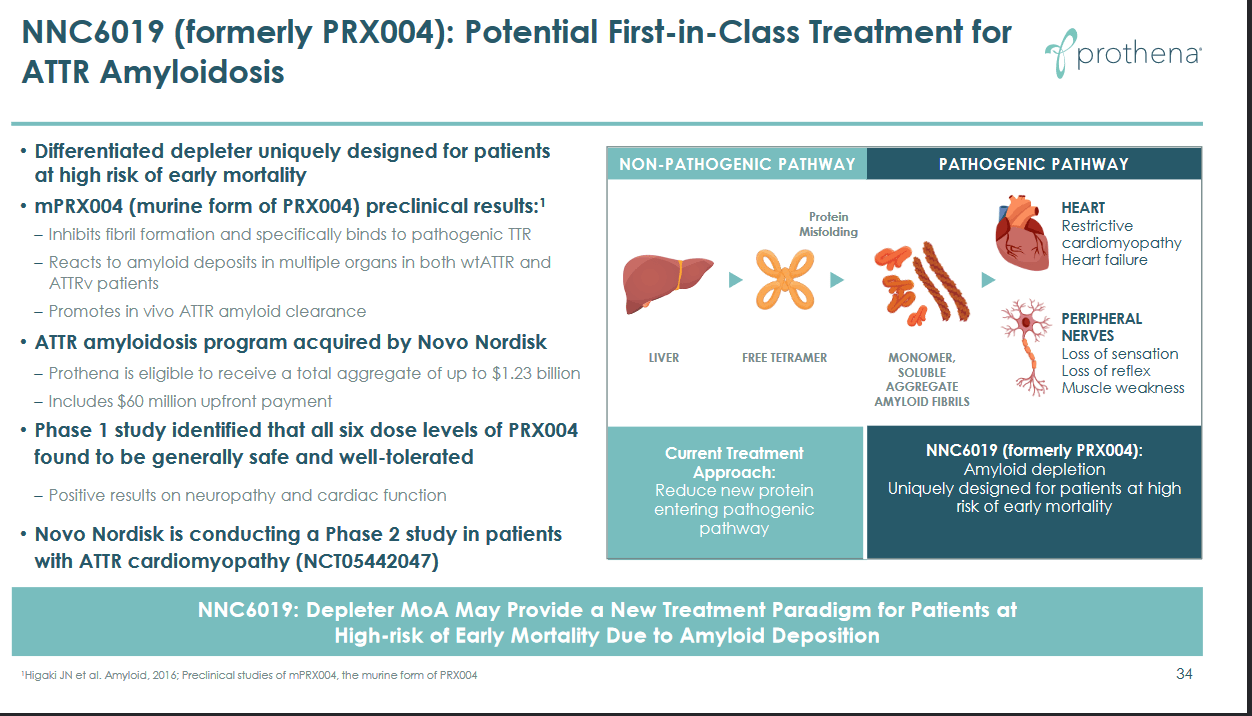

NNC6019 is Prothena's drug candidate in a Phase 2 trial for ATTR amyloidosis, which the company sold to Novo Nordisk. That Phase 2 trial is planned to investigate safety and efficacy in 99 patients over the course of 52 weeks, and was initiated in August 2022. The drug's goal is to deplete the amyloid load and thereby improve function and burden on organs, as it had shown to do in preclinical studies.

NNC6019 for ATTR amyloidosis (Corporate Presentation)

{kind=link}

The latest news here is that Prothena has now received a total of $100 million from a total of $1.2 billion which it is eligible to receive.

Financials

Prothena is well funded. The company reported a cash balance of $497 million for Q3 2022. The recent public offering may have added another $172 million.

On the other hand, its cash burn is high, with $127 million spent over the last year.

Institutional ownership is at 90.67%, and short interest is at 11.10%.

Risks

Investing in biotech companies comes with high risk, and in this case, given Prothena's high market cap, that is no different. Any trial may be halted for safety reasons or other concerns any regulatory authority may have. The competitive landscape changes constantly, and as many of Prothena's trials are still in early stages, it is unclear what it will look like by the time any of time may reach the final stages. Partnerships with large pharma may be ended, and in case of companies with a high market cap, the consequences may be dramatic as last seen with Fate Therapeutics ( FATE ). Apart from those for AL amyloidosis and ATTR amyloidosis, the drug candidates of Prothena are in a highly competitive field, and many of their predecessors have failed.

Conclusion

Prothena's pipeline has several high-value assets which may trigger several milestone payments and royalties, or may lead to substantial sales if wholly owned.

The most compelling candidate is a Phase 3 drug candidate by the name of Birtamimab, which may be a good addition to standard of care in Stage IV AL amyloidosis, if successful in a Phase 3 trial. The market should know that by 2024, or sooner if an interim analysis by the FDA's data monitoring committee would indicate so. Prothena may license or sell this drug candidate at a given point.

If one combines all of the potential milestone payments, for the entirety of Prothena's pipeline except for the wholly-owned drug candidates Birtamimab, PRX012 and PRX123, one comes to total possible milestone payments of more than $3 billion. That does not include potential royalties.

From the perspective both of Birtamimab's potential and its partnerships, Prothena has received due appreciation by the market.

However, I am surprised by the sustained market reaction in light of Eisai's news on Leqembi. That market reaction, adding $1.3 billion in one day, has been followed by a remarkable amount of insider sales. Funds have bought Prothena's shares, and institutional ownership of this stock is very high. PRX012 is an anti-amyloid antibody, many of which have failed in the past. Its high binding affinity to amyloid oligomers and fibrils may lead to efficacy in removing amyloid, but the question is how that relates to safety. The most an anti-amyloid antibody has been shown to do is moderately slow down the decline, and I do not believe much more is to be expected from this type of treatments. Commercialization is probably five to ten years away, one does not know how the competitive landscape will look by then, nor how easily these drugs can be commercialized. At this point, we only have one large commercial failure to go on by the name of Aduhelm. The share price seems to have accounted for the possibility that PRX012 will one day be bought by big pharma. If it doesn't, Prothena will have to commercialized it itself. I think holding the stock comes with a high risk that the market will start realizing it overreacted on the basis of another company's news.

For that reason, I am rating Prothena as a Sell.

For further details see:

Prothena: I'm Not A Buyer At A $3 Billion Valuation